eSIM Market Size, Share & Industry Analysis, By Application (Smartphones, Laptops/Tablets, Connected Cars, Wearable Devices, Smart Home Appliances, Vehicle Tracking, and Others), By Industry (Retail, Consumer Electronics, Manufacturing, Automotive, Transportation & Logistics, Energy & Utilities, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

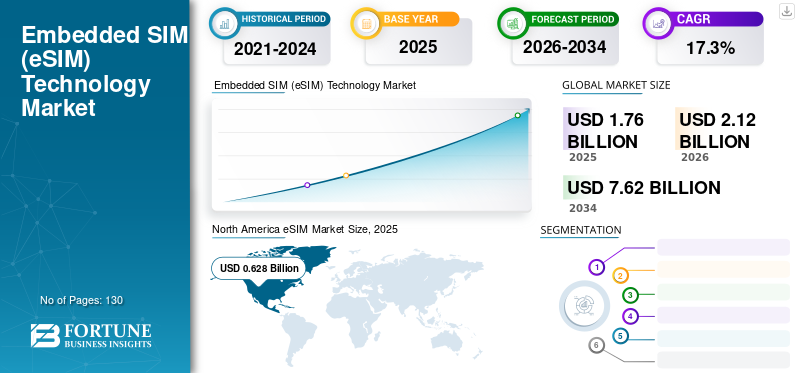

The global eSIM market size was valued at USD 1.76 billion in 2025 and is projected to grow from USD 2.12 billion in 2026 to USD 7.62 billion by 2034, exhibiting a CAGR of 17.3% during the forecast (2026-2034). North America accounted for a market value of USD 0.628 million in 2025.

Embedded SIM or eSIM technology facilitates remote provisioning, allowing users to switch, download, and delete different operator profiles without requiring a physical SIM. eSIMs save physical space within devices and offer greater flexibility. They are environmentally friendly, which significantly helps to cut down the production of plastic cards.

Download Free sample to learn more about this report.

ESIM Market Key Takeaways:

- 2025 Market Size: USD 1.76 billion

- 2026 Market Size: USD 2.12 billion

- 2034 Forecast Market Size: USD 7.62 billion

- CAGR: 17.3% from 2026–2034

- North America dominated the eSIM market with a 35.70% share in 2025.

- The consumer electronics segment is projected to lead with a 24.63% share in 2026.

- The connected cars segment is expected to hold a 23.87% share in 2026.

North America

North America accounted for USD 0.63 billion in 2025 and is projected to reach USD 0.75 billion in 2026, maintaining its position as the leading regional market.

Asia Pacific

Asia Pacific generated USD 0.28 billion in 2025 and is expected to reach USD 0.35 billion in 2026, with the highest CAGR during the forecast period.

Europe

Europe held 30.80% of global revenue in 2025, valued at USD 0.54 billion, and is projected to reach USD 0.65 billion in 2026.

U.S.

The country remains a major contributor to North America’s revenue, supported by strong adoption of eSIM-enabled smartphones, wearables, and connected vehicles.

Japan

The Japan eSIM market is projected to reach USD 0.049 billion in 2026, driven by rising demand for connected consumer electronics and IoT devices.

Read More

The demand for these chips in the market is increasing, mainly due to technological advancements in manufacturing machinery equipment, Industry 4.0, and other high-tech devices that are increasingly connected and can be monitored remotely. Hence, several OEMs and Mobile Network Operators (MNOs) have been innovating solutions by forming partnerships and collaborations for the eSIM market growth. For instance,

- Cloudflare announced the first zero-trust SIM for smartphones to protect corporate networks. Zero Trust SIM is an embedded SIM that is deployable on existing IOS and Android devices, thus mitigating the risk of SIM exchange attacks.

- Monogoto partnered with Workz to build a cloud platform to handle M2M and consumer eSIM devices for its customer base across 180 countries. Monogoto uses this technology to connect applications such as wearables, ATMs, smart lights, and other devices. The partnership allows customers to change profiles and install SIMs on supported QR code devices.

Thus, this technology is one of the prominent drivers for the Internet of Things (IoT) that is estimated to be used in various devices such as smartphones, transport, health monitoring, and others.

The COVID-19 pandemic caused a semiconductor shortage that disrupted the supply chains of various industries. Even OEMs and telecom operators were struck owing to the insufficient number of physical SIM cards as SIM plants transferred their production to advanced technologies. Mobile network operatives were resistant to shifting to advanced technology. Thus, consumers needed time to replace their smartphones and other devices with new advancements.

The sales revenue incurred in 2020 was less than the projected sales. Thus, there was a slight decline in the year-on-year market, but overall, the revenue growth had a positive impact.

eSIM Market Trends

Integration of Embedded SIM Technology with 5G Devices to Augment Market Growth

5G technology is designed and developed to connect with everything; it can deliver higher-speed internet access, increased availability, better reliability, and low latency. Thus, it is offering the ability to connect M2M devices virtually on a large scale, along with privacy and security. For instance,

- STMicroelectronics launched the ST4SIM-201 embedded SIM (eSIM), a 5G M2M eSIM to carry out machine-to-machine (M2M) communication by following all the industry standards of 5G network access and M2M security.

From the connectivity perspective, 5G-enabled eSIM devices promote market growth in consumer and IoT sectors. For instance,

- According to the GSMA intelligence, among the 60 embedded SIM-enabled smartphones launched in 2021, more than half had 5G technology. Samsung and Apple were among the top players to launch 19 and 15 variants, respectively.

- OPPO, in collaboration with Thales Group, launched its first 5G SA-compatible eSIM smartphone, Find X3 Pro. The OPPO Find X3 Pro provides MNOs and customers with a 5G experience through 5G S.A. networks.

Hence, 5G is a better network for eSIMs as it enables complete digitalization of the user's journey, along with data analysis and automation, thus increasing the demand for eSIM-equipped sensors in the market.

Download Free sample to learn more about this report.

eSIM Market Growth Factors

MVNOs to Drive the Market Growth with International Roaming Services

With the eSIM technology, global connectivity issues are resolved efficiently. The physical SIM is linked to a single operator that can't be changed without going through the complete process of exchanging the SIM from the local operator. Whereas, these cards enable consumers to save multiple mobile operative profiles and be allowed to change a profile at any time OTA (over-the-air) without needing a physical SIM replacement.

Hence, Mobile Virtual Network Operators (MVNOs) are at the center of the industry with significant revenues from international roaming, International Direct Dialing (IDD), messaging, and data services, and will eliminate international roaming revenues. Several key players and new entrants are introducing new tariff plans with advanced technology for international roaming across the world. For instance,

- According to the GSMA Intelligence, more than 230 MVNOs were providing such SIM services in December 2021.

- Airalo, an MVNO that offers embedded SIM internet services in multiple countries worldwide, updated its data plans without roaming tariffs. Airalo is a Singapore-based startup founded in 2019 that provides borderless cellular connectivity services.

Smartphone users can pick an additional regional provider in a host country from the device's convenience. Thus, this technology terminates international roaming as Smart Global MVNOs enable all-in-one global connectivity and surge the demand for international roaming.

Impact of Key Drivers:

| Rank | Market Drivers | Overall Impact Rank | CAGR Contribution (2026–2034) | Impact 2026–2028 | Impact 2029–2031 | Impact 2032–2034 |

| 1 | Increasing adoption of IoT and connected devices | High | 7.00% | High | High | High |

| 2 | Growing deployment of 5G networks and increasing adoption of connected consumer electronics | High | 5.00% | Medium | High | High |

| 3 | Rising adoption of eSIM technology in automotive and connected mobility applications | Medium-High | 3.50% | Medium | High | High |

| 4 | Expansion of enterprise digital transformation and remote SIM provisioning across industries | Medium | 2.00% | Medium | Medium | High |

| 5 | Increasing penetration of eSIM-enabled smartphones, wearables, and tablets | Medium-Low | 1.50% | High | Medium | Medium |

| 6 | Others (growth of smart cities, adoption in industrial IoT, consumer preference for digital connectivity, regulatory support, increasing travel eSIM usage, etc.) | Low | 1.00% | Low | Low | Low |

| Total Positive Growth Contribution | 20.00% |

RESTRAINING FACTORS

Lack of Awareness Among Consumers Hinders the Market Growth

The eSIM market share is growing commercially, and the associated connectivity services and benefits are significant. But still, there are several parts of the world where people are unaware of the technology. The penetration of embedded SIM technology is comparatively less in developing nations, accompanied by lesser awareness and technical knowledge. For instance,

- According to the Giesecke+Devrient GmbH eSIM report, on average, only 20% of consumers are aware of this SIM technology in prominent markets. The number is even lower in some markets. Only 12% of consumers in Canada were aware of this technology, even though Canada was one of the early adopters in the market.

- 80% of consumers still don't know about this technology, thereby posing risks to large-scale adoption and hindering market growth.

Impact of Key Restraints:

|

Rank

|

Market Restraints | Overall Impact Rank | Negative CAGR Contribution (2026–2034) | Impact 2026–2028 | Impact 2029–2031 | Impact 2032–2034 |

| 1 | Limited carrier interoperability and ecosystem fragmentation | High | −1.1% | High | Medium | Low |

| 2 | Cybersecurity, privacy, and data protection concerns | Medium-High | −0.8% | Medium | Medium | High |

| 3 | Regulatory complexities and varying telecom policies across regions | Medium | −0.5% | High | Medium | Low |

| 4 | Others (consumer awareness gaps, legacy device compatibility, migration complexity, supply chain constraints, implementation costs, etc.) | Low | −0.3% | Low | Low | Low |

| Total Negative Growth Impact | −2.7% |

eSIM Market Segmentation Analysis

By Application Analysis

Increasing Demand for Connected Cars to Augment the Market Growth

As per the application, the market is split into smartphones, laptops/tablets, wearable devices, connected cars, smart home appliances, vehicle tracking, and others.

The connected cars segment will hold the largest share of 23.87% in 2026, followed by the smartphones segment. These chips allow the vehicle to be connected by several operators and allow the choice of regional operators' connectivity at the vehicle's destination country, thus driving the market for connected cars. Wearable devices such as smartwatches and smart glasses are projected to grow with the highest CAGR. Embedded SIM support and management are becoming more significant with advanced cellular-connected devices, such as AR/VR headsets, smartwatches, and mHealth devices. mHealth devices, such as glucose monitors, fall detectors, ECG monitors, and kids' or pets' trackers, are flourishing in the market. For instance,

- MetAlert partnered with POD Group to advance embedded SIM IoT connectivity. MetAlert, Inc. is a developer of wearable GPS human, remote patient monitoring, and asset tracking. MetAlert selected POD Group's ENO ONE solution for the enhancement of the Smartsole platform.

Thus, such innovations in the wearable sector are driving the demand for such cards in the market.

By Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Increasing Consumer Demand for eSIM-Enabled Devices to Create Opportunities in the Coming Years

By industry, the market is split into retail, consumer electronics, automotive, manufacturing, transportation & logistics, energy & utilities, and others (healthcare).

The intervention of eSIM technology with 5G also brings innovations in the different industrial sectors to increase the quality of existing applications. In 2023, the automotive segment accounted for the largest share of the market. Improved reliability and flexible service for connected cars and emergency call systems enhance the demand for such SIM technology in the market. It enables trucks and cars with cellular connectivity, unlocking capabilities and features. Integrating 5G technology with eSIM in the automation sector offers cellular connectivity, new mobility features, and automated capabilities to deliver a better customer experience. For instance,

- BMW Group, in partnership with Deutsche Telekom, integrated 5G and Personal eSIM networking and developed BMW iX's first premium vehicle with 5G.

- IDEMIA introduced an automotive 5G embedded SIM certified according to GSMA standards for an enriched passenger car experience. The advanced automotive offering is combined with Dual SIM Dual Active (DSDA) technology that allows carmakers to process their telematics services independently. It also enables passengers and drivers to have an ideal data stream in the vehicle with the desired carrier.

As per our research, the consumer electronics segment is projected to have the highest growth rate in the market, with tech giants expanding this SIM technology in a wide range of consumer devices. Various tech incubators are supporting startups testing advanced consumer IoT and advanced technology devices, such as headsets, smoke detectors, and kids/pets or health monitoring wearable devices.

- The consumer electronics segment is projected to dominate the market with a share of 24.63% in 2026.

The rising launch of embedded SIM-only smartphones and initiatives by vendors to improve the consumer experience for onboarding/activation help boost consumer awareness and adoption.

REGIONAL INSIGHTS

The market is studied across North America, South America, Europe, the Middle East & Africa, and Asia Pacific, and each region is further studied across countries.

North America eSIM Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

Our analysis shows that North America generates the maximum revenue share during the forecast period. The North America market was valued at USD 0.63 billion in 2025, capturing 35.70% of global revenue, and is estimated to reach USD 0.75 billion in 2026. Significant players, such as Apple Inc., Alphabet Inc., and Samsung Electronics Co. Ltd, offer embedded SIM-enabled devices and are contributing to the strong consumer demand for such devices in the region. For instance,

- According to GSMA Intelligence, awareness regarding this technology increased from 17% in 2020 to 27% in 2021. Also, more OEMs are taking initiatives to adopt this technology than telecom operators in the U.S. Thus, this is driving the demand for high-tech compatible devices in the region.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

The market in Asia Pacific reached USD 0.28 billion in 2025, representing 15.70% of total market revenue, and is projected to reach USD 0.35 billion in 2026. The report specifies that Asia Pacific will witness the maximum CAGR during the forecast period. Developing countries in the region, such as India, South Korea, and Japan, are making noteworthy advancements toward digitization and facilitating high-tech solutions with the increasing consumer demand for flexible solutions and services. The Japan market is projected to reach USD 0.049 billion by 2026, the China market is projected to reach USD 0.094 billion by 2026, and the India market is projected to reach USD 0.082 billion by 2026.

The adoption of smartphones is increasing in these developing nations. Several prominent players in the market, such as Samsung, Apple, and Google, are introducing embedded SIM technology, thus creating various opportunities in these regions. For instance,

- Reliance Jio, Bharti Airtel, and Vi were the only telecom companies to enable embedded SIM support for smartphones. The technology supports both the devices, android and iPhones.

This market is growing in Europe with the increasing advancements by key players in the region, such as Deutsche Telekom, Giesecke+Devrient GmbH, and others. For instance,

- Deutsche Telekom (DT), a German MNO, announced its decision to adopt embedded SIM technology. The company is operating in various European countries and is predominantly prioritizing the implementation of this technology. The company would provide such a SIM instead of a physical SIM to the customer, and it plans to support all devices with such technology.

South America

South America is estimated to show moderate growth during the forecast period due to high-tech companies, government investments to improve IT & telecommunication, and the growing awareness regarding advanced technology in the region. For instance,

- According to the GSMA Intelligence report 2021, SIM awareness in Brazil has increased from 22% in 2020 to 28% in 2021. Thus, the increasing awareness among consumers would create opportunities for the region's market.

Europe

In 2025, Europe held 30.80% of the global market, reaching a valuation of USD 0.54 billion, and is projected to grow to USD 0.65 billion in 2026. Europe represents a steadily expanding market for eSIM, driven by active participation from major mobile network operators and technology providers in implementing embedded SIM solutions. The region operates within a structured regulatory framework for telecommunications, data protection, and digital services, which supports secure and standardized deployment of eSIM technology across borders. Increasing initiatives by key players to replace physical SIMs with embedded alternatives are strengthening enterprise and consumer adoption. These developments are driving demand for eSIM-enabled devices across smartphones, IoT, and connected consumer electronics, contributing to consistent regional growth. The UK market is projected to reach USD 0.15 billion by 2026, and the German market is projected to reach USD 0.165 billion by 2026.

Middle East & Africa & Latin America

In 2025, the Middle East & Africa market stood at USD 0.13 billion, representing 7.20% of global demand, and is projected to grow to USD 0.16 billion in 2026. Latin America maintained a strong presence in the global market, reaching USD 0.19 billion in 2025, accounting for a 10.50% share, and is expected to reach USD 0.22 billion in 2026.

Competitive Landscape

Technological Developments by Leading Companies to Aid Market Proliferation

The key players are keen on developing embedded SIM technology solutions in numerous applications such as smartwatches, smartphones, laptops/tablets, wearable devices, and others. Development of new products and advancements in existing products to expand business opportunities are the key strategies of enterprises. Likewise, market players strategically acquire businesses and partnerships worldwide for global expansion.

List of Key Companies Profiled:

- Thales Group (France)

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- NXP Semiconductors (Netherlands)

- Giesecke+Devrient GmbH (Germany)

- Sierra Wireless Inc. (Canada)

- IDEMIA (France)

- KORE Wireless (U.S.)

- Kigen (U.K.)

- Valid S.A. (Rio de Janeiro)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Giesecke+Devrient (G+D) and AWS partnered to deliver a cloud-native eSIM management platform, enabling mobile operators and enterprises to deploy and manage eSIM services more efficiently with improved scalability and operational flexibility.

- April 2025: GSMA highlighted the commercialization of the SGP.32 IoT eSIM specification at MWC25, marking a major industry milestone that simplifies remote SIM provisioning, enhances interoperability, and accelerates enterprise and IoT eSIM adoption.

- June 2025: Kigen secured new funding to accelerate global deployment of eSIM and iSIM technologies, with investments focused on expanding secure connectivity solutions for IoT, industrial automation, and AI-enabled connected devices.

- October 2025: AT&T and Thales introduced a standardized IoT eSIM solution based on the GSMA SGP.32 specification, advancing scalable remote connectivity and simplifying lifecycle management for large-scale industrial and enterprise IoT deployments.

- February 2026: Kigen announced commercially available GSMA eUICC Security Assurance (eSA)-certified eSIMs, supporting both consumer and IoT specifications while enabling secure remote provisioning, cybersecurity compliance, and large-scale deployment of connected devices

eSIM Industry Leader Insights

Thales: Philippe Vallée, Executive Vice President, Cybersecurity & Digital Identity, emphasized that accelerating digital transformation, the expansion of secure connected devices, and increasing demand for trusted digital identities are driving sustained investment in secure connectivity platforms. His comments indicate that eSIM and digital security technologies will play an increasingly important role as enterprises and mobile ecosystems scale connected services globally. (Source: Thales Group)

Giesecke+Devrient (G+D): BeeGek Lim, Head of Digital Connectivity Solutions for APAC, stated that the eSIM market continues to expand across consumer and IoT applications, with industry collaboration and interoperable standards accelerating commercial adoption. His remarks highlight growing opportunities for secure remote connectivity as enterprises deploy increasingly connected devices worldwide. (Source: Nasdaq)

Kigen: Vincent Korstanje, Chief Executive Officer (CEO), emphasized that the next phase of industrial IoT growth depends on secure, scalable eSIM and iSIM infrastructure that simplifies device deployment while enabling AI-ready connected ecosystems. His comments reflect rising enterprise demand for flexible connectivity solutions and continued strategic investment to support long-term expansion of global IoT markets. (Source: Kigen)

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The study on the market includes prominent areas globally to gain enhanced knowledge of the industry verticals. Moreover, the research offers insights into the most recent endeavors and industry developments and an analysis of high-tech solutions being adopted promptly worldwide. It also highlights some of the growth-stimulating limitations and elements, allowing the reader to obtain a comprehensive understanding of the market.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.3% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Application

By Industry

By Region

|

Research Methodology

The market estimates in this study are triangulated using a combination of top-down, bottom-up, and primary-interview-based approaches, supported by both paid/proprietary and public data sources. Each approach is cross-validated against the others to arrive at a consistent global market size.

1. Top-Down Approach

This approach begins with the overall revenues and market shares of the leading companies operating in the eSIM ecosystem, which are then aggregated and calibrated to estimate the total global market size. The revenue contribution of each major player drawn from annual reports, investor presentations, and segment-level disclosures is mapped against the overall connectivity/IoT-semiconductor market to derive the eSIM-specific revenue pool, which is then apportioned across regions and segments (application, industry, and geography).

Companies referenced for this approach Thales Group (France), Infineon Technologies AG (Germany), STMicroelectronics (Switzerland), NXP Semiconductors (Netherlands), Giesecke+Devrient GmbH (Germany), Sierra Wireless Inc. (Canada), IDEMIA (France), KORE Wireless (U.S.), Kigen (U.K.), and Valid S.A. (Rio de Janeiro), along with device-side players such as Apple Inc., Alphabet Inc., and Samsung Electronics Co. Ltd., who were noted as key contributors to regional demand. fortunebusinessinsights

2. Bottom-Up Approach

This approach builds the market size from the ground up by analyzing country-level eSIM market size/consumption for all major markets, then aggregating these to arrive at the regional and, subsequently, the global market figure. Country-level estimates are built from local device shipment volumes, MNO/MVNO eSIM activation data, OEM penetration rates, and industry adoption patterns (automotive, consumer electronics, IoT), validated against local regulatory and telecom association data.

Countries covered: United States, Canada, Mexico, Brazil, Argentina, U.K., Germany, France, Italy, Spain, Russia, Benelux, Nordics, China, India, Japan, South Korea, ASEAN, Oceania, Turkey, Israel, GCC, South Africa, North Africa, and Rest of World.

Companies referenced for cross-verification at the country level: the same key-player set, Thales Group, Infineon Technologies AG, STMicroelectronics, NXP Semiconductors, Giesecke+Devrient GmbH, Sierra Wireless Inc., IDEMIA, KORE Wireless, Kigen, and Valid S.A., supplemented by region-specific operators such as Deutsche Telekom, Reliance Jio, Bharti Airtel, and Vi, whose regional deployments help validate country-specific estimates.

3. Primary Research / Stakeholder Interview Approach

Structured interviews and discussions are conducted with stakeholders across both the supply side and the demand/end-user side of the value chain to validate secondary findings, fill data gaps, and capture qualitative insight on trends, pricing, and adoption barriers.

Supply-side respondents:

- CEOs, CTOs, and VPs of Product/Strategy at eSIM chip and module manufacturers

- Sales Managers and Business Development Managers at semiconductor and connectivity solution providers

- Product Managers overseeing eSIM/IoT connectivity platforms

- Regional Sales Heads at MNOs/MVNOs offering eSIM-enabled plans

Demand/end-user side respondents:

- Procurement Managers and Category Managers at OEMs (smartphone, wearable, automotive)

- IT/Connectivity Managers at enterprises deploying IoT/M2M fleets

- Telecom analysts and industry consultants

- Distributors and channel partners handling SIM/eSIM provisioning

4. Data Sources

Company-level sources:

- Annual reports and investor presentations of key companies: Thales Group, Infineon Technologies AG, STMicroelectronics, NXP Semiconductors, Giesecke+Devrient GmbH, Sierra Wireless Inc., IDEMIA, KORE Wireless, Kigen, and Valid S.A. fortunebusinessinsights

- Press releases and corporate disclosures on partnerships/product launches (e.g., IDEMIA–Microsoft, Sierra Wireless–Orange Wholesale, NXP–Qualcomm collaborations)

Association/industry body sources:

- GSMA / GSMA Intelligence reports (eSIM adoption, awareness surveys, 5G-eSIM device tracking)

- Giesecke+Devrient GmbH eSIM consumer awareness reports

- Regional telecom regulatory bodies (e.g., national telecom authorities in the U.S., EU, India)

Interview sources:

Direct interviews/discussions with representatives at the key companies profiled above (Thales Group, Infineon, STMicroelectronics, NXP, Giesecke+Devrient, Sierra Wireless, IDEMIA, KORE Wireless, Kigen, Valid S.A.) and select MNOs/MVNOs (Deutsche Telekom, Airalo)

5. Triangulation & Validation

The market estimates from the top-down and bottom-up approaches are cross-checked against each other and against primary interview inputs. Discrepancies are resolved by revisiting company financials, country-level demand drivers, and stakeholder feedback until convergence is achieved, ensuring the final market figures reflect a statistically and logically consistent global estimate.

Author Section

Technology Team

This report has been developed by Fortune Business Insights' dedicated analyst team specializing in the Next Generation Technology segment. Our analysts continuously monitor technological advancements, regulatory developments, competitive strategies, product innovations, investment activities, and evolving customer requirements across the segment. By combining extensive primary interviews with rigorous secondary research and proprietary market modeling, the team delivers comprehensive, accurate, and actionable insights into the eSIM market. This domain-focused research approach ensures that the report reflects the latest industry developments while providing strategic intelligence to support informed business decisions.

Frequently Asked Questions

The market is projected to reach USD 7.62 billion by 2034.

In 2025, the market stood at USD 1.76 billion.

The market is projected to grow at a CAGR of 17.3% over the forecast period (2026-2034).

Smartphones, connected cars, and wearable devices are likely to lead the market.

Wearable devices will boost sales in the market.

Thales Group, STMicroelectronics, Giesecke Devrient GmbH, Sierra Wireless Inc., IDEMIA, and NXP Semiconductors are the top players in the market.

North America is expected to hold the highest market share.

By Industry, consumer electronics is expected to grow with the highest CAGR.

- 2021-2034

- 2025

- 2021-2024

- 130

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us