Vehicle Security Systems Market Size, Share & Industry Analysis, By System Function (Access Control & Anti-Theft Systems, Intrusion Detection & Alarm Systems, Vehicle Immobilization Systems, Vehicle Tracking & Recovery Systems, and Vehicle Cybersecurity & Digital Protection Systems), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Sales Channel (OEM and Aftermarket), By Offering (Hardware and Software), By Propulsion (ICE and Electric), and Regional Forecast, 2026-2034

Vehicle Security Systems Market Size and Future Outlook

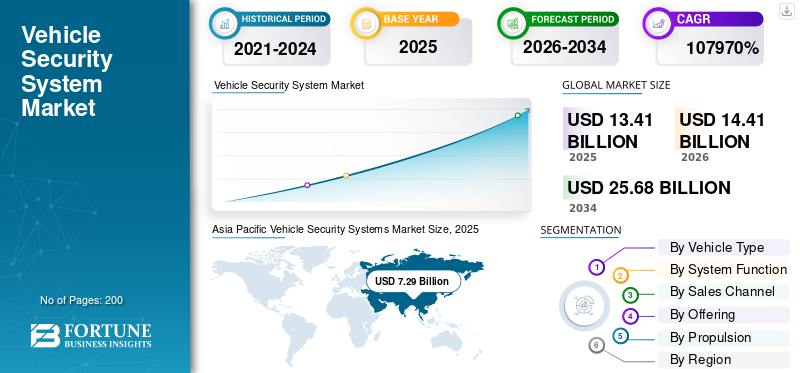

The global vehicle security systems market size was valued at USD 13.41 billion in 2025. The market is projected to grow from USD 14.41 billion in 2026 to USD 25.68 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period. Asia Pacific dominated the global vehicle security systems market with a market share of 54.36% in 2025.

Vehicle security systems are integrated automotive technologies that prevent unauthorized access, deter theft, detect intrusion, enable vehicle tracking, and protect onboard electronics through hardware, software, and connected security solutions. Key market drivers include rising vehicle thefts, stricter safety regulations, growth of connected and electric vehicles, increasing consumer awareness, expanding aftermarket demand, and rising cybersecurity threats to modern automotive systems.

Major players in the vehicle security systems market include Bosch, Continental, ZF, Valeo, and Denso, competing through advanced anti-theft technologies, connected security platforms, cybersecurity integration, and compliance-driven safety innovations.

Download Free sample to learn more about this report.

Vehicle Security Systems Market Key Takeaways

- 2025 Market Size: USD 13.41 Billion

- 2026 Market Size: USD 14.41 Billion

- 2034 Forecast Market Size: USD 25.68 Billion

- CAGR: 7.5% from 2026–2034

- Asia Pacific dominated the vehicle security systems market with a 54.36% share in 2025.

- The hatchback & sedans segment is expected to grow at a CAGR of 6.8% during the forecast period.

- The aftermarket channel segment is expected to grow at a CAGR of 6.3% during the forecast period.

Asia Pacific

Asia Pacific remained the largest regional market, supported by strong vehicle production and rising vehicle ownership.

Europe

Europe held the second-largest market share and is projected to grow at a CAGR of 7.3%.

North America

North America ranked as the third-largest market, driven by connected vehicle adoption and strong aftermarket demand.

U.S.

The vehicle security systems market is estimated at around USD 1.81 billion in 2026, accounting for approximately 12.6% of global revenue.

Japan

The vehicle security systems market is estimated at around USD 1.39 billion in 2026.

Read More

VEHICLE SECURITY SYSTEMS MARKET TRENDS

Convergence of Physical Security and Cyber Protection to Shape Market Expansion

One of the key trends in the vehicle security systems market is the convergence of traditional anti-theft hardware with cybersecurity and data protection. Modern solutions combine access control, intrusion detection, encrypted communication, and AI-based threat monitoring. This reflects growing vehicle connectivity and reliance on software-driven architectures. Moreover, trends of integrating physical and digital security are redefining product design, supplier capabilities, and competitive positioning across the automotive ecosystem.

- For instance, in January 2026, NVIDIA announced general availability of the DRIVE AGX developer kit, featuring high-performance SoCs, secure boot, hardware isolation, and AI compute to support autonomous driving, automotive cybersecurity, and security systems market, and software-defined vehicle development.

MARKET DYNAMICS

MARKET DRIVERS

Rising Vehicle Theft and Mandatory Safety Norms to Drive Market Expansion

Increasing incidents of vehicle theft across passenger and commercial vehicles are a primary growth driver of the market. Governments in many countries mandate immobilizers and access control systems in new vehicles, ensuring baseline demand. Growing consumer awareness of asset protection, higher vehicle values, and increased urban vehicle density further support adoption. OEM-fitment of security features has become a standard expectation rather than an optional add-on, sustaining long-term vehicle security system industry growth. Due to the introduction of advanced vehicle security market systems, regions and countries are witnessing a decline in vehicle theft, which enhances the vehicle security systems market demand.

- For instance, in September 2025, S. vehicle thefts dropped 23% in the first half of the year compared to 2024, with 334,114 stolen vehicles reported, reflecting improved vehicle anti-theft system market tech use, law enforcement collaboration, and advanced data analytics aiding theft prevention.

MARKET RESTRAINTS

High System Complexity and Cost Sensitivity to Limit Wider Penetration

Advanced vehicle security systems combine hardware, software, connectivity, and cybersecurity layers, increasing system complexity and overall costs. In price-sensitive markets, this restricts the adoption of premium security features beyond basic mandatory systems. Integration challenges with older vehicle platforms and limited affordability among used-vehicle owners also constrain rapid upgrades. These factors collectively slow penetration of advanced digital security solutions despite strong underlying demand fundamentals in the smart vehicle security systems industry.

MARKET OPPORTUNITIES

Software-Defined Vehicles and Subscription Models to Unlock New Revenue Streams

The transition toward software-defined vehicles presents significant vehicle security systems market opportunities. Cloud-based monitoring, over-the-air updates, and subscription-driven cybersecurity services enable recurring revenue beyond initial hardware sales. Integration with digital keys, mobile apps, and fleet management platforms expands use cases. As OEMs seek differentiation through connected services, the vehicle tracking & security systems market is increasingly positioned as value-added, monetizable features rather than standalone components.

- In January 2026, DXC Technology launched AMBER, a secure automotive software platform enabling software-defined vehicles through modular architecture, OTA updates, embedded cybersecurity controls, and lifecycle management supporting connected, electric, and autonomous vehicle ecosystems.

MARKET CHALLENGES

Rapidly Evolving Cyber Threats to Challenge Long-Term System Reliability

As vehicles become increasingly connected, security threats are evolving in complexity and frequency. Hackers continuously develop new attack vectors targeting vehicle software, communication networks, and digital access points. Ensuring long-term protection requires constant software updates, rigorous testing, and compliance with evolving regulations. Maintaining resilience against unknown threats places sustained pressure on R&D investment, response speed, and cross-industry collaboration.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

SUVs Segment Leads due to Higher Vehicle Value

Based on vehicle type, the market is segmented into hatchbacks & sedans, SUVs, LCVs, and HCVs.

The SUVs segment dominates the market due to higher vehicle value, increased theft risk, and greater integration of advanced electronic and connected features. SUVs typically adopt multi-layer intelligent vehicle security solutions, including immobilizers, intrusion alarms, tracking, and cybersecurity modules. Growing consumer preference for premium and mid-size SUVs, especially in urban and semi-urban markets, drives OEM-fitment of advanced security systems. Higher penetration of connected services and ADAS further reinforces sustained demand across both developed and emerging regions.

- In April 2025, Hyundai and Kia announced security upgrades for nearly 4 million vehicles, adding immobilizer software logic, enhanced ECU authentication, and OTA-compatible updates to address theft vulnerabilities in non-immobilized models.

The hatchback & sedans segment is the second-largest and is expected to grow at a CAGR of 6.8%. Large global vehicle parc, affordability-driven sales, and regulatory mandates for basic security systems sustain steady OEM and aftermarket demand across the global car security systems market forecast period.

By System Function

Widespread Theft Prevention Needs and Regulatory Mandates to Sustain Segment Dominance

Based on system function, the market is segmented into access control & anti-theft systems, intrusion detection & alarm systems, vehicle immobilization systems, vehicle tracking & recovery systems, vehicle cybersecurity & digital protection systems.

Access control & anti-theft systems hold the largest vehicle security systems market share due to the mandatory global vehicle immobilizer market, central locking, alarms, and keyless entry across mass-market and premium vehicles. High replacement rates, large installed base, and strong aftermarket demand ensure consistent revenues. OEM-standard fitment in passenger and commercial vehicles, coupled with rising theft incidents, sustains long-term dominance across both developed and emerging automotive markets.

Vehicle cybersecurity & digital protection systems are the fastest-growing segment, expanding at a CAGR of 10.1%. Rising vehicle connectivity, OTA updates, software-defined architectures, and increasing cyberattack risks are accelerating adoption across EVs, the connected vehicle security market, and autonomous vehicle platforms.

- For instance, in March 2024, LG Magna e-Powertrain obtained Cyber Security Management System certification, validating secure software development, encrypted communication, access control, and compliance with UNECE R155 requirements for automotive components.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Mandatory Integration and Rising Vehicle Electrification to Drive OEM Channel Dominance

By sales channel, the market is divided into OEM and aftermarket.

The OEM channel dominates and remains the fastest-growing in the market of vehicle security systems due to regulatory requirements for immobilizers and alarms, increasing vehicle connectivity, and factory-level integration of cybersecurity. OEM-fitted systems ensure seamless compatibility, software updates, and compliance. Rapid adoption of connected, electric, and software-defined vehicles further accelerates OEM demand, reinforcing long-term growth leadership.

- For instance, in November 2025, Panasonic Automotive announced enhanced in-vehicle cybersecurity solutions, integrating secure ECUs, encrypted data communication, and OTA update protection to support software-defined, connected, and electric vehicle platforms globally.

The aftermarket channel segment is expected to grow at a CAGR of 6.3%. The segmental demand is supported by vehicle parc expansion, security upgrades in older vehicles, rising theft incidents, and cost-effective retrofit solutions offered by independent installers and service centers.

By Offering

Hardware Segment Dominates due to Widespread Deployment of Immobilizers

By offering, the market is categorized into hardware and software.

The hardware segment holds the dominating share in the market of vehicle security systems due to widespread deployment of immobilizers, alarms, sensors, control units, and locking mechanisms across all vehicle categories. Mandatory fitment, frequent replacements, and a large global vehicle parc ensure consistent demand. Hardware remains foundational for both OEM and aftermarket security solutions, supporting stable revenues despite gradual shifts toward digital layers.

Software is the fastest-growing segment, expanding at a CAGR of 9.7% over the forecast period. The growth of the segment is driven by connected vehicles, OTA updates, cybersecurity needs, data analytics, and subscription-based security services integrated with cloud and mobile platforms.

- For example, in January 2026, KODA partnered with Upstream to enhance connected-vehicle cyber resilience, deploying cloud-based threat detection, real-time anomaly monitoring, and OTA security analytics to protect vehicle fleets across their entire digital lifecycle.

By Propulsion

Large Installed Vehicle Base and Slower Technology Turnover to Sustain ICE Dominance

By propulsion, the market is bifurcated into ICE and electric.

ICE vehicles hold the largest share in the market due to their vast global parc and long replacement cycles. Mandatory immobilizers, alarms, and access control systems across passenger and commercial ICE vehicles drive steady OEM and aftermarket demand. High exposure to physical theft, especially in emerging markets, sustains continued investment in conventional and connected security solutions.

Electric vehicles are the fastest-growing segment, expanding at a CAGR of 11.8%. Growth is driven by high vehicle value, software-defined architectures, constant connectivity, and heightened vulnerability to cyber threats, thereby accelerating the adoption of advanced digital and cybersecurity-focused protection systems.

- For instance, in December 2025, Autocrypt announced plans to expand electric vehicle cybersecurity technologies into the MENA region in 2026, offering V2X security, in-vehicle intrusion detection, CSMS compliance, and cloud-based threat monitoring solutions.

Vehicle Security Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Vehicle Security Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing market in the global vehicular security devices industry. The regional growth is driven by high vehicle production in China, Japan, and India, and rising vehicle ownership. Increasing theft rates, mandatory immobilizer regulations, and rapid adoption of connected vehicles support demand for car theft deterrent systems. Expanding EV penetration, growing middle-class income, and strong OEM manufacturing ecosystems accelerate integration of advanced hardware and software-based security systems across passenger and commercial vehicles.

- For instance, in January 2026, Fujitsu announced a secure mobility platform integrating AI-based threat detection, encrypted vehicle-to-cloud communication, and compliance with UNECE R155/R156 to strengthen cybersecurity for software-defined and connected vehicles globally.

China Vehicle Security Systems Market

China’s vehicle security systems market in 2026 is estimated at around USD 4.31 billion, accounting for roughly 29.9% of global revenues. China shows dominance in the Asia Pacific region, driven by rising vehicle theft, EV penetration, connected vehicles, and mandatory safety technologies.

Japan Vehicle Security Systems Market

The Japan vehicle security systems market in 2026 is estimated at around USD 1.39 billion, accounting for roughly 9.6% of global revenues. Japan’s vehicle security systems market growth is supported by advanced OEM security integration, high passenger car penetration, and strong demand for smart immobilizers.

India Vehicle Security Systems Market

The Indian vehicle security systems market in 2026 is estimated at around USD 0.69 billion, accounting for roughly 4.8% of global revenues. The market is fueled by increasing vehicle ownership, theft concerns, affordable aftermarket systems, and evolving safety regulations.

Europe

Europe holds the second-largest market share in vehicle security systems and is projected to grow at a CAGR of 7.3%. Stringent vehicle safety and cybersecurity regulations, high penetration of premium vehicles, and strong OEM focus on connected and software-defined platforms drive demand. Rising EV adoption and UNECE cybersecurity compliance requirements further boost the integration of advanced digital vehicle security solutions.

- In January 2026, EU-funded initiatives advanced automotive cybersecurity by developing intrusion detection systems, encrypted V2X communication, and AI-based threat monitoring frameworks to protect connected and autonomous vehicles across Europe.

Germany Vehicle Security Systems Market

The Germany vehicle security systems market in 2026 is estimated at around USD 0.91 billion, accounting for roughly 6.3% of global revenues. Germany market is driven by premium vehicle production, embedded OEM security features, ADAS integration, and stringent safety norms.

U.K. Vehicle Security Systems Market

The U.K. vehicle security systems market in 2026 is estimated at around USD 0.28 billion, accounting for roughly 2.0% of global revenues. The country’s market is supported by high vehicle theft rates, insurance requirements, and rising adoption of connected security solutions.

North America

North America is the third-largest market, supported by high vehicle ownership, elevated vehicle values, and strong adoption of connected and keyless entry systems. OEM-led integration of cybersecurity, growing EV sales, and rising concerns over digital vehicle theft sustain demand. A well-established aftermarket and strong presence of global Tier-1 suppliers reinforce regional market stability.

- For instance, in November 2025, Ford published a USPTO patent detailing a camera-based vehicle security system using vibration sensors, onboard processors, and event-triggered video capture to detect theft attempts and automatically activate surveillance responses.

U.S. Vehicle Security Systems Market

The U.S. vehicle security systems market in 2026 is estimated at around USD 1.81 billion, accounting for roughly 12.6% of global revenues. U.S. leads the North American market, driven by a large vehicle parc, telematics adoption, connected cars, and strong aftermarket demand.

Rest of the World

The Rest of the World region, including South America, the Middle East, and Africa, is experiencing gradual growth driven by improving vehicle safety regulations and rising urbanization. Increasing vehicle parc, theft concerns, and demand for aftermarket security upgrades support adoption. OEM localization, cost-effective hardware solutions, and expanding service networks further contribute to market development.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Connectivity, Cybersecurity Integration, and Regulatory Compliance Define Competitive Intensity

The vehicle security systems market is moderately consolidated, with global Tier-1 suppliers and specialized technology firms dominating OEM supply while regional players compete in the aftermarket. Competition is driven by connected security platforms, cybersecurity capabilities, and regulatory compliance. Leading players such as Bosch, Continental, ZF, Valeo, and Denso are focusing on integrating anti-theft hardware with software, cloud monitoring, and OTA updates. Companies pursue strategic partnerships with OEMs, cybersecurity firms, and telecom providers to enhance digital protection. Investments in R&D, platform scalability, and regional customization strengthen competitive positioning across mature and emerging automotive markets.

- For instance, in July 2025, Valeo unveiled next-generation vehicle technologies featuring secure ADAS, encrypted sensor fusion, cybersecurity-compliant ECUs, and software-defined architectures at IAA Mobility 2025.

LIST OF KEY VEHICLE SECURITY SYSTEMS COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- DENSO Corporation (Japan)

- Valeo SA (France)

- Aptiv PLC (Ireland)

- ZF Friedrichshafen AG (Germany)

- Lear Corporation (U.S.)

- NXP Semiconductors (Netherlands)

- STMicroelectronics (Switzerland)

- Thales Group (France)

- HARMAN International (U.S.)

- Visteon Corporation (U.S.)

- Vodafone Automotive (Italy)

- Spireon (U.S.)

- CalAmp Corp (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Autocrypt unveiled its Automotive-CIS global integrated cybersecurity infrastructure standard at CES 2026, unifying CSMS, SUMS, vSOC, and TARA frameworks across the full vehicle software lifecycle to support software-defined vehicles and AI mobility.

- December 2025: Siemens enhanced its PAVE360 platform with real-world validation, combining digital twins, virtual ECU testing, and cybersecurity verification to accelerate safe development of connected and autonomous vehicles.

- September 2025: Stellantis joined GlobalPlatform to strengthen vehicle cybersecurity standards, focusing on secure elements, trusted execution environments, and standardized hardware-based protection for connected and software-defined vehicle architectures.

- February 2025: Vodafone Automotive partnered with PlaxidityX to deploy cloud-based intrusion detection, telematics security, and OTA protection, safeguarding vehicles against relay attacks and modern digital theft methods.

- December 2024: Thales introduced secure contactless vehicle access solutions using encrypted digital keys, NFC, and cloud-based identity management to enhance reliability and cybersecurity for next-generation connected vehicles. This marks the company's presence in the vehicle access control systems market.

- November 2024: VicOne expanded its partner ecosystem, integrating embedded threat detection, secure boot, and real-time vulnerability monitoring to strengthen software-defined vehicle cybersecurity.

- October 2024: Panasonic announced enhanced automotive cybersecurity technologies integrating secure ECUs, encrypted in-vehicle networks, hardware-based authentication, and OTA software protection to support connected, electric, and software-defined vehicle platforms.

- October 2022: Denso announced automotive cybersecurity initiatives focused on secure ECUs, intrusion detection systems, encrypted vehicle networks, and compliance with global CSMS regulations for connected vehicle safety.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By System Function, By Sales Channel, By Offering, By Propulsion, and By Region |

|

By Vehicle Type |

|

|

By System Function |

|

|

By Sales Channel |

|

|

By Offering |

|

|

By Propulsion |

|

|

By Geography |

North America (By Vehicle Type, By System Function, By Sales Channel, By Offering, By Propulsion, and By Country) o U.S. o Canada o Mexico Europe (By Vehicle Type, By System Function, By Sales Channel, By Offering, By Propulsion, and By Country) o Germany o U.K. o France o Rest of Europe Asia Pacific (By Vehicle Type, By System Function, By Sales Channel, By Offering, By Propulsion, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific Rest of the World (By Vehicle Type, By System Function, By Sales Channel, By Offering, and By Propulsion) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 13.41 billion in 2025 and is projected to reach USD 25.68 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 7.29 billion.

The market is expected to exhibit a CAGR of 7.5% during the forecast period (2026-2034).

The SUVs segment leads the market in terms of vehicle type.

Rising vehicle theft and mandatory safety norms are the key factors driving market expansion.

Key players in the market include Bosch, Continental, ZF, Valeo, and Denso.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us