3D Printing Filament Market Size, Share & Industry Analysis, By Material Type (PLA (Polylactic Acid), ABS (Acrylonitrile Butadiene Styrene), PETG (Polyethylene Terephthalate Glycol),Nylon (Polyamide), TPU/TPE (Thermoplastic Polyurethane/Elastomers), Composite Filaments, Polycarbonate (PC), and Others), By Application (Prototyping, Functional Parts & End-Use Components, Tooling & Fixtures, Visual Models & Concept Design, and Others), By End Use Industry (Aerospace & Defense , Automotive, Healthcare & Medical Devices, Consumer Electronics, and Others), Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

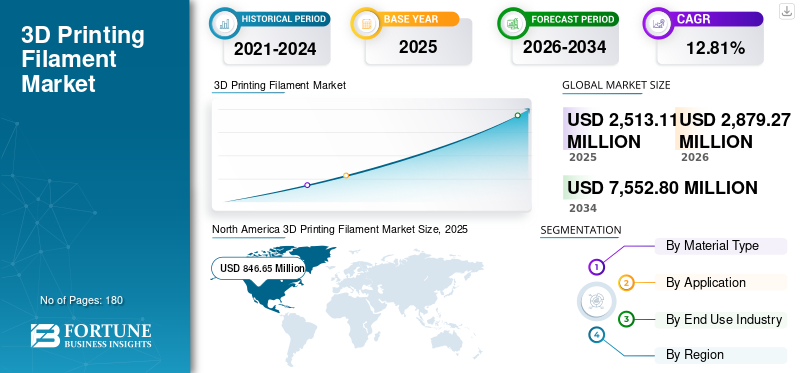

The global 3D printing filament market size was valued at USD 2,513.11 million in 2025. The market is projected to grow from USD 2,879.27 million in 2026 to USD 7,552.80 million by 2034, exhibiting a CAGR of 12.81% during the forecast period. North America dominated the global market with a market share of 33.7% in 2025.

The growth of the 3D printing filament market is primarily driven by the rapid expansion of fused deposition modeling (FDM/FFF), adoption of 3d printing across industrial, commercial, and consumer segments. Globally, millions of desktop and industrial FDM printers are in operation, and each printer requires recurring filament consumption, creating a strong repeat-purchase demand. The increasing shift of 3D printing from prototyping to functional parts, tooling, jigs, and fixtures is significantly boosting filament usage volumes. Industrial users typically consume 5–10× more filament per printer than hobby users, accelerating market growth.

In addition, the rising adoption of engineering and composite filaments such as PETG, nylon, TPU, and carbon-fiber-reinforced materials is increasing the average selling price of filaments.

- For instance, in December 2025, supermaterial innovator Lyten announced the release of two new high-performance additive manufacturing products, including a PA1205 3D printing filament powered by Lyten’s graphene-enhanced technology. The PA1205 filament delivers significantly improved mechanical strength, such as up to 100% greater X/Y-axis strength and 43% higher Z-axis strength, compared with conventional composite filaments, making it suitable for demanding applications in motorsports, aerospace, and defense.

Polymaker is a global 3D printing materials company specializing in high-quality filaments for FDM/FFF printers. Based in Shanghai with offices in North America and Europe, Polymaker produces a wide range of polymers, including PLA, ABS, PETG, nylon, TPU, and advanced composites.

Download Free sample to learn more about this report.

3D PRINTING FILAMENT MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2,513.11 Million

- 2026 Market Size: USD 2,879.27 Million

- 2034 Forecast Market Size: USD 7,552.80 Million

- CAGR: 12.81% from 2026–2034

- North America dominated the 3D printing filament market with a 33.7% share in 2025.

- The PLA (Polylactic Acid) segment held the largest market share in 2025.

- The aerospace & defense segment dominated the market in 2025.

North America

North America reached USD 846.85 million in 2025, accounting for 33.7% of global market revenue.

Asia Pacific

Asia Pacific was valued at USD 781.61 million in 2025, ranking as the second-largest regional market.

Europe

Europe reached USD 641.68 million in 2025 and is projected to grow at a CAGR of 12.94%.

U.S.

The market was valued at USD 651.26 million in 2025, accounting for 25.91% of global revenue.

Japan

The market was valued at USD 113.09 million in 2025, representing 4.50% of global revenue.

Read More

3D PRINTING FILAMENT MARKET TRENDS

A Shift from Basic Filaments to Engineering & Composite Materials are the Key Market Trends

The 3D printing filament market is witnessing rapid evolution driven by material innovation, industrial adoption, and sustainability initiatives. One of the key trends is the shift from basic filaments to engineering and composite materials. While PLA and ABS still account for a significant portion of usage, increasing demand for PETG, nylon, TPU, and carbon-fiber-reinforced filaments is rising as 3D printing moves beyond prototyping to functional and end-use parts. Industrial users now consume up to 5–10 times more filament per printer than hobbyists, supporting higher overall volumes.

Another major trend is the growing focus on sustainability, with manufacturers introducing recycled and bio-based filaments to reduce environmental impact. Additionally, print farms and service bureaus are expanding rapidly, driving bulk filament consumption and consistent demand.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rise in the Installed Base of 3D Printers

The 3D printing filament market is driven by the expanding adoption of fused deposition modeling (FDM/FFF) technology across industrial, commercial, and educational sectors. One of the primary drivers is the growing installed base of 3D printers, which has reached millions of units globally, creating continuous demand for consumable filaments.

As 3D printing transitions from rapid prototyping to functional and end-use part production, filament consumption per printer is rising significantly, with industrial users typically consuming three to five kilograms per month, compared to less than one kilogram for hobby users. In addition, the increasing use of 3D printing for tooling, jigs, and fixtures, which reduces lead times by up to 70% and lowers manufacturing costs, is driving the market growth.

MARKET RESTRAINTS

High Cost of Advanced and Specialty Filaments

The high cost of advanced and specialty filaments, such as composites, nylon, and high-temperature materials, can cost 3–10 times more than standard PLA or ABS. This restricts usage among small businesses, educational institutions, and hobbyists with limited budgets. Another restraint is inconsistent filament quality, including diameter variations and moisture sensitivity, which can lead to print failures, material waste, and increased operating costs, particularly in low-cost or unbranded filaments. Additionally, material limitations of FDM filaments, such as lower surface finish and mechanical strength compared to injection-molded plastics, reduce suitability for certain high-precision applications.

MARKET OPPORTUNITIES

Increasing Use of 3D Printing Filament in the Healthcare Sector is Driving the Growth Opportunities

The increasing use of 3D printing in the healthcare sector is creating a strong market opportunity for 3D printing filaments, driven by the need for customization, speed, and cost efficiency. Hospitals and medical device manufacturers are widely adopting FDM-based 3D printing to produce patient-specific anatomical models, surgical guides, prosthetics, orthotics, and medical tools, all of which rely heavily on filament materials.

For instance, PLA and PETG filaments are commonly used for anatomical models that help surgeons plan complex procedures, while TPU filaments are increasingly used for flexible prosthetics, braces, and wearable medical components. In many hospitals, 3D-printed surgical guides have been shown to reduce operation time by 20–30%, improving clinical outcomes and efficiency.

MARKET CHALLENGES

Raw Material Price Volatility & Supply Chain Disruption Present Significant Challenges for Market Growth

Raw material price volatility and supply chain disruptions represent a significant challenge for the 3D printing filament market, directly affecting production stability and pricing consistency. Filaments are primarily manufactured from petroleum-based polymers and specialty additives whose prices fluctuate due to changes in crude oil costs, energy prices, and global demand-supply imbalances. Sudden increases in resin prices can raise filament production costs, forcing manufacturers to either absorb margin pressure or pass higher prices on to customers.

In addition, supply chain disruptions caused by logistics bottlenecks, trade restrictions, or geopolitical tensions can delay the procurement of critical raw materials and colorants, extending lead times and reducing product availability. Smaller filament producers are particularly vulnerable, as they often lack long-term supply contracts or diversified sourcing options.

Segmentation Analysis

By Material Type

PLA (Polylactic Acid) is Dominant as it is Majorly Used Across Automotive, Aerospace & Defense Sector

Based on the segmentation of material type, the market is classified into PLA (Polylactic Acid), ABS (Acrylonitrile Butadiene Styrene), PETG (Polyethylene Terephthalate Glycol), Nylon (Polyamide), TPU/TPE(Thermoplastic Polyurethane / Elastomers), Composite Filaments, Polycarbonate (PC), and Others. In 2025, the PLA (Polylactic Acid) segment dominated the market share. The ease of printing, low warping, dimensional accuracy, and cost effectiveness of PLA make it ideal for producing complex prototype components quickly. Additionally, PLA’s biodegradable nature supports sustainability goals, further strengthening its adoption across these industries.

The composite filaments segment is experiencing the highest growth and is expected to grow at a CAGR of 18.41%.

To know how our report can help streamline your business, Speak to Analyst

By Application

Prototyping is Dominant Because 3D Printing Enables Rapid, Low-Cost Design Iteration and Functional Testing

On the basis of the segmentation of application, the market is classified into prototyping, functional parts & end-use components, tooling & fixtures, visual models & concept design, educational & training models, and others. In 2025, the prototyping segment dominated the global market. Prototyping is a major driver of the 3D printing filament market because it enables faster product development, design flexibility, and significant cost savings across industries. Companies increasingly rely on rapid prototyping to shorten development cycles, as 3D printing allows engineers to produce and test multiple design iterations within days instead of weeks. This reduces reliance on expensive tooling and molds, which can account for a large share of early-stage product costs. Prototyping also supports early detection of design flaws, helping manufacturers avoid costly revisions at later stages.

The functional parts & end-use components segment is expected to grow at a CAGR of 14.81%.

By End Use Industry

The Aerospace & Defense Sector Widely Uses 3D Printing Filament Due to Its Ability to Support Rapid Prototyping and Lightweight Part Production

On the basis of the segmentation of end use industry, the market is classified into aerospace & defense, automotive, healthcare & medical devices, consumer electronics, industrial manufacturing, and others. In 2025, the aerospace & defense segment dominated the global market. Aerospace and defense manufacturers rely on filament-based 3D printing to create functional prototypes, tooling, jigs, and fixtures that meet precise dimensional and performance requirements. Filaments such as PETG, nylon, polycarbonate, and composite materials are used to produce durable parts capable of withstanding mechanical stress and elevated temperatures.

The healthcare & medical devices segment is expected to grow at a CAGR of 15.11%.

3D Printing Filament Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America 3D Printing Filament Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 846.85 million, and also took the leading share in 2026 with USD 961.76 million.

North America’s 3D printing filament market is driven by strong adoption of additive manufacturing across aerospace, automotive, healthcare, and industrial sectors. The region benefits from a large installed base of FDM/FFF printers, advanced R&D infrastructure, and widespread use of 3D printing for prototyping, tooling, and end-use parts. High investment in innovation and rapid technology commercialization further supports sustained filament demand.

U.S. 3D Printing Filament Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 651.26 million in 2025, accounting for roughly 25.91% of the global market size.

Europe

Europe is projected to record a growth rate of 12.94% in the coming years, which is the third highest among all regions, and reach a valuation of USD 641.68 million by 2025. Europe’s 3D printing filament market is driven by strong adoption of additive manufacturing across automotive industrial, aerospace, industrial manufacturing, and healthcare sectors. The region emphasizes precision engineering, sustainability, and advanced manufacturing practices, supporting consistent filament demand. Increasing use of 3D printing for tooling, jigs, fixtures, and low-volume production, along with strong integration in education and research institutions, automotive and consumer goods, continues to accelerate market growth across Europe.

Germany 3D Printing Filament Market

The Germany 3D printing filament market in 2025 is estimated to be around USD 204.78 million 2025 and is estimated at around USD 238.05 million, representing roughly 8.15% of the global 3D printing filament revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 781.61 million in 2025 and secure the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 159.98 million and USD 295.26 million, respectively, in 2025.

Asia Pacific’s 3D printing filament market is driven by rapid industrialization, expanding manufacturing capacity, and increasing adoption of sustainable bio based, additive manufacturing in automotive, electronics, and industrial sectors. Strong growth in China and India, rising use of 3D printing in prototyping and tooling, and expanding education and startup ecosystems are boosting filament consumption.

Japan 3D Printing Filament Market

The Japan 3D Printing Filament market in 2025 is estimated at around USD 113.09 million, accounting for roughly 4.50% of global 3D printing filament revenues.

Japan’s 3D printing filament market is driven by its advanced manufacturing ecosystem, strong precision engineering culture, and increasing use of additive manufacturing in automotive, electronics, and industrial applications.

China 3D Printing Filament Market

China’s 3D printing filament market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 295.26 million, representing roughly 11.75% of the global 3D printing filament.

India 3D Printing Filament Market

The India 3D printing filament market in 2025 is estimated at around USD 159.98 million, accounting for roughly 6.37% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 152.89 million in 2025.

Latin America’s 3D printing filament market is being driven by the increasing localization of manufacturing and the need to reduce import dependence through cost-efficient, on-demand production using filament-based 3D printing.

Brazil 3D Printing Filament Market

Brazil's 3D printing filament market is projected to be around USD 70.46 million in 2025, representing roughly 2.80% of the global 3D printing filament market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market is set to reach a valuation of USD 90.09 million in 2025.

The Middle East & Africa 3D printing filament market is driven by government-led industrial diversification programs and the growing use of additive manufacturing for localized production in infrastructure, oil & gas maintenance, and defense-related applications.

GCC 3D Printing Filament Market

The GCC 3D printing filament market is projected to be around USD 48.59 million in 2025, representing roughly 1.93% of the global 3D printing filament market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors are actively expanding their 3D printing filament market share via partnerships, business expansion, and technological advancements.

The global 3D printing filament market holds a fragmented market structure, constituting prominent players such as Höganäs AB, 3D Systems Corporation, Stratasys, Ltd., and others. Companies operating in the 3D Printing Filament are adopting targeted growth strategies focused on strengthening technical capability, expanding manufacturing presence, and improving access to high-demand sectors.

- For instance, in January 2025, Stratasys, Ltd. launched its TrueDent solution in Europe, introducing monolithic digital dentures to the regional dental market while strengthening distribution agreements with key partners such as Galimplant, Gold Quadrat, and Métaux Précieux. The move positions Stratasys to expand its polymer 3D printing materials portfolio, including filament-based solutions, into the dental and medical segment, reflecting its broader strategy to grow materials adoption across industries.

Other key players in the global market include Evonik Industries AG, General Electric, Arcam AB, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY 3D PRINTING FILAMENT COMPANIES PROFILED

- Höganäs AB (Sweden)

- 3D Systems Corporation (United States)

- Stratasys, Ltd. (Israel)

- Evonik Industries AG (Germany)

- General Electric (United States)

- Arcam AB (Sweden)

- Royal DSM N.V (Netherlands)

- Arkema S.A (France)

- ExOne (United States)

- Polymaker (China)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, Stratasys, Ltd. unveiled an expanded suite of materials, improved features, and software enhancements to support broader additive manufacturing adoption across industries such as aerospace, automotive, healthcare, and consumer products. These updates aim to streamline workflows and enhance reliability when printing with polymer materials and advanced filament types, reinforcing Stratasys’s commitment to high-performance AM solutions.

- In April 2025, Stratasys introduced new validated materials for its F900 fused deposition modeling (FDM) system, including AIS Antero 800NA and AIS Antero 840CN03. These advanced filaments are designed for aerospace, defense, and industrial applications, offering enhanced performance and reliability in large-scale additive manufacturing environments where high heat and mechanical stress resistance are critical.

- In March 2025, Evonik announced continued expansion of its INFINAM portfolio, focusing on high-performance polymer filaments for industrial 3D printing. The materials are engineered for durability, thermal stability, and consistent print performance, supporting applications in engineering, medical devices, and advanced manufacturing.

- In October 2024, Evonik disclosed new automation initiatives at its thermoplastics facilities to improve polymer consistency and scalability for additive manufacturing materials. While not limited to filaments, the initiative strengthens the supply chain for filament-grade polymers.

- In June 2024, Arkema announced progress in developing specialty polymer feedstocks optimized for 3D printing filament production. The materials are designed to improve strength, flexibility, and thermal performance, supporting demanding industrial applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.81% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Material Type, Application, End Use Industry, and Region |

|

By Material Type |

· PLA (Polylactic Acid) · ABS (Acrylonitrile Butadiene Styrene) · PETG (Polyethylene Terephthalate Glycol) · Nylon (Polyamide) · TPU/TPE(Thermoplastic Polyurethane / Elastomers) · Composite Filaments · Polycarbonate (PC) · Others |

|

By Application |

· Prototyping · Functional Parts & End-Use Components · Tooling & Fixtures · Visual Models & Concept Design · Educational & Training Models · Others |

|

By End Use Industry |

· Aerospace & Defense · Automotive · Healthcare & Medical Devices · Consumer Electronics · Industrial Manufacturing · Others |

|

By Geography |

· North America (By Material Type, Application, End Use Industry, and Country) o U.S. o Canada · Europe (By Material Type, Application, End Use Industry, and Country) o UK o Germany o France o Spain o Italy o Rest of Europe · Asia Pacific (By Material Type, Application, End Use Industry, and Country) o China o India o Japan o Australia o South Korea o Rest of Asia Pacific · Latin America (By Material Type, Application, End Use Industry, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Material Type, Application, End Use Industry, and Country) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2,513.11 million in 2025 and is projected to reach USD 7,552.80 million by 2034.

In 2025, the market value stood at USD 846.85 million.

The market is expected to exhibit a CAGR of 12.81% during the forecast period of 2026-2034.

The PLA (Polylactic Acid) 3D printing filament segment led the market by material type.

Increasing adoption of localized, on-demand manufacturing to reduce inventory holding and spare-parts downtime is driving growth in the 3D printing filament market.

Hoganas AB, 3D Systems Corporation, Stratasys, Ltd., Evonik Industries AG, and others are some of the prominent players in the market.

North America dominated the market in 2025.

Wider adoption of digital manufacturing, demand for rapid design iteration, material performance improvements, and the need for cost-efficient, flexible production are the major factors expected to favor 3D printing technology adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us