Wireless Brain Sensors Market Size, Share & Industry Analysis by Product Type (Electroencephalography (EEG) Sensors, Electrocorticography (ECoG) Sensors, Intracranial Pressure (ICP) Sensors, Wearable fNIRs, & Others), By Application (Traumatic Brain Injury (TBI) Monitoring, Stroke Monitoring & Rehabilitation, Sleep Disorders & Mental Health Research, & Neurological Conditions), By Type (Implantable and Non-implantable), By Technology (Radiofrequency (RF) Based Sensors, Bluetooth / BLE Sensors, and Near Field Communication (NFC) / RFID Sensors), By End-User, and Regional Forecast, 2026-2034

Wireless Brain Sensors Market Size and Future Outlook

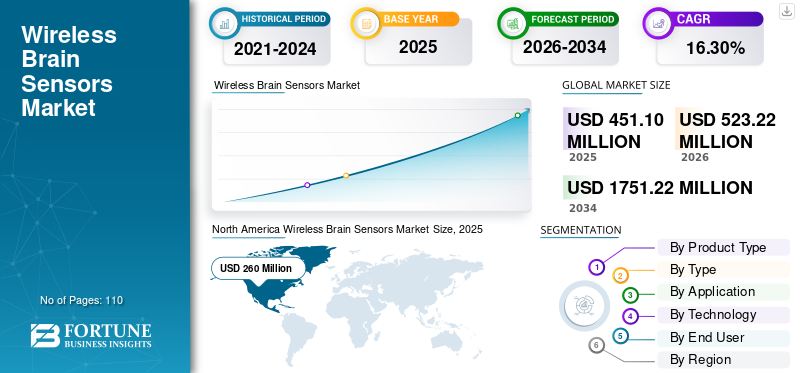

The global wireless brain sensors market size was valued at USD 451.10 million in 2025. The market is projected to grow from USD 523.22 million in 2026 to USD 1751.22 million by 2034, exhibiting a CAGR of 16.30% during the forecast period. North America dominated the wireless brain sensors market with a market share of 56.90% in 2025.

Wireless brain sensors are designed to record and transmit brain activity in real time without requiring physical wiring. These sensors are gaining traction in both clinical and research environments for studying neurological disorders, evaluating brain injuries, and supporting treatment planning. The market growth is largely fueled by the increasing incidence of neurological diseases, continuous improvements in wireless communication technologies, and the rising preference for minimally invasive monitoring solutions. Moreover, the expanding use of wearable and implantable brain sensors in applications such as neurorehabilitation and sleep monitoring is projected to have a positive impact on market growth.

Furthermore, the market includes several major players with Zeto, Inc., Epitel, Inc., Ceribell, Inc., and NextSense, Inc. at the forefront. Robust focus on research and development, along with technological innovations, is assisting these companies to maintain their strong presence in the global market.

Download Free sample to learn more about this report.

Wireless Brain Sensors MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 451.10 million

- 2026 Market Size: USD 523.22 million

- 2034 Forecast Market Size: USD 1,751.22 million

- CAGR: 16.30% from 2026–2034

- North America dominated the wireless brain sensors market with a 56.90% share in 2025.

- EEG segment led the market in 2025 with 52.15% share due to strong clinical adoption and non-invasive monitoring capabilities.

- Non-implantable segment held the dominant share in 2026 with 69.75% due to rising demand for minimally invasive neuro-monitoring solutions.

North American

North America reached USD 0.30 billion in 2026, supported by high neurological disease prevalence and strong regulatory approvals.

Europe

Europe reached USD 0.12 billion in 2026, driven by rising adoption of wireless brain monitoring for neurological disorder management.

Asia Pacific

Asia Pacific reached USD 0.09 billion in 2026, supported by rapid healthcare digitization and increasing neurological diagnostics demand.

U.S.

Market estimated at USD 280 million in 2026, driven by advanced neurotechnology adoption and strong clinical infrastructure.

Japan

Growth supported by increasing aging population and rising demand for advanced brain monitoring solutions.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Technological Advancements in Sensor Technology to Boost Market Growth

Recent advancements in sensor miniaturization, wireless data transmission, and biocompatible materials are playing a vital role in improving the accuracy, longevity, and overall usability of wireless brain sensors. Moreover, the integration of IoT and artificial intelligence into wireless monitoring systems enables real-time analytics and remote tracking, proving especially valuable in post-surgical and home-care applications. Such innovations have considerably enhanced the reliability, efficiency, and accessibility of wireless brain monitoring technologies across hospitals, clinics, and research centers, thereby boosting the global wireless brain sensors market growth.

- For instance, in May 2025, Epsilon Medical Inc. received FDA approval for its EP-01 endovascular EEG device. The new device has been developed for the monitoring and recording of brain electrical signals for epilepsy treatment.

MARKET RESTRAINTS

Significant Cost of Sensors Along with Stringent Reimbursement Policies to Hamper Market Growth

The high production cost of wireless brain sensors, coupled with insufficient reimbursement coverage, remains a major obstacle to widespread adoption. Implantable variants are especially costly due to the need for complex surgical implantation and extensive post-operative management. Additionally, limited or inconsistent reimbursement policies in developing regions further hinder access to advanced neuro-monitoring technologies, constraining overall market growth and penetration.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence to Offer Significant Opportunities for Market Players

The incorporation of artificial intelligence algorithms and cloud computing platforms offers a significant growth opportunity for market participants. AI-driven analytics enable the automatic interpretation of brain activity, supporting the early diagnosis of neurological disorders and improved clinical decision-making. Meanwhile, cloud-based monitoring allows healthcare providers to remotely access and track patient data in real time, enabling timely interventions and continuous neurological evaluation. Collectively, such advancements are expected to the drive faster adoption of wireless brain sensors across hospitals, research institutions, and tele-neurology networks.

- For instance, in September 2025, Natus Medical Incorporated announced plans to acquire Holberg EEG with an aim to enter into AI-based Neurodiagnostic solutions. The platform holds the capability to interpret EEG signals more accurately and in detail.

WIRELESS BRAIN SENSORS MARKET TRENDS

Rising Preference for Wearable Neurotechnology Devices is one of the Prominent Trends

A major trend influencing the market is the growing adoption of wearable brain sensors that support long-term, ambulatory monitoring. Lightweight, user-friendly headbands and skin patches equipped with wireless EEG or functional near-infrared spectroscopy (fNIRS) sensors are becoming increasingly popular across clinical and consumer health applications. In addition, these devices are also finding expanding roles in neurofeedback therapy, gaming, and cognitive performance enhancement. The shift toward home-based and continuous brain monitoring is transforming the market landscape, driving collaborations between medical technology developers and digital health companies.

- For instance, in October 2025, the University of Oxford's NeuroMetrology Lab and Clario announced a strategic partnership with an aim to develop wearable sensor technology called Opal for comprehensive analysis of Parkinson’s disease.

MARKET CHALLENGES

Data Security Concerns to Offer Significant Challenge to Market Growth

Wireless data transmission introduces key challenges related to signal integrity, latency, and data security. Interference during transmission can distort or weaken signals, affecting the accuracy of brain activity readings. Inadequate encryption and cybersecurity measures may also expose sensitive patient information to potential breaches. Furthermore, the lack of standardized calibration protocols across different manufacturers continues to hinder consistency, regulatory compliance, and large-scale clinical adoption of wireless brain sensor technologies.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Non-invasive Nature of EEG Coupled with Comparatively Lower Cost to Accelerate Segment Growth

On the basis of segmentation by product, the market is classified into electroencephalography (EEG) sensors, electrocorticography (ECoG) sensors, intracranial pressure (ICP) sensors, wearable fNIRs, and others.

To know how our report can help streamline your business, Speak to Analyst

The EEG segment held the highest global wireless brain sensors market share 52.15% in 2025. The segment growth is attributed to its established clinical value, non-invasive design, and ability to record rapid brain electrical activity with less cost and complexity compared to implantable technologies. Moreover, these systems are widely used in neurology departments, sleep disorder centers, epilepsy monitoring, and brain-computer interface research. Their adaptability into wearable and semi-wearable formats makes them ideal for wireless integration. Furthermore, ongoing advancements in dry electrode technology, artifact reduction algorithms, and wireless transmission are enhancing comfort, reliability, and suitability for long-term monitoring. In addition, an increasing number of FDA approvals is projected to have a positive impact on segment growth.

- In April 2025, Epitel received FDA approval for its EEG system, which is specifically designed for the neurological monitoring of pediatric patients and infants.

The intracranial pressure (ICP) sensors segment is expected to grow at a CAGR of 16.8% over the forecast period.

By Type

Superior Safety and User-Friendliness of Non-Implantable Brain Sensors to Accelerate Segment Growth

In terms of type, the market is categorized into implantable and non-implantable.

The non-implantable segment captured the largest share of the market in 2025. In 2026, the segment dominates with a 69.75% share. The segment growth is majorly attributed to the increasing global emphasis on minimally invasive diagnostics, remote monitoring, and consumer-oriented neurotechnology. Moreover, non-implantable sensors allow for long-term brain activity tracking without the risks, costs, or recovery time associated with surgical procedures, making them especially well-suited for outpatient and home-care use. In addition, emphasis on market players for technological developments is further expected to boost segment growth during the forecast period.

- For instance, in June 2025, iMotions announced a strategic partnership with Artinis Medical Systems, one of the global players in functional near-infrared spectroscopy (fNIRs) technology. The collaboration is intended for the integration of fNIRs technology and software suites of the respective companies.

The implantable segment is expected to grow at a CAGR of 14.8% over the forecast period.

By Application

Rising Need for Real-time Monitoring of Neurological Conditions to Boost Segment Growth

In terms of application, the market is categorized into traumatic brain injury (TBI) monitoring, sleep disorders & mental health research, neurological conditions, and others.

The neurological conditions segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 48.96% share. Neurological disorders such as epilepsy, Parkinson’s disease, Alzheimer’s disease, stroke recovery, and other neurodegenerative conditions generate a consistent need for continuous and real-time monitoring of brain activity. Moreover, wireless sensors allow healthcare providers to observe neurological signals beyond hospital settings, improving disease management, facilitating early detection of flare-ups, and enhancing patient outcomes.

- According to data published by the World Health Organization (WHO) in February 2024, an estimated 50 million people have epilepsy worldwide.

The traumatic brain injury (TBI) monitoring segment is expected to grow at a CAGR of 17.3% over the forecast period.

By Technology

Long Distance Transmission Capabilities of RF-based Technology to Accelerate Segment Growth

Based on technology, the market is segmented into radiofrequency (RF) based sensors, Bluetooth / BLE sensors, near field communication (NFC) / RFID sensors, and others.

The radiofrequency (RF) based sensors segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 48.46% share. RF-based wireless sensors dominate the market owing to their superior data transmission range, energy efficiency, and reliability in medical environments. In addition, the technology enables both implantable and wearable sensors to transmit neural signals through biological tissue and across moderate distances without restricting patient mobility. This capability is particularly critical in applications such as ambulatory monitoring and neuroprosthetics, where stable, low-latency connectivity and minimal power usage are essential.

The Bluetooth/BLE sensor segment is expected to grow at a CAGR of 16.7% over the forecast period.

By End User

Availability of Cutting-Edge Resources in Hospital Settings to Accelerate Hospitals & Clinics Segment Growth

Based on end-user, the market is segmented into hospitals & clinics, research & academic institutes, and homecare & remote patient monitoring.

In 2024, the global market was dominated by the hospitals & clinics segment in terms of end-user. Hospitals and specialty clinics constitute the largest end-user segment in the wireless brain sensors market, supported by their advanced infrastructure, access to skilled neurologists, adherence to regulatory standards, and financial capacity to invest in state-of-the-art technologies. Moreover, these institutions conduct a wide range of neurological procedures, including surgeries, continuous EEG monitoring, ICU-based diagnostics, and long-term brain activity assessments, thereby making them the primary buyers of high-performance brain sensor systems.

In addition, the research & academic institutes segment is projected to grow at a CAGR of 15.3% during the study period.

Wireless Brain Sensors Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

The market in North America reached USD 0.26 billion in 2025, representing 56.90% of total market revenue, and is projected to reach USD 0.3 billion in 2026. The factors influencing the region’s dominance include a considerable prevalence of neurological diseases, technological advancements, and product approvals. In 2026, the U.S. market is estimated to reach USD 280 million.

- For instance, in September 2024, a group of researchers at the Icahn School of Medicine announced the development of a new non-invasive ICP technology for comprehensive analysis of intracranial hypertension.

North America Wireless Brain Sensors Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe

Europe contributed approximately USD 0.1 billion to the global market in 2025, accounting for 22.53% share, and is expected to reach USD 0.12 billion in 2026. Europe is projected to witness notable growth in the years to come. During the forecast period, European region is projected to record the growth rate of 15.2%, and touch a valuation of USD 101.6 million in 2025. This is primarily due to the extensive adoption of wireless brain sensors for the management of neurological conditions. Backed by these factors, countries including U.K., Germany, and France are anticipated to record the valuation of USD 20 million, USD 20 million, and USD 14.4 million respectively in 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 0.08 billion, representing 16.95% of global demand, and is projected to grow to USD 0.09 billion in 2026. Asia Pacific is expected to exhibit the fastest CAGR during the forecast period. India and China are estimated to reach USD 10 million and USD 20 million, respectively in 2026.

In 2025, the rest of the world market records a valuation of USD 16.3 million.

COMPETITIVE LANDSCAPE

Key Industry Players:

Robust Focus on R&D Activities Coupled with Extensive Investments to Help Companies in Maintain their Market Position

The global wireless brain sensors market shows a semi-concentrated structure with a number of small- to mid-size players who are actively operational worldwide. These market participants show active involvement in geographic expansion, strategic collaborations, and product innovation.

Zeto, Inc., Epitel, Inc., Ceribell, Inc., and NextSense, Inc. are some of the dominating players in the market. A comprehensive range of wireless brain sensors, continual innovation, and extensive focus on research & development are few characteristics of these players that support their dominance.

Apart from this, other major players in the market include Kernel, Inc., Neurosity, Inc., Blackrock Neurotech, LLC, Neuralink Corp., and others. These participants are undertaking numerous strategic initiatives such as partnerships with healthcare providers to enhance their market presence.

LIST OF KEY WIRELESS BRAIN SENSORS COMPANIES PROFILED:

- Zeto, Inc. (U.S.)

- Epitel, Inc. (U.S.)

- Ceribell, Inc. (U.S.)

- NextSense, Inc. (U.S.)

- EMOTIV, Inc. (U.S.)

- Kernel, Inc. (U.S.)

- Neurosity, Inc. (U.S.)

- Blackrock Neurotech, LLC (U.S.)

- Neuralink Corp. (U.S.)

- NeuroPace, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Samsung announced the development of its ear-based EEG devices, which enable the real-time monitoring of brain activities.

- April 2024: Soterix Medical Inc. announced the launch of the MxN-GO EEG system. The system was developed for research applications, especially for the monitoring of brain activities.

- April 2024: Integra LifeSciences Holdings Corporation announced the relaunch of its CereLink ICP monitoring system.

- January 2024: Aditxt, Inc. announced the acquisition of an EEG product portfolio from Brain Scientific, Inc. Through this strategic step, the company is planning to consolidate its position in the neurology monitoring market.

- March 2021: Brain Scientific received FDA approval for its next-generation NeuroCap EEG device. The device has been specifically designed for pediatric use.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.30% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type

By Type

By Application

By Technology

By End User

By Geography

|

Frequently Asked Questions

The global wireless brain sensors market size is projected to grow from $520 million in 2026 to $1750 million by 2034, exhibiting a CAGR of 16.30%

In 2025, the market value stood at USD 260 million.

The market is expected to exhibit a CAGR of 16.30% during the forecast period of 2026-2034.

In 2025, the electroencephalography (EEG) sensors segment led the market by product type.

The key factors driving the market are the rising prevalence of neurological disorders and technological developments.

Zeto, Inc., Epitel, Inc., and Ceribell, Inc., are some of the prominent players in the market.

North America dominated the market in 2025.

The benefits of brain sensors for brain activity monitoring, extensive investments for new product developments, and new product approvals are key factors anticipated to push product adoption.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us