Active Phased Array Radar Market Size, Share and Industry Analysis, By Component (T/R Modules, Antennas, Power Supplies, Processors, Control Systems, and Others), By Frequency Band (VHF/UHF Bands, L-band, S-band, C-band, and others), By Technology, By Array Architecture, By Installation Type (Fixed, Portable, and Mobile), By Waveform Type (Pulse-Doppler, Continuous Wave (CW), and others), By Cooling Mechanism, By Application (Surveillance, Targeting/Tracking, Navigation, and Others), By Platform (Airborne, Naval, Ground-Based, and Space-Based), By End User, and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

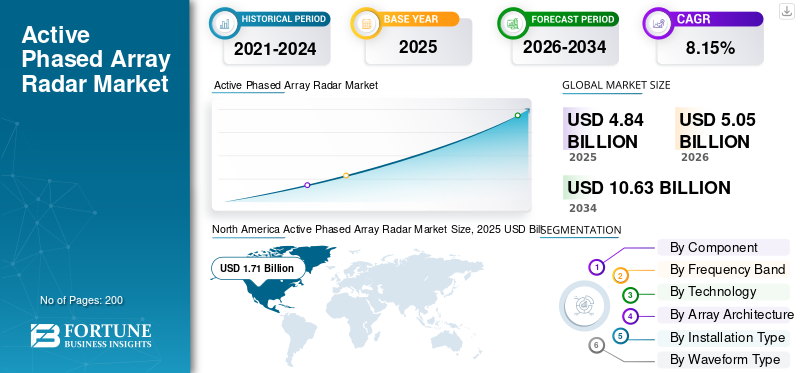

The global active phased array radar market size was valued at USD 4.84 billion in 2025. The market is projected to grow from USD 5.05 billion in 2026 to USD 10.63 billion by 2034, exhibiting a CAGR of 9.76% during the forecast period. North America dominated the global active phased array radar market with a share of 35.33% in 2025.

Active Phased Array Radar (APAR) symbolizes a modern version of the radar system architecture, which uses a large number of Transmit/Receive Modules (TRMs) to enable electronic beam steering. This modern architecture enables the radar to perform a variety of tasks, such as detection, tracking, scanning, and guiding the missiles.

The market growth is primarily driven by global defense modernization programs, particularly across North America, Asia Pacific, and the developing countries. Global military spending focused on future designs for aerial threat detection architectures against hypersonic and unmanned systems acts as the key strategy to drive the global active phased array radar market.

The active phased array radar market is highly competitive and technologically concentrated, dominated by leading firms such as Raytheon Technologies, Northrop Grumman, Lockheed Martin, BAE Systems, Thales Group, Leonardo S.p.A., Saab AB, and other prominent international competitors such as Israel Aerospace Industries, China Electronics Technology Group Corporation (CETC), Mitsubishi Electric, Hensoldt, and Elbit Systems.

Download Free sample to learn more about this report.

Market Dynamics

Market Driving

Military Modernization Initiatives and Defense Acquisition Acceleration Drives Market Growth

Modern-day worldwide defense policies increasingly focus on acquiring an Advanced Phased Array Radar system, which is now considered a vital infrastructure component that can enhance surveillance, detection, and threat protection tools. As a result of the Government of the United States of America's Executive Order called Modernizing Defense Acquisitions, which came out in April of 2025, there is now a direct demand increase in acquiring next-generation radar technologies, which includes APAR systems.

As tensions continue to rise in the worldwide geopolitical arena between major strategic power nations, there is a continuing demand for a sophisticated detection system that can effectively protect against hypersonic missiles, unmanned aerial vehicles, or new-generation electronic warfare.

Market Restrain

Thermal Management and System Integration Problems Can Hamper Market Growth

Active Phased Array Radar systems generate very high power densities and thermal hotspots that are focused on the densely packed arrays of the antennae, especially around the power-consuming modules and supporting circuitry. For ground-based systems, the presence of electromagnetic interference hardening and RF-sealing further compounds the thermal management issues by hindering airflow and the fundamental limitations of passive thermal solutions for overall management and mitigation purposes.

The system integration complexities increase exponentially as APAR technology is incorporated into broader defense architectures. Effective deployment requires seamless hardware-software compatibility, and common interface standardization and migration for significant collaboration between defense contractors and system integrators.

Market Opportunity

Civilian Weather Monitoring and Advanced Transportation Systems Integration to Offer New Market Opportunities

The commercial weather prediction industry offers a significant growth prospect, especially with the inclusion of APAR technology into the country's surveillance systems that are seeking replacements for aging NEXRAD systems. The phased array weather radar technology supports flexible beam-steering operations, thus enabling forecasters to undertake targeted information gathering on a rapidly evolving severe weather event, such as a tornado or a rotating thunderstorm, without necessarily undertaking an entire scan of the atmosphere, and hence improving warning lead times for disaster preparedness.

In parallel, civil aviation authorities are increasingly acknowledging the value of APAR integration for more advanced air traffic control systems, boasting higher resolution and the ability to process more than one target at a time, enabling more accurate weather monitoring in terminal and en-route airspace.

Active Phased Array Radar Market Trend

Software-Defined Radar Architecture and Cognitive Radar Development Catalyze the Market Trends

Software-defined radar designs represent a revolutionary shift away from traditional hardware-focused designs, providing flexibility for multi-mission operations, swift algorithm tuning, real-time threat response, and adaptive operational parameter design tailored for future threats. Cognitive radar solutions integrating perception-action cycle implementations dynamically alter operational and processing parameters over long-term time scales, learning from environmental characteristics and threat appearances in adaptive resource management and effectiveness.

An example of this advancement is Northrop Grumman's digital AESA technology, referred to as the Electronically Modulated Microwave Intelligent Radar Integration System, which completed its first flight in August 2024. The demonstration validated the concurrent execution of radar, electronic warfare, and communication missions, highlighting the operational advantages of digitally enabled AESA architectures. This capability is supported by modern semiconductor processing in California and Maryland-based production operations.

Market Challenges

Shortage of Specialized Skills to Hinder Market Growth

The development of the APAR systems is constrained by a persistent shortage of specialized skills across the signal processing, mathematics, radio frequency engineering, physics of antenna arrays, software-defined system architecture, and development of machine learning algorithms, which remain stringently limited in the global defense industrial base, specifically for emerging economies trying to develop domestic APAR capabilities. Talent retention further compounds these issues. Highly skilled APAR engineers are increasingly migrating to the commercial wireless communication industry, offering improved compensation benefits and location flexibility over classified defense programs.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

T/R Module Segment Dominated Due to Higher Demand Catalyze the Market Growth

The global market by component is classified into T/R Modules, antennas, power supplies, processors, control systems, and others.

Transmit-Receive (T/R) modules accounted for the largest market share, capturing around 40.25% of the total market. This dominance stems from their role as the fundamental building blocks of phased array antenna architectures. These modules perform critical functions such as signal transmission amplification, reception amplification, signal amplitude and phase control functions, making them indispensable to radar performance.

Processors represent the fastest-growing segment, registering the highest CAGR of 11.59% over the study period. Growth is driven by the growing need for integrating AI & ML algorithms, software-defined radar capability enhancement, and enhanced computing requirements due to real-time beamforming and adaptive signal processing in radar systems.

By Frequency Band

Growing Requirement for Synthetic Aperture Radar Applications to Boost Market Growth

The global market by frequency band is classified into VHF/UHF Bands, L-band, S-band, C-band, X-band, and K/Ka/Ku-band.

The VHF/UHF frequency band segment is estimated to be the fastest-growing during the forecast period, showing a compound annual growth rate of 11.19% from 2026 to 2034. This growth is driven by the growing need for synthetic aperture radar applications and the increasing need for early detection of stealth aircraft widely in international early-warning networks that support integrated global air defense architectures.

The X-band segment holds the dominant market share, accounting for around 32.43% of the total market. It is mainly driven by increased military expenditure globally, complexities of warfare requiring surveillance and detection of higher accuracy, and network lock-in effects associated with defense radar systems deployed by military forces across different countries.

By Technology

GaN Technology to Display Fastest Growth due to its Ability to Create Revolutionary Power Density Advancements

The global market by technology is classified into gallium nitride (GaN), gallium arsenide (GaAs), and silicon-based modules.

Gallium nitride (GaN) is estimated to be the fastest-growing segment in the market, witnessing the highest compound annual growth rate of 10.98%. The rapid expansion of the market signifies the basic technological paradigm shift away from the traditional Gallium Arsenide technology, shift away from better GaN technology integration to create revolutionary power density advancements.

Gallium Arsenide GaAs lead the market, accounting for an estimated 43.13% of market share. This leadership is attributable to its strong installed base of military facilities currently in service.

By Array Architecture

Superior Operational Performance to Catalyze Active Electronically Scanned Array (AESA) Segment Growth

The global market by array architecture is classified into Active Electronically Scanned Array (AESA) and Passive Electronically Scanned Array (PESA).

Active electronically scanned array (AESA) is estimated to be the fastest-growing segment, showing the highest CAGR of 9.98% during the forecast period, while also accounting for the largest market share of 87.45% globally. The growth is driven by superior operational performance, such as the elimination of single-point failure dependencies through distributed transmit-receive module architectures, actuate progression of the phase change process, and accelerated defense modernization efforts centered on multi-function radar capability integration on military platforms.

Passive Electronically Scanned Array (PESA) technology continues to witness significant market share, driven by its lower manufacturing cost, coupled with proven operational reliability created over decades of continuous service in cost-sensitive military applications, where acquisition affordability prioritizes performance optimization.

By Installation Type

Growing Demand for Advanced Surveillance Systems to Drive Portable Segment Growth

The global market by installation type is classified into fixed, portable, and mobile.

The portable segment is estimated to be the fastest-growing, showing the highest CAGR of 11.95% during the forecast period from 2026-2034. Growth reflects the escalation of defense demand for lightweight, advanced surveillance systems that support contemporary distributed warfare requirements.

The fixed segment continues to maintain market dominance, accounting for 43.62% of the total market share. Its leadership is mainly influenced by sustained requirements for early warning strategies, coastal surveillance, weather monitoring, and permanent defense infrastructures that establish baseline surveillance architecture within integrated air defense networks and early warning systems.

By Waveform Type

Frequency-Modulated Continuous Wave (FMCW) Segment to Dominate owing to Rising Deployments

The global market by waveform type is classified into Pulse-Doppler, Frequency-Modulated Continuous Wave (FMCW), and Continuous Wave (CW)

The Frequency-Modulated Continuous Wave (FMCW) segment is estimated to be the fastest-growing with the highest CAGR of 11.50% during the forecast period from 2026-2034. Accelerating autonomous vehicle development and mandated deployment of ADAS across global automotive fleets drive the segment’s growth.

Pulse-Doppler commands the dominant position in the market, with a market share of 84.19%. This leading position is indicative of continued demand from established military radar systems, weather forecasting networks, and commercial aviation infrastructure.

By Cooling Mechanism

Air-cooled Segment to Witness Fastest Growth due to Ease of Transportation

The global market by cooling mechanism is classified into air-cooled and liquid-cooled

Air-cooled is expected to showcase the fastest-growth with the highest CAGR of 10.60% during the forecast period from 2026 to 2034. This is due to the increasing need for lightweight aircraft, ease of transportation, and supportive requirements from expeditionary forces in terms of developing their ability to be deployable in mobile warfare operations.

The liquid-cooled segment leads with a strong dominating market share position, with the highest share of 62.61% in the market for the year 2025. Highly advanced liquid-cooled technology applied to defense, data centers, semiconductor, and emerging auto markets, mitigating market risks associated with dependence on a single market application.

By Application

Surveillance Segment Dominated the Market due to Rising Emphasis on Protection of Critical Infrastructure

The global market by application is classified into surveillance, targeting/tracking, navigation, fire control, weather monitoring, air traffic control, and others.

Fire control is projected to be the fastest-growing, registering the highest CAGR of 10.86% during the forecast period. It is driven by the accelerated pace of modernization programs related to fighter aircraft, fleet expansion, and the development of emerging sixth-generation fighter aircraft fitted with advanced AESA fire control radar systems that provide superior air-to-air combat effectiveness with simultaneous engagement capacity for multiple targets.

The surveillance segment accounted for the largest share with 34.60% share in 2025. Increasing border security needs, emphasis on protection of critical infrastructure, and manifestations of geopolitical tension across major regions drive the segment growth.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Critical Role In Establishing Strategic Defense Infrastructure Boosted Segment Growth

The global market by platform is classified into airborne, naval, ground-based, and space-based.

The space-based segment is estimated to be the fastest-growing segment, displaying the highest CAGR of 11.17% during the forecast period from 2026 to 2034. This is mainly due to the rising investment in local satellite constellation technology and remote sensing technology.

The ground-based segment accounted for the largest market share at 35.03%, due to its critical role in establishing strategic defense infrastructure in the provision of continuous surveillance over the territories, territorial waters, and airspace for availability on a 24/7/365 basis for national security reasons.

By End User

Defense Segment to Lead due to Rising Modernization Efforts

The global market by end user is classified into defense, civil government, and commercial.

Defense is estimated to be the fastest-growing industry with the highest CAGR of 9.98% and dominates the market with 86.70% share. This is attributed to the extraordinary level of defense modernization efforts and military procurement acceleration being witnessed by defense institutions around the globe. The record shows an increase in geopolitical tensions, security threats, and strategic competition, representing an increase in defense budgets toward advanced radar system purchases.

Civilian government is estimated to be the second-fastest-growing segment in this market. This encompasses weather forecasting infrastructure, air traffic control systems, and disaster preparation networks, making a huge institutional investment commitment toward infrastructure renewal in the civilian domain.

Active Phased Array Radar Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America Active Phased Array Radar Market Size, 2025 USD Billion To get more information on the regional analysis of this market, Download Free sample

The active phased array radar market growth in Asia Pacific is estimated to be the fastest-growing region, registering a CAGR of 11.60% during the forecast period. Market expansion is driven by strong geopolitical tensions, ambitious indigenous development initiatives on defense technologies, and sustained investments in military modernization across major economies. The key growth catalyst has emerged to be India.

- For instance, in March 2025, India’s Ministry of Defence is in the process of executing major capital procurement contracts, Ashwini AESA radar from Bharat Electronics Limited, which represents an indigenous low-level transportable radar deployment by advanced gallium nitride solid-state technology that enables detection and tracking across diverse aerial threats.

North America continues to hold the dominant market share in the active phased array radar market, due to unparalleled investment by the U.S. Department of Defense in state-of-the-art radar systems for strategic military modernization initiatives across navies, air forces, and missile defense.

- In June 2025, Raytheon Technologies was awarded a USD 536 million firm-fixed-price contract by the U.S. Navy for continued SPY-6 family radar support, including training, engineering services, ship installation, integration, testing, and software capability enhancements, with SPY-6 deployments planned across more than 60 naval vessels, further cementing the region’s leadership in high-end APAR adoption.

The U.S. Navy awarded Raytheon an additional firm-fixed-price five-year contract of USD 602.9 million for comprehensive maintenance and spare parts support for F/A-18 AESA radar systems, ensuring fleet operational availability through 2030. In addition, in April 2025, the U.S. Air Force approved Raytheon LTAMD radar for low-rate initial production, featuring a 360-degree coverage architecture and detection/tracking capabilities to double performance metrics relative to legacy Patriot radar systems.

Europe continues to speed up the APAR market with collaborative multinational defense technology development initiatives focused on meeting the hypersonic threat and layered early warning capabilities that will be required across integrated space-based and ground-based radar systems. The call for the European Commission's European Defence Fund 2025 achieved a record 410 project proposals, with a strong focus on developing next-generation military radars, sensors, and space-based intelligence reconnaissance constellations through collaborative research addressing European sovereign defense capability objectives and NATO interoperability standards.

Middle Eastern regional powers are accelerating defense spending, targeting air defense modernization and advanced radar system procurement in response to asymmetric aerial threats, missile proliferation, and complex security environments.

The Latin American region shows a moderate but strategically significant APAR market growth, driven by naval modernization programs and the integration of advanced frigate platforms with phased array radar systems.

Competitive Analysis

Key Market Players

Strengthen Government Spending and Growing Substantial Research and Development Infrastructure by Major Key Players Accelerate the Market Growth

The active phased array radar market is a highly consolidated and capital-intensive market, dominated by major multinational defense contractors who have established relationships with governments, substantial research and development infrastructure, and proven technological capabilities across military platforms. Raytheon Technologies, Northrop Grumman, Lockheed Martin, BAE Systems, Thales Group, Leonardo, Hensoldt, and so on collectively command global market value through diversified product portfolios, established supply chains, and sustained defense procurement contracts with Allied governments.

The APAR market continues to be concentrated, with high levels of competition among established North American and European defense contractors, while emerging Asian competitors have been progressively capturing market segments by cost optimization, developing indigenous capability, and forming strategic technology partnerships. This has formed multi-polar competitive dynamics, focusing on continuous technological differentiation across a range of areas, including artificial intelligence, gallium nitride semiconductor integration, and software-defined radar architecture evolution.

List of Key Active Phased Array Radar Market Company Profiled

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- BAE Systems plc (U.K.)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- HENSOLDT AG (Germany)

- Israel Aerospace Industries Ltd. (IAI) (Israel)

- ASELSAN A.Ş. (Turkey)

- CEA Technologies Pty Limited (Australia)

- Bharat Electronics Limited (India)

- Mitsubishi Electric Corporation (Japan)

- Hanwha Systems Co., Ltd. (South Korea)

- Indra Sistemas, S.A. (Spain)

- Northrop Grumman Corporation (U.S.)

KEY DEVELOPMENTS

- December 2025:- French aerospace and defense company Thales has given SFO Technologies a contract to produce intricate wired structures for the RBE2 active electronically scanned array (AESA) radar utilized in the Rafael fighter jet, representing progress in the localization of sophisticated defense technologies in line with the Make in India initiative.

- October 2025:- Saab awarded a contract by the NATO Support and Procurement Agency (NSPA) to extend the lifespan of the Arthur radar systems used by the Spanish Army. The contract is valued at around USD 51.23 million.

- October 2025:- The U.S. Army granted Saab a contract for the supply of Giraffe 1X radars to assist security cooperation partners. The total value of the order is around USD 46 million.

- June 2025:- Hensoldt and Indra manufactured the initial Eurofighter Common Radar System Mark 1 (ECRS Mk1) Step 1 radars incorporating new hardware. The debut ECRS Mk1 radars are equipped with cutting-edge subsystems for both the processor and the antenna power supply and control (APSC).

- February 2025:- Saab introduced a coastal surveillance radar during the NAVDEX 2025 exhibition. The Coast Control radar systems operate effectively as an advanced phased-array, non-rotating radar that is software-defined, designed to protect territorial waters and uphold national sovereignty.

REPORT COVERAGE

The global active phased array radar market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the global active phased array radar market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product type launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.15% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Component · T/R Modules · Antennas · Power Supplies · Processors · Control Systems · Others By Frequency Band · VHF/UHF Bands · L-band · S-band · C-band · X-band · K/Ka/Ku-band By Technology · Gallium Nitride (GaN) · Gallium Arsenide (GaAs) · Silicon-based Modules By Array Architecture · Active Electronically Scanned Array (AESA) · Passive Electronically Scanned Array (PESA) By Installation Type · Fixed · Portable · Mobile By Waveform Type · Pulse-Doppler · Frequency-Modulated Continuous Wave (FMCW) · Continuous Wave (CW) By Cooling Mechanism · Air-Cooled · Liquid-Cooled By Application · Surveillance · Targeting/Tracking · Navigation · Fire Control · Weather Monitoring · Air Traffic Control · Others By Platform · Airborne · Naval · Ground-Based · Space-Based By End User · Defense · Civil Government · Commercial By Geographic

· U.S. (By End User) · Canada (By End User)

· U.K. (By End User) · Germany (By End User) · France (By End User) · Russia (By End User) · Nordic Countries (By End User) · Rest of Europe (By End User)

· China (By End User) · India (By End User) · Japan (By End User) · South Korea (By End User) · Australia (By End User) · Rest of Asia Pacific (By End User)

· Israel (By End User) · United Arab Emirates (By End User) · Saudi Arabia (By End User) · Turkey (By End User) · South Africa (By End User) · Rest of Middle East & Africa (By End User)

· Brazil (By End User) · Argentina (By End User)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.84 billion in 2025 and is projected to reach USD 10.63 billion by 2034.

In 2025, the Europe market value stood at USD 1.71 billion.

The market is expected to exhibit a CAGR of 9.76% during the forecast period (2026-2034).

The Gallium Nitride (GaN) segment is expected to be the fastest-growing segment over the forecast period.

Military modernization initiatives and defense acquisition are key factors driving market growth.

Raytheon Technologies, Northrop Grumman, Lockheed Martin, BAE Systems, Thales Group, Leonardo S.p.A., and Saab AB are top players in the market.

North America dominated the market in 2025.

- 2021-2032

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us