Industry 4.0 Market Size, Share & Global Industry Analysis, By Application (Industrial Automation, Smart Factory, and Industrial IoT), By Vertical (Manufacturing, Energy & Utilities, Automotive, Oil and Gas, Aerospace and Defense, Electronics and Consumer Goods, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

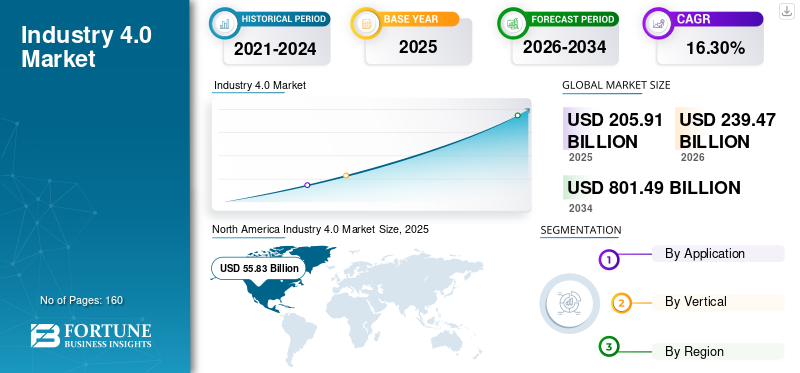

The global industry 4.0 market size was estimated at USD 205.91 billion in 2025. The market is expected to rise from USD 239.47 billion in 2026 to USD 801.49 billion by 2034, expanding at a CAGR of 16.30% from 2026 to 2034. North America dominated the industry 4.0 market with a market share of 27.12% in 2025, driven by widespread adoption of smart manufacturing and strong government support.

The market is driven by accelerated digitalization of industrial operations, rising automation intensity, and persistent pressure on manufacturers to improve productivity and resilience. The Industry 4.0 market represents the convergence of cyber-physical systems, advanced analytics, industrial automation, and connected machinery across value chains. Enterprises increasingly integrate data-driven control architectures to optimize production, asset utilization, and supply responsiveness.

Industry 4.0 adoption is no longer limited to large enterprises. Small and medium-sized enterprises increasingly deploy modular automation, cloud-based manufacturing execution systems, and scalable Industrial Internet of Things (IIoT) platforms. This shift expands the industry 4.0 market size while reshaping purchasing behavior toward flexible, software-centric solutions. The market structure favors vendors offering interoperable systems rather than closed automation stacks.

The industry 4.0 market growth trajectory reflects long-term structural change rather than cyclical investment. Manufacturers prioritize operational visibility, predictive maintenance, and quality assurance under volatile demand conditions. These priorities sustain spending even during macroeconomic uncertainty. As a result, the industry 4.0 market share is increasingly captured by providers combining hardware, software, and services into integrated solutions.

From a strategic perspective, Industry 4.0 functions as a foundational layer for smart manufacturing, digital supply networks, and industrial sustainability initiatives. Government-backed industrial modernization programs further reinforce adoption. The market remains heterogeneous, shaped by sector-specific automation maturity, regulatory environments, and workforce readiness. Despite uneven adoption rates, Industry 4.0 has transitioned from experimental deployment to core industrial infrastructure.

Within the scope considered, players include ABB Ltd., Siemens AG, and Cognex Corporation, among others. The Industry 4.0 product offerings of ABB Ltd. include robotics, PLC automation, control room solutions, and motors and generators, among others. Similarly, Siemens AG provides building technologies, industrial automation, and mobility, among others.

The growing trend of digitization and internet penetration, driven by the focus of various industries on efficiency and profitability, is creating market growth opportunities. Recent advances in digital technologies and industrial computerization have begun to expand the possibilities for disrupting industrial value chains. With the advent of the fourth industrial revolution (i4.0), companies are experiencing improved efficiencies, reduced cost benefits, increased production, personalized offerings, and, most importantly, the development of new revenue and business models.

For instance, in May 2021, Robert Bosch Engineering and Business Solutions Private Limited launched Phantom Edge to provide a real-time view of electric parameters, appliance-level information, electrical energy consumption, and operating usage. The Phantom Edge combines Artificial Intelligence (AI) and the Internet of Things (IoT) and can be used across sectors such as retail, industrial manufacturing, healthcare, agriculture, and mobility.

Download Free sample to learn more about this report.

Industry 4.0 Market Key Takeaways

- 2025 Market Size: USD 205.91 billion

- 2026 Market Size: USD 239.47 billion

- 2034 Forecast Market Size: USD 801.49 billion

- CAGR: 16.30% from 2026–2034

- North America dominated the Industry 4.0 market with a 27.12% share in 2025.

- The Manufacturing segment is expected to dominate the global market during the forecast period.

- The Industrial IoT (IIoT) segment continues to witness strong adoption across industries.

Asia Pacific

Rapid industrial automation and government-led digital initiatives drive regional expansion.

North America

North America reached USD 55.83 billion in 2025 and is projected to grow to USD 64.94 billion in 2026.

Europe

Strong investments in automation and smart manufacturing continue to support market growth.

U.S.

Large-scale smart factory investments and industrial modernization accelerate Industry 4.0 adoption.

Japan

Precision manufacturing and robotics integration continue to strengthen Industry 4.0 deployment.

Read More

Industry 4.0 Market Trends

Predictive Maintenance Using Digital Twin Solution Will be a Significant Market Trend

As the Internet of Things (IoT) has grown in popularity in recent years, digital twins have attracted significant attention. A digital twin is a virtual model that follows the lifecycle of a physical entity or mechanism. This technology has enabled OEM manufacturers and automakers to remotely track and manage equipment and systems by providing near-real-time insights between the physical and digital worlds. To spot bottlenecks, streamline processes, and innovate product growth, digital twin technology provides an unparalleled insight into assets and production.

Companies are incorporating digital twin technology that can detect operational anomalies and irregularities in real time to gain a holistic view of equipment performance. Spare component maintenance and replenishment can be scheduled in advance to reduce time-to-service and prevent costly asset failures. Predictive maintenance with digital twins would help OEMs generate new service-based revenue while also improving product reliability. Additionally, companies in the market are launching advanced digital twin solutions that provide better visibility into equipment and improve operational efficiency. For instance,

- In February 2020, Huawei Technologies Co., Ltd., a digital technology company headquartered in China, launched digital site twins. This solution creates an exact digital replica of a physical site, enabling smoother digital operations.

- In June 2020, Siemens AG launched Teamcenter X Software, which enables enterprises to quickly integrate, scale, and implement PLM technology in functional disciplines. This launch would further support the creation of a digital twin with bill-of-materials integration and multi-domain design.

The Industry 4.0 market trends indicate a decisive shift from isolated automation projects toward enterprise-wide digital transformation. Manufacturers increasingly pursue connected production ecosystems that integrate operational technology and information technology environments. This convergence supports real-time decision-making and closed-loop process optimization across plants.

Download Free sample to learn more about this report.

Customer demand trends emphasize measurable return on investment rather than technological novelty. Buyers favor solutions that deliver rapid efficiency gains, energy optimization, and reduced downtime. Subscription-based software models and outcome-based service contracts are gaining acceptance, particularly in asset-intensive industries. These preferences influence vendor pricing strategies and solution packaging.

Industry drivers include persistent labor shortages, rising input costs, and supply chain volatility. Automation and advanced analytics mitigate workforce constraints while improving production predictability. Competitive pressure also intensifies as digital leaders outperform peers on cost, quality, and responsiveness. Late adopters face growing performance gaps.

Competitive trends reflect consolidation and ecosystem partnerships. Automation vendors collaborate with cloud providers, industrial software firms, and system integrators to deliver end-to-end offerings. Acquisitions target analytics, artificial intelligence, and edge computing capabilities. Differentiation increasingly depends on software depth rather than hardware scale.

DRIVING FACTORS

Increased Adoption of Industrial Robots and Surge in Industrial Automation Demand Drive the Market Growth

Over the last few decades, robots have progressed from being prohibitively costly machines with minimal capabilities to being inexpensive machines capable of performing a wide range of tasks. Industrial robots, in particular, are widely used worldwide. According to the latest robotics industry trends, industrial robots are increasingly used in manufacturing hubs, driving rapid advancements, development, and evolution.

The manufacturing sector has witnessed growing acceptance of robotics engineering and technology in its production processes, driven by rapid advances in robotics. Industrial robots are multipurpose, automatically controlled, programmable manipulators. Welding, heavy lifting, ironing, assembling, picking and positioning, palletizing, product inspection, and testing are just a few of the popular industrial robot applications, all of which require significant human endurance, speed, and precision.

According to the International Federation of Robotics (IFR), around 486,800 units were shipped worldwide in 2021. Industrial robots perform repeatable tasks and eliminate the need for human labor. Furthermore, they can operate in hazardous and external risks that humans cannot. Thus, robotics technology will be a key trend in the industry.

- For instance, in February 2021, ABB Ltd launched the SWIFTI cobot. This collaborative robotic family provides enhanced safety, the precision of an industrial robot, robustness, and ease of use, with speed, for various applications, including manufacturing and logistics.

Manufacturers face continuous pressure to reduce costs and improve throughput. Industry 4.0 technologies enable predictive maintenance, process automation, and real-time performance monitoring. Evidence shows reduced downtime and improved asset utilization. The impact is strongest in discrete manufacturing and high-capital-intensity process industries.

Aging workforces and technical labor shortages drive automation adoption. Smart machines and decision-support systems offset human resource gaps. This driver is particularly relevant in advanced economies and export-oriented manufacturing hubs. Recent disruptions exposed vulnerabilities in global production networks. Industry 4.0 enables end-to-end visibility and adaptive scheduling. Digitally connected factories respond faster to demand fluctuations. The automotive, electronics, and consumer goods sectors are highly sensitive.

Industries face stricter quality, traceability, and safety requirements. Automated inspection, data logging, and digital documentation reduce compliance risks. Regulated sectors such as aerospace, defense, and pharmaceuticals are most affected. Falling sensor, connectivity, and cloud computing costs lower adoption barriers. Scalable platforms support phased deployment. This driver expands the addressable market among small and medium-sized enterprises.

RESTRAINING FACTORS

Data Risks Associated with the Integration of Advanced Technologies to Restrict Growth

The integration and implementation of industry solutions offer several benefits but also pose risks that could hamper business development in the near future. Data and security challenges associated with the implementation of advanced technologies are expected to hamper the market growth. According to a study published by Cybercrime Magazine in 2021, the cost of cybercrime reached USD 6.0 trillion globally in 2021 and is predicted to reach USD 10.5 trillion by 2025. Industry 4.0 systems are unable to prevent hackers from accessing the manufacturer's data and collecting sensitive information due to their inherent susceptibility to attacks. As a result, there is a need to raise awareness of such threats and to understand the necessity of cybersecurity solutions at all levels of organizational networks.

Despite strong momentum, several constraints limit the pace of Industry 4.0 market expansion. Integrated automation projects require capital expenditure across hardware, software, and integration services. Budget constraints delay adoption, especially among smaller manufacturers. This restraint is most visible in cost-sensitive regions.

Many facilities operate aging equipment lacking digital interfaces. Retrofitting increases project complexity and risk. Industries with long asset lifecycles face slower transition timelines. Expanded connectivity increases exposure to cyber threats. Manufacturers remain cautious about sharing operational data. Compliance uncertainty slows cloud adoption in regulated markets.

Digital transformation requires new skills and cultural adaptation. Skills gaps and resistance to automation hinder implementation. This issue affects traditional manufacturing clusters. Inconsistent industrial standards complicate system integration. Vendor lock-in risks remain a concern. These issues limit scalability across multi-site operations.

Market Opportunities

The Industry 4.0 market presents significant opportunities across technology, geography, and business models.

High-growth segments include smart factories, digital twins, and industrial analytics platforms. Manufacturers increasingly invest in virtual commissioning, simulation, and predictive optimization. These applications deliver fast payback and operational transparency. Market gaps persist in mid-market solutions tailored for small and medium-sized enterprises. Simplified deployment, modular pricing, and cloud-native architectures remain underpenetrated. Vendors addressing this gap can expand market reach.

Technology-driven opportunities center on artificial intelligence at the edge, autonomous systems, and closed-loop quality control. Integration of sustainability metrics into production systems supports regulatory compliance and energy optimization. Geographic expansion opportunities are strongest in Asia-Pacific and parts of Latin America, where industrial modernization accelerates. Government incentives and infrastructure investment support adoption.

Regulatory and policy frameworks increasingly favor digital manufacturing through tax incentives, innovation grants, and sustainability mandates. Environmental, social, and governance objectives align with Industry 4.0 through energy efficiency, waste reduction, and transparent reporting.

Industry 4.0 Market Segmentation Analysis

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Industrial IoT (IIoT) to Gain Momentum during Forecast Period

Based on application, the market is classified into industrial automation, smart factory, and industrial IoT. Industrial IoT (IoT in the industrial sector) combines the advancements of two transformative revolutions. The possible benefits of IoT technology have motivated several industrial equipment manufacturers to adopt IoT. By connecting industrial equipment wirelessly and collecting sensor data, manufacturers can estimate the current state of machines, improve performance, and identify potential failures while planning maintenance programs. Industrial automation provides a wide range of technologies that help in reducing human intervention. Further, it helps in flexibility and the quality of manufacturing processes.

Automation solutions include programmable logic controllers, distributed control systems, robotics, and advanced motion control integrated with digital interfaces. These systems increasingly embed analytics and connectivity, transforming traditional automation into adaptive production platforms. Adoption is strongest in high-volume manufacturing environments where consistency, uptime, and throughput determine competitiveness.

Smart factory applications represent the fastest-growing segment of the Industry 4.0 market. Unlike conventional automation, smart factories emphasize end-to-end connectivity, real-time intelligence, and self-optimizing processes. These environments integrate digital twins, manufacturing execution systems, and advanced analytics to synchronize production, quality, and logistics. Smart factory deployments extend beyond the shop floor, connecting suppliers, warehouses, and distribution networks. This application area attracts investment from manufacturers pursuing long-term resilience rather than incremental efficiency gains.

Industrial Internet of Things applications enable the data layer underlying Industry 4.0 architectures. IIoT platforms connect sensors, machines, and assets to centralized or edge-based analytics systems. This application supports predictive maintenance, energy optimization, and condition monitoring across distributed operations. The IIoT market share in Industry 4.0 continues to expand as connectivity costs decline and interoperability improves. Adoption is particularly pronounced in asset-intensive industries, where unplanned downtime poses significant financial risk.

By Vertical Analysis

Manufacturing to Capture Maximum Market Share in the Forthcoming Years

Based on vertical, the market is further segregated into manufacturing, energy & utilities, automotive, oil and gas, aerospace and defense, electronics and consumer goods, and others.

The manufacturing segment is estimated to dominate the global market during the forecast period. The automotive, transportation, and chemical segments are projected to be the most promising verticals for implementing i4.0. The deployment of smart robots & machines in the manufacturing sector has been on the rise over the past few years. Investments in research and development are underway to design an integrated system that enables robots and humans to work together on complex tasks through sensor-connected human-machine interfaces.

Manufacturing represents the largest contributor to the overall Industry 4.0 market size. Discrete and process manufacturers deploy Industry 4.0 solutions to address margin pressure, customer demand for customization, and supply volatility. Automotive and electronics manufacturers lead adoption due to complex production workflows and globalized supply chains. Manufacturing investments increasingly prioritize software-defined capabilities, reflecting a shift from hardware-centric automation toward data-driven operations.

The adoption of advanced solutions will be high in the automotive sector during the forecast period. Plants equipped with technology can track the production equipment and processes to detect possible problems before they cause production downtime. Automobile manufacturers that are i4.0-ready can also configure individual vehicles, thereby reducing delivery time. Manufacturers must configure vehicle configurations to meet changing customer demands. Unlike conventional auto production, the IIoT-enabled device allows for customization, such as the dashboard and steering wheel. Furthermore, the concept of self-driving vehicles has become a reality owing to i4.0. Companies across the automotive ecosystem are investing heavily in product and manufacturing process innovations to stay competitive amid rapid technological advances.

The energy and utilities vertical demonstrates growing adoption driven by grid modernization, asset monitoring, and regulatory compliance. Industry 4.0 technologies support real-time monitoring of generation assets, transmission infrastructure, and consumption patterns. Utilities leverage advanced analytics to improve reliability, manage distributed energy resources, and optimize maintenance cycles—this vertical values cybersecurity, system redundancy, and regulatory alignment, shaping vendor selection criteria.

Automotive applications emphasize flexibility, traceability, and quality assurance. Industry 4.0 enables rapid model changeovers, automated inspection, and synchronized supplier integration. Electric vehicle production further accelerates digital investment, driven by new component architectures and stringent quality requirements. Automotive manufacturers represent early adopters of digital twins and closed-loop production control, influencing broader industry 4.0 market trends.

Oil and gas adoption centers on operational safety, asset integrity, and remote monitoring. Industry 4.0 applications support predictive maintenance for drilling equipment, pipelines, and refineries. Harsh operating environments drive demand for robust sensors and edge analytics. While capital-intensive, this vertical exhibits cautious adoption cycles influenced by commodity price volatility and regulatory scrutiny.

Aerospace and defense applications prioritize precision, compliance, and lifecycle traceability. Industry 4.0 solutions support complex assembly processes, digital quality records, and secure data management. Adoption remains selective due to stringent certification requirements but delivers high value through reduced rework and improved program visibility.

Electronics and consumer goods manufacturers leverage Industry 4.0 to manage short product lifecycles and demand variability. Automation combined with analytics enables rapid scaling and localized production. This vertical shows strong interest in flexible automation and cloud-based manufacturing platforms.

REGIONAL INSIGHTS

Geographically, the market is segmented across five major regions: North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Industry 4.0 Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North American companies are increasingly embracing smart manufacturing, and the region is expected to dominate the market. The majority of factories operating in the market are now equipped with new machinery and smart factory technology, enabling other businesses to transition from conventional to smart manufacturing. Major players operating in the market, government initiatives, and increasing funding for research and development activities are vital factors that make North America a dynamic region for the growth of the market. The North America held the dominant share in 2026 valuing at USD 64.94 Billion and also took the leading share in 2025 with USD 55.83 Billion.

North America Industry 4.0 market analysis indicates steady expansion supported by advanced manufacturing infrastructure and strong technology ecosystems. The region contributes a significant share of the global Industry 4.0 market size, driven by productivity-focused investment. Enterprises prioritize automation, analytics, and cybersecurity. Favorable business environments and digital readiness support sustained adoption.

United States Industry 4.0 Market

The United States industry 4.0 market leads regional growth through large-scale industrial modernization and software-driven innovation. Manufacturers invest heavily in smart factories and industrial analytics to address labor constraints. Federal initiatives and private capital reinforce technology deployment, while competitive intensity accelerates adoption.

Europe

Europe had the second-largest share of the global Industry 4.0 market in 2021. The European industry has made a substantial investment in technologies and skills to maintain its position in the global market. The deployment of connected objects and automation has transformed German manufacturing and ushered in the fourth industrial revolution. The establishment of connectivity, networked objects, real-time data processing, and ubiquitous information is shifting paradigms in industries. Tech giants, including Siemens, Honeywell, and General Electric, are among the early adopters of i4.0 and are far ahead in its implementation.

The European Industry 4.0 market analysis reflects strong alignment with regulatory frameworks and industrial standards. The region emphasizes interoperability, sustainability, and workforce integration. Europe maintains a sizable share of the Industry 4.0 market, supported by advanced engineering capabilities and coordinated policy support.

Germany Industry 4.0 Market

Germany's Industry 4.0 market performance remains influential, driven by its leadership in industrial automation and standards development. German manufacturers are adopting Industry 4.0 to preserve global competitiveness and strengthen export performance. Strong integration between equipment suppliers and manufacturers sustains innovation.

United Kingdom Industry 4.0 Market

The United Kingdom Industry 4.0 market demonstrates selective, yet accelerating, adoption. Investment focuses on advanced manufacturing, aerospace, and automotive sectors. Digital skills initiatives and industrial strategy reforms support market growth despite macroeconomic uncertainty.

Asia-Pacific

The Asia Pacific market is led by Japan, China, and South Korea, driven by their extensive efforts to adopt industrial automation and implement disruptive technologies across their manufacturing value chains. The plan encompasses the top 10 industries, including semiconductors, advanced robotics, electric cars, and artificial intelligence. This state-driven industrial policy aims to make China dominant in global high-tech manufacturing and draws inspiration from the German government’s i4.0 development plan. Japan launched its Society 5.0 program to address economic, social, and industrial challenges.

- For instance, in September 2020, Siemens AG launched an Advanced Manufacturing Transformation Center (AMTC) in Southeast Asia to support i4.0. This will provide training, support, and guidance to companies in Southeast Asia.

Asia-Pacific Industry 4.0 market analysis shows the fastest growth globally, driven by large-scale industrial expansion and government-led digitization programs. The region’s Industry 4.0 market growth is driven by manufacturing scale, rising automation intensity, and infrastructure investment.

Japan Industry 4.0 Market

Japan's Industry 4.0 market adoption emphasizes precision manufacturing and the integration of robotics. Japanese firms focus on smart automation to address workforce aging and maintain quality leadership. A strong industrial heritage supports gradual yet sustained deployment.

China Industry 4.0 Market

China's Industry 4.0 market expansion reflects national industrial upgrading priorities. Large manufacturers invest aggressively in smart factories, IIoT platforms, and domestic automation technologies. Policy support and scale advantages position China as a major contributor to global growth.

To know how our report can help streamline your business, Speak to Analyst

Latin America & Middle East America

Latin America Industry 4.0 market analysis indicates emerging adoption driven by manufacturing modernization and nearshoring trends. Investment remains uneven but accelerates in the automotive and consumer goods sectors. Infrastructure gaps present challenges alongside long-term opportunities. The Middle East and Africa Industry 4.0 market analysis shows early-stage adoption concentrated in energy, utilities, and industrial hubs. Digital transformation supports operational efficiency and diversification strategies. Adoption remains selective due to capital constraints and skills availability.

In Latin America, the Middle East & and Africa, the fourth industrial revolution is supported by government initiatives and the realization of the significance of adopting digital technologies to sustain the global market. For instance, in October 2020, the Middle East government planned to develop the Industry 4.0 revolution by forming a partnership with the World Economic Forum. The progress in the UAE's economy also underscores its capacity to become a world leader by addressing key challenges in digital transformation and technological advancement. The strategy is designed to strengthen its position as a global hub and expand its support for the national economy. Also, in Brazil, leading players have partnered to accelerate the deployment of technological assets and speed up the adoption of advanced technologies.

Industry 4.0 Industry Competitive Landscape

Key Players are Adopting Several Strategies, such as Mergers and acquisitions, to maintain their Position in the Market.

Oracle Corporation, Cisco Systems Inc., and others are some of the major players in the market. They are currently deploying advanced solutions integrated with digital twins and 3D printing, among others. Additionally, intense market competition is forcing key players to focus on acquisition strategies to strengthen their positions. For instance,

- February 2021 – Software and SAP SE partnered to combine SAP's S/4HANA Cloud with Software AG's analytics platform, TrendMiner. This alliance will bring sensor-generated data into analytics for companies seeking Industry 4.0 solutions.

- February 2021 – ABB Ltd. launched GoFa to assist workers with ergonomic and repetitive tasks. Further, the launch will support the growing demand for robots that are capable of handling heavier payloads to enhance flexibility and productivity.

- March 2020 - Cisco Systems Inc. collaborated with Microsoft Corporation to allow seamless data orchestration from Cisco IoT Edge to Azure IoT Cloud. This collaboration will empower customers to get a pre-integrated IoT edge-to-cloud application solution and a seamless flow of data through the IoT edge.

The Industry 4.0 market competitive landscape is characterized by a mix of global automation incumbents, industrial software specialists, cloud service providers, and niche technology firms. Market positioning increasingly depends on the ability to deliver integrated, interoperable solutions that span hardware, software, and lifecycle services. Vendors with strong portfolios across industrial automation, analytics, and connectivity capture a larger share of the Industry 4.0 market by addressing complex, multi-site deployment needs.

Established automation providers leverage deep domain expertise, installed base advantage, and long-term customer relationships. Their strengths lie in reliability, safety compliance, and global service networks. However, these firms often face challenges in software agility and cloud-native innovation, prompting strategic partnerships and acquisitions. Their competitive strategies focus on expanding digital platforms and embedding intelligence into traditional control systems.

Industrial software and platform providers differentiate through advanced analytics, artificial intelligence, and digital twin capabilities. These players benefit from faster innovation cycles and scalable architectures. Their primary weakness remains limited control over physical assets, requiring close collaboration with equipment manufacturers. Strategy centers on ecosystem development and vertical-specific solutions.

Cloud and technology companies play an increasingly influential role by providing infrastructure, data platforms, and edge computing services. Their strengths include scalability, cybersecurity investment, and developer ecosystems. Constraints arise from limited industrial process knowledge and concerns over data sovereignty. The strategic focus emphasizes hybrid architectures and alignment with compliance.

Smaller specialized firms contribute innovation in areas such as machine vision, predictive maintenance, and edge analytics. While technologically advanced, they face challenges with scaling and integration. Overall, competitive intensity drives consolidation, partnership formation, and a shift toward outcome-based value propositions.

LIST OF KEY COMPANIES PROFILED:

- ABB Ltd (Switzerland)

- Siemens AG (Germany)

- Cognex Corporation (U.S.)

- Schneider Electric SE (France)

- Honeywell International Inc. (U.S.)

- Emerson Electric Co. (U.S.)

- Rockwell Automation, Inc. (U.S.)

- General Electric Company (U.S.)

- Robert Bosch GmbH (Germany)

- Cisco Systems Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- January 2024: Siemens expanded its industrial digitalization portfolio through enhanced integration of artificial intelligence within its automation software suite, aiming to improve predictive maintenance and real-time production optimization across discrete manufacturing environments.

- June 2024: Rockwell Automation announced a strategic collaboration with cloud technology partners to strengthen industrial edge analytics capabilities, targeting improved data processing latency and cybersecurity resilience for large-scale smart factory deployments.

- October 2024: Schneider Electric advanced its Industry 4.0 offerings by introducing sustainability-focused digital manufacturing tools designed to integrate energy optimization, emissions monitoring, and production efficiency within unified industrial platforms.

- March 2025: ABB launched next-generation robotics and automation solutions incorporating machine learning and autonomous control features, supporting flexible manufacturing and faster changeover in automotive and electronics production lines.

- August 2025: Honeywell strengthened its industrial Internet of Things capabilities through platform enhancements focused on asset performance management and remote operations, addressing reliability and safety requirements in energy and process industries.

REPORT COVERAGE

The research report provides an in-depth analysis of the Industry 4.0 market. It focuses on key aspects, including leading companies, applications, and the adoption of advanced technologies across several industry verticals. In addition, it offers insights into market trends and highlights key industry developments. In addition to the aforementioned factors, the report also highlights several key factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Application, Vertical, and Region |

|

By Application |

|

|

By Vertical |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market is expected to reach USD 801.49 billion by 2034.

Fortune Business Insights says that the market value stood at USD 205.91 billion in 2025.

The market is expected to grow at a CAGR of 16.3% in the forecast period (2026-2034).

By application, the industrial IoT segment is expected to lead the market during the forecast period.

The increased adoption of industrial robots is one of the key drivers.

Siemens AG, Cognex Corporation, Schneider Electric SE, Honeywell International Inc., Emerson Electric Co., Rockwell Automation, Inc., General Electric Company, and Robert Bosch GmbH are the top companies in the market.

By vertical, manufacturing segment holds the major market with a share of 27.12% in 2025.

(Note that, the purpose of the below list is to highlight the exhaustiveness of study that goes into understanding the ecosystem and/or estimating the market size

This does not necessarily mean that all the below companies are profiled in the report. Kindly refer Companies Profiled Section for more details on the list of companies profiled in the report.

However, at the same, we are open to profile additional company(s) on specific request)

- ABB Ltd

- AIBrain

- Amazon Web Services

- Ansys

- BASLER AG

- Cisco Systems, Inc.

- Cognex Corporation

- Denso Corporation

- Emerson Electric Co.

- Fanuc Corporation

- General Electric Company

- General Vision

- Google Inc

- Hewlett Packard Enterprise Company

- Honeywell International Inc.

- Intel Corporation

- International Business Machines Corporation

- KUKA

- L&T Technology Services (LTTS)

- Microsoft Corporation

- Mitsubishi Electric Corp.

- QUALCOMM INC.

- Robert Bosch GmbH

- Rockwell Automation, Inc.

- SAP SE

- Schneider Electric SE

- Siemens AG

- Stratasys LTD.

- U-BLOX

- Yaskawa

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us