Industrial Automation Market Size, Share & Industry Analysis, By Component (Hardware, Software), By Industry (Discrete Automation, Process Automation), and Regional Forecast, 2026-2034

Industrial Automation Market Size & Industry Overview

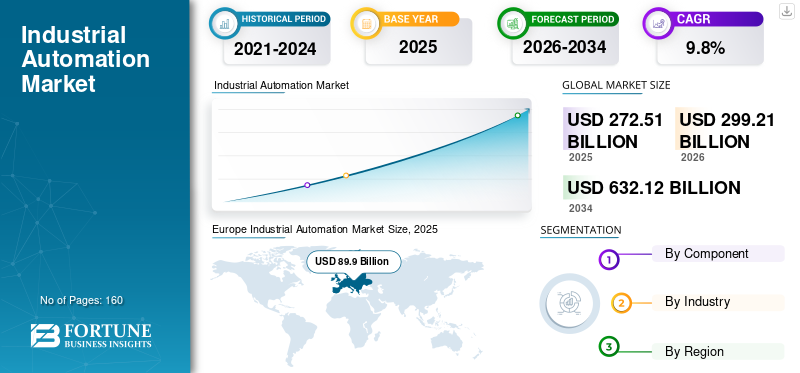

The global industrial automation market size was estimated at USD 272.51 billion in 2025. The market is expected to rise from USD 299.21 billion in 2026 to USD 632.12 billion by 2034, expanding at a CAGR of 9.80% from 2026 to 2034. Europe dominated the industrial automation market with a market share of 32.99% in 2025.

Europe accounted for a market value of USD 89.9 billion in 2025. In the research report, we have studied the solutions offered by market players such as Emerson Electric Co. Its automation solutions include Programmable Automation Controllers, Industrial I/O, Motion Control, Automation/Control Software, Panel & Industrial PCs, Industrial Web Panels, and Industrial Monitors. Similarly, ABB’s automation products include Control Systems, Turbocharging, and Programmable Logic Controllers.

The advent of 5G wireless technology and the increasing adoption of industry 4.0 are surging the demand for automation solutions across sectors. Expansion of augmented reality (AR), digital twin, digitalization, and industrial IoT is expected to be significant indicators of the global industrial automation market growth. For instance, in July 2021, Rockwell Automation Inc. collaborated with a cloud-based product digitalization and traceability platform, Kezzler AS. The partnership aims to enable manufacturers to capture their product's end-to-end journey from raw material sources to the point of sale or beyond by using cloud-based chain solutions.

Download Free sample to learn more about this report.

Industrial Automation Market Key Takeaways

- 2025 Market Size: USD 272.51 billion

- 2026 Market Size: USD 299.21 billion

- 2034 Forecast Market Size: USD 632.12 billion

- CAGR: 9.80% from 2026–2034

- Europe dominated the industrial automation market with a 32.99% share in 2025.

- The software segment is expected to hold a major market share during the forecast period.

- The discrete automation industry segment is projected to account for 29.1% of the market in 2026.

Europe

Europe led the market with a valuation of USD 89.9 billion in 2025.

Asia Pacific

Asia Pacific is anticipated to witness significant growth driven by strong robotics and factory automation adoption.

North America

North America is expected to record substantial growth due to advanced manufacturing capabilities and efficient trade practices.

U.S.

Increasing adoption of advanced manufacturing technologies is supporting industrial automation growth.

Japan

Strong presence of robotics and factory automation manufacturers continues to drive market expansion.

Read More

Industrial Automation Market TRENDS

Increasing Implementation of Digital Twins and AR Technology in Manufacturing to Favor Market Growth

Digital twin helps organizations understand the feasibility, reduce risk during implementation and estimate potential improvements. With the advent of the industrial Internet of Things, such as cloud systems and smart sensors, digital twin implementation and maintenance have become more manageable. Organizations incorporate digital twin technology into their business operations to reduce the risk of equipment failure. It also helps to automatically schedule the repairs by creating a simulation of the process. For instance, in July 2019, DHL International GmbH, a German logistics company, integrated a supply chain solution using a digital twin for Tetra Pak’s warehouse. It would help deliver scalable, cost-effective, and agile supply chain operations. Internet of Things (IoT) technology is incorporated in transport vehicles to create a digital twin. It keeps shipment of essentials, such as foods and drinks, safe from farm to consumer. Such rising adoption of digital twin technology is attributed to the increasing demand for automation solutions in the coming years.

Download Free sample to learn more about this report.

Disruptive technologies such as augmented reality (AR) and virtual reality (VR) help in automating business and operational performance. Organizations are leveraging AR to upskill their employees to handle digital operations. Market players are incorporating AR technology with their manufacturing tools. For instance, Siemens offers Assist AR, an augmented reality solution that automates the process of assembly, maintenance, and inspection & extracting 3D models from digital manufacturing software and Siemens PLM. Such solutions are likely to foster the demand for automation solutions in the coming years.

Rising Adoption of Industrial IoT to Boost Market Value

The IoT plays a crucial role in automation technology as IoT helps create and streamline effective, affordable, and responsive systems architectures. Industrial IoT (IIoT) solutions help connect industrial assets, create transparency quickly and easily, and increase productivity. IIoT and edge computing solutions help to simplify device management and shop floor software across the entire lifecycle. Hence, organizations deploy IIoT solutions to automate the manufacturing process and provide a better customer experience. Such rapid adoption of IIoT solutions across industries is expected to foster market growth.

Industrial IoT solutions leverage artificial intelligence (AI), advanced analytics, edge computing, and cloud computing to analyze machine data and get meaningful insights to optimize asset productivity and availability. For instance, Siemens offers industrial IoT solutions: IndustrialEdge, MindSphere, and Mendix, which provide insights from industrial data using advanced technologies such as AI, edge computing, cloud, and advanced analytics. Schmalz, a vacuum automation and ergonomic handling solution provider leverages Siemens Industrial IoT's capabilities to enhance customer maintenance and extended analytics services. Hence, such growing expansion of Industrial IoT across industries is likely to drive the market growth in the upcoming years.

DRIVING FACTORS

Fourth Industrial Revolution to Embrace Partnerships and Collaborations in Global Market

Industry 4.0 has transformed the digital supply chain across industries. Customers’ changing requirements such as personalized and instantaneous services force organizations to embrace industry 4.0. With rapid technology evolution, the market players partner with techno-savvy companies to develop new solutions built upon proven technologies. For instance, in February 2020, Honeywell International Inc. and Tech Mahindra Limited partnered to develop digitized “Factories of the Future” by leveraging digital technologies. The collaboration aims to accelerate the digital transformation journey by empowering manufacturers. Similarly, Siemens collaborated with SAP SE to offer industry4.0-enabled business processes to enterprises. These processes will allow building a digital thread for the complete product lifecycle.

With such partnerships and collaborations, companies are focusing on capitalizing on 5G, industry 4.0, and digital transformation & software capabilities to enable the manufacturers to scale up their growth and realize the potential of industry 4.0 technologies and solutions. Such partnerships and collaborations are anticipated to boost the demand for automation solutions across industries in the coming years.

RESTRAINING FACTORS

High Initial Capital Investments to Impede Market Growth

Industrial automation processes are cost-effective, but the initial capital cost required for the implementation of technology and training employees is high. Further, the return on investment (ROI) cannot be predicted, owing to the fragmented nature of the industry. High upfront costs and unpredictable return on investment make small and medium-sized enterprises (SMEs) hesitant to adopt the benefit of technology. However, smart manufacturing and government policies, such as the Government of India MSME business loan scheme and Make in India movement, are likely to overcome this restraint and create market opportunities for the solutions shortly.

INDUSTRIAL AUTOMATION MARKET SEGMENTATION ANALYSIS

By Component Analysis

Increasing Demand to Streamline Business Process is Driving Adoption of Automation Software

Based on component, the industrial automation market is classified into hardware and software. Software is likely to hold a major market share during the forecast period. Automation software includes human-machine interface (HMI), manufacturing operations management (MOM) software, supervisory control, and data acquisition (SCADA). It enables businesses to streamline the manufacturing process. The hardware segment is projected to showcase rapid growth during the forecast period, owing to IoT's increasing demand for advanced automation processes in the industries.

By Hardware Analysis

Developments in Technology to Boost Innovations in Industrial Robots

The hardware segment comprises sensors, Programmable Logic Controller (PLC), Human-Machine Interface (HMI), servo, laser markers, safety light curtain, and robots. Servo is anticipated to hold a major market share, followed by sensors within the hardware. The robots are projected to show a remarkable growth rate. With advancements in technology and the emergence of Industry 4.0, market players are introducing advanced robots for automation purposes. For instance, in January 2021, Omron Corporation launched the i4 series SCARA robot, which automates high-precision, high-speed assembly, and transportation processes. Similarly, in May 2020, Mitsubishi Electric Corporation launched Melfa Assista, a series of robots that collaboratively works with humans.

By Sensors Analysis

Inductive Sensors to Account for Major Industrial Automation Market Share

Sensors are further classified into photoelectric, laser, inductive, and others. Inductive sensors are projected to hold a major market share due to their capabilities such as a large degree of mounting flexibility, weld field immunity, and robust metallic detection. The photoelectric sensor is estimated to exhibit notable growth, owing to its capabilities such as detecting a change in surface condition and detecting objects through several optical properties. Market players introduce advanced sensors to collect data from automated systems and provide analysis and decision-making. For instance, in February 2019, Rockwell Automation launched a new photoelectric sensor, “Allen-Bradley 42AF RightSight M30”, designed for long-distance detection and improving environmental resistance.

By Servo Analysis

Intricate Position Control to Surge Demand for Servo Motors and Drives

Servo is classified into motor and drive. Servo motors and drives are the machinery's essential components that require intricate position control such as camera focus, conveyor belt, and robotics automation. Servo drives are expected to hold the highest market share. Schneider Electric offers a comprehensive range of servo drives, including Lexium XX series servo drives and Unilink servo drives. Servo motors are expected to grow with the highest CAGR during the forecast period. Market players are introducing new servo motors for automation systems. For instance, in May 2021, IQ Motion Control, an electric motors and controller manufacturer, launched a new range of servo motors for robotics and industrial applications.

By Motor Analysis

DC Motors to be Preferred Solution for Industrial Applications

Based on motor type, servo motor is further categorized into AC motor and DC motor. DC motors are expected to hold a major market share during the forecast period. DC motors are used explicitly in applications designed to move heavy loads in industrial automation applications. For instance, Portescap expanded the DC motors platform by introducing 22ECP-2A motors with a new amalgamated driver. Such factors contribute to the growth of DC motors across industrial applications. AC motors are likely to grow with the highest CAGR during the forecast period. It is expected to witness a significant adoption attributed to low maintenance and reduced costs.

By Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Discrete Automation to Drive Demand for Automation Solutions

By industry, the industrial automation market is classified into discrete automation and process automation. The discrete automation industry is expected to hold a major market share during the forecast period, with a share of 29.1% in 2026. The discrete automation industry is further segmented into automotive, electronics, heavy manufacturing, packaging, and others. Automotive and heavy manufacturing industries are likely to surge the demand for automation solutions.

The process automation industry is sub-categorized into oil & gas, chemicals, pulp & paper, mining and metals, healthcare, and others. The mining and metals industry is projected to hold a major market share, followed by healthcare, oil & gas, and chemicals.

REGIONAL ANALYSIS

Europe to Dominate Global Market Attributed to Highest Robot Density Globally

Geographically the market is analyzed across five major regions, including North America, Europe, Asia Pacific, the Middle East & Africa, and South America. These regions are further categorized into countries.

Europe

Europe Industrial Automation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Europe Industrial Automation Market size was valued at USD 89.9 Billion in 2025. Industrial automation market share for Europe reached around 33% of the global revenue in 2021. In January 2021, the International Federation of Robotics (IFR) stated that, by region, Western Europe (225 units per 10,000 employees) and Nordic European Countries (204 units per 10,000 employees) had maximum robot density worldwide. Germany ranks fourth among the top automated countries globally, with 346 units per 10,000 employees. These are some of the key factors that contribute to the major share of the region.

Asia Pacific

Asia Pacific is anticipated to showcase a significant growth rate during the forecast period 2022-2029. Japan is the largest producer of robots and factory automation systems. The presence of robotics & factory automation products and manufacturing companies, such as Omron Corp., Yaskawa Electric, Yokogawa Electric, Mitsubishi Electric, and Nidec Corp., across Japan contributes to the industrial automation demand in the region.

China

China is a major producer of sensors, batteries, microchips, and other components used in the IoT system. In addition, in India, government initiatives such as Make in India and MSME support small and medium-sized businesses to adopt advanced manufacturing solutions. Such active initiatives by the government are expected to propel market growth in this region.

To know how our report can help streamline your business, Speak to Analyst

North America

North America will witness significant growth in the coming years due to manufacturers' advanced production capabilities and efficient trading practices. The Middle East & Africa is projected to have notable growth in the coming years. With increasing digital transformation process, the adoption of artificial intelligence and robotic process automation is gaining traction in the region South America is estimated to represent a steady market growth. Brazil with growing demand for advance technologies showcases vast opportunity for automation players.

KEY INDUSTRY PLAYERS

Market Players are Developing Innovative Applications for Robotics and Automation Solutions Driven by Significant Investments

The market players are involved in mergers & acquisitions, partnerships, and collaborations to expand the market presence. The key players operating in the market include ABB Ltd, Rockwell Automation, and Honeywell International, which are developing innovative applications for robotics and automation solutions to achieve new growth potential. For instance, ABB Ltd. invests approximately 5% in research and development to expand its product portfolio focusing on machine-centric robotics, digital factory automation, collaborative robotics, and artificial intelligence.

Similarly, in June 2018, PTC partnered with Rockwell Automation. In this partnership, Rockwell Automation invested USD 1 billion in PTC. With this partnership, the companies aligned Vuforia augmented reality (AR), PTC’s Thingworx Internet of Things (IoT), Kepware industrial connectivity with Rockwell’s FactoryTalk MES FactoryTalk Analytics, and other automation platforms.

LIST OF KEY COMPANIES PROFILED:

- ABB Ltd. (Switzerland)

- Emerson Electric Co. (U.S.)

- General Electric Company (U.S.)

- Honeywell International Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Omron Corporation (Japan)

- Rockwell Automation Inc. (U.S.)

- Schneider Electric SE (France)

- Siemens AG (Germany)

- Yokogawa Electric Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

- July 2021-Rockwell Automation Inc. collaborated with a cloud-based product digitalization and traceability platform, Kezzler AS. The partnership aims to enable manufactures to capture their product's end-to-end journey from raw material sources to the point of sale or beyond by using cloud-based chain solutions.

- July 2021- Siemens AG expanded partnership with SAP SE to deliver a new solution for the services and asset lifecycle management. The partnership aims to connect plant floor operations, product development through digital twins, and remote condition monitoring with original equipment manufacturers (OEMs) to facilitate collaboration across the asset lifecycle.

- June 2021- Rockwell Automation Inc. acquired Plex Systems, a smart manufacturing solution provider, for USD 2.22 billion. The acquisition aims to expand industrial cloud offerings with Plex Systems’ cloud-native smart manufacturing platform.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The global industrial automation market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the advanced market over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

Component, Industry, and Geography |

|

By Component |

|

|

By Industry |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to reach USD 632.12 billion by 2034.

In 2025, the market value stood at USD 272.51 billion.

Growing at a CAGR of 9.8%, the market will exhibit steady growth in the forecast period (2026-2034).

Software is expected to be the leading segment in this market during the forecast period.

Increasing deployments of fifth-generation wireless technology, industrial IoT, industry 4.0, smart factories, and robotics are major factors driving the market growth.

ABB Ltd., Rockwell Automation Inc., Emerson Electric Co., Schneider Electric SE, Honeywell International Inc., and Mitsubishi Electric Corporation are some of the major players in the global market.

Europe dominated the market share.

Asia Pacific is expected to exhibit the highest growth rate during the forecast period.

Below is the list of companies that are studied in order to estimate the market size and/or understanding the market ecosystem

This list does not necessarily mean that all the below companies are profiled in the report. The report includes profiles of only the top 10 players based on revenue/market share.

Industrial Automation Market

- Siemens

- ABB

- Emerson Process Management

- Rockwell automation

- Schneider Electric

- Honeywell process solutions

- Mitsubishi electric

- Yokogawa electric

- Omron automation

- Danaher Industrial Ltd

- FANUC America Corporation

- PHOENIX CONTACT

- SmartClean Technologies Pte. Ltd.

- JM VisTec System

- B&R

- Festo Inc.

- SAVCOS AUTOMATION PTE LTD.

- Quadrant Technologies

- Hitech Digital Solutions LLP.

- SMEC AUTOMATION PVT. LTD.

- SESTO Robotics.

- Xiaoxin Machines Pte Ltd.

- Accuron Technologies

- Electrotek Pte Ltd.

- Genics Electortech Pvt. Ltd.

- TVARIT GmbH

- Flexciton Ltd

- Metis Labs

- Elaratech Automation

- Automi AI

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us