Biolubricants Market Size, Share & Industry Analysis, By Application (Hydraulic Fluids, Metalworking Fluids, Chainsaw Oils, Mold Release Agents, Two-Cycle Engine Oils, Gear Oils, Greases, and Others), By End-use Industry (Automotive and Other Transportation, Metalworking, Mining, Forestry, Marine, Engines, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

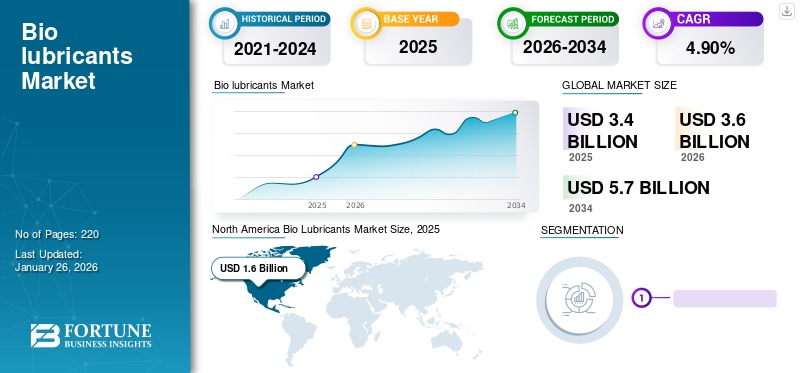

KEY MARKET INSIGHTS

The global biolubricants market size was valued at USD 3.61 billion in 2025. The market is projected to grow from USD 3.78 billion in 2026 to USD 5.94 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period. North America dominated the biolubricants market with a market share of 45.71% in 2025.

Biolubricants are emerging as an important alternative to conventional lubricants due to their environmentally friendly nature and sustainable composition. These lubricants are generally formulated using sustainable and biodegradable base stocks, which makes them increasingly significant across various end-use industries. The global demand for bio-based lubricants is expected to witness notable growth during the forecast period, supported by their rising adoption in the transportation and manufacturing sectors. This increasing demand is largely driven by growing environmental awareness, stronger understanding of sustainability concerns, the implementation of stringent regulations, and the wider acceptance of bio-based lubricants among industries.

Moreover, favorable legislative support, along with increasing government expenditure on research and development and product innovation, is anticipated to create strong growth opportunities for the market. The major key companies operating in the market are Cargill, Axel Christiernsson, BECHEM, Cortec Corporation, Environmental Lubricants Manufacturing, Inc., Klüber Lubrication, and Novvi, LLC.

Download Free sample to learn more about this report.

BIOLUBRICANTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.61 billion

- 2026 Market Size: USD 3.78 billion

- 2034 Forecast Market Size: USD 5.94 billion

- CAGR: 5.8% from 2026–2034

- North America dominated the biolubricants market with a 45.71% share in 2025.

- The hydraulic fluids segment led the market due to increasing use of bio-based lubricants in forestry and heavy equipment.

- The automotive and other transportation segment dominated the market owing to rising demand for environmentally friendly, high-performance lubricants.

North America

The market reached USD 1.65 billion in 2025, driven by automotive industry expansion, regulatory support, and growing adoption of biodegradable lubricants.

Europe

The market is expected to witness steady growth, supported by stringent environmental regulations and increasing adoption of sustainable industrial lubricants.

Asia Pacific

The market is projected to grow strongly, fueled by expanding industrialization, rising automotive production, and increasing environmental awareness.

U.S.

The market reached USD 1.38 billion in 2025, supported by strong regulatory initiatives and increasing use of environmentally acceptable lubricants in marine and automotive applications.

Japan

The market is expected to grow steadily, driven by increasing demand for sustainable lubricants across automotive and industrial applications.

Read More

BIOLUBRICANTS MARKET TRENDS

Shift Towards Mineral Oil-Based Lubricants is a Notable Market Trend

Biolubricants have gained growing importance as a sustainable alternative to conventional petroleum-based oils, particularly in addressing environmental concerns associated with lubricant use. The increasing adoption of biolubricants as a suitable substitute for petroleum-based oils has helped reduce environmental risks. Renewable raw materials such as plant oils and animal fats are being progressively utilized in lubricant production. With the required chemical modifications, environmental and economic considerations are encouraging the use of plant oils, animal fats, and even used oils and fats in lubricant applications. Vegetable oil-based lubricants offer several advantages over petroleum based lubricants, including biodegradability, renewability, cost-effectiveness, and lower environmental impact. Although mineral oil-based lubricants continue to dominate the market, their extensive usage has created serious environmental challenges. A significant share of lubricants used in various applications is eventually released into the environment due to leakages, equipment damage, operational instability, and system failures. In many cases, lubricants are reprocessed and reused multiple times before final disposal, further increasing the risk of environmental contamination. These losses have contributed to the pollution of air, freshwater, and soil. As public awareness of the harmful environmental effects of mineral oil-based lubricants continues to rise, the demand for biodegradable and bio-based lubricants is increasing steadily.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Stringent Government Regulations Governing Oil-based Lubricants to Boost Market Growth

Bio-based lubricants are gaining momentum due to strong regulatory support and rising environmental awareness, particularly in the U.S. and Europe. Key frameworks such as North America’s Vessel General Permit and Europe’s EU Ecolabel promote the adoption of sustainable lubricants with lower environmental impact. At the same time, end-use industries are increasingly preferring high-performance lubricants that improve energy efficiency and extend machinery lifespan. Regulators are also tightening renewable content requirements and evaluating lubricants based on their full lifecycle impact, from production to disposal. These developments are expected to support demand and strengthen biolubricants market growth and sustainability.

Rapid Development of Advanced Technologies to Fuel Market Growth

Biolubricants are emerging as a preferred sustainable substitute for conventional petroleum-based lubricants, due to continuous technological advancements that are improving their performance and cost efficiency.

The development of advanced technologies has significantly enhanced the effectiveness of biolubricants, making them more competitive than before. Innovations such as nanotechnology have enabled the creation of nanofluid-based biolubricants, where nanoparticles help reduce friction and wear, thereby improving lubrication performance. Likewise, the use of ionic liquids has contributed to the production of more stable biolubricants with longer shelf life. Growing demand for environmentally friendly lubricants is further driving market expansion, as industries such as automotive, manufacturing, and aerospace increasingly adopt these products to lower carbon footprint and meet regulatory requirements. In addition, the cost-effectiveness is supported by longer service life and reduced maintenance needs. As sustainability continues to remain a key focus across industries, further technological advancements are expected to furthermore drive the development of more efficient and environmentally friendly biolubricants.

Market Restraints

High Cost and Low Lubricating Properties to Hamper Market Growth

Bio-based lubricants offer strong environmental advantages, particularly due to their organic nature and high biodegradability, making them a promising alternative to conventional lubricants.

However, the direct use of vegetable oil-based lubricants as base oils remains limited due to certain performance challenges, including low oxidative stability, weak thermal and hydrolytic resistance, poor low-temperature behavior, and a limited viscosity range. These limitations can be addressed through chemical modification, usage of antioxidants, and blending with mineral oils. However, such measures often increase production costs, raise contamination concerns, and reduce biodegradability. As a result, developing a cost-effective bio-lubricant that combines high performance with superior biodegradability remains a major challenge. In addition, pricing continues to be a key barrier, as bio-based lubricants generally cost around 30%–40% more than conventional alternatives. Although most of them are positioned against mid- to high-performance mineral oil lubricants, their higher cost can still be justified in applications where biodegradability, lubricity, viscosity performance, and fire resistance are critical.

Market Opportunities

Environmental Regulations and Sustainable Industrial Practices is Driving Growth Potential

The market presents strong opportunities driven by stringent environmental regulations promoting biodegradable and low-toxicity lubricants. Increasing demand in environmentally sensitive sectors such as marine, agriculture, forestry, and construction significantly supports adoption. Technological advancements in synthetic esters and high-performance additive systems are enhancing oxidation stability and thermal resistance, enabling bio-lubricants to compete with conventional alternatives. Growing corporate sustainability commitments and ESG-driven procurement policies are further accelerating the shift toward renewable-based lubricants, thus strengthening long-term growth prospects in the market.

Market Challenges

High Costs and Performance Constraints are Limiting the Wider Adoption in the Market

The market faces challenges primarily due to higher production costs compared to petroleum-based lubricants, driven by feedstock price volatility and limited economies of scale. Dependence on agricultural raw materials such as vegetable oils creates supply chain uncertainties and competition with food markets. Additionally, performance limitations under extreme temperature and heavy-load conditions, along with compatibility concerns in existing machinery, can slow industrial adoption. Limited global standardization and lower awareness among end users further restrict large-scale penetration, hence moderating overall market expansion.

Impact of Tariffs

Increasing tariffs on raw materials such as vegetable oils and chemical additives, along with duties on finished bio-lubricant products, are impacting the overall cost structure of the market. Higher import costs can lead to increased production expenses, which may be passed on to end users, thereby affecting price competitiveness against conventional lubricants. Additionally, tariffs may disrupt global supply chains and limit access to cost-effective feedstocks. However, these challenges are also encouraging domestic production facilities, local sourcing of raw materials, and investment in regional manufacturing capabilities, ultimately supporting long-term market resilience and reducing dependency on imports.

Segmentation Analysis

By Application

Hydraulic Fluids Segment Holds a Leading Share Owing to Increasing Use Of Bio-Based Lubricants in Forestry Operations

Based on application, the market is segmented into hydraulic fluids, metalworking fluids, chainsaw oils, mold release agents, two-cycle engine oils, gear oils, greases, and others.

The hydraulic fluids segment accounted for the largest biolubricants market share in 2025, driven by the increasing use of bio-based lubricants in equipment such as harvesters, cranes, tractors, and load carriers, particularly in forestry operations. These applications are highly exposed to fluid leakage and spill risks, encouraging manufacturers to develop products for areas where lubricant loss during use is common.

Chainsaw oils also represent an important lost-in-use application requiring continuous lubrication in bars and chains. Although relatively small, this segment offers attractive growth potential, as chainsaws are largely used outdoors in environmentally sensitive areas such as forests and agricultural fields. In such applications, bio-based lubricants are preferred because the oil is subjected to centrifugal force during operation and is often dispersed directly onto the ground. The segment in expected to grow at a CAGR of 6.2% during the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Automotive and Other Transportation Segment to Takes the Lead Due to Low Toxicity and Strong Lubricating Properties

In terms of end-use industry, the market is segmented into automotive and other transportation, metalworking, mining, forestry, marine, engines, and others.

The automotive and other transportation segment held the leading market share in volume terms in 2025, supported by growing emphasis on environmentally friendly, durable, high-performance, and energy-efficient lubricants in the automotive and machinery sectors. These lubricants are increasingly considered to be a suitable alternative in automotive applications due to their low toxicity, strong lubricating ability, high viscosity index, high combustion temperature, and potential to extend machine service life.

In addition, several industries are adopting bio-based metalworking fluids for applications such as gear cutting, grinding, and general machining. Compared to petroleum-based products, these fluids offer benefits such as better viscosity-pressure performance, lower volatility, higher flash points, reduced smoke generation, and lower fire risk. The segment is anticipated to growat a CAGR of 7.5% during the forecast period. Bio-greases are also well suited for forestry equipment, construction vehicles, rail curves, rail flanges, and marine industry, where lubricants are often lost directly into soil or water. Although a range of high-performance bio-greases is available in the market, production volume remains limited.

BIOLUBIRCANTS MARKET REGIONAL OUTLOOK

By region, the market is studied across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

North America

North America Biolubricants Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest market share of the market in 2025 with valuation of USD 1.65 billion and is also expected to retain its leading position throughout the forecast period. Growth in the region is being supported by the recovery and expansion of the automotive industry in the U.S. and Canada, along with increasing regulatory pressure from the U.S. government to reduce the use of conventional lubricants. In addition, the U.S. Air Force’s support for plant-derived biodegradable products as part of its broader strategic and defense initiatives is further contributing to regional market growth. Rising government expenditure in the market for marine and automotive applications is also expected to create significant growth opportunities.

U.S. Biolubricants Market

The U.S. market in 2025 reached a valuation of USD 1.38 billion, accounting for approximately 38.2% of regional revenues. Strong regulatory support and rising adoption of environmentally acceptable lubricants in marine and automotive sectors drive the country’s market growth.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

Asia Pacific has emerged as a major automotive manufacturing hub alongside established markets such as the U.S. and Germany. China, India, Indonesia, and Thailand play an important role in producing and supplying passenger cars and other vehicles to developed economies. The continued shift of manufacturing facilities to Asian countries is expected to support higher automotive investment and broader industrial growth, driven by favorable government policies and the availability of low-cost labor. In addition, the growing shift toward sustainable and more efficient vehicles is anticipated to further drive the market in the region.

China Biolubricants Market

Based on Asia Pacific’s strong contribution and China’s position as the leading country in the regional market, the China market was valued at USD 0.26 billion in 2025, accounting for approximately 7.2% of regional revenues. Rapid industrialization and expanding automotive production, along with increasing environmental regulations, boosting the demand in the market.

Europe

In Europe, the adoption of bio-based chemicals is being supported by stringent environmental regulations and the continued transition toward a bio-economy across Germany, Italy, Nordic nations, Benelux, and France.

Germany Biolubricants Market

Germany’s market reached a valuation of USD 0.15 billion in 2025, accounting for approximately 4.0% of regional revenues. Strict sustainability policies and strong presence of advanced manufacturing industries support the product adoption..

Latin America and Middle East & Africa

The Middle East & Africa and Latin America markets are expected to record notable growth during the forecast period, supported by the expanding base oil market, rapid industrialization, population growth, and increasing urbanization. Rising economic development and improving living standards have also led to stronger demand for high-performance and premium passenger vehicles across the region. These favorable trends have attracted significant investments from global automotive manufacturers, which is expected to further support the growth of the market.

Brazil Biolubricants Market

The Brazilian market in 2025 was valued at USD 0.19 billion, accounting for approximately 5.2% of Latin America revenues. Growing agricultural activities and rising awareness for biodegradable lubricants drive market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Planning by Leading Companies is Strengthening their Market Share

The biolubricants market is highly competitive, with major oil companies competing alongside independent and small- to medium-sized specialist manufacturers. Although the market is still in an early stage of development, it remains fairly concentrated, with leading key players such as Panolin, Fuchs, Total, Shell, Exxon Mobil Corporation, and bp p.l.c. accounting for a significant share. Large global oil refiners who traditionally focused on conventional lubricants, are increasingly expanding their portfolios to include biodegradable lubricants for transportation applications. Other notable participants include Cargill, Axel Christiernsson, BECHEM, Cortec Corporation, Environmental Lubricants Manufacturing, Inc., Klüber Lubrication, and Novvi, LLC. At the same time, several smaller companies remain active in the market, with many concentrating primarily on research and development in the market.

LIST OF KEY BIOLUBIRCANTS COMPANIES PROFILED

- PANOLIN AG (Switzerland)

- FUCHS (Germany)

- Shell (Netherlands)

- Exxon Mobil Corporation (U.S.)

- Total (France)

- Cargill (U.S.)

- Axel Christiernsson (Sweden)

- BECHEM (Germany)

- Cortec Corporation (U.S.)

- Environmental Lubricants Manufacturing, Inc. (U.S.)

- Klüber Lubrication (Germany)

- Novvi, LLC. (U.S.)

- Repsol (Spain)

- bp p.l.c. (U.K.)

- Emery Oleochemicals (Malaysia)

- IGOL (Norway)

- LanoPro (Norway)

KEY INDUSTRY DEVELOPMENTS

- October 2025: FUCHS highlighted that its ACT-based lubricant range has expanded, with engine oils and automatic transmission oils among the most advanced products. These products are based on recycled or bio-based raw materials, maintain high performance, indicating further commercialization of circular/renewable lubricant technologies.

- October 2025: Klüber Lubrication launched a new generation of environmentally responsible lubricants using mass-balanced, bio-based raw materials with REDcert² certification, with the first launch focused on the Klübersynth GH 6 MB gear oil series, signalling the commercialization of lower-emission lubricants without changing application performance.

- September 2025: Shell formally positioned Shell PANOLIN as its new biodegradable lubricants brand, stating that the range brings together decades of biodegradables R&D, offers readily biodegradable fluids with low aquatic ecotoxicity, and includes certifications such as EU Ecolabel, OSPAR, CEFAS, and USDA BioPreferred, signalling brand consolidation and a broader commercial platform for Shell’s bio-lubricants portfolio.

- March 2025: Cargill published its “Fluids for next generation EV passenger cars” brochure, highlighting the Priolube EF 3446, EF 3221, and EF 7010 synthetic ester base oils alongside Perfad traction-reducing co-base fluids for EV gearboxes, transmissions, and e-axles, signalling a stronger push into bio-based / biodegradable next-generation lubricant formulations for electric mobility.

- November 2024: TotalEnergies Lubrifiants launched the Rubia EV3R heavy-duty range, with more than 50% of the base oils coming from re-refined high-end base oils and packaging made with 50% recycled HDPE, signalling broader commercialization of environmentally friendly lubricants in the commercial vehicle segment.

- October 2024: FUCHS formally launched ACT (Advanced Circular Technologies), describing it as a shift from traditional fossil-based raw materials to recycled and bio-based ones, marking a broader platform for circular, lower-carbon lubricant development across its portfolio.

- July 2024: Axel Christiernsson announced that its Nol, Sweden plant installed Kettle 55, increasing production capacity and flexibility, with the company specifically noting higher capacity for lithium alternatives driven by rising demand for HYCAL technology, signalling manufacturing expansion relevant to environmentally adapted calcium-based grease solutions.

REPORT COVERAGE

The global biolubricants market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, products, and products. Also, it offers insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors contributing to the market's growth in recent years. It further includes historical data & forecasts revenue growth at global, regional, and country levels and analyzes the industry's latest market dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) and Volume (Million Tons) |

| Growth Rate | CAGR of 5.8% from 2026 to 2034 |

| Segmentation | By Application, End-use Industry, and Region |

| By Application |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.61 billion in 2025 and is projected to reach USD 5.94 billion by 2034.

In 2025, the North America market size stood at USD 1.65 billion.

Registering a CAGR of 5.8%, the market will exhibit steady growth during the forecast period.

The automotive and other transportation segment led the market in 2025.

Growing stringent regulations to aid market growth.

Panolin, Fuchs, Total, Shell, Exxon Mobil Corporation, and BP p.l.c. are the major players in the market.

North America dominated the market in terms of share in 2025.

Growing government spending on R&D to drive the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 220

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us