Vertiports Market Size, Share, and Industry Analysis, By Type (Vertihubs, Vertibases, and Vertipads), By Solution (Landing Pads, Terminal Gates, Ground Support Equipment, Charging Stations, Ground Control Stations, and Others), By Location (Ground Based, Rooftop and Elevated, and Floating), By Topology (Single, Linear, Satellite, and Pier), By Landscape (Urban Vertiports and Regional Vertiports), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

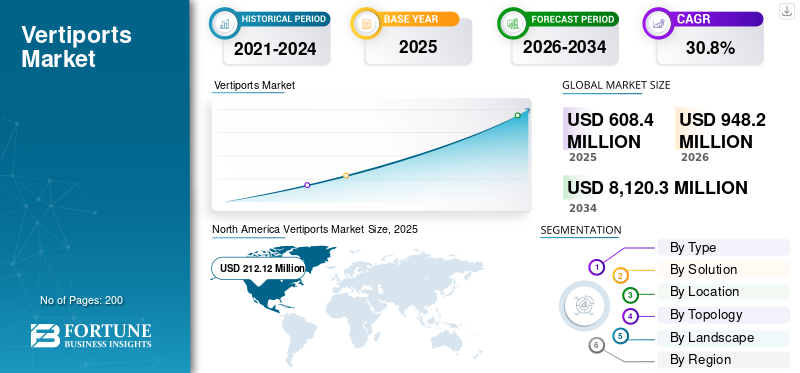

The global vertiports market size was valued at USD 608.4 million in 2025. The market is projected to grow from USD 948.2 million in 2026 to USD 8,120.3 million by 2034, exhibiting a CAGR of 30.8% during the forecast period. North America dominated the vertiports market with a market share of 34.86% in 2025.

The vertiports market is rapidly emerging as a critical infrastructure segment within the Urban Air Mobility (UAM) ecosystem, driven by the growing adoption of electric vertical takeoff and landing (eVTOL) vehicles for passenger, cargo, and emergency applications. Vertiports serve as specialized hubs for eVTOL operations, encompassing landing and takeoff pads, maintenance facilities, charging stations, and passenger terminals. The integration of vertiports with existing transport networks is essential to address urban congestion, reduce travel times, and support sustainable city mobility solutions. Technological advancements in automated air traffic management and battery charging infrastructure further accelerate the market’s growth. Key growth regions include Asia Pacific, especially China and India, with rapid urbanization and smart city initiatives fostering investment and deployment of vertiports. Developed regions such as North America and Europe focus on regulatory frameworks and integration challenges.

Key players driving this transformation include Varon Vehicles Corporation, Groupe ADP, Lilium, Bayards Vertiports, Vports, Aeroauto, Urban-Air Port Limited, UrbanV, SKYPORTS INFRASTRUCTURE LIMITED, and Volocopter GmbH. These companies are innovating in vertiport design, construction, and operations to meet rising demand and support eVTOL commercialization.

Download Free sample to learn more about this report.

Vertiports Market Key Takeaways

- 2025 Market Size: USD 608.4 million

- 2026 Market Size: USD 948.2 million

- 2034 Forecast Market Size: USD 8,120.3 million

- CAGR: 30.8% from 2026–2034

- North America dominated the vertiports market with a market share of 34.86% in 2025.

- Vertipads led the infrastructure segment with an anticipated 43.30% share in 2026.

- The single-site configuration segment is expected to dominate with a 45.77% share in 2026.

North America

North America held the dominant share in 2024, valued at USD 126.48 million, and also took the leading share in 2025 with USD 212.12 million. Airport connectors and FBO-adjacent sites drive early demand, underpinned by mature standards and deep infrastructure capital.

Europe

Europe is projected to grow at 30.7%, reaching USD 294.5 million in 2026, reflecting accelerating investment in urban air mobility infrastructure.

Asia Pacific

Asia Pacific is estimated to reach USD 281.7 million by 2026, driven by tourism corridors, new-town developments, and expanding airport connector networks.

U.S.

The market is estimated to reach USD 284.8 million in 2026, with demand concentrated in Tier-1 metros featuring high airport traffic, dense CBDs, and supportive utility infrastructure.

Japan

Japan is expected to witness growing opportunities driven by the development of advanced air mobility infrastructure and urban air transportation initiatives.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Urban Congestion Solutions and eVTOL Adoption are Boosting Market Growth

A primary driver of the vertiports market growth is the urgent global need to address urban congestion and inefficiencies in ground transport. Electric VTOL aircraft offer promising alternatives that can bypass traffic snarls and reduce travel time, particularly in megacities. This enlarges demand for dedicated vertiport infrastructure to facilitate frequent, efficient passenger and cargo transfers. Technological improvements in eVTOL safety, battery charging, and airspace management have made vertiports more viable operationally and commercially. Moreover, growing government policies prioritizing clean, sustainable transportation strengthen the impetus for vertiport networks as essential urban mobility components.

MARKET RESTRAINTS

High Initial Costs and Regulatory Complexity to Hamper Market Growth

Despite its promise, the vertiports market faces significant restraints from the high capital expenditures required for land acquisition, advanced technological systems, and specialized construction. Urban real estate costs further escalate initial investments. Additionally, the regulatory landscape for vertiports remains fragmented and nascent, with complex zoning, aviation, and safety regulations that vary by region. This causes delays, increased costs, and uncertainty for developers and operators. Coordination among multiple government agencies and alignment with existing airspace management and transport infrastructure impose further challenges. Such barriers slow deployment and may constrain market scalability.

VERTIPORTS MARKET TRENDS

Technological Innovation and Urban Integration Driving Rapid Expansion

The vertiports market is rapidly evolving due to significant technological advancements and growing urban air mobility (UAM) adoption. Vertiports, as specialized infrastructure for electric vertical takeoff and landing (eVTOL) vehicles, are becoming integral to urban transport, cargo, and emergency services. Advances in automation, robotics, and charging infrastructure are transforming vertiports into highly efficient, smart hubs that streamline passenger handling and aircraft operations. Increasing investments focus on integrating vertiports within existing transport networks and urban landscapes to solve traffic congestion and enable sustainable aerial mobility. Modular and scalable designs are becoming more prevalent, supporting rapid deployment in both dense urban centers and suburban areas. This trend aligns with broader smart city developments, emphasizing seamless connectivity, environmental sustainability, and enhanced passenger experience, accelerating vertiport market growth globally.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

Multi-Use Infrastructure and Strategic Urban Development to Accentuate Market Growth

Vertiports present a unique growth opportunity as they evolve beyond simple landing zones into multi-functional complexes combining passenger terminals, cargo handling, maintenance, and charging facilities. Governments and private stakeholders are collaborating to embed vertiports into urban planning, especially as cities seek innovative solutions to congestion and pollution. The opportunity expands with the integration of vertiports near airports, train stations, and commercial hubs, enabling multi-modal transport networks. Emerging economies such as China and India offer especially strong potential owing to rapid urbanization and large-scale smart city initiatives. Infrastructure providers and technology firms can leverage partnerships and public-private models to capture first-mover advantage. Vertiports also open avenues for diversified revenue streams through retail services, logistics, and specialized urban air mobility programs.

MARKET CHALLENGES

Safety, Standardization, and Public Acceptance are Major Challenges in Market

Key challenges include ensuring robust safety and air traffic integration for eVTOL operations amid growing urban complexity. Vertiports must meet rigorous standards for noise management, emergency response, cybersecurity, and operational reliability. The lack of globally harmonized regulations complicates consistent vertiport development. Public acceptance is critical and hinges on addressing concerns related to noise pollution, visual impact, and safety perceptions. Urban planners and operators must navigate these socio-technical issues while maintaining efficient, seamless operations. Developing interoperable systems and community engagement remain essential for widespread adoption.

SEGMENTATION ANALYSIS

By Type

Vertipads Led Market Due to Their Adaptability and Space Efficiency in Urban Environments

By type, the market is segmented into vertihubs, vertibases, and vertipads.

The vertipads segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 43.30% share. Vertipads are in demand due to their adaptability in urban environments, enabling easy installation on rooftops and constrained spaces to support last-mile connections and efficient electric vertical aircraft operations.

The vertihubs segment is expected to grow at a CAGR of 31.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Solution

Increasing Volume of eVTOL Flights Boosted Demand for Landing Pads

By solution, the market is classified into landing pads, terminal gates, ground support equipment, charging stations, ground control stations, and others.

The landing pads segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 28.73% share. Landing pads are essential for managing the increasing volume of eVTOL flights, ensuring safe landings and takeoffs within crowded cityscapes, and offering modular solutions for scalable urban deployment.

The charging stations segment is expected to grow at a CAGR of 32.3% over the forecast period.

By Location

Ground Based Segment Dominated Market Due to Its Cost-Efficiency and Capacity to Handle Higher Traffic Volumes

By location, the market is classified into ground based, rooftop and elevated, and floating.

The ground based segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 56.19% share. Ground-based vertiports are sought after for their lower costs, ease of integration with existing surface transport infrastructure, and ability to handle higher traffic volumes, making them ideal for both urban and suburban deployments.

The rooftop and elevated segment is expected to grow at a CAGR of 31.2% over the forecast period.

By Topology

Simplicity and Cost-Effectiveness Fueled Single Topology Vertiport Adoption

By topology, the market is classified into single, linear, satellite, and pier.

The single segment captured the largest vertiports market share in 2025. In 2026, the segment is anticipated to dominate with a 45.77% share. Single topology vertiports, featuring a single landing/takeoff zone, are preferred in smaller cities or low-demand locations due to their straightforward design, reduced costs, and simpler regulatory requirements, facilitating faster deployment.

The satellite segment is expected to grow at a CAGR of 31.9% over the forecast period.

By Landscape

Addressing Urban Congestion and Aerial Mobility Needs Spurred Urban Vertiports Segment Growth

By landscape, the market is classified into urban vertiports and regional vertiports.

The urban vertiports segment captured the largest market share in 2025. In 2026, the segment is anticipated to dominate with a 75.23% share. Urban vertiports are in demand primarily as they directly respond to urban congestion issues by providing efficient aerial transport hubs that support rapid passenger and cargo movement within cities, aligned with smart city mobility frameworks.

The regional vertiports segment is expected to grow at a CAGR of 30.3% over the forecast period.

VERTIPORTS MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Vertiports Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 126.48 million, and also took the leading share in 2025 with USD 212.12 million. Airport connectors and FBO-adjacent sites drive early demand, underpinned by mature standards and deep infrastructure capital. Corporate travel, tourism, and medical missions create dependable flows. Rooftop retrofits in dense downtown areas are gathering pace, while power upgrades and community engagement determine the cadence of multi-pad hub deployments.

In 2026, the U.S. market is estimated to reach USD 284.8 million. U.S. demand clusters around Tier-1 metros with strong airport traffic, dense CBDs, and supportive utilities. FBO partnerships, corporate shuttles, and medical logistics underpin early utilization, while rooftop retrofits and energy upgrades unlock multi-pad operations in high-value corridors.

Europe

During the forecast period, the European region is projected to record a growth rate of 30.7% and touch the valuation of USD 294.5 million by 2026. City-region planning and intermodal thinking concentrate demand around airports, rail nodes, and river sites. Showcase routes catalyze investment, especially where tourism and business travel overlap. Harmonized safety guidance supports rooftop and historic district sensitivity, with a strong emphasis on noise compliance and public interest operations, such as medical logistics.

Asia Pacific

The market in Asia Pacific is estimated to reach USD 281.7 million by 2026. Tourism corridors, new-town developments, and airport connectors generate step-function demand. Governments use pilot corridors to de-risk wider rollouts, while megacity rooftops unlock premium catchments. Domestic OEMs and tech ecosystems accelerate adoption, though power reliability and typhoon/monsoon operating envelopes shape design and scheduling.

Rest of the World

The rest of the world market is expected to reach a valuation of USD 42.3 million by 2026. Select city-states and tourism hubs spearhead demand via government-backed networks and exclusive concessions. Airport-city connectors and waterfront sites lead. Financing often blends public funds with strategic airline or developer capital, while environmental approvals and grid constraints define how quickly capacity scales beyond initial nodes.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Product Innovation, Partnerships, and Urban Integration by Key Players to Boost Market Revenue

These key players are growing rapidly by advancing innovative vertiport designs, forming strategic partnerships, and aligning with urban air mobility frameworks. Varon Vehicles and Lilium focus on integrating vehicle and infrastructure technologies for seamless operations, while Groupe ADP and Urban-Air Port Limited leverage airport and urban infrastructure expertise for scalable vertiport deployments. Bayards Vertiports and SKYPORTS specialize in modular and sustainable vertiport construction. Volocopter GmbH leads in operational pilots and commercial eVTOL services. Collaborative ecosystems and government backing support their expansion, ensuring adaptability to regulatory environments and urban planning needs. This collective growth is accelerating the adoption of vertiports globally, positioning these companies as pivotal forces shaping the aerial mobility future.

LIST OF KEY VERTIPORT COMPANIES PROFILED

- Varon Vehicles Corporation (U.S.)

- Groupe ADP (France)

- LILIUM (Germany)

- Bayards Vertiports (Netherlands)

- Vports (Canada)

- Aeroauto (U.S.)

- Urban-Air Port Limited (U.K.)

- UrbanV (Italy)

- SKYPORTS INFRASTRUCTURE LIMITED (U.K.)

- Volocopter GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- June 2025 - UrbanV and Signature Aviation announced a joint venture aimed at accelerating vertiport network development across the U.S., with initial focus on Florida, New York, California, and Texas. The partners plan to leverage Signature’s nationwide FBO footprint and UrbanV’s AAM infrastructure know-how to fast-track site selection and deployment.

- November 2024 - EHang signed a Memorandum of Understanding with Vertiports Network during the Smart City Expo & Tomorrow Mobility World Congress. The agreement frames collaboration on an Advanced Air Mobility (AAM) ecosystem, combining EHang’s eVTOL expertise with Vertiports Network’s modular vertiport design and network operations capabilities.

- June 2024 – Skyports Infrastructure and Jeju Air signed a partnership to advance vertiport deployment for air-taxi services in Korea. Formalized at a signing ceremony in Gimpo City, the agreement combines Skyports’ vertiport development capabilities with Jeju Air’s operational expertise to accelerate a nationwide AAM network.

- June 2023 - UrbanV and SITA entered a Memorandum of Understanding to deliver integrated digital solutions for passenger processing, operations, and turnaround management at UrbanV’s Rome vertiports, slated to begin operations in 2024. The MoU also covers joint exploration of similar deployments for vertiports in other global markets.

- March 2023 - Eve Air Mobility signed a Letter of Intent with Ferrovial Vertiports to evaluate Eve’s Urban Air Traffic Management (Urban ATM) software for vertiport and eVTOL operations. The collaboration will assess how Urban ATM can support safe, reliable, and scalable traffic management across Ferrovial’s planned vertiport network.

REPORT COVERAGE

The vertiports market report delivers a focused deep dive on the ecosystem profiling, leading infrastructure developers and operators, core components (pads, charging, control systems, passenger processing), and the primary use cases spanning urban air mobility and regional links. It maps the policy milestones, pilot programs, and network build-outs now underway, and highlights the shifts shaping the next wave of deployments. Together, these insights explain the rapid acceleration in recent years and the factors set to drive market growth in the coming years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 30.8% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Type · Vertihubs · Vertibases · Vertipads |

|

By Solution · Landing Pads · Terminal Gates · Ground Support Equipment · Charging Stations · Ground Control Stations · Others |

|

|

By Location · Ground Based · Rooftop and Elevated · Floating |

|

|

By Topology · Single · Linear · Satellite · Pier |

|

|

By Landscape · Urban Vertiports · Regional Vertiports |

|

|

By Region · North America (By Type, Solution, Location, Topology, Landscape, and Country) o U.S. (By Landscape) o Canada (By Landscape) · Europe (By Type, Solution, Location, Topology, Landscape, and Country) o U.K. (By Landscape) o Germany (By Landscape) o France (By Landscape) o Russia (By Landscape) o Rest of Europe (By Landscape) · Asia Pacific (By Type, Solution, Location, Topology, Landscape, and Country) o China (By Landscape) o Japan (By Landscape) o India (By Landscape) o Rest of Asia Pacific (By Landscape) · Rest of the World (By Type, Solution, Location, Topology, Landscape, and Sub-Region) o Middle East and Africa (By Landscape) o Latin America (By Landscape) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 608.4 million in 2025 and is estimated to reach USD 8,120.3 million by 2034.

The market is growing at a CAGR of 30.8% during the projection period (2026-2034).

By type, the vertipads segment led the global market.

By topology, the single segment dominated the market.

Varon Vehicles Corporation, Groupe ADP, LILIUM, Bayards Vertiports, Vports, and Aeroauto are some of the leading OEMs in the market.

North America held the highest market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us