Vials Packaging Market Size, Share & Industry Analysis, By Material (Glass, Plastic, Cyclic Olefin Copolymer, and Cyclic Olefin Polymer), By Capacity (Up to 10 ml, 11-50 ml, 51-100 ml, and Above 100 ml), By Application (Healthcare, Food & Beverages, Cosmetics, Chemicals, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

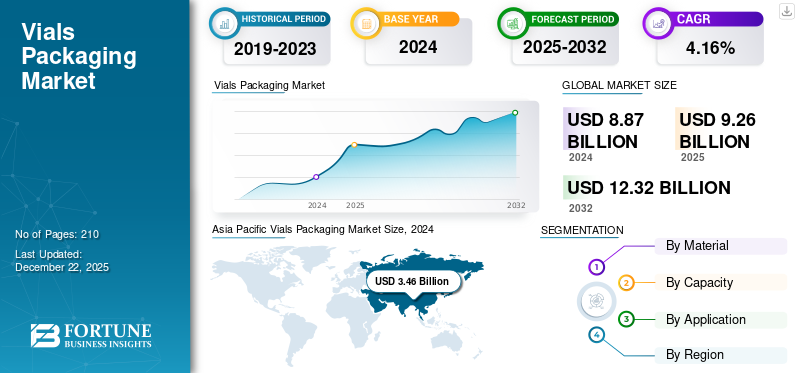

The global vials packaging market size was valued at USD 9.26 billion in 2025 and is projected to grow from USD 9.66 billion in 2026 to USD 13.12 billion by 2034, exhibiting a CAGR of 3.91% during the forecast period. Asia Pacific dominated the vials packaging market with a market share of 39.01% in 2024.

The vials packaging market is an integral segment of the pharmaceutical packaging industry, primarily focused on packaging solutions for injectable drugs, vaccines, biologics, and diagnostic products. Vials serve as containers that ensure drug safety, sterility, and ease of administration. The global market has witnessed substantial growth, largely driven by the high demand for injectable pharmaceuticals and expanding vaccine production globally.

Vials have been vital to various industries for centuries, acting as basic yet crucial instruments in numerous uses. Due to their versatility, these compact containers have made their presence known in laboratories, pharmacies, and cosmetic sand food sectors. Specifically, small plastic containers are gaining popularity for their low cost and ease of use, increasingly appearing in multiple industries. The rising environmental concerns and growing recycling rates of glass material drive the global market growth.

- Environmental Engineering Research states that the worldwide glass recycling rate is projected to be merely 21% of all glass manufactured, with container glass attaining the highest recycling rate at around 32%. Conversely, the recycling rate for flat glass is considerably lower, around 11%.

- In 2022, North America and Europe represent 29% and 27% of the worldwide glass packaging market market share, respectively, and possess advanced recycling programs and infrastructure compared to other areas.

Schott AG and SGD Pharma are the leading manufacturers, accounting for the largest global market share.

Download Free sample to learn more about this report.

Vials Packaging MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 9.26 billion

- 2026 Market Size: USD 9.66 billion

- 2034 Forecast Market Size: USD 13.12 billion

- CAGR: 3.91% from 2026–2034

- Asia Pacific dominated the vials packaging market with a 39.01% share in 2024.

- Glass segment held the largest share due to high chemical resistance and strong barrier properties.

- Up to 10 ml capacity segment dominated due to high demand in vaccines and injectable drugs.

North American

North America shows steady growth driven by biologics, specialty drugs, and advanced packaging demand.

Europe

Europe is supported by strong glass recycling systems and sustainability-driven packaging adoption.

Asia Pacific

Asia Pacific leads the market due to strong pharmaceutical manufacturing and healthcare expansion.

U.S.

Growth driven by rising demand for biologics, biosimilars, and injectable drug packaging.

Japan

Stable demand supported by advanced healthcare infrastructure and pharmaceutical production.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand from the Pharmaceutical Sector Drives Market Growth

A prominent industry where vials are widely utilized is the pharmaceutical sector. Vials act as the main packaging for various medications, including liquid suspensions, powders, and solid pills. The distinct features of vials, such as their ability to seal hermetically and their small dimensions, render them perfect for maintaining the efficacy and integrity of medications. The market is experiencing significant growth due to the rising demand in the pharmaceutical sector, especially for injectable drugs and biologics. The rising prevalence of chronic diseases such as cancer, diabetes, and autoimmune disorders is propelling demand for pharmaceutical glass packaging and injectable biologic therapies, which require secure vial packaging.

The demand for vials is growing rapidly as they hold the medications and guarantee their safety and effectiveness. Furthermore, heightened emphasis on vaccination initiatives has significantly boosted the use of vials for storing and distributing vaccines. Moreover, advancements in vial design, such as innovative glass formulations and tamper-evident features, enhance the popularity of vials.

- According to the European Federation of Pharmaceutical Industries and Associations, the research-driven pharmaceutical industry can significantly contribute to reviving Europe's growth and securing its future competitiveness in a progressing global economy. In 2023, it invested approximately USD 55,540 million in R&D in Europe.

- In 2023, North America represented 53.3% of global pharmaceutical sales, while Europe accounted for 22.7%. As per IQVIA (MIDAS May 2024), 67.1% of the sales from new medications introduced between 2018 and 2023 occurred in the U.S. market, while 15.8% took place in the European market.

MARKET RESTRAINTS

Several Regulatory Compliances Hampers the Market Expansion

The pharmaceutical and medical sectors implement some of the strictest packaging rules. Vials intended for medications, vaccines, and biologics must adhere to stringent standards for sterilization, leak resistance, and compatibility with their contents (e.g., avoiding interactions between the drug and the vial material). Regions such as the EU, U.S., and Asia exhibit diverse packaging standards and requirements. Staying abreast of regulatory shifts in various markets poses a significant challenge for businesses seeking to uphold a global footprint, thus hampering vials packaging market growth.

- The U.S. Food and Drug Administration (FDA) released updated Guidance on Container Closure Systems and Component Changes for Glass Vials and Stoppers, offering drug manufacturers advice on reporting and executing various standard alterations to packaging market systems that include glass vials and stoppers.

MARKET OPPORTUNITIES

Growing Emphasis on Sustainable and Eco-friendly Materials Will Offer Potential Growth Opportunities

There is an increasing focus on environmentally friendly packaging options as consumers and regulators push for less plastic use and greater recyclability. This provides manufacturers with the opportunity to innovate and develop sustainable vials, including those constructed from recycled glass, bio-based plastics, or plant-derived materials. The shift toward a circular economy offers manufacturers chances to create vials that are easier to reuse or recycle. Manufacturers focusing on designing returnable vial systems or single-material vials (such as recyclable plastic or glass) can benefit from this trend. Henceforth, increasing emphasis on sustainable and eco-friendly packaging materials by consumers and manufacturers will offer potential growth opportunities.

- The Plastic Industry Association states that a global consumer survey from 2023 revealed that 80% of respondents are ready to spend extra on products that are sustainably sourced, indicating the growing significance of plastic sustainability in purchasing choices.

VIALS PACKAGING MARKET TRENDS

Innovative Developments and Advanced Vial Designs Emerge as a Key Trend

Vials are seeing a surge in demand and innovative advancements, especially within the pharmaceutical and healthcare sectors, with an emphasis on sustainability, quality, and safety. Notable trends include a move towards eco-friendly materials, innovative vial designs aimed at improving product safety and user convenience, and the integration of technology to enhance production and quality control processes. Although glass continues to be a leading choice, ongoing research, and development are investigating alternatives such as bio-based plastics for certain vial uses. The creation of break-resistant vials is boosting reliability and consumer confidence, especially regarding handling and transportation. Manufacturers are looking into specialized coatings and sealants to improve vial performance, including lyophilization-compatible vials and coatings that safeguard sensitive biologics, thus emerging as a significant trend for market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Significant Benefits Offered Boosts the Segmental Growth of Glass

Based on material, the market is divided into glass, plastic, cyclic olefin copolymer, and cyclic olefin polymer.

The glass segment accounted for the larger share of the market in 2024. Glass is frequently favored because of its natural characteristics that enable easy sterilization and visibility of what's inside. Glass vials are commonly utilized for packaging generic parenteral medications because of their chemical resistance, which reduces interaction between the drug and its container, thereby maintaining the therapeutic efficacy of the stored medications. Glass vials are notably robust and impermeable. Glass remains the most dominant packaging material due to its excellent chemical inertness, barrier properties, and compatibility with a wide range of pharmaceutical products, particularly injectable drugs. Borosilicate glass is commonly used for its thermal resistance and durability.

Plastic material is the second-dominating segment of the market. Plastic vials provide numerous benefits compared to glass vials, such as safety, durability, resistance to chemicals, and cost-effectiveness. They are break-resistant, light-in-weight, and can be easily moved and managed. Moreover, plastic vials can be manufactured in different shapes and sizes, which makes them ideal for numerous uses. Plastic vials are gaining traction due to their lightweight, lower manufacturing costs, and resistance to breakage.

By Capacity

Rising Utilization of Up to 10 ml in the Pharmaceutical Sector Drives Segmental Growth

Based on capacity, the market is divided into up to 10 ml, 11-50 ml, 51-100 ml, and above 100 ml.

Up to 10 ml segment accounted for the larger vials packaging market share in 2024. The segment’s growth is mainly fueled by the growing need for vaccines and biologics, especially within the pharmaceutical sector. These compact containers are perfect for single-use applications, guaranteeing sterility and minimizing contamination risks. Moreover, the increase in chronic conditions requiring injectable treatments greatly enhances the demand for capacity. This is the most commonly used size, especially for vaccines, insulin, and other injectables requiring small doses. It holds the largest market share due to the rise in vaccine demand and biologics administered in small quantities.

51-100 ml is the second-leading capacity segment of the market. The increasing need for multi-dose formulations in the pharmaceutical sector aids the expansion of this segment. Larger vials are less common but used for storage and bulk drug packaging in pharmaceutical manufacturing. The growth of this segment is tied closely to production scale rather than end-user consumption.

By Application

Rising Demand from the Healthcare Sector Drives the Segment’s Growth

Based on application, the market is segmented into healthcare, food & beverages, cosmetics, chemicals, and others.

The healthcare segment dominated the market in 2024. Vials serve an essential function in the healthcare sector by ensuring secure and dependable storage and management of drugs, samples, and reagents. They provide various advantages, such as shielding against external factors such as air, humidity, and light, which can diminish the quality of medications. Vials also enable careful examination of the contents and guarantee uniform chemical interaction with the medication because of their consistent wall thickness. The increasing demand for vials from the healthcare sector enhances segmental growth.

On the other hand, the cosmetics segment is expected to witness steady growth during the forecast period. Vials offer a perfect solution for packaging a range of cosmetic items, from fragrances to skin serums. The clear quality of glass and plastic vials enables consumers to view the color and texture of the product within, which can be an essential marketing advantage.

Vials Packaging Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Vials Packaging Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominates the global market. The swift expansion can be linked to glass manufacturing operations and heightened usage in the healthcare, food & beverages, and cosmetics sectors. The swiftly expanding healthcare and cosmetic sectors are anticipated to drive the demand in the Asia Pacific region. This is due to the rapid expansion of the pharmaceutical manufacturing hubs in China and India, increasing healthcare spending, rising chronic disease burden, and improving cold chain infrastructure. Moreover, the rising embrace of luxury brands is persistently developing creative packaging to capture consumers' interest, contributing to the market expansion in the Asia Pacific region. The well-established pharmaceutical sector in major countries also drives market growth.

- The Press Information Bureau (PIB) states that India's pharmaceutical sector for FY 2023-24 was estimated at USD 50 billion, with domestic usage at USD 23.5 billion and exports at USD 26.5 billion. India's pharmaceutical sector is regarded as the third largest globally by volume and ranks 14th for production value.

North America

North America is the second-largest market. Major producers in various sectors are establishing a foundation for advancement by utilizing sustainable packaging, and glass serves as a superb packaging option. In an effort to rival global manufacturing centers such as China and Japan, North America has been working to innovate and embrace glass packaging. The rising demand for specialty drugs, biosimilars, and biologics, along with an increase in personalized medicine and targeted therapies, cushions the demand for vials in the U.S. The rapidly growing food and beverage sector in the North American region also cushions the market growth.

- The Unifor Organization states that in terms of production value, the food and beverage sector ranks as the second largest manufacturing industry in Canada, with total sales approaching USD 118 billion in 2019. In 2021, the sector added USD 34.5 billion to the national Gross Domestic Product (GDP), representing almost 2% of the overall GDP. The food and beverage sector is the biggest employer in Canada’s manufacturing industry, offering jobs to over 300,000 Canadians.

Europe

Europe is a significant market for vial packaging. The recycling of glass is quickly rising in the region, particularly in developed countries. Europe excelled in recycling by achieving the highest recycling rates, which, in turn, enhances the utilization of glass vials in the region.

- According to the FEVE- The European Container Glass Federation, the EU average collection of glass packaging for recycling was 80.1% in 2021. The multi-stakeholder collaboration Close the Glass Loop seeks to achieve a post-consumer glass container collection goal of 90% by 2030, ensuring it is recycled for use in container glass production.

Latin America

Latin America region is expected to observe considerable growth. The significant healthcare expenditure in the major parts of the Latin American region has led to increased demand for advanced sterilization devices in hospitals and medical facilities. Likewise, the booming medical tourism sector, coupled with the availability of affordable advanced sterilization tools, significantly expands the market reach in Brazil, increasing the demand for vials in this region.

Latin America

Middle East & Africa region will experience moderate growth in the forthcoming years. The pharmaceutical industry in the Middle East and Africa region is experiencing significant growth, driven by a combination of factors including a growing and aging population, increasing prevalence of chronic diseases, and rising healthcare expenditure. It thus boosts demand for vials.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Development and Introduction of New Products by Key Companies Resulted in Their Dominating Positions

The global vials packaging market is concentrated with companies such as Schott AG, SGD Pharma, Gerresheimer AG, West Pharmaceutical Services Inc., DWK Life Science Inc., and Sigma-Aldrich Co. LLC, accounting for a significant share.

Schott AG is a German technology group and a premier company in specialty glass and material technology, established by Otto Schott. They create, produce, and sell a variety of specialized glass, glass ceramics, and materials for various industries. Employing more than 17,100 people worldwide, Schott is active in multiple industries, such as home appliances, automotive, electronics, pharmaceuticals, and others.

SGD Pharma is a global leader in pharmaceutical glass primary packaging, providing a diverse selection of vials, ampoules, bottles, and additional products in Type I, II, and III glass. The firm runs five production facilities in Europe and Asia, generating more than 2 billion vials each year.

Additionally, Gerresheimer AG and West Pharmaceutical Services Inc. are among the other prominent players in the market. Focus on significant investments in the research & development of innovative products has supported the pharmaceutical companies' share in the market.

- In November 2022, Gerresheimer AG and Stevanato Group S.p.A., a worldwide provider of drug containment, drug delivery, and diagnostic solutions for the pharmaceutical, biotechnology, and life sciences sectors, announced at CPhl Worldwide the official introduction of a novel and innovative ready-to-use (RTU) vial platform, EZ-fill Smart, aimed at enhancing drug packaging quality, lowering total cost of ownership (TCO), and reducing lead times for clients.

LIST OF KEY VIALS PACKAGING COMPANIES PROFILED

- Schott AG (Germany)

- SGD Pharma (France)

- Gerresheimer AG (Germany)

- West Pharmaceutical Services Inc. (U.S.)

- DWK Life Science Inc. (Germany)

- Sigma-Aldrich Co. LLC (U.S.)

- AptarGroup, Inc. (U.S.)

- Jarsking Group (U.S.)

- Nipro Corporation (Japan)

- Tekniplex (U.S.)

- Corning Incorporated (U.S.)

- Adelphi Healthcare Packaging (U.K.)

- Phoenix Glass Inc. (U.S.)

- Pacific Vial Manufacturing Inc. (U.S.)

- Origin Pharma Packaging (U.K.)

KEY INDUSTRY DEVELOPMENTS

- October 2024: Nipro PharmaPackaging revealed the introduction of its novel D2F (Direct-to-Fill) glass vials, utilizing Stevanato Group’s cutting-edge EZ-fill technology, providing a premium ready-to-use (RTU) option. D2F glass vials undergo washing, depyrogenation, packaging in nest and tub formats, and sterilization, delivering a seamless RTU solution.

- February 2024: SGD Pharma introduced a new collection of Type I injectable vials made from tubular glass. The updated vials showcase a newly developed external low-friction coating by Corning. SGD Pharma’s expertise in vial conversion is paired with Corning’s unique glass-coating technology to enhance productivity on pharmaceutical filling lines and accelerate the worldwide distribution of injectable therapies.

- January 2024: SCHOTT Pharma introduced new vials for mRNA and gene treatments. EVERIC freeze vials can endure storage temperatures as low as -80°C, which is essential for vaccines, including gene therapy and mRNA medicines. These new vials help prevent the loss of critical medications and expensive downtimes due to their strength-optimized design that minimizes the risk of breakage.

- October 2023: SCHOTT launched advanced type I borosilicate glass tubing to fulfill upcoming demands of the pharmaceutical sector. The product and associated services will bolster three key industry trends: the growth of intricate pharmaceuticals, sustainability, and digital transformation.

- September 2023: Corning Inc. introduced Corning Viridian Vials, broadening its range of pharmaceutical glass-packaging offerings. Viridian Vials aim to enhance filling-line efficiency by as much as 50% and decrease vial-manufacturing carbon-dioxide-equivalent (CO2e) emissions by up to 30%.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.91% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Capacity

|

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.66 billion in 2026 and is projected to record a valuation of USD 13.12 billion by 2034.

In 2024, the market value stood at USD 3.46 billion.

The market is expected to grow at a CAGR of 3.91% during the forecast period.

The healthcare segment led the market, by application.

The key factor driving the market is the increasing demand from the pharmaceutical sector.

Schott AG, SGD Pharma, Gerresheimer AG, West Pharmaceutical Services Inc., DWK Life Science Inc., and Sigma-Aldrich Co. LLC are the top players in the market.

Asia Pacific dominated the market in 2025.

Increased demand from the healthcare and cosmetic industries is one of the factors that are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us