Acrylic Polymers Market Size, Share & Industry Analysis, By Type (Waterborne and Solvent-borne), By Application (Paints & Coatings, Adhesives & Sealants, Construction, Textiles & Nonwovens, Paper & Packaging, and Others), and Regional Forecast, 2025-2032

Acrylic Polymers Market Size and Future Outlook

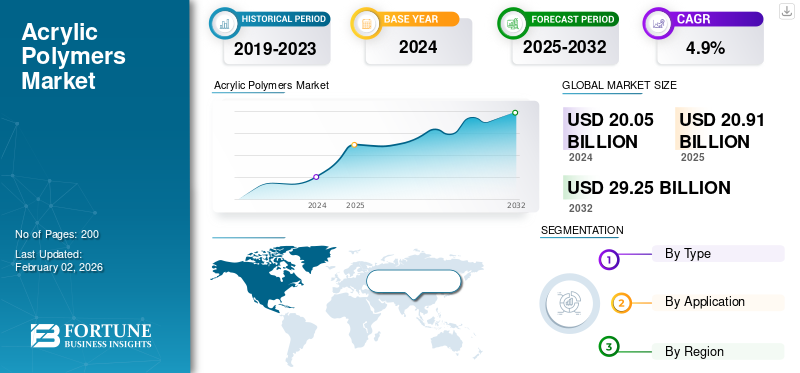

The global acrylic polymers market size was valued at USD 20.05 billion in 2024. The market is projected to grow from USD 20.91 billion in 2025 to USD 29.25 billion by 2032, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the global acrylic polymer market with a market share of 43.24% in 2024.

Acrylic polymers are a wide family of synthetic polymers made from acrylic acid, methacrylic acid, and their esters. They are produced through free-radical polymerization, a process in which monomers, such as methyl methacrylate (MMA), ethyl acrylate, or butyl acrylate, join together to form long molecular chains. Chemically, acrylic polymers have a carbon-based backbone with pendant acrylate or methacrylate groups that provide excellent resistance to UV radiation, weathering, and oxidation. These properties make them durable that retain clarity, color, and performance even in tough outdoor conditions. The polymers can be formulated as thermoplastics, elastomers, or latex emulsions, each serving different industrial uses. They are widely used across various industries, including construction, automotive, packaging, textiles, and paints and coatings.

The market is driven by rising demand for high-performance, weather-resistant materials that offer durability, optical clarity, and chemical stability. The versatility of acrylic polymers, which can be engineered into rigid plastics, flexible films, or water-based emulsions, allows manufacturers to tailor them for both industrial and consumer applications.

Furthermore, the market encompasses several major players, including Mallard Creek Polymers, TOAGOSEI CO., LTD., NIPPON SHOKUBAI CO., LTD., KAMSONS POLYMER LIMITED, and Celanese Corporation. A broad portfolio, innovative product launches, and strong geographic presence have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Acrylic Polymer Market KEY TAKEAWAYS

- 2024 Market Size: USD 20.05 billion

- 2025 Market Size: USD 20.91 billion

- 2032 Forecast Market Size: USD 29.25 billion

- CAGR: 4.9% from 2025–2032

- Asia Pacific dominated the acrylic polymers market with a 43.24% share in 2024.

- The waterborne segment held the largest market share in 2024.

- The paints & coatings segment accounted for a 36.6% share in 2025.

Asia Pacific

Asia Pacific USD 8.67 billion in 2024. Strong industrialization, infrastructure growth, and demand from paints, coatings, adhesives, and construction driving dominance.

Europe

Europe USD 4.83 billion in 2025. Green construction initiatives, strong R&D, and demand for specialty coatings driving regional expansion.

North America

North America USD 4.42 billion in 2025. Mature coatings and adhesives industry with strong shift toward low-VOC and waterborne acrylic systems supporting growth.

U.S.

U.S. USD 3.71 billion in 2025. Strong demand from paints, coatings, adhesives, packaging, and infrastructure renovation driving market growth.

Japan

Japan Rising demand for low-VOC and waterborne acrylic systems driven by strict environmental regulations and sustainability focus.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Demand from Construction and Infrastructure Development to Propel the Market Growth

Acrylic-based coatings, adhesives, sealants, and waterproofing compounds are widely used in residential, commercial, and civil engineering applications due to their superior weather resistance, adhesion, and UV protection. In emerging economies such as India, China, and Indonesia, large-scale urban development projects are accelerating the consumption of acrylic emulsions for architectural paints and façade coatings. Developed regions, such as North America and Europe, are also witnessing a rise in renovation and retrofitting activities, further supporting demand for sustainable, low-VOC acrylic coatings. Additionally, acrylic polymers’ excellent durability and aesthetic properties make them preferred materials for protective and decorative coatings in infrastructure such as bridges, highways, and buildings. The shift toward energy-efficient and environmentally friendly construction materials also favors water-based acrylic formulations over solvent-based alternatives.

MARKET RESTRAINTS:

Volatility in Raw Material Prices to Restrict Market Expansion

The high volatility of raw material prices for acrylate monomers, such as methyl methacrylate (MMA), butyl acrylate, and ethyl acrylate, restrains the acrylic polymers market growth. These feedstocks are derived from petrochemical sources, such as propylene, which are subject to frequent price fluctuations due to instability in the crude oil market and disruptions to the supply chain. When crude oil prices surge, production costs for acrylic monomers rise sharply, squeezing profit margins for polymer manufacturers and downstream users.

- For instance, the global MMA market experienced price spikes in 2022–2023, following energy crises in Europe and supply tightness in Asia, which compelled manufacturers to pass on higher costs to coatings and adhesive producers.

MARKET OPPORTUNITIES:

Shift Toward Sustainable and Low-VOC Formulations to Create Lucrative Growth Opportunities

Acrylic polymers are increasingly preferred for producing waterborne paints, coatings, and adhesives that replace traditional solvent-based systems. These water-based acrylics emit significantly lower levels of Volatile Organic Compounds (VOCs), aligning with stricter emission standards in regions such as Europe and North America. Organizations such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) are enforcing policies to reduce air pollutants, compelling the industry to adopt greener technologies.

- For example, companies such as Dow and Arkema have launched bio-based and recyclable acrylic polymers derived from renewable raw materials to meet their sustainability goals.

MARKET CHALLENGES:

Environmental and Regulatory Challenges to Hamper Market Growth

Many acrylic monomers and additives including methyl methacrylate and certain plasticizers, are derived from non-renewable petrochemical sources and emit Volatile Organic Compounds (VOCs) during manufacturing or application. Governments across the European Union, U.S., and Japan are tightening their restrictions on VOC emissions, hazardous waste, and microplastic release, compelling companies to reformulate or invest in costly compliance technologies.

- For example, under the European REACH regulation, stricter chemical safety standards have increased the compliance burden for acrylic polymer producers operating in the region.

ACRYLIC POLYMERS MARKET TRENDS:

Advancements in Polymer Technology and Product Innovation are One of the Significant Market Trends

Modern polymer design enables fine-tuning of molecular weight, particle size, and functional groups to achieve specific mechanical and optical properties. For instance, new-generation acrylic copolymers exhibit improved impact strength, chemical resistance, and thermal stability, expanding their utility in high-performance applications such as medical devices, electronics, and 3D printing. Emulsion polymerization and controlled radical polymerization techniques are allowing manufacturers to create customized latexes for specialty coatings and adhesives with enhanced performance and reduced environmental impact. Companies like Mitsubishi Chemical and Evonik have introduced specialty acrylics tailored for advanced applications, including optical films and electronic encapsulants.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Waterborne Coatings Held the Dominant Share Due to Their Sustainable Nature

The market is segmented by type, and it is classified into waterborne and solvent-borne.

The waterborne segment held the largest acrylic polymers market share in 2024 and is expected to experience substantial growth due to the increasing global emphasis on environmental sustainability and stricter VOC emission regulations. These formulations utilize water as the primary solvent, resulting in significantly reduced toxic emissions compared to solvent-borne counterparts. Governments in Europe, North America, and certain parts of Asia have implemented stringent standards that promote the use of water-based coatings and adhesives. Additionally, advancements in emulsion polymerization have improved film formation, durability, and weather resistance, thereby expanding their applications in architectural paints, industrial coatings, and packaging adhesives.

The growth of the solvent-borne segment is driven by its rising demand in developing economies, where regulatory constraints are not that strict and cost efficiency remains a priority. Additionally, advancements in high-solids and low-VOC solvent-borne formulations have helped maintain their relevance in performance-critical markets. Marine and aerospace industries and protective coatings continue to rely on these systems for their long-term durability and gloss retention.

By Application

Paints & Coatings Segment Takes the Leading Share Owing to Increasing Demand for Food, Beverage, And Pharmaceutical Applications

Based on application, the market is segmented into paints & coatings, adhesives & sealants, construction, textiles & nonwovens, paper & packaging, and others.

The paints & coatings segment dominates the market, driven by acrylic polymers’ excellent weatherability, gloss retention, and color stability. Their ability to form durable, UV-resistant films makes them ideal for architectural, automotive, and industrial coatings. The global shift toward waterborne formulations, driven by stricter VOC emission regulations, is further fueling demand for acrylic emulsions and resins. Additionally, growing construction and infrastructure spending, particularly in the Asia Pacific region, is driving the increased consumption of decorative coatings. Furthermore, the segment holds a share of 36.6% in 2025.

The adhesives & sealants segment is expected to witness a favorable growth throughout the forecast period. This expansion is attributed to its increasing use in the construction, packaging, automotive, and electronics industries, offering quick curing and strong adhesion to a diverse range of substrates. Growth in demand is supported by shift toward lightweight, high-performance materials, and waterborne systems that meet environmental standards. Acrylic-based pressure-sensitive adhesives (PSAs) are expanding their applications in labels, tapes, and medical products, further strengthening their demand. The superior balance between flexibility and durability keeps acrylic polymers a preferred binder and film former in modern adhesive formulations. In addition, adhesives & sealants application is projected to grow at a CAGR of 4.7% during the study period.

The growth of the construction segment in the market is driven by increased spending on residential and commercial projects across the Asia Pacific and the Middle East. The trend of green building solutions is accelerating the use of low-VOC, water-based acrylic emulsions in exterior paints, sealants, and admixtures. Moreover, renovation projects are sustaining the demand for high-performance surface coatings.

The growth of the textiles & nonwovens segment is driven by rising demand for technical textiles in automotive, filtration, and healthcare sectors. The increasing demand for hygiene products, including wipes and medical disposables, is further driving the need for acrylic binders.

The growth of the paper & packaging segment is driven by the rising consumption of flexible packaging and label materials, propelled by the demand from e-commerce and food delivery sectors. Acrylic emulsions allows for development of low-VOC, recyclable coatings and pressure-sensitive adhesives, aligning with sustainability mandates and circular economy goals. Moreover, companies emphasis on eco-friendly packaging solutions has accelerated the replacement of solvent-based systems.

To know how our report can help streamline your business, Speak to Analyst

Acrylic Polymers Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Acrylic Polymers Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the dominant share in 2023, valued at USD 8.28 billion, and maintained its leading position in 2024, with a value of USD 8.67 billion. The factors fostering the region's dominance include rapid industrialization, infrastructure expansion, and robust manufacturing activities. Major economies such as China, India, Japan, and South Korea are witnessing high demand from the paints and coatings, adhesives, and construction. The region’s focus on waterborne technologies, urban housing, and automotive refinishing continues to strengthen the demand for the product. China’s massive construction programs and India’s growing textile and packaging industries are further reinforcing regional growth.

Additionally, the cost competitiveness of local resin producers and their capacity expansions support the supply base. Rising environmental regulations in Japan and South Korea are driving demand for greener, low-VOC acrylic formulations, thereby amplifying the need for sustainable systems. In 2025, the China market is estimated to reach USD 2.64 billion.

- China is the fastest-growing market, driven by rapid industrial growth, urbanization, and dominant manufacturing output in paints, coatings, textiles, and packaging. Massive construction projects, both residential and commercial, are sustaining high demand for acrylic emulsions and waterproof coatings. The government’s focus on low-VOC and environmentally friendly materials, supported by tightening emission norms, is accelerating the transition to waterborne acrylic systems.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is expected to experience significant growth in the years to come. During the forecast period, the European region is projected to record a growth rate of 4.8%, the second-highest among all regions, and reach a valuation of USD 4.83 billion by 2025. Green construction initiatives, energy-efficient building renovations, and innovation in specialty coatings drive the market's growth in the region. Germany, France, and Italy lead the production of high-value acrylic resins for industrial and performance applications. The region’s strong R&D orientation, focusing on bio-acrylics, UV-curable polymers, and recyclability continues to define competitive differentiation. Backed by these factors, countries including the U.K. are expected to record valuations of USD 0.56 billion, Germany USD 1.01 billion, and France USD 0.55 billion in 2025.

North America

After Europe, the market in North America is estimated to reach USD 4.42 billion in 2025 and secure the position of the third-largest region in the market. The market growth is driven by a mature yet innovation-intensive paints and coatings sector for architectural and industrial applications. The region emphasizes low-VOC, waterborne, and high-solid acrylic systems to meet stringent EPA and state-level environmental standards. Rising investments in residential renovation, infrastructure upgrades, and packaging innovation in the U.S. are expanding end-use demand. The adhesives and sealants industry also benefits from strong manufacturing and e-commerce growth. In 2025, the U.S. market is estimated to reach USD 3.71 billion.

In the U.S., the market is driven by mature yet evolving end-use industries, including paints and coatings, adhesives, and packaging, which are underpinned by steady housing, automotive, and manufacturing activities. Stricter EPA and state-level VOC regulations are accelerating the shift toward waterborne and high-solid acrylic systems. Investments in green building renovation, advanced packaging technologies, and infrastructure renewal are expanding the scope of application. Furthermore, the rise of e-commerce and electric vehicles boosts demand for high-performance adhesives and coatings. Innovation in bio-based and recyclable acrylic formulations aligns with the country’s broader sustainability commitments.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2025 is expected to reach a valuation of USD 1.52 billion. The market's growth in the region is driven by expansion in infrastructure, automotive refinishing, and packaging applications. Local coatings manufacturers are gradually transitioning from solvent-borne to waterborne acrylic systems in response to rising environmental awareness. Government initiatives promoting affordable housing and industrialization also contribute to construction-driven demand.

In the Middle East and Africa, the GCC is expected to reach a value of USD 0.46 billion by 2025. The market’s growth is attributed to the expansion of infrastructure, construction, and industrial projects across the Gulf Cooperation Council (GCC) nations and North Africa. Mega-development programs, such as Saudi Arabia’s NEOM, the UAE’s smart city initiatives, and Egypt's infrastructure modernization efforts, are driving demand for acrylic-based paints, coatings, and waterproofing materials. The region’s warm climate and its need for UV- and heat-resistant coatings enhance the appeal of acrylic formulations.

COMPETITIVE LANDSCAPE

Key Industry Players:

Key Market Participants are Witnessing Growth Prospects By Providing Innovative Paints & Coatings Solutions

The global market is fragmented in nature. It is characterized by the presence of numerous global, regional, and small-scale manufacturers, suppliers, and traders, rather than being dominated by a few major corporations. Major players in the market include Mallard Creek Polymers, TOAGOSEI CO., LTD., NIPPON SHOKUBAI CO., LTD., KAMSONS POLYMER LIMITED, and Celanese Corporation. Producers in North America and Europe are aiming to expand their presence in China and other countries across Asia Pacific to strengthen their market positions and increase their market share. To achieve this, key market players have developed a strong regional presence, established effective distribution channels, and offered a broad range of products.

LIST OF KEY ACRYLIC POLYMERS COMPANIES PROFILED:

- Mallard Creek Polymers (Germany)

- TOAGOSEI CO., LTD. (Japan)

- NIPPON SHOKUBAI CO., LTD. (Japan)

- KAMSONS POLYMER LIMITED (India)

- Celanese Corporation (U.S.)

- Plaskolite (U.S.)

- Gellner Industrial (U.S.)

- Evonik (Germany)

- Lubrizol (U.S.)

- Capital Resin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2022: Arkema introduced mass-balance, bio-attributed acrylic monomers (certified), enabling lower-carbon specialty acrylic additives and resins across multiple end uses.

- July 2022: BASF completed the installation and start-up of a state-of-the-art acrylic dispersions line in Dahej, India, boosting supply for South Asia across coatings, construction, adhesives, and paper.

- March 2021: BASF commenced operations of a new acrylic dispersions line at Pasir Gudang, Malaysia, doubling regional capacity for coatings, construction, adhesives, and packaging customers.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 4.9% from 2025-2032 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 20.05 billion in 2024 and is projected to reach USD 29.25 billion by 2032.

In 2024, the market value stood at USD 8.67 billion.

The market is expected to exhibit a CAGR of 4.9% during the forecast period.

The waterborne segment led the market by type.

Rising demand from the paints & coatings, adhesives & sealants, and construction sectors, driven by superior durability, weather resistance, and aesthetic performance are key factors driving the market growth.

Mallard Creek Polymers, TOAGOSEI CO., LTD., NIPPON SHOKUBAI CO., LTD., KAMSONS POLYMER LIMITED, and Celanese Corporation are the prominent players in the market.

Asia Pacific dominated the market in 2024.

The growing shift toward waterborne and low-VOC formulations, increasing infrastructure development, and expanding use in sustainable and high-performance material applications are the major factors that are expected to favor product adoption.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us