Warehousing and Distribution Logistics Market Size, Share & Industry Analysis, By End-User Industry (Retail, E-commerce & Omnichannel, Food, Beverage & FMCG, Pharmaceuticals & Healthcare, Industrial, Automotive & Chemicals, and Electronics & High-Value Goods), By Mode of Transport (Road, Rail, Sea/Waterways, & Air), By Distribution Channel (Retail & Store Replenishment, Wholesale & Distributor Fulfillment, D2C & E-commerce Delivery, and Industrial & Institutional Deliveries), By Service Type (Warehousing services, Distribution services, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

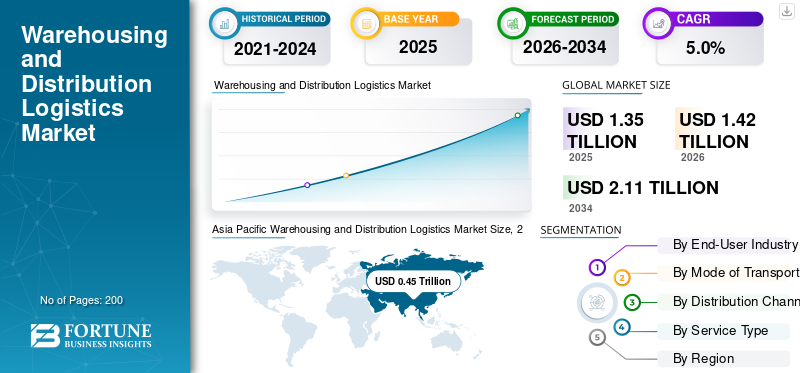

The global warehousing and distribution logistics market size was valued at USD 1.35 trillion in 2025. The market is projected to grow from USD 1.42 trillion in 2026 to USD 2.11 trillion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the global market with a market share of 33.33% in 2025.

The growth of the global warehousing and distribution logistics market is witnessing steady progress, driven by the expansion of e-commerce, rising inventory localization, and increasing outsourcing of logistics operations by manufacturers, retailers, and FMCG companies. Businesses are shifting toward centralized and regional distribution centers to improve service levels, reduce delivery lead times, and enhance inventory visibility. Growth in omnichannel retailing is further increasing demand for fulfillment centers, last-mile distribution, and returns management. Additionally, the rising adoption of automation, warehouse management systems (WMS), robotics, and real-time tracking advanced technologies is improving operational efficiency, accuracy, and scalability across warehousing and distribution networks. Government investments in industrial parks, logistics parks, and multimodal infrastructure are also supporting market expansion, particularly in the Asia Pacific region and emerging economies.

- For instance, in October 2025, DHL Supply Chain announced the expansion of its contract warehousing footprint across Asia and Europe, adding new multi-client distribution centers to support retail, e-commerce, and life sciences customers. The expansion focused on automation-enabled facilities, sustainability initiatives, and integrated warehousing and distribution solutions. Furthermore, major players such as CEVA Logistics, GXO Logistics, Kuehne + Nagel, DB Schenker, and DSV Solutions are emphasizing capacity expansion, digitalization, and value-added services to meet evolving customer requirements and strengthen long-term supply chain partnerships.

Download Free sample to learn more about this report.

WAREHOUSING AND DISTRIBUTION LOGISTICS MARKET TRENDS

Automation and Digitalization Transform Warehouse and Distribution Operations

Automation and digitalization are reshaping the warehousing and distribution logistics industry by improving accuracy, speed, and cost efficiency. Companies are increasingly deploying warehouse management systems, robotics, automated storage and retrieval systems, and data-driven inventory optimization to handle rising order volumes and SKU complexity. Digital tools, including real-time inventory visibility, predictive analytics, and yard management systems, enhance coordination across distribution networks and reduce operational bottlenecks. These technologies enable scalable operations, support omnichannel fulfillment, and mitigate labor dependency, particularly in high-volume e-commerce and retail environments. Automation adoption is becoming a competitive differentiator for service providers seeking long-term contracts.

- In April 2024, Amazon announced the deployment of new AI-enabled robotics systems across multiple global fulfillment centers to improve picking efficiency and order accuracy.

MARKET DYNAMICS

MARKET DRIVERS

E-commerce Expansion and Inventory Localization to Drive Market Growth

The rapid expansion of e-commerce and the strategic shift toward inventory localization are fueling demand for warehousing and distribution logistics globally. Retailers and manufacturers are expanding the number of regional and urban distribution centers to reduce costs, delivery times, and enhance service reliability. Omnichannel fulfillment models require flexible storage, fast order processing, and efficient last-mile coordination, significantly increasing warehousing intensity per unit of sales. Additionally, companies are holding higher safety stock levels to mitigate supply chain disruptions, further boosting demand for storage and distribution services. This structural shift supports significant growth across both mature and emerging markets.

- In September 2023, Walmart expanded its U.S. and international fulfillment center network to support faster e-commerce deliveries and localized inventory positioning.

MARKET RESTRAINTS

Labor Shortages and Rising Operating Costs to Deter Market Development

Labor shortages and rising operating costs present a significant restraint for warehousing and distribution logistics providers. Warehouses are labor-intensive operations, and competition for skilled workers has increased wage pressure, particularly in developed markets. Higher energy costs, real estate prices, and compliance expenses further impact operating margins. Smaller and mid-sized logistics providers often face challenges in absorbing these costs or investing in large-scale automation. Additionally, high team member turnover disrupts operational continuity and increases training costs. These factors collectively constrain profitability and slow capacity expansion in cost-sensitive regions and service segments.

- In August 2023, multiple logistics associations in Europe reported persistent labor shortages in warehouses, prompting operators to increase wages and reassess their operational models.

MARKET OPPORTUNITIES

Growth of Cold Chain and Pharmaceutical Logistics Creates Several Market Opportunities

The expansion of cold chain and pharmaceutical logistics presents a major opportunity for warehousing and distribution service providers. Rising demand for temperature-sensitive food products, biologics, vaccines, and specialty pharmaceuticals is driving investments in controlled and monitored storage facilities. These services command premium pricing due to regulatory compliance, infrastructure intensity, and operational complexity. Emerging markets are witnessing the rapid development of cold chain logistics as healthcare access improves and organized food retail expands. Providers with validated facilities, monitoring systems, and compliance expertise are well-positioned to capture long-term, high-margin contracts in this segment.

- In January 2024, DHL Supply Chain announced the expansion of its life sciences and healthcare warehousing facilities across Asia Pacific to support pharmaceutical cold chain demand.

MARKET CHALLENGE

Managing Network Complexity Across Multi-Node Distribution Systems Presents Challenge to Market Progress

Managing increasing network complexity is a key challenge in global warehousing and distribution logistics market growth. Companies now operate multi-node distribution networks spanning central warehouses, regional DCs, urban order fulfillment centers, and cross-dock facilities. Coordinating inventory flows, transportation schedules, and service-level agreements across these nodes requires advanced planning and system integration. Any disruption, such as IT failures, capacity imbalances, or infrastructure constraints, can cascade across the network. Ensuring consistent service quality while optimizing costs across geographies remains difficult, particularly for providers serving omnichannel and multinational customers.

Download Free sample to learn more about this report.

Segmentation Analysis

By End-User Industry

Retail, E-Commerce, and Omnichannel Segment Lead due to High Order Frequency

Based on end-use industry, the market is segmented into retail, e-commerce & omnichannel, food, beverage & FMCG, pharmaceuticals & healthcare, industrial, automotive & chemicals, and electronics & high-value goods. The retail, e-commerce, and omnichannel segment secures the key warehousing and distribution logistics market share due to high order frequency, large SKU volumes, and growing consumer expectations for fast delivery and easy returns. Companies are expanding regional and urban fulfillment centers to support same-day and next-day deliveries, significantly increasing warehousing intensity. This segment benefits from sustained online retail growth and inventory localization strategies.

The industrial, automotive & chemicals segment is expected to witness the fastest-growth, with a CAGR of 7.2% over the forecast period.

- In October 2024, Amazon expanded multiple last-mile and fulfillment facilities across North America and Europe to support faster omnichannel deliveries.

To know how our report can help streamline your business, Speak to Analyst

By Mode of Transport

Road Segment Captures the Key Market Share due to Its Flexibility

Based on mode of transport, the market is segmented into road, rail, sea/waterways, and air. The road segment dominates due to its flexibility, door-to-door connectivity, and critical role in first-mile and last-mile distribution from warehouses and distribution centers. It supports retail replenishment, e-commerce deliveries, and industrial shipments, making it indispensable across regions. Even as rail and air grow for specific use cases, road-based distribution remains central to warehousing-linked logistics operations.

The rail segment is projected to grow at a CAGR of 5.7% over the forecast period.

- In July 2023, the U.S. Department of Transportation increased funding for road freight infrastructure under federal logistics and supply chain programs.

By Distribution Channel

Retail & Store Replenishment Fulfillment Accelerates Distribution Channel Transformation

Based on distribution channel, the market is segmented into retail & store replenishment, wholesale & distributor fulfillment, Direct-to-Consumer (D2C) & e-commerce delivery, and industrial & institutional deliveries. The Retail & Store Replenishment segment dominates the market, driven by rising online sales, brand-owned digital platforms, and consumer demand for fast home delivery. This channel requires highly automated warehouses, parcel-level picking, and efficient last-mile coordination, which significantly increases the logistics service value per order.

The Direct-to-Consumer (D2C) & e-commerce delivery segment is projected to grow at a CAGR of 7.3% over the forecast period.

- In March 2024, Walmart expanded its automated e-commerce fulfillment centers to support growing D2C and online grocery demand.

By Service Type

Warehousing Services Segment Leads the Market due to its Improved Visibility

Based on service type, the market is segmented into warehousing services, distribution services, and integrated warehousing & distribution services. The warehousing services segment dominates as customers increasingly prefer single-provider, end-to-end logistics solutions to reduce complexity, improve visibility, optimize costs, and increase cost-effectiveness with customer satisfaction. Integrated contracts allow better coordination between inventory management and outbound distribution, particularly for retail, FMCG, and e-commerce customers. Long-term outsourcing agreements and digital platform integration further support this segment’s leadership.

The integrated warehousing & distribution service segment is projected to experience the fastest-growth, with a CAGR of 5.6% over the forecast period.

- In February 2024, DHL Supply Chain announced new multi-year integrated logistics contracts with global retail and FMCG customers.

WAREHOUSING AND DISTRIBUTION LOGISTICS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Warehousing and Distribution Logistics Market Size, 2025 (USD Trillion)

To get more information on the regional analysis of this market, Download Free sample

North America represents a mature yet resilient warehousing and distribution logistics market, driven by the adoption of advanced contract logistics, dense distribution center networks, and high e-commerce penetration. The U.S. and Mexico play complementary roles, with the U.S. leading in automation, large-scale fulfillment, and omnichannel logistics, while Mexico benefits from nearshoring and cross-border distribution activity. Continued investment in robotics, warehouse management systems, and cold storage supports steady growth, despite rising labor and real estate costs.

U.S. Warehousing and Distribution Logistics Market

The U.S. market is characterized by large, highly automated fulfillment centers, strong penetration of third-party logistics, and advanced last-mile networks that support e-commerce, retail, and healthcare distribution. Growth is further supported by nearshoring, inventory localization, and sustained consumer demand.

Europe

Europe’s warehousing and distribution logistics market is stable and highly structured, supported by dense retail networks, strong FMCG and pharmaceutical supply chains, and high outsourcing levels. Growth is moderate due to market maturity; however, demand remains resilient, driven by omnichannel retailing, regulatory-driven inventory decentralization, and cross-border trade within Europe. Sustainability requirements and energy efficiency investments are increasingly shaping warehouse design and operational strategies across major economies.

U.K. Warehousing and Distribution Logistics Market

The U.K. market benefits from strong e-commerce adoption, advanced fulfillment infrastructure, and a high concentration of urban distribution centers. Retail and grocery logistics drive demand, while investments in automation offset labor constraints and rising operating costs.

Germany Warehousing and Distribution Logistics Market

Germany serves as Europe’s logistics hub, supported by robust industrial output, extensive automotive supply chains, and its central geographic positioning. High warehouse utilization, advanced automation adoption, and cross-border distribution activity underpin steady demand for warehousing and distribution services.

Asia Pacific

Asia Pacific is the fastest-growing and largest regional market, driven by manufacturing scale, rapid e-commerce expansion, and rising domestic consumption. China, India, and Southeast Asia are seeing significant investments in mega distribution centers, urban fulfillment hubs, and cold chain infrastructure. Growing pharmaceutical and electronics distribution, combined with improving logistics infrastructure, supports sustained high growth across both developed and emerging economies.

China Warehousing and Distribution Logistics Market

China dominates regional demand due to its manufacturing scale, massive domestic consumption, and highly developed e-commerce ecosystem. Investments in automated warehouses, same-day delivery networks, and regional distribution hubs continue to expand warehousing intensity.

Japan Warehousing and Distribution Logistics Market

Japan’s market is mature but technology-driven, with strong adoption of automation, robotics, and precision inventory management. High service-level expectations, pharmaceutical distribution, and efficient retail replenishment networks support demand.

India Warehousing and Distribution Logistics Market

India is a high-growth market, driven by the expansion of e-commerce, organized retail, and pharmaceutical distribution. Government logistics parks, GST-driven warehouse consolidation, and the rising adoption of third-party logistics support rapid capacity expansion.

Rest of the World

The Rest of the World, including Latin America and the Middle East & Africa, is experiencing steady growth as modern warehousing and organized distribution networks expand. Infrastructure investments, free trade zones, and rising consumer markets support demand. Growth is strongest in Gulf countries and select African and Latin American economies, driven by retail expansion, healthcare logistics, and the development of regional trade hubs.

COMPETITIVE LANDSCAPE

Key Industry Players

Automation-Driven Operations, Integrated Service Models, and Network Expansion Shape Market Competitiveness

The global warehousing and distribution logistics market is characterized by increasing automation, integrated service offerings, and the expansion of multi-regional networks. Leading players, or logistics companies including DHL Supply Chain, GXO Logistics, Kuehne + Nagel, DSV Solutions, CEVA Logistics, DB Schenker, and GEODIS, compete through large-scale contract warehousing, technology-enabled fulfillment, and end-to-end distribution solutions. Companies strengthen competitiveness by investing in robotics, warehouse management systems, data analytics, and sustainable facility design. Strategic initiatives include expanding the footprint in high-growth regions, securing long-term outsourcing contracts, and enhancing sector-specific capabilities in e-commerce, FMCG, pharmaceuticals, and cold chain logistics to improve efficiency, scalability, and customer retention.

LIST OF KEY WAREHOUSING AND DISTRIBUTION LOGISTICS COMPANIES PROFILED

- DHL Supply Chain (Germany)

- Kuehne + Nagel – Contract Logistics (Switzerland)

- DSV Solutions (Denmark)

- CEVA Logistics (France)

- DB Schenker – Contract Logistics (Germany)

- XPO Logistics (U.S.)

- GXO Logistics (U.S.)

- Ryder Supply Chain Solutions (U.S.)

- UPS Supply Chain Solutions (U.S.)

- GEODIS (France)

- FedEx Supply Chain (U.S.)

- Nippon Express (NX Group) (Japan)

- Kintetsu World Express (Japan)

- Yusen Logistics (Japan)

- CJ Logistics (South Korea)

KEY INDUSTRY DEVELOPMENTS

- December 2025- DHL Supply Chain announced a five-year strategic alliance with Robust. AI to deploy collaborative Carter robots in Mexico, enhancing operational efficiencies and automation in retail warehousing and boosting productivity and safety through scalable robotics integrations in its warehouse management systems.

- December 2025- Mahindra Logistics expanded its warehouse leasing footprint across Telangana, Pune, and Northeast India, strategically targeting emerging industrial corridors to meet rising logistics demand and strengthen distribution capacity in India’s fast-growing supply chain market.

- July 2025- GXO Logistics and Blue Yonder announced a global strategic agreement to integrate warehouse and logistics capabilities with real-time forecasting and data insights, delivering enhanced inventory flexibility, process visibility, and faster speed-to-market for high-volume warehouse operations.

- July 2025- GXO Logistics and Blue Yonder announced a global strategic agreement to integrate warehouse and logistics capabilities with real-time forecasting and data insights, delivering enhanced inventory flexibility, process visibility, and faster speed-to-market for high-volume warehouse operations.

- May 2025- DHL Group signed a strategic Memorandum of Understanding (MoU) with Boston Dynamics to deploy over 1,000 additional Stretch robots globally, accelerating warehouse automation and expanding applications such as case picking and container unloading to improve efficiency, resilience, and scalability across its distribution network.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.0% from 2026 to 2034 |

|

Unit |

Value (USD Trillion) |

|

Segmentation |

By End-User Industry, By Mode of Transport, By Distribution Channel, By Service Type, and By Region |

|

By End-User Industry |

· Retail, E-commerce & Omnichannel · Food, Beverage & FMCG · Pharmaceuticals & Healthcare · Industrial, Automotive & Chemicals · Electronics & High-Value Goods |

|

By Mode of Transport |

· Road · Rail · Sea/Waterways · Air |

|

By Distribution Channel |

· Retail & Store Replenishment · Wholesale & Distributor Fulfillment · Direct-to-Consumer (D2C) & E-commerce Delivery · Industrial & Institutional Deliveries |

|

By Service Type |

· Warehousing services · Distribution services · Integrated warehousing & distribution service |

|

By Geography |

· North America (By End-User Industry, By Mode of Transport, By Distribution Channel, By Service Type, and By Country) o U.S. (By Mode of Transport) o Canada (By Mode of Transport) o Mexico (By Mode of Transport) · Europe (By End-User Industry, By Mode of Transport, By Distribution Channel, By Service Type, and By Country) o Germany (By Mode of Transport) o U.K. (By Mode of Transport) o France (By Mode of Transport) o Rest of Europe (By Mode of Transport) · Asia Pacific (By End-User Industry, By Mode of Transport, By Distribution Channel, By Service Type, and By Country) o China (By Mode of Transport) o Japan (By Mode of Transport) o India (By Mode of Transport) o South Korea (By Mode of Transport) o Rest of Asia Pacific (By Mode of Transport) · Rest of the World (By End-User Industry, By Mode of Transport, By Distribution Channel, and By Service Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.35 trillion in 2025 and is projected to reach USD 2.11 trillion by 2034.

In 2025, the market value stood at USD 0.45 trillion.

The market is expected to grow at a CAGR of 5.0% during the forecast period from 2026 to 2034.

The retail & store replenishment segment leads the market.

E-commerce expansion and inventory localization are the key factors driving market growth.

Key market players in the industry include DHL Supply Chain, Kuehne + Nagel, DB Schenker, DSV, and XPO Logistics.

Asia Pacific accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world are the key regions considered in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us