Vintage Packaging Market Size, Share & Industry Analysis, By Material (Paper & Paperboard, Glass, Metal, and Others), By Product Type (Films & Labels, Boxes & Cartons, Bottles & Jars, Bags & Pouches, and Others), By End Use (Food & Beverages, Personal Care & Cosmetics, Consumer Goods, Fashion & Apparel, and Others), and Regional Forecast, 2026-2034

Vintage Packaging Market Size and Future Outlook

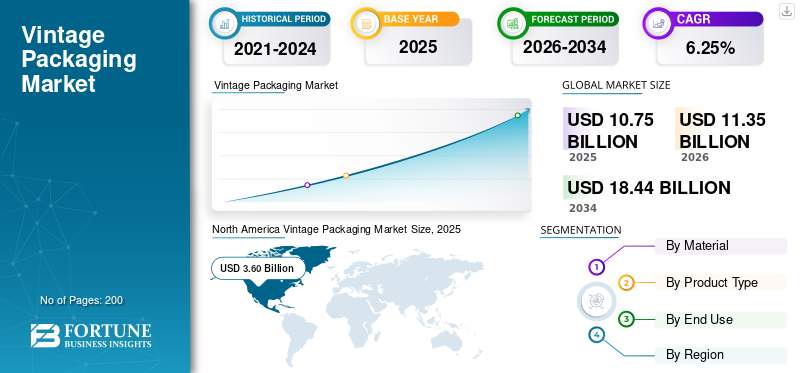

The global vintage packaging market size was valued at USD 10.75 billion in 2025. The market is projected to grow from USD 11.35 billion in 2026 to USD 18.44 billion by 2034, exhibiting a CAGR of 6.25% during the forecast period. North America dominated the vintage packaging market with a market share of 33.48% in 2025.

The global market pertains to the sector dedicated to the design, production, and provision of packaging solutions that emulate historical, retro, or nostalgic styles. The growing consumer inclination toward nostalgic and high-quality products is fueling the demand for vintage-inspired packaging, as brands are progressively adopting retro designs to distinguish their offerings, reinforce emotional ties, and improve perceived authenticity, especially in competitive industries such as beverages, personal care, and artisanal foods.

Furthermore, several leading companies, including Amcor, Smurfit Kappa, and Mondi, operating in the market, are prioritizing product innovation and increasing their investments in research and development activities.

Download Free sample to learn more about this report.

VINTAGE PACKAGING MARKET TRENDS

Premiumization Through Nostalgic Branding is Widely Influencing Market Developments

A significant trend in the global market is the growing incorporation of nostalgic, unique designs alongside premiumization strategies. This trend is particularly evident in sectors such as alcoholic beverages, gourmet foods, and luxury personal care items, where storytelling is essential for engaging consumers. Additionally, companies are merging vintage aesthetics with modern sustainable elements, including recyclable materials and minimalist designs, to meet changing environmental impact and standards. The combination of retro charm with modern functionality is enabling brands to differentiate themselves on store shelves while enhancing perceived value.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Emotional and Experiential Branding is Driving Market Growth

A primary factor propelling the vintage packaging market growth is the increasing consumer preference for emotional and experiential branding. Contemporary consumers, especially millennials and Gen Z, are more attracted to products that trigger nostalgia and provide a narrative that extends beyond mere functionality. This emotional bond frequently leads to increased brand loyalty and a readiness to pay higher prices. In fiercely competitive markets, such differentiation is essential. Consequently, businesses in various sectors, including beverages, confectionery, and cosmetics, are making substantial investments in retro-themed packaging designs to boost consumer engagement and encourage repeat purchases.

MARKET RESTRAINTS

Higher Production and Design Costs Hampers Market Growth

A major limitation in the vintage packaging sector is the comparatively elevated expense linked to the creation of retro-style packaging. In contrast to conventional packaging, vintage designs frequently necessitate specialized packaging materials, elaborate detailing, custom printing methods, and distinctive structural formats, all of which heighten production complexity and costs. Furthermore, ensuring uniformity in vintage aesthetics across substantial production quantities can further drive up expenses. These financial limitations may hinder widespread acceptance, especially in markets that are sensitive to price, where cost efficiency is a crucial factor in packaging choices.

MARKET OPPORTUNITIES

Expansion in Artisanal and Craft Product Segments Offers Potential Growth Opportunities

A significant opportunity exists for the sector due to the swift expansion of artisanal and craft product categories. Producers of small-batch items, including craft beverages, handmade cosmetics, specialty foods, and organic products, are increasingly turning to vintage packaging for expressing authenticity, tradition, and craftsmanship. As consumer interest in locally sourced and unique offerings continues to increase, the need for visually striking and narrative-driven packaging solutions is anticipated to rise. This situation presents a beneficial landscape for packaging manufacturers to provide customized, low-volume vintage designs specifically aimed at niche markets.

MARKET CHALLENGES

Stringent Environmental Regulations and Compliance Pose a Critical Challenge to Market Growth

One of the primary challenges faced in the sector is finding a balance between traditional aesthetics and contemporary sustainability standards. Numerous vintage packaging designs depend on materials such as coated papers, multi-layer laminates, or decorative features that may not be easily recyclable or environmentally sustainable. As regulatory pressures and consumer awareness regarding sustainability grow, brands are urged to reimagine packaging without sacrificing its retro charm. Effectively incorporating eco-friendly materials while preserving the authenticity and visual richness of vintage-style packaging continues to be a complex and ongoing challenge for manufacturers.

Segmentation Analysis

By Material

Sustainability Appeal, Print Versatility, and Cost Efficiency Drive the Dominance of Paper & Paperboard Segment

Based on the material, the market is divided into paper & paperboard, glass, metal, and others.

The paper & paperboard segment is expected to account for the largest vintage packaging market share. The prevalence of paper and paperboard in the global market is mainly influenced by their effective alignment with both aesthetic and functional needs. Their organic appearance and tactile quality further contribute to authenticity, rendering them suitable for nostalgic branding. From a financial standpoint, paper-based materials are comparatively affordable and readily accessible in contrast to alternatives such as glass or metal. Moreover, rising regulatory demands and consumer inclination toward sustainable packaging support the use of paper and paperboard due to their recyclability and biodegradability, thereby strengthening their extensive use across various industries.

The glass segment is expected to grow at a CAGR of 6.29% over the forecast period.

By Product Type

High Customization, Branding Flexibility, and Cost Advantage Drive the Dominance of Films & Labels Segment

Based on product type, the market is segmented into films & labels, boxes & cartons, bottles & jars, bags & pouches, and others.

In 2025, the films & labels segment dominated the global market which can be primarily credited to their unparalleled design and application flexibility. These formats enable brands to seamlessly integrate retro graphics, weathered textures, and traditional typography without modifying the core packaging structure, rendering them exceptionally cost-efficient. Furthermore, innovations in printing technologies, such as digital and flexographic printing, facilitate the production of high-quality vintage aesthetics on a large scale. Their reduced material consumption, straightforward replacement, and versatility positions films and labels as the favored option for brands aiming for striking yet budget-friendly vintage packaging solutions.

The boxes & cartons segment is projected to grow at a CAGR of 6.29% over the forecast period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Strong Branding Needs, High Product Turnover, and Consumer Nostalgia Drive the Dominance of Food & Beverages Segment

Based on the end use, the market is segmented into food & beverages, personal care & cosmetics, consumer goods, fashion & apparel, and others.

The food & beverages segment is expected to hold a dominant market share over the forecast period primarily due to its significant dependence on visual aesthetics and brand narratives to sway consumer purchasing choices. Items such as craft beverages, sweets, dairy products, and specialty foods often utilize vintage packaging to convey authenticity, tradition, and quality, which strongly appeal to consumers. Furthermore, the tendency for impulse purchases in retail settings heightens the necessity for striking, nostalgic designs. Coupled with the increasing demand for artisanal and high-end food items, these elements together bolster the extensive use of vintage-style packaging within this sector.

The personal care & cosmetics segment is projected to grow at a CAGR of 6.25% over the forecast period.

Vintage Packaging Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Vintage Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 3.40 billion, and maintained its leading position in 2025, with a value of USD 3.60 billion. In North America, the market is propelled by a robust demand for premium and craft offerings, especially in the sectors of beverages and artisanal foods. Brands actively utilize vintage-style packaging to communicate authenticity and heritage, while consumers demonstrate a significant willingness to invest in nostalgic, visually unique products that elevate perceived quality and narrative.

U.S. Vintage Packaging Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 2.82 billion in 2025, accounting for roughly 26.23% of global sales. In the U.S., fierce market competition compels brands to utilize vintage-style packaging as a means of differentiation and to enhance experiential appeal. Companies capitalize on retro designs to forge emotional connections and strengthen brand identity, particularly in sectors such as craft alcohol, organic foods, and personal care, where the impact on shelves and the art of storytelling play a crucial role in influencing purchasing decisions.

Asia Pacific

Asia Pacific region reached USD 2.85 billion in 2025 and secured the position of the second-largest region in the market. In the region, swift urbanization coupled with a rising middle class population is driving the demand for high-quality and aesthetically pleasing products. The adoption of vintage-style packaging is on the rise as brands seek to enhance their image and emulate Western luxury trends. The growth of the food, beverage, and cosmetics sectors is further propelling the popularity of retro-inspired packaging designs.

Japan Vintage Packaging Market

The Japanese market in 2025 was valued at around USD 0.54 billion, accounting for roughly 4.98% of global revenues. Japan's market is propelled by a profound admiration for design, meticulous detail, and a gentle sense of nostalgia. Brands integrate minimalist vintage features to showcase craftsmanship and cultural legacy. The heightened consumer awareness regarding packaging quality and visual appeal promotes the adoption of sophisticated retro designs, especially in the sectors of confectionery, beverages, and personal care items.

China Vintage Packaging Market

China's market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 0.91 billion, representing roughly 8.48% of global sales.

India Vintage Packaging Market

The Indian market size in 2025 was recorded at around USD 0.76 billion, accounting for roughly 7.10% of the global high-revenue markets.

Europe

Europe is projected to grow at 5.94% over the coming years, the third-highest among regions, and reached a valuation of USD 2.15 billion in 2025. The market in Europe is significantly influenced by a robust cultural focus on heritage and tradition, which renders vintage-style packaging particularly pertinent. Furthermore, stringent sustainability regulations compel brands to embrace environmentally friendly paper-based vintage formats. This blend of authenticity, adherence to regulations, and premium positioning fosters consistent demand within the food, beverage, and cosmetics industries.

U.K. Vintage Packaging Market

The U.K. market value in 2025 was recorded at USD 0.41 billion, representing approximately 3.80% of global revenues.

Germany Vintage Packaging Market

Germany's market size reached approximately USD 0.46 billion in 2025, equivalent to around 4.32% of global sales.

Latin America

The Latin America region is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 0.95 billion in 2025. In Latin America, the use of vintage-style packaging is motivated by the necessity for economical differentiation within competitive retail settings. Local brands employ retro-inspired designs to emphasize tradition and authenticity while keeping costs relatively low. The increasing demand for packaged foods and beverages facilitates the gradual embrace of these packaging styles.

Middle East & Africa

In the Middle East & Africa, South Africa reached USD 0.25 billion in 2025. In the Middle East & Africa, the growth of premium retail sectors alongside increasing disposable incomes serves as a significant catalyst. Vintage-style packaging is employed to convey notions of luxury, exclusivity, and cultural depth, particularly in the realms of gourmet foods, fragrances, and specialty beverages. The emphasis on distinctive brand identity fosters steady market expansion.

Saudi Arabia Vintage Packaging Market

The Saudi Arabian market reached approximately USD 0.34 billion in 2025, accounting for roughly 3.15% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Leaders Drive Growth by Focusing on Acquisitions and Expanding Product Launch

The global industry features a semi-integrated composition, with major players in the packaging sector including Amcor, Smurfit Kappa, and Mondi. These organizations maintain significant market shares through the execution of diverse tactical plans, such as collaborations among operating entities to advance research.

- In February 2026, Amcor Plc declared the enhancement of its sustainable packaging range with the introduction of new recyclable flexible films aimed at supporting premium and vintage-style branding. This innovation facilitates the use of high-quality retro graphics while ensuring adherence to environmental standards. Such a development reinforces Amcor's standing in merging nostalgic aesthetics with contemporary sustainability, especially for food and beverage brands that are seeking ways to stand out.

Other prominent participants in the worldwide market include Graphic Packaging International, Crown, and O-I Inc. These players are anticipated to emphasize product innovation, tactical alliances, and industry partnerships in order to strengthen their global market shares over the forecast period.

LIST OF KEY VINTAGE PACKAGING COMPANIES PROFILED

- Amcor Plc (Switzerland)

- Smurfit Kappa (Ireland)

- Mondi (U.K.)

- Graphic Packaging International (U.S.)

- Crown (U.S.)

- O-I Inc. (U.S.)

- Vintage Packaging (U.S.)

- Deufol SE (Germany)

- DS Smith (U.K.)

- International Paper Company (U.S.)

- Embelia (Spain)

- Vintage Offset (India)

- Arrow Systems Inc. (U.S.)

- Yima Label (China)

- Rapid Tags & Label (U.K.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Smurfit Kappa has introduced a new collection of paper-based packaging solutions designed specifically for premium and retro-themed branding applications. These solutions emphasize improved printability and textured finishes to complement vintage aesthetics. The company has noted an increasing demand from artisanal food and beverage brands that are seeking sustainable yet visually appealing packaging.

- August 2025: Mondi has launched a specialized series of kraft paper designed for high-end packaging applications, featuring designs inspired by vintage aesthetics. This product line enhances surface quality, allowing for intricate printing and embossing, which makes it ideal for brands seeking a nostalgic appeal. Additionally, Mondi has increased its production capacity in Eastern Europe to meet the growing demand for sustainable paper packaging.

- May 2024: DS Smith has introduced a circular design initiative aimed at substituting intricate plastic packaging with recyclable paperboard options that are appropriate for vintage-style branding. The company has partnered with various European food brands to revamp packaging by employing retro-inspired visuals printed on sustainable materials. This initiative embodies DS Smith's strategy to harmonize sustainability with consumer preferences that lean toward nostalgic packaging.

- January 2024: Graphic Packaging International has broadened its range of premium paperboard packaging solutions aimed at the craft beverage and specialty food sectors. The latest products feature customizable cartons equipped with high-definition printing and embossing capabilities that enhance vintage branding. The company has noted a rise in demand from brands seeking to stand out with nostalgic packaging designs.

- September 2023: Crown Holdings has introduced a new range of decorative metal packaging solutions, featuring embossed cans and tins tailored for retro and vintage branding. These offerings primarily target beverage and specialty food companies that are seeking enhanced shelf appeal. The company emphasized the increasing trend of nostalgic packaging as a key factor in boosting consumer engagement.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.25% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, Product Type, End Use, and Region |

| By Material |

|

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 10.75 billion in 2025 and is projected to reach USD 18.44 billion by 2034.

In 2025, the market value stood at USD 3.60 billion.

The market is expected to grow at a CAGR of 6.25% over the forecast period.

By material, the paper & paperboard segment is expected to lead the market.

The growing demand for emotional and experiential branding is driving the market growth.

Amcor, Smurfit Kappa, and Mondi are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us