Zero-Emission Heavy Machinery Market Size, Share & Industry Analysis, By Machinery Type (Earthmoving & Excavation, Haulage & Dumping, Material Handling, Lifting & Access, and Others), By Powertrain (Battery-Electric (BEV), Hydrogen Fuel Cell Electric (FCEV), and Others), By Application (Construction, Mining, Ports & Logistics Terminals, Industrial & Municipal, and Others), and Regional Forecast, 2026-2034

Zero-Emission Heavy Machinery Market Size and Future Outlook

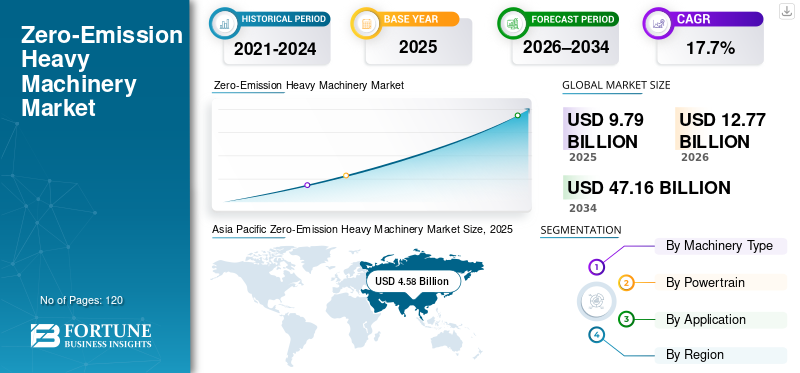

The global zero-emission heavy machinery market size was valued at USD 9.79 billion in 2025. The market is projected to grow from USD 12.77 billion in 2026 to USD 47.16 billion by 2034, exhibiting a CAGR of 17.7% during the forecast period. Asia Pacific dominated the zero-emission heavy machinery market with a market share of 46.78% in 2025.

Zero-emission heavy machinery includes construction, mining, material handling, and industrial equipment powered by battery-electric, hydrogen fuel cell, or other non-combustion-based powertrains that eliminate direct tailpipe emissions. These machines are increasingly deployed to comply with tightening environmental regulations, reduce carbon footprints, and lower operating emissions across high-impact industries.

The market has gained a strong and fast momentum primarily due to the worldwide decarbonization initiatives, greater acceptance of electric construction and mining gear, and more public and private money being invested in clean infrastructure. In addition, the industrialized and developing countries are more inclined toward helping market expansion by offering grants, carrying out test projects, and enacting laws for environment-friendly machines.

Major OEMs such as Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment, Hitachi Construction Machinery, and Liebherr Group are intensifying their focus on electrification and hydrogen-powered equipment portfolios to align with long-term sustainability goals.

- For instance, in April 2024, Volvo Construction Equipment expanded its global zero-emission lineup by introducing electric excavators and wheel loaders for large-scale infrastructure and urban construction projects.

Download Free sample to learn more about this report.

ZERO-EMISSION HEAVY MACHINERY MARKET TRENDS

Electrification of Construction and Mining Equipment is a Key Market Trend

The accelerating shift toward electrification of heavy machinery is a major trend shaping the global market. Construction and mining operators are increasingly transitioning from diesel powered equipment to battery-electric and hydrogen-based alternatives to meet emissions regulations target and reduce noise and operating costs.

Additionally, the integration of zero-emission machinery into smart construction sites, autonomous mines, and electrified ports is further strengthening demand. These machines support sustainable operations while enabling compatibility with digital fleet management and automation systems.

- For instance, in 2025, Komatsu Ltd. announced the expansion of its electric and hydrogen-powered mining truck development program as part of its long-term carbon neutrality roadmap.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Emission Regulations and Decarbonization Targets to Drive Market Growth

Stringent emission norms and carbon reduction targets imposed by governments worldwide are a primary driver for the zero-emission heavy machinery market. Regulations targeting diesel engines in construction, mining, and industrial equipment are accelerating the adoption of electric and hydrogen-powered alternatives.

Furthermore, end users are increasingly prioritizing sustainability commitments and ESG goals, prompting investments in low- and zero-emission fleets to enhance environmental performance and corporate reputation.

- To illustrate, in 2024, the European Union reinforced its emission reduction framework for non-road mobile machinery, accelerating the shift toward electric and hydrogen-powered heavy equipment.

MARKET RESTRAINTS

High Initial Equipment Costs and Infrastructure Limitations to Restrict Market Growth

Zero-emission heavy machinery has a tremendous market potential but the initial investment is quite high, which acts as a major barrier to its acceptance. The initial cost of battery-electric and hydrogen-powered equipment is much higher than that of the diesel-powered machines, which is a factor that restricts the use of such equipment by operators who are sensitive to prices.

Moreover, the lack of charging and hydrogen refueling stations, especially in secluded areas where construction and mining activities are taking place, makes the operations difficult but also hinders the quick spread of such technologies.

- For instance, in February 2024, Shell permanently closed all seven of its hydrogen refueling stations in California due to market and supply challenges. This underscores persistent infrastructure constraints that hinder the widespread adoption of hydrogen-powered zero-emission equipment.

MARKET OPPORTUNITIES

Growth of Green Infrastructure Projects and Clean Mining to Create Opportunities

The expansion of green infrastructure projects and clean mining initiatives presents significant opportunities for market players. Governments and private developers are increasingly mandating the use of low- and zero-emission equipment in urban construction, renewable energy projects, and sustainable mining operations.

Additionally, advancements in battery energy density and hydrogen fuel cell systems technology are expected to enhance equipment performance and reduce the total cost of ownership over time.

- For instance, in 2025, Hitachi Construction Machinery partnered with energy providers to pilot zero-emission construction sites using battery-electric excavators and loaders in Japan.

Segmentation Analysis

By Machinery Type

Strong Demand for Construction Equipment to Drive Earthmoving & Excavation Segment’s Dominance

Based on machinery type, the market is segmented into earthmoving & excavation, haulage & dumping, material handling, lifting & access, and others.

The earthmoving and excavation segment took the lead as the largest market share holder. The segment is driven by the robust adoption of electric excavators, loaders, and compact construction equipment in urban and infrastructure projects.

- For instance, Caterpillar Inc. showcased prototype battery-electric excavators as part of its sustainable construction equipment roadmap in 2024.

The haulage & dumping segment is expected to register the highest CAGR of 19.7% over the forecast period. This is supported by the growing adoption of electric and hydrogen-powered mining trucks in large-scale mining operations.

By Powertrain

Battery-Electric Powertrains Segment Leads Due to Expanding Charging Infrastructure

Based on powertrain, the market is segmented into battery-electric (BEV), hydrogen fuel cell electric (FCEV), and others.

The battery-electric (BEV) segment holds the highest zero-emission heavy machinery market share, owing to technological maturity, improving battery performance, and expanding charging infrastructure.

- For instance, Volvo Construction Equipment has commercialized multiple BEV models across construction and material handling applications globally.

The hydrogen fuel cell electric (FCEV) segment is projected to grow at the highest CAGR of 20.5% over the forecast period. This is driven by suitability for high-load and long-duty-cycle applications such as mining haulage.

To know how our report can help streamline your business, Speak to Analyst

By Application

Construction Segment Leads Due to Investments in Public Infrastructure

Based on application, the market is segmented into construction, mining, ports & logistics terminals, industrial & municipal, and others.

The construction segment holds the highest market share, supported by urban emission regulations, noise reduction requirements, and public infrastructure investments.

- For instance, in 2024, several European cities mandated zero-emission construction zones, accelerating the adoption of electric construction machinery.

The ports & logistics terminals segment is expected to grow at a strong pace with highest CAGR of 19.5% over the analysis period, driven by the electrification of port equipment and material handling systems.

Zero-Emission Heavy Machinery Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Zero-Emission Heavy Machinery Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global zero-emission heavy machinery market and is expected to register the highest CAGR during the forecast period. Rapid urbanization, large-scale infrastructure development, and expanding mining activities across the region are accelerating the demand for clean and sustainable machinery. Government incentives, emission regulations, and public investments in electrification across China, Japan, South Korea, and India further strengthen market growth.

Japan Zero-Emission Heavy Machinery Market

The Japan market is estimated to reach a value of around USD 0.74 billion in 2026, representing approximately 5.8% of global revenues. The market is supported by advanced robotics and electrification capabilities, strong focus on hydrogen technologies, and continuous innovation in construction and mining equipment. The country’s emphasis on carbon neutrality and smart infrastructure development continues to drive the adoption of battery-electric and hydrogen-powered heavy machinery.

China Zero-Emission Heavy Machinery Market

The China market is estimated to hit a valuation of around USD 3.47 billion in 2026, representing approximately 27.2% of global revenues, accounting for a substantial share of global demand. Growth is driven by aggressive decarbonization policies, large-scale infrastructure projects, and government-backed electrification programs for construction and mining equipment. China’s strong domestic manufacturing base further accelerates the commercialization of zero-emission machinery.

India Zero-Emission Heavy Machinery Market

In 2026, the India market is estimated to reach approximately USD 0.72 billion, accounting for approximately 5.6% of global revenues, supported by expanding infrastructure development, smart city initiatives, and increasing focus on sustainable construction practices. Government programs promoting electrification, along with rising awareness of environmental impacts from diesel-powered equipment, are gradually driving the adoption of zero-emission heavy machinery.

North America

North America zero-emission heavy machinery market is expanding, supported by the early adoption of electrification technologies across construction, mining, and industrial sectors. The region benefits from strong regulatory pressure to reduce emissions from non-road mobile machinery, along with rising investments in sustainable infrastructure and clean mining initiatives. The presence of major OEMs, technology providers, and pilot deployments of battery-electric and hydrogen-powered equipment further supports market development.

U.S. Zero-Emission Heavy Machinery Market

The U.S. market is estimated to touch around USD 1.77 billion in 2026, accounting for a 13.9% of global revenues. Growth is driven by increasing adoption of electric construction equipment, federal and state-level decarbonization policies, and investments in zero-emission infrastructure projects. The rising focus on reducing diesel dependency in construction sites and mining operations, particularly in urban and environmentally sensitive regions, continues to support market expansion.

Europe

Europe also holds a significant position in the global zero-emission heavy machinery market due to stringent emission regulations, strong sustainability mandates, and early commercialization of electric and hydrogen-powered heavy equipment. The region has been at the forefront of zero-emission construction initiatives, particularly in urban infrastructure and public works projects. Additionally, Europe’s strong base of construction and mining equipment manufacturers supports continuous innovation and deployment of clean machinery solutions.

U.K. Zero-Emission Heavy Machinery Market

The U.K. market is estimated to reach USD 0.55 billion in 2026, representing approximately 4.3% of global market revenues, supported by government-led net-zero targets and increasing adoption of zero-emission equipment in construction and municipal applications. Infrastructure development projects, combined with growing restrictions on diesel-powered machinery in urban areas, are accelerating the demand for electric and low-emission heavy equipment across the country.

Germany Zero-Emission Heavy Machinery Market

Germany’s market is estimated to touch a value of approximately USD 0.76 billion in 2026, accounting for approximately 5.9% of global revenues. The market expansion is driven by strong industrial electrification, advanced engineering capabilities, and leadership in sustainable construction practices. The country’s focus on energy transition, coupled with high penetration of electric and hydrogen-powered industrial equipment, positions Germany as a key contributor to global zero-emission heavy machinery market growth.

South America and Middle East & Africa

South America and the Middle East & Africa are expected to witness steady growth during the forecast period. The market expansion is supported by mining investments, infrastructure development, and gradual adoption of cleaner technologies across construction and industrial sectors. Although adoption remains at a nascent stage compared to developed regions, the increasing emphasis on sustainability and operational efficiency is encouraging the deployment of zero-emission heavy machinery in large-scale projects.

GCC Zero-Emission Heavy Machinery Market

The GCC market is poised to reach about USD 0.44 billion in 2026, which represents approximately 3.4% of the global market. The main factors driving regional expansion are large infrastructure projects, smart city transformations, and national sustainability goals. Besides, the governments in the region have a major concern of reducing carbon footprint of construction and industrial operations and gradually allowing the use of machinery powered by batteries and hydrogen.

COMPETITIVE LANDSCAPE

Key Industry Players

Expansion of Electrification and Hydrogen Portfolios by Leading Players to Strengthen their Standing

The global zero-emission heavy machinery market features a competitive landscape dominated by leading OEMs focusing on electrification, hydrogen innovation, and sustainable equipment development. Companies are investing heavily in R&D, pilot deployments, and strategic partnerships to accelerate commercialization.

- For instance, in 2024, Liebherr Group expanded its hydrogen-powered equipment development program targeting mining and heavy construction applications.

LIST OF KEY ZERO-EMISSION HEAVY MACHINERY COMPANIES PROFILED

- Caterpillar Inc. (U.S.)

- Komatsu Ltd. (Japan)

- Volvo Construction Equipment (Sweden)

- Hitachi Construction Machinery (Japan)

- Liebherr Group (Switzerland)

- Sandvik AB (Sweden)

- Doosan Bobcat Inc. (U.S.)

- Hyundai Construction Equipment (South Korea)

- JCB Ltd. (U.K.)

- XCMG Group (China)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Komatsu Ltd. entered into a strategic partnership with several global mining operators to test the hydrogen-powered haulage trucks. The collaboration aimed at the reduction of emissions from mining and also at the development of the site for zero-emission mining.

- January 2025: Volvo Construction Equipment added new battery-electric excavators and wheel loaders for medium and heavy duty vehicles application that made the zero-emission equipment for infrastructure, quarrying, and urban construction projects even more electrifying.

- November 2024: Liebherr Group announced the development of a hydrogen-powered internal combustion engine platform for heavy construction and mining equipment, supporting its long-term roadmap toward zero-emission and low-emission machinery.

- October 2024: Caterpillar Inc. revealed new battery-electric and hybrid prototype machines at international construction equipment exhibitions, highlighting its strategy to offer multiple zero-emission powertrain options tailored to different job-site requirements.

- September 2024: Hitachi Construction Machinery, together with energy and infrastructure firms in Japan, started a project that involves the use of zero-emission construction equipment on the pilot construction sites, where the focus will be on electric-operated excavators with a charging ecosystem.

REPORT COVERAGE

The global zero-emission heavy machinery market analysis includes a comprehensive study of market size and forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence physiotherapy equipment market growth over the forecast period. The report also covers technological advancements, product innovation, regulatory considerations, and key strategic developments such as partnerships and acquisitions. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Machinery Type, Powertrain, Application, and Region |

|

By Machinery Type |

· Earthmoving & Excavation · Haulage & Dumping · Material Handling · Lifting & Access · Others |

|

By Powertrain |

· Battery-Electric (BEV) · Hydrogen Fuel Cell Electric (FCEV) · Others |

|

By Application |

· Construction · Mining · Ports & Logistics Terminals · Industrial & Municipal · Others |

|

By Region |

· North America (By Machinery Type, Powertrain, Application and Country) o U.S. (By Powertrain) o Canada (By Powertrain) o Mexico (By Powertrain) · Europe (By Machinery Type, Powertrain, Application and Country) o Germany (By Powertrain) o U.K. (By Powertrain) o France (By Powertrain) o Italy (By Powertrain) o Spain (By Powertrain) o Rest of Europe · Asia Pacific (By Machinery Type, Powertrain, Application and Country) o China (By Powertrain) o Japan (By Powertrain) o India (By Powertrain) o South Korea (By Powertrain) o Rest of Asia Pacific · South America (By Machinery Type, Powertrain, Application and Country) o Brazil (By Powertrain) o Argentina (By Powertrain) o Rest of South America · Middle East & Africa (By Machinery Type, Powertrain, Application and Country) o GCC (By Powertrain) o South Africa (By Powertrain) o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.79 billion in 2025 and is projected to reach USD 47.16 billion by 2034.

In 2025, the market value stood at USD 4.58 billion.

The market is expected to exhibit a CAGR of 17.7% during the forecast period of 2026-2034.

By application, the construction segment leads the market.

Stringent emission regulations and decarbonization targets are the key factors driving the market growth.

Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment, Hitachi Construction Machinery, and Liebherr Group are among the major players in the global market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us