Washed Silica Sand Market Size, Share & Industry Analysis, By Particle Size (Medium, Fine, Coarse, and Others), By Application (Construction, Oil & Gas Recovery, Glass Manufacturing, Foundry, Water Filtration, and Others), and Regional Forecast, 2026-2034

Washed Silica Sand Market Size and Future Outlook

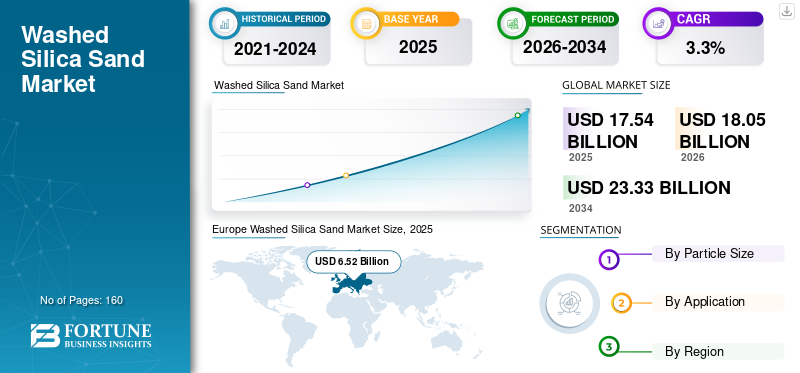

The global washed silica sand market size was valued at USD 17.54 billion in 2025. The market is projected to grow from USD 18.05 billion in 2026 to USD 23.33 billion by 2034, exhibiting a CAGR of 3.3% during the forecast period. Europe dominated the global washed silica sand market with a market share of 37.17% in 2025.

Washed silica sand is processed quartz-rich sand that is washed and classified to remove clay, silt, and other impurities and to achieve consistent particle-size distributions. It is used across glass manufacturing, construction materials, foundry molds and cores, oil and gas recovery (proppant and well services), and water filtration, where purity, sizing, and supply reliability determine suitability and pricing.

The market growth is driven by sustained construction activities in emerging regions, continued need for corrosion-resistant and high-performance industrial materials, and stable, long-term demand for filtration media. At the same time, short-cycle volatility in oil and gas recovery demand creates year-to-year fluctuations in certain grades, especially medium to coarse sands.

Furthermore, the market comprises several major players, including Stone Skipper LLP, Sibelco, Quarzwerke Group, EUROQUARZ, and CDE Group. A broad product portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

WASHED SILICA SAND MARKET TRENDS

Specifications, Tightening, Safety Regulation, and Water and Infrastructure Investments are the Significant Market Trends

Washed silica sand is becoming increasingly specification-driven as end users tighten acceptable limits on impurities, moisture, and particle-size distribution to improve downstream yields and reduce process variability. Alongside this, worker exposure rules for respirable crystalline silica are prompting stricter controls and documentation across mining, processing, and handling. For oil and gas recovery, the shift toward in-basin supply and greater use of wet sand is reshaping regional trade flows and raising the importance of local beneficiation.

Water treatment and filtration programs are supporting steady demand for consistently graded sands. At the same time, glass producers continue to increase cullet usage to lower energy consumption and emissions, influencing virgin silica demand mix by grade and region.

- For instance, USGS notes that increased efforts to reduce cost, emissions, and crystalline-silica exposure are contributing to more in-basin 'dry sand' and undried 'wet sand' being used as frac sand, changing the supplier mix and logistics patterns.

MARKET DYNAMICS

MARKET DRIVERS

Construction-Led Demand and Long-Life Performance Requirements Are Supporting Product Consumption, Driving the Market Growth

Construction remains the largest demand center in many regions, supported by steady needs for dry-mix mortars, grouts, flooring systems, roofing granules, and related building products, where consistent sizing improves workability and finished performance. Industrial users also favor washed sands for process reliability as utilities and municipalities continue to invest in water and wastewater treatment systems that require stable filtration media quality.

In glass manufacturing, it is a critical raw material, as purity and iron content can influence optical properties and yields. Even as recycled cullet usage rises, baseline demand for high-quality silica is supported by glass production capacity and product quality requirements.

- For instance, USGS reports that U.S. industrial sand and gravel use in 2024 remained highly concentrated in frac sand and well packing and cementing, while glassmaking represented a smaller but structurally important share, illustrating how key end-use sectors anchor demand.

MARKET RESTRAINTS

Permission Constraints and Demand Cyclability Can Restrict Market Expansion

Washed silica sand supply depends on access to suitable quartz-rich deposits and permits required for extraction, water use, and tailings management. Local zoning, land development priorities, and community concerns can push new operations farther from demand hubs, increasing delivered costs and reducing competitiveness in freight-sensitive markets.

Demand-side cyclicality is an additional restraint, particularly for medium- and coarse-grade products linked to oil and gas recovery. Oversupply and price compression can result in production limitations, idled facilities, and deferred capital spending, which in turn affect downstream logistics providers and regional trade flows.

- For instance, the USGS notes that in 2024, an oversupply of frac sand led to lower prices and caused many operations to reduce production or idle.

MARKET CHALLENGES

Freight Sensitivity, Quality Consistency, and Tightening Silica Exposure Standards to Hamper Market Growth

The market remains highly freight-sensitive and delivered economics often determine supplier selection more than ex-works pricing. Producers must balance deposit location, processing costs, and logistics access to remain competitive in local and regional catchments, especially for construction and lower-value grades.

At the same time, maintaining consistent particle-size distributions and impurity limits across variable ore bodies and weather conditions requires robust process control. Tightening standards for respirable crystalline silica exposure increases compliance requirements across extraction, processing, and handling, placing additional emphasis on dust control, monitoring, and operating discipline.

MARKET OPPORTUNITIES

Water Infrastructure Programs, Higher-Quality Building Products, and Low-Iron Sand Development to Create Lucrative Growth Opportunities

Public investment in water infrastructure supports long-duration demand for filtration-grade sands, where consistent sizing and low fines improve performance and reduce operational issues. In building products, higher performance expectations for durability, aesthetics, and installation productivity can increase the preference for washed and closely graded sands over less-processed alternatives.

On the supply side, the development of low-iron, higher-purity silica resources can open up higher-value markets for specialty glass and industrial applications. Producers with scalable beneficiation and quality assurance capabilities are better positioned to leverage these opportunities, particularly where downstream industries seek secure local supply.

- For example, according to Glass Alliance Europe reports, overall European glass production was slightly more than 36 million tonnes in 2024, reinforcing the importance of a stable regional silica raw-material ecosystem and opportunities for qualified suppliers.

Download Free sample to learn more about this report.

Segmentation Analysis

By Particle Size

Medium Segment Took the Leading Share Due to Its Usage in Borad Mix of Requierments

Based on particle size, the market is segmented into medium, fine, coarse, and others.

The medium segment accounted for the largest washed silica sand market share in 2025. The segment is growing because it serves the broadest mix of construction products, industrial uses, and oil and gas recovery requirements, where controlled sizing supports performance and handling functions. Furthermore, the segment held a share of 46.7% in 2025.

The fine segment is expected to grow significantly, supported by dry-mix construction materials and certain glass and industrial applications where higher surface area and packing behavior are beneficial. Fine segment is projected to grow at a 3.1% CAGR during the forecast period.

Coarse grades remain more application-specific, with a stronger focus on filtration and select industrial and oilfield applications. Growing adoption of green building practices further supports their demand.

By Application

To know how our report can help streamline your business, Speak to Analyst

Construction Segment Dominates the Market Due to the Extensive Use of the Product in Making Building Products

In terms of application, the market is categorized into the construction, oil & gas recovery, glass manufacturing, foundry, water filtration, and others.

The construction segment accounted for the largest share in 2025. The segment's growth is driven by demand for mortars, grouts, flooring systems, and other building products, where consistently washed sand improves mix quality and finished performance. Furthermore, the segment held 33.5% share in 2025.

The oil & gas recovery segment is also expected to experience favorable growth over the projected period. The segment's demand is driven by its use as a proppant in hydraulic fracturing, where higher well completion intensity and longer laterals increase sand loading per well. In North America, activity remains closely tied to E&P spending and rig/completion cycles, while operators continue optimizing well productivity. The segment is expected to grow at a CAGR of 3.1% over the forecast period.

Washed Silica Sand Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Europe

Europe Washed Silica Sand Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2025, valued at USD 6.52 billion, and is expected to maintain the leading share in 2026, with USD 6.73 billion. The regional market's growth is driven by demand for construction materials, established glass manufacturing capacity, and industrial casting supply chains. The region’s market is supported by mature deposit development and processing infrastructure, alongside increasing attention to product consistency and environmental compliance.

U.K. Washed Silica Sand Market

The U.K. market in 2025 was valued at around USD 0.84 billion, representing approximately 4.0% of global market revenue.

Germany Washed Silica Sand Market

Germany’s market was valued approximately USD 1.64 billion in 2025, equivalent to around 5.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 4.34 billion by 2026. The market’s growth is driven by residential renovation, commercial builds, and technical insulation needs in glass manufacturing facilities.

U.S. Washed Silica Sand Market

In 2025, the U.S. market reached USD 3.78 billion. The U.S. dominates regional consumption given country’s building stock size and scale of construction activities. In the U.S., year-to-year demand remains strongly influenced by hydraulic fracturing activities and proppant supply dynamics, while a steady baseline demand persists in glassmaking and industrial uses.

Asia Pacific

Asia Pacific is expected to experience significant growth in the coming years. During the forecast period, the Asia Paific region is projected to grow at a 3.1% CAGR and reach a valuation of USD 5.86 billion in 2026. The region benefits from intensity of construction activities, expanding infrastructure, and large-scale manufacturing ecosystems in the glass and foundry industries. China remains the largest consumption base, while India and Southeast Asian countries continue to rise as there is an increase demand for construction materials, industrial production, and filtration.

China Washed Silica Sand Market

In 2025, the China market valued at USD 2.37 billion. China’s market demand is driven by large-scale consumption of construction materials, significant glass production capacity, and broad industrial applications that rely on consistent silica feedstock quality.

Latin America

Latin America is experiencing steady growth with its market in 2026 expected to reach a valuation of USD 0.53 billion. The region is driven by demand concentrated in construction materials and selective industrial uses, and with country-level variability depending on local deposit quality and processing capacity.

The Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by project-based demand in industrial facilities, desalination and water infrastructure, and coastal construction, where corrosion resistance and filtration needs are pronounced. Limited local processing capacity in several countries increases reliance on imports and regional supply chains.

GCC Washed Silica Sand Market

GCC reached USD 0.22 billion by 2025, accounting for approximately 2.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players Are Enhancing Deposit Quality, and Specialty Grades to Maintain Their Market Positions

The market includes a mix of multinational industrial minerals groups, regional deposit owners, and application-focused producers. Competition is shaped by deposit quality, beneficiation, sizing capabilities, quality assurance systems, and the ability to supply large, consistent volumes with reliable logistics. Some of the key market players include Stone Skipper LLP, Sibelco, Quarzwerke Group, EUROQUARZ, and CDE Group. They also differentiate through specialty grades for glass and filtration, as well as multi-region distribution networks.

LIST OF KEY WASHED SILICA SAND COMPANIES PROFILED

- Stone Skipper LLP.(India)

- Sibelco (Belgium)

- Quarzwerke Group (Germany)

- EUROQUARZ (Germany)

- SHREE SILICAAM MINERALS LLP (India)

- CDE Group (Ireland)

- Silica Services, LLC. (U.S.)

- All India Minerals (India)

- SUJAL LOGISTICS PVT. LTD. (India)

- PLATINUM MINERAL (Canada)

KEY INDUSTRY DEVELOPMENTS

- July 2024: U.S. Silica Holdings, Inc. was completely accquired by Apollo Global Management, transitioning the company into private ownership while maintaining the U.S. Silica name and leadership, positioning it for longer-term strategic investments across silica and sands processing operations.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.3% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Particle Size, Application, and Region |

|

By Particle Size |

|

|

By Application |

|

|

By Region |

North America (By Particle Size, Application, and Country) o U.S. (By Application) o Canada (By Application) Europe (By Particle Size, Application, and Country) o Germany (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) ·Asia Pacific (By Particle Size, Application, and Country) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) Latin America (By Particle Size, Application, and Country) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) Middle East & Africa (By Particle Size, Application, and Country) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 17.54 billion in 2025 and is projected to reach USD 23.33 billion by 2034.

Recording a CAGR of 3.3%, the market is slated to exhibit steady growth during the forecast period.

The construction application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Stone Skipper LLP, Sibelco, Quarzwerke Group, EUROQUARZ, and CDE Group are some of the prominent players in the market.

The growth driver is the rising use of washed, graded silica sand in large-volume applications in construction materials and oil & gas recovery (proppant), where consistent particle sizing and low impurity levels are critical for performance.

The major factors expected to favor product adoption in the market are stricter quality/spec requirements in glass, foundry, filtration, and engineered construction products, which are pushing users toward washed, specification-grade sand, while infrastructure spending and ongoing well completion activity sustain baseline demand across regions.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us