White Cement Market Size, Share & Industry Analysis, By Product (While Portland Cement, While Masonry Cement), By Application (Residential, Commercial) and Regional Forecast, 2026-2034

White Cement Market Overview

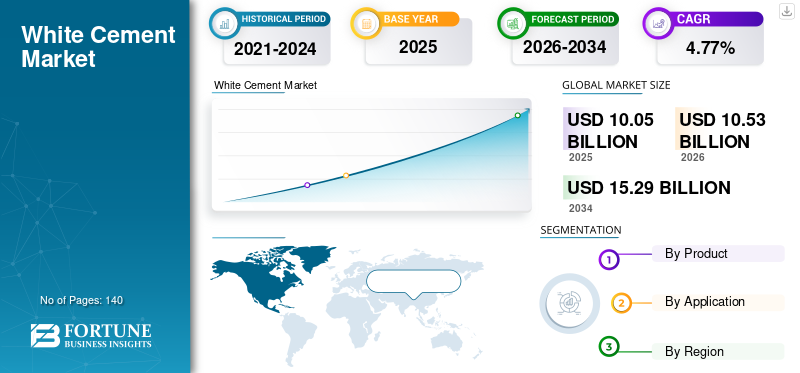

The white cement market size was valued at USD 10.05 billion in 2025. The market is projected to grow from USD 10.53 billion in 2026 to USD 15.28 billion by 2034, exhibiting a CAGR of 4.77 % during the forecast period.

The white cement market is witnessing significant expansion due to increasing demand for decorative construction materials, architectural aesthetics, and premium infrastructure projects. White cement is extensively used in wall putty, terrazzo flooring, precast structures, decorative concrete, and luxury residential applications because of its superior brightness and smooth texture. The white cement market Report highlights rising adoption across commercial complexes, public infrastructure, and modern urban development projects. Construction companies are focusing on sustainable and visually appealing structures, which is accelerating the use of white cement products worldwide. Growing renovation activities and increasing investment in smart cities are further strengthening white cement market Growth and long-term industry expansion.

The USA white cement market is experiencing strong demand due to infrastructure modernization, luxury housing construction, and increasing use of decorative concrete products. Builders and architects in the United States are utilizing white cement for highways, commercial buildings, museums, sidewalks, and premium residential projects because of its durability and reflective properties. The white cement market Analysis for the USA indicates growing use in sustainable construction projects that focus on energy-efficient surfaces and aesthetic building materials. Rising investment in public infrastructure rehabilitation and urban redevelopment projects continues to create opportunities for manufacturers operating within the United States construction sector.

Download Free sample to learn more about this report.

Key Takeaways

Market Size & Growth

- Global market size 2025: USD 10.05 billion

- Global market size 2034: USD 15.28 billion

- CAGR (2025–2034): 4.77 %

Market Share – Regional

- North America: 24%

- Europe: 22%

- Asia-Pacific: 38%

- Rest of World: 16%

Country-Level Shares

- Germany: 26% of Europe’s market

- United Kingdom:18% of Europe’s market

- Japan: 14% of Asia-Pacific market

- China: 41% of Asia-Pacific market

White Cement Market Latest Trends

The white cement market Trends show increasing demand for eco-friendly and decorative construction materials across residential and commercial sectors. Manufacturers are introducing low-carbon cement production technologies to improve sustainability and comply with stricter environmental regulations. White cement is increasingly used in luxury facades, designer flooring systems, artistic concrete applications, and urban landscaping projects. Rising consumer preference for modern architectural aesthetics is encouraging builders to adopt premium white cement products for high-end construction applications.

Download Free sample to learn more about this report.

The white cement market Research Report also highlights increasing investment in prefabricated construction systems and smart city development. White cement-based products are gaining popularity in wall putty, tile adhesives, decorative panels, and ready-mix applications because they provide superior finish quality and long-lasting appearance. Technological advancements in clinker processing and energy-efficient kilns are helping manufacturers improve product consistency and operational efficiency. Growing demand from tourism infrastructure, hospitality projects, and transportation hubs is further supporting the white cement market Growth globally.

White Cement Market Dynamics

DRIVER

Rising Demand for Decorative and Premium Construction Materials

The increasing demand for aesthetically attractive buildings and premium infrastructure is one of the biggest growth drivers in the white cement market. Construction companies are increasingly using white cement in decorative architecture, luxury housing, monuments, shopping malls, airports, and commercial complexes because of its superior visual appearance and high durability. White cement is preferred in colored concrete applications, terrazzo flooring, and precast decorative structures due to its compatibility with pigments and modern finishing technologies. The White Cement Industry Report indicates that urbanization and modernization of infrastructure are significantly boosting product demand.

Architects and engineers are emphasizing sustainable and visually appealing construction designs, leading to higher adoption of white cement products across developed and emerging economies. Government investment in smart cities and public infrastructure projects is further increasing the use of white cement in pavements, decorative walkways, bridges, and transportation hubs. Rising disposable income and increasing consumer spending on luxury housing projects continue to strengthen white cement market Opportunities worldwide.

RESTRAINT

High Production and Energy Consumption Costs

One of the major restraints in the white cement market is the high manufacturing cost associated with specialized raw materials and energy-intensive production processes. White cement requires limestone and kaolin with extremely low iron content, which increases procurement expenses and limits raw material availability in several regions. Specialized kiln systems and advanced clinker production technologies further raise operational costs compared to ordinary gray cement manufacturing.

Energy price fluctuations and transportation costs continue to create financial pressure on manufacturers. The white cement market Analysis indicates that maintaining brightness consistency and product purity requires additional processing stages, increasing overall production expenditure. Smaller manufacturers often struggle to compete with large multinational producers that possess integrated production facilities and stronger supply chain networks. Environmental regulations regarding carbon emissions and industrial waste management are also increasing compliance costs, creating barriers for market expansion in price-sensitive economies.

OPPORTUNITY

Expansion of Sustainable and Smart Construction Projects

The rapid expansion of sustainable construction and smart urban development is creating substantial opportunities within the white cement market. Governments and private developers are increasingly focusing on green buildings and energy-efficient infrastructure, where white cement plays an important role due to its reflective and decorative properties. White cement is widely used in sustainable urban projects, modern facades, reflective pavements, and environmentally efficient construction systems.

The white cement market Forecast indicates rising investment in commercial complexes, luxury hospitality projects, tourism infrastructure, and public transportation systems. Decorative concrete solutions, prefabricated structures, and modern architectural applications are opening new growth avenues for manufacturers. Emerging economies are also investing heavily in infrastructure modernization and residential housing expansion, creating long-term demand for white cement products. Companies focusing on low-emission production technologies and innovative decorative applications are expected to gain a competitive advantage in the global market.

CHALLENGE

Environmental Regulations and Raw Material Limitations

The white cement market faces significant challenges due to increasing environmental regulations and limited availability of high-quality raw materials. White cement manufacturing requires specialized limestone with low iron content, and sourcing these materials consistently can be difficult in several regions. Mining restrictions and environmental policies are creating additional pressure on cement manufacturers to optimize resource utilization while maintaining product quality standards.

The white cement market Insights also highlight challenges associated with reducing industrial carbon emissions and improving energy efficiency. Governments worldwide are implementing strict environmental regulations that require manufacturers to adopt cleaner production technologies and alternative fuel systems. These transitions involve substantial capital investment and technological upgrades. In addition, supply chain disruptions, fuel price volatility, and transportation challenges continue to affect operational efficiency and profitability for manufacturers across international markets.

White Cement Market Segmentation

By Product

White Portland Cement holds nearly 72% of the white cement market Share because of its extensive use in decorative and structural construction applications. The product is widely utilized in luxury residential buildings, museums, commercial complexes, architectural facades, and transportation infrastructure projects. White Portland Cement provides superior brightness, high compressive strength, and compatibility with pigments, making it ideal for colored concrete and decorative finishes. Builders prefer this product for terrazzo flooring, decorative wall panels, precast structures, and artistic construction applications. The white cement market Outlook for White Portland Cement remains strong due to increasing urbanization and premium construction activities across developing economies. Demand from architects and engineering firms continues to rise because of the product’s durability and aesthetic appeal. Manufacturers are investing in advanced clinker technologies and sustainable production methods to improve operational efficiency and product quality. Export demand is also increasing as construction companies seek high-performance decorative cement products for modern infrastructure projects worldwide.

White Masonry Cement accounts for around 28% of the white cement market Share and is primarily used in masonry work, decorative bricklaying, wall finishing, and restoration projects. The product offers superior workability, smooth texture, and consistent brightness, making it highly suitable for premium residential and commercial construction. White Masonry Cement is increasingly used in urban landscaping, outdoor decorative structures, and customized architectural projects where visual quality is essential. The white cement market Research Report indicates growing use of White Masonry Cement in residential renovation activities and heritage restoration projects across Europe and North America. Contractors prefer this product for tile grouting, decorative mortar systems, and premium finishing applications because it provides enhanced durability and aesthetic consistency. Manufacturers are introducing improved formulations with higher moisture resistance and better bonding performance to meet changing construction industry requirements and strengthen market competitiveness.

By Application

The residential segment contributes approximately 58% of the white cement market Share due to rising demand for luxury housing, decorative interiors, and premium exterior finishes. White cement is extensively used in villas, apartments, modern housing complexes, decorative flooring, wall putty, and architectural landscaping applications. Urbanization and rising consumer preference for visually attractive construction materials are significantly supporting segment expansion. The white cement market Analysis highlights increasing demand for decorative concrete and sustainable residential construction systems. Homeowners are investing in premium wall coatings, textured surfaces, and modern design elements that utilize white cement-based products. Smart city projects and urban redevelopment activities are also encouraging residential construction companies to adopt aesthetically appealing and durable materials. Rapid housing development in emerging economies is expected to further support long-term demand within the residential segment.

The commercial segment holds nearly 42% of the white cement market Share because of increasing investments in office complexes, shopping malls, airports, hotels, and transportation infrastructure. Commercial developers are increasingly using white cement in facades, decorative pavements, parking areas, and public infrastructure due to its brightness and long-lasting finish quality. The material is highly preferred for premium commercial projects that require modern architectural appearance and structural durability. The White Cement Industry Analysis shows rising demand from hospitality and retail sectors, where decorative and luxury construction materials are becoming essential for brand image and customer experience. Infrastructure modernization projects involving railway stations, museums, and convention centers are also contributing to segment growth. White cement is additionally used in reflective building surfaces that improve energy efficiency in commercial structures, supporting sustainable construction initiatives worldwide.

White Cement Market Regional Outlook

North America

North America accounts for approximately 24% of the global white cement market Share due to strong demand from infrastructure modernization, premium housing projects, and decorative architectural construction. White cement is widely used in public infrastructure, transportation systems, commercial complexes, and urban landscaping projects throughout the region. Increasing focus on sustainable construction and energy-efficient building materials is further supporting market demand across North America.

The United States dominates regional consumption because of rising investment in smart infrastructure, commercial redevelopment, and high-end residential construction. Contractors and architects prefer white cement for reflective pavements, artistic concrete, and luxury facades. The white cement market Report indicates that increasing renovation of historical buildings and urban modernization projects will continue to support regional growth over the coming years.

Europe

Europe represents nearly 22% of the white cement market Share due to strong emphasis on sustainable construction and advanced architectural standards. The region has a well-established construction industry with significant demand for decorative concrete products, prefabricated structures, and premium infrastructure materials. White cement is extensively utilized in heritage restoration projects, luxury commercial buildings, and public transportation infrastructure.

The white cement market Trends in Europe indicate increasing investment in environmentally sustainable cement production technologies and low-emission construction materials. Countries across the region are promoting green infrastructure initiatives and energy-efficient urban development programs. Decorative paving systems, designer facades, and artistic concrete applications are also contributing to rising demand for white cement products across European construction markets.

Germany White Cement Market

Germany contributes approximately 26% of Europe’s white cement market Share due to advanced infrastructure development and strong adoption of sustainable construction technologies. White cement is extensively used in commercial buildings, transportation projects, decorative facades, and urban redevelopment programs across the country. German construction companies prioritize high-quality materials that provide durability, visual appeal, and environmental efficiency.

The white cement market Insights for Germany highlight increasing use of prefabricated construction systems and architectural concrete applications. Demand for restoration materials in historical structures and public monuments is also supporting market expansion. Manufacturers are focusing on low-emission production technologies and energy-efficient clinker processing systems to comply with strict environmental standards and strengthen their competitive position in the European market.

United Kingdom White Cement Market

The United Kingdom accounts for nearly 18% of Europe’s white cement market Share because of growing investment in infrastructure redevelopment and premium housing construction. White cement is increasingly used in commercial complexes, decorative landscaping projects, transportation hubs, and urban regeneration programs. Developers prefer white cement products because they provide long-lasting finish quality and superior design flexibility.

The white cement market Research Report for the United Kingdom indicates rising demand for decorative concrete walkways, luxury interiors, and prefabricated building systems. Restoration of historical buildings and heritage structures is also creating additional opportunities for manufacturers. Increasing focus on sustainable urban development and energy-efficient architecture continues to support white cement adoption across residential and commercial construction sectors.

Asia-Pacific

Asia-Pacific holds approximately 38% of the white cement market Share and remains the fastest-growing regional market due to rapid urbanization, industrialization, and infrastructure expansion. Governments across the region are investing heavily in smart cities, transportation systems, airports, and commercial complexes, creating strong demand for decorative and durable construction materials. White cement is increasingly used in luxury housing projects, tourism infrastructure, and modern public developments.

The white cement market Growth in Asia-Pacific is supported by rising disposable income, changing architectural preferences, and growing adoption of decorative concrete solutions. Manufacturers are expanding production facilities and export operations to meet increasing regional demand. Infrastructure modernization and rapid residential construction activities are expected to maintain strong market momentum throughout the forecast period.

Japan White Cement Market

Japan contributes around 14% of the Asia-Pacific white cement market Share due to advanced construction standards and strong emphasis on premium infrastructure development. White cement is widely used in transportation systems, earthquake-resistant structures, commercial buildings, and urban redevelopment projects. Japanese construction companies prioritize high-performance materials that combine durability with modern architectural aesthetics.

The white cement market Outlook for Japan highlights increasing use of white cement in prefabricated housing systems and sustainable urban development. Renovation of aging infrastructure and modernization of metropolitan areas are driving long-term product demand. Manufacturers are investing in advanced production technologies and environmentally efficient processing systems to comply with strict industrial regulations and maintain high-quality standards.

China White Cement Market

China accounts for approximately 41% of the Asia-Pacific white cement market Share because of massive infrastructure investment and rapid urban expansion. White cement is extensively used in airports, commercial towers, residential complexes, public transportation systems, and decorative construction applications. Growing demand for modern architectural designs and decorative concrete products is significantly supporting market growth in China.

The White Cement Industry Report indicates increasing adoption of sustainable construction materials and prefabricated building technologies throughout the country. Government investment in smart city development and urban infrastructure modernization continues to create strong opportunities for manufacturers. China’s large-scale construction activities and export-oriented production capabilities make it one of the most influential markets in the global white cement industry.

Rest of the World

The Rest of World region holds nearly 16% of the global white cement market Share due to growing infrastructure development and tourism-related construction activities across the Middle East, Africa, and Latin America. White cement is increasingly used in luxury hotels, religious structures, public infrastructure, and decorative commercial projects because of its premium appearance and reflective properties.

The white cement market Opportunities in these regions are supported by government investment in transportation systems, urban development, and modern residential housing. Middle Eastern countries are focusing on iconic architectural projects and large-scale tourism infrastructure, increasing demand for white cement products. African and Latin American markets are also witnessing higher consumption due to expanding construction industries and modernization of urban infrastructure.

List of Top White Cement Companies

- Cementir Holding N.V.

- Çimsa Çimento Sanayi ve Ticaret A.Ş

- Royal White Cement

- LafargeHolcim

- Aditya Birla (Grasim Industries Limited)

- Cimsa

- Dyckerhoff GMBH

- Federal White Cement

- India Cements Ltd

- J.K. Cement Company

- Ultratech Cement Ltd

- Saudi White Cement Company

Top Two Companies by Market Share

- LafargeHolcim – 17%

- Ultratech Cement Ltd – 14%

Investment Analysis and Opportunities

The white cement market is attracting substantial investment due to rising demand for premium decorative construction materials and sustainable infrastructure solutions. Manufacturers are investing in advanced kiln technologies, energy-efficient production systems, and environmentally sustainable clinker processing facilities to strengthen operational efficiency and improve product quality. Infrastructure modernization projects across Asia-Pacific and the Middle East are creating significant opportunities for capacity expansion and export growth.

The white cement market Opportunities are also increasing because of growing demand for luxury residential projects, smart cities, and modern commercial developments. Investors are focusing on companies with strong distribution networks, integrated production facilities, and innovative decorative cement product portfolios. Strategic partnerships between construction firms and white cement manufacturers are improving market penetration across emerging economies. Companies investing in low-carbon production technologies and specialized architectural cement products are expected to achieve stronger competitive positioning in the international market.

New Product Development

Innovation remains a key focus area in the white cement market as manufacturers continue introducing advanced products with improved durability, brightness, and sustainability performance. Companies are developing white cement solutions with enhanced moisture resistance, rapid setting capabilities, and superior compatibility with decorative pigments. These products are increasingly used in luxury construction, artistic concrete applications, and modern prefabricated building systems.

The white cement market Trends also indicate rising development of environmentally sustainable cement formulations designed to reduce carbon emissions and improve energy efficiency. Manufacturers are launching specialized white cement products for tile adhesives, wall putty, self-leveling flooring systems, and decorative exterior coatings. Advanced packaging technologies and supply chain improvements are also helping companies maintain product consistency and strengthen distribution capabilities across international construction markets.

Five Recent Developments (2023-2025)

- Ultratech Cement expanded its decorative white cement distribution network across residential and infrastructure markets.

- LafargeHolcim introduced advanced low-emission clinker technologies for sustainable white cement manufacturing.

- Çimsa Çimento increased export production capacity to strengthen supply in Europe and North America.

- Saudi White Cement Company upgraded processing systems to improve energy efficiency and product quality.

- JK Cement expanded its portfolio of decorative white cement products for premium architectural applications.

Report Coverage of White Cement Market

The white cement market Report provides comprehensive analysis of industry trends, competitive landscape, market segmentation, regional developments, and technological advancements. The report evaluates key growth drivers such as decorative construction demand, urban infrastructure expansion, sustainable architecture, and modernization of commercial buildings. It also examines challenges associated with environmental regulations, raw material sourcing, and production efficiency.

Request for Customization to gain extensive market insights.

The white cement market Research Report includes detailed segmentation by product type, application, and regional market outlook. The study highlights strategic developments by major manufacturers, investment activities, new product innovation, and supply chain expansion. Market insights related to residential construction, commercial infrastructure, tourism projects, and decorative architectural applications are also covered extensively. The report scope supports investors, manufacturers, suppliers, contractors, and construction companies in understanding current industry conditions and future business opportunities.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us