Active, Smart, and Intelligent Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper & Paperboard, Glass, Metal, and Others), By Technology (Active, Smart, and Intelligent), By Packaging Type (Rigid Packaging and Flexible Packaging), By End-use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Electronics & Industrial Goods, Logistics & E-commerce, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

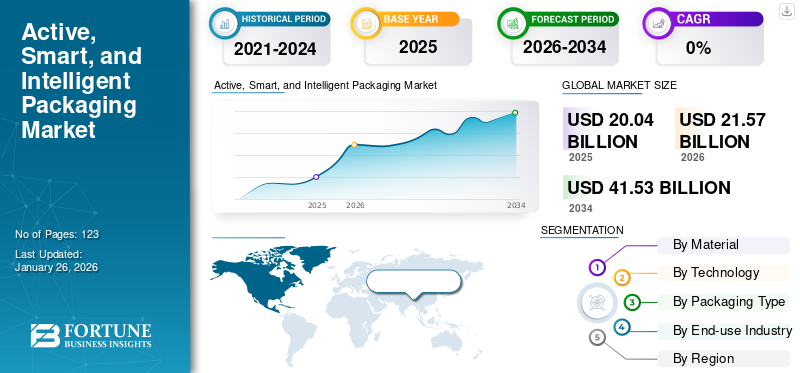

The global active, smart, and intelligent packaging market size was valued at USD 20.04 billion in 2025 and is projected to grow from USD 21.57 billion in 2026 to USD 41.53 billion by 2034, exhibiting a CAGR of 8.53% during the forecast period. Asia Pacific dominated the global market with a share of 38.62% in 2025.

Active, smart, and intelligent packaging refers to high-performance packaging solutions designed to protect and preserve products through the use of materials including plastics, paper, and aluminum foil, often coated with a thin metallic layer. This metallic or multilayer layer construction improves products’ resistance to moisture, oxygen, light, and contaminants, helping to extend shelf life, maintain product integrity, and support premium branding. These technologies are applied across food & beverage, pharmaceuticals, personal care, and industrial goods delivering value through extended shelf life, tamper evidence, and improved consumer engagement.

Major manufacturers such as Amcor plc, Sealed Air Corporation, Tetra Pak International S.A., Avery Dennison Corporation, and Smartrac N.V. have been active in incorporating digital solutions, smart sensor technologies, and sustainable materials to create efficiencies and traceability. Manufacturers are gradually investing in IoT- and smart label-enabled packaging solutions to facilitate real-time data sharing through the supply chain. Increasingly, collaborative partnerships with food, pharmaceutical, and logistics companies to create customized active and smart solutions that extend shelf life, validate product integrity, and reduce waste.

Download Free sample to learn more about this report.

Active, Smart, and Intelligent Packaging Market KEY TAKEAWAYS

- 2025 Market Size: USD 20.04 billion

- 2026 Market Size: USD 21.57 billion

- 2034 Forecast Market Size: USD 41.53 billion

- CAGR: 8.53% from 2026–2034

- Asia Pacific dominated the active, smart, and intelligent packaging market with a 38.62% share in 2025.

- The Plastic segment is projected to hold the largest market share of 49.79% in 2026.

- The Food & Beverages end-user segment is expected to account for the largest market share of 46.13% in 2026.

Asia Pacific

The market was valued at USD 7.74 billion in 2025 and is projected to reach USD 8.46 billion in 2026.

North America

The market reached USD 5.46 billion in 2025 and is projected to grow to USD 5.80 billion in 2026.

Europe

The market was valued at USD 4.44 billion in 2025 and is expected to reach USD 4.78 billion in 2026.

U.S.

The market is expected to grow steadily, driven by rising demand for connected and smart packaging technologies.

Japan

Japan is expected to witness steady growth, driven by technological innovation and strong food safety standards.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Regulatory Pressure & Consumer Demand for Recyclable‒High-Barrier Materials to Propel Market Growth

Governments are increasingly mandating higher levels of recyclability, recycled content, and restrictions on non-recyclable barrier layers, while consumers demand packaging that combines strong protection with environmental responsibility. This regulatory push compels packaging innovators to develop mono-material high-barrier films and paper-based alternatives that still protect against moisture, oxygen, light, etc. Brand owners see this as crucial not only for compliance but also for consumer brand trust and shelf differentiation.

- Amcor’s LifeSpan Performance Paper, a high-barrier recyclable paper-based packaging (with over 80% paper fiber content and PVDC-free), recovers over 80% of its content in the recycling process under European recycling streams.

MARKET RESTRAINTS

Recycling Infrastructure Limitations Restricts the Market Expansion

Despite advancements in active, smart, and intelligent packaging technology, effective recycling remains a significant challenge. The presence of complex materials such as multilayer plastics, integrated sensors, and embedded electronics complicates the recycling process, often leading to contamination and inefficiencies. Furthermore, inadequate waste management policies and insufficient recycling capacities hinder the effective processing of these materials.

- A study by AMERIPEN highlights that, despite increased collection efforts, the U.S. still faces significant gaps in recycling infrastructure, particularly for materials like PET, which may result in falling short of 2025 recycling goals unless collection rates and advanced recycling capabilities increase significantly.

MARKET OPPORTUNITIES

Integration of Smart Packaging with IoT for Enhanced Consumer Engagement

The global shift towards digitalization presents a significant opportunity for the Active, Smart, and Intelligent Packaging market. By integrating Internet of Things (IoT) technologies, packaging can offer real-time tracking, authentication, and consumer interaction through features like NFC tags and QR codes. These smart solutions not only enhance user experience but also provide valuable data analytics for brands, enabling personalized marketing and improved supply chain management. As consumer demand for transparency and interactivity grows, the adoption of IoT-enabled packaging solutions is poised to revolutionize the industry.

- Amcor's AmFiber™ Performance Paper, a recyclable paper-based packaging solution, has demonstrated over 80% recyclability in various global markets, including Brazil, where the current paper recycling rate stands at 66.9%.

ACTIVE, SMART, AND INTELLIGENT PACKAGING MARKET TRENDS

Regulatory Pressures and Consumer Demand Propel Sustainable Packaging Innovations

The global active, smart, and intelligent packaging market growth is increasingly influenced by stringent regulatory requirements and shifting consumer preferences toward sustainability. Governments worldwide are implementing stricter regulations on packaging materials, emphasizing recyclability and the reduction of single-use plastics. Simultaneously, consumers are demanding more environmentally friendly packaging options, prompting brands to innovate and adopt sustainable materials. This convergence of regulatory pressures and consumer demand is driving the development and adoption of recyclable and sustainable packaging solutions across various industries, including food and beverage, pharmaceuticals, and personal care.

- The European Union Regulation on Packaging & Packaging Waste (PPWR), effective February 2025, will compel healthcare brands to move towards recyclable packaging by 2030. This rule is accelerating the shift away from traditional PVC and aluminum foil to new and more recyclable materials based on mono-polypropylene (PP) and polyethylene (PE), which offer improved recyclability and reduced carbon footprint.

MARKET CHALLENGES

Complex Recycling Processes for Smart Packaging Materials to Hamper Market Growth

The integration of advanced technologies into packaging has introduced complexities in recycling processes. Smart packaging often incorporates materials such as multi-layer plastics, embedded sensors, and RFID tags, which are challenging to separate during recycling. This complexity can lead to contamination in recycling streams, reducing the quality and quantity of recycled materials. Additionally, lack of specialized infrastructure to handle these advanced materials further exacerbates the recycling issue.

- The UK's Smart Sustainable Packaging (SSPP) Challenge has revealed that its work has boosted U.K. plastics recycling infrastructure and enabled potential carbon dioxide equivalent savings of more than 1.5 million tonnes between 2025 and 2030 as it has funded projects have come online and reached commercial scale operation.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Plastic Material in Active, Smart, and Intelligent Packaging Boosted Segmental Dominance

On the basis of material, the market is segmented into plastic, paper & paperboard, glass, metal, and others.

Plastic segment is projected to dominate the market with a share of 49.79% in 2026, continues to be the dominant material in the active, smart, and intelligent packaging market share due to its versatility, cost-effectiveness, and adaptability to advanced functionalities. Materials such as polyethylene terephthalate (PET), polypropylene (PP), and polyethylene (PE) are widely used for integrating sensors, RFID tags, and other smart features. The flexibility of plastic allows for the creation of lightweight, durable, and protective packaging solutions that meet the demands in various industries, including food and beverage, pharmaceuticals, and consumer electronics. Companies like Klöckner Pentaplast and Sonoco Products Company have expanded their sustainable PET and PVC blister solutions tailored for healthcare and electronics packaging.

By Technology

Active Packaging Technology Is Projected To Dominate as it Enhances the Product Quality

On the basis of technology, the market is segmented into active, smart, and intelligent.

The active segment holds a substantial market share in 2025. In 2026, the segment is anticipated to dominate with over 40.70% share. Active packaging segment technology remains the dominant segment in the global market. This approach involves incorporating substances into packaging materials that actively interact with the product or its environment, such as oxygen scavengers and moisture regulators. These functionalities enhance product shelf life and maintain quality, making active packaging particularly prevalent in the food and beverage, pharmaceutical, and healthcare industries. The widespread adoption is driven by the increasing demand for extended product freshness and safety, as well as advancements in material science that enable more efficient and cost-effective solutions.

Smart segment is expected to grow at a CAGR of 7.23% over the forecast period.

By Packaging Type

Flexible Packaging Dominates The Market, Integrating Smart Technologies

Based on packaging type, the market is segmented into rigid and flexible.

Flexible packaging leads the global market share with 56.42% in 2026, driven by its adaptability, cost-effectiveness, and alignment with consumer preferences for convenience and sustainability. Materials such as films, pouches, and wraps are increasingly integrated with smart technologies like sensors and RFID tags, enhancing product traceability, freshness monitoring, and consumer engagement. This trend is particularly prominent in food and beverage, pharmaceuticals, and personal care end-user industries, where packaging plays a crucial role in preserving product integrity and providing real-time information to consumers.

By End-Use Industry

Food & Beverages Sector Leads The Market Due To Requirement For Shelf Life, Safety, Convenience, and Sustainability

Based on end-use industry, the market is segmented into food & beverages, pharmaceuticals & healthcare, personal care & cosmetics, electronics & industrial goods, logistics & e-commerce, and others.

The food & beverages end-user industry leads the global market 46.13% share in 2026, driven by the need for packaging solutions that enhance product shelf life, ensure safety, and meet consumer demand for convenience and sustainability. Smart packaging technologies, such as freshness indicators, temperature sensors, and tamper-evident features, are increasingly integrated into packaging materials to monitor and maintain product quality throughout the supply chain. This trend is particularly evident in perishable goods like dairy products, ready-to-eat meals, and beverages, where maintaining freshness is critical.

In addition, the pharmaceuticals & healthcare end-use industry is witnessing steady growth and projected to grow at a CAGR of 8.69% during the study period, driven by the critical need for packaging solutions that ensure drug safety, efficacy, and compliance with stringent regulatory standards.

Active, Smart, and Intelligent Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

The Asia Pacific market generated USD 7.74 billion in 2025, representing 38.62% of the global market landscape, and is expected to reach USD 8.46 billion in 2026. Asia Pacific dominates the global market owing to rapid urbanization, expanding food processing industries, and rising adoption of smart packaging technologies in China, Japan, and India. Government initiatives promoting food safety and quality have accelerated the use of intelligent packaging with freshness sensors and oxygen absorbers. In 2026, the Chinese market is estimated to reach USD 3.56 billion.

- For instance, India’s food processing industry accounts for 32% of the country’s total food market and 12.8% of manufacturing GDP, according to the Ministry of Food Processing Industries (MoFPI, 2024) — highlighting the region’s demand for smart packaging in food preservation and export logistics.

Other regions such as Europe and North America are anticipated to witness notable growth in the coming years.

Asia Pacific Active, Smart, and Intelligent Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

During the forecast period, North America recorded a market size of USD 5.46 billion in 2025, capturing 27.26% of the global market share, and is projected to reach USD 5.8 billion in 2026. The U.S. and Canada have witnessed growing adoption of such packaging in food, beverage, and pharmaceutical end-user industries. Consumer awareness regarding freshness indicators, temperature tracking, and anti-counterfeiting technologies continues to boost the market, while major packaging companies collaborate with tech providers to create connected packaging ecosystems.

Europe

After North America, in 2025, Europe represented USD 4.44 billion, accounting for 22.18% of the worldwide market, and is projected to grow to USD 4.78 billion in 2026. and secure the position of the third-largest region in the market. In the region, Germany and the UK are both estimated to reach USD 1.05 billion and USD 0.76 billion, respectively, in 2026. Europe represents a mature market where stringent EU regulations on food safety and waste reduction have propelled active and intelligent packaging adoption.

Latin America and the Middle East & Africa

Over the forecast period, Latin America and the Middle East & Africa regions are set to witness a moderate growth in this market. In 2025, Latin America held 7.07% of the global market, reaching a valuation of USD 1.42 billion, and is projected to grow to USD 1.49 billion in 2026. Latin America is witnessing steady growth driven by rising food exports and increasing investments in food packaging preservation technologies. In the Middle East & Africa, South Africa is set to attain the value of USD 0.30 billion in 2025. Middle East & Africa accounted for USD 0.97 billion in 2025, representing 4.86% of the global market share, and is projected to reach USD 1.03 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

A wide range of Product Offerings, coupled with a strong distribution network of key companies, supported their Leading Positions

The global market shows a semi-concentrated structure with numerous small- to mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Amcor plc, Sealed Air Corporation, and Tetra Pak International are some of the dominating players in the global market. A broad portfolio of carded and clamshell blister solutions, global reach through strong manufacturing footprints, and continuous investment in recyclable and eco-friendly packaging designs are key characteristics that reinforce their market leadership.

Apart from this, other prominent players in the market include Constantia Flexibles, Klöckner Pentaplast, UFlex Ltd., Tekni-Plex, Inc., Sealed Air Corporation, and Huhtamäki Oyj. These companies are actively pursuing strategic initiatives such as acquisitions, expansion of blister film production capacity, and development of innovative barrier coatings to strengthen their market position and meet rising demand from pharmaceuticals, healthcare, and consumer goods end-user industries.

LIST OF KEY ACTIVE, SMART, AND INTELLIGENT PACKAGING COMPANIES PROFILED:

- Amcor plc (Switzerland)

- Sealed Air Corporation (U.S.)

- Tetra Pak International (Switzerland)

- Avery Dennison Corporation (U.S.)

- BASF SE (Germany)

- 3M Company (U.S.)

- Ball Corporation (U.S.)

- Berry Global Inc. (U.S.)

- Huhtamaki Oyj (Finland)

- Smurfit Kappa Group (Ireland)

- Crown Holdings, Inc. (U.S.)

- Mondi Group (Austria)

- Stora Enso Oyj (Finland)

- Zebra Technologies Corporation (U.S.)

- Multisorb Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Kezzler expanded its offerings in smart packaging & QR code consumer engagement helping in strengthen traceability, transparency, and consumer engagement features.

- April 2025: Packsize added high-throughput, fit-to-size automated packaging technology. Enhances its capability in smart/automated packaging with sustainable and efficient solutions.

- October 2024: Avery Dennison has announced the launch of AD Dura 2.0, a reinforced reusable label solution offering resistance to water, heat, vibration and shock.Designed for harsh environments, the durable and robust AD Dura 2.0 can be used in conjunction with a host of Avery Dennison RFID UHF and HF/NFC inlay designs for dry and wet label formats including the AD Circus™ NTAG213 and AD Dogbone® M730. The solution supports longer product life cycles and waste reduction.

- April 2024: Avery Dennison, a global leader in materials science and digital identification solutions, is partnering with Controlant, a leader in digital transformation of pharma supply chains, to drive real-time, end-to-end visibility and support sustainability initiatives in the pharma industry.

- October 2023: Multi-Color Corporation (MCC), one of the largest label companies in the world, announced the acquisition of Starport Technologies, a provider of smart label solutions based in Kansas City, Missouri. Financial terms of the transaction were not disclosed.

REPORT COVERAGE

The global active, smart, and intelligent packaging market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2025-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.53% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, By Packaging Type, By Technology and By End-use Industry, and Region |

|

By Material |

· Plastic · Paper & Paperboard · Glass · Metal · Others |

|

By Technology |

· Active · Smart · Intelligent |

|

By Packaging Type |

· Rigid Packaging o Bottles & Jars o Trays o Cans & Containers o Others · Flexible Packaging o Pouches & Sachets o Films & Wraps o Bags o Others |

|

By End-use Industry |

· Food & Beverages · Pharmaceuticals & Healthcare · Personal Care & Cosmetics · Electronics & Industrial Goods · Logistics & E-commerce · Others |

|

By Region |

· North America (By Material, Technology, Packaging Type, End-use Industry and Country) o U.S. (By End-user Industry) o Canada (By End-user Industry) · Europe (By Material, Technology, Packaging Type, End-use Industry , and Country) o Germany (By End-user Industry) o France (By End-user Industry) o U.K. (By End-user Industry) o Italy (By End-user Industry) o Spain (By End-user Industry) o Russia (By End-user Industry) o Poland (By End-user Industry) o Romania (By End-user Industry) o Rest of Europe (By End-user Industry) · Asia Pacific (By Material, Technology, Packaging Type, End-use Industry, and Country) o China (By End-user Industry) o Japan (By End-user Industry) o India (By End-user Industry) o Australia (By End-user Industry) o Southeast Asia (By End-user Industry) o Rest of Asia Pacific (By End-user Industry) · Latin America (By Material, Technology, Packaging Type, End-use Industry and Country) o Brazil (By End-user Industry) o Mexico (By End-user Industry) o Rest of Latin America (By End-user Industry) · Middle East & Africa (By Material, Technology, Packaging Type, End-use Industry and Country) o Saudi Arabia (By End-user Industry) o UAE (By End-user Industry) o Oman (By End-user Industry) o South Africa (By End-user Industry) o Rest of the Middle East & Africa (By End-user Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 20.04 billion in 2025 and is projected to reach USD 41.53 billion by 2034.

In 2025, the market value in the Asia Pacific stood at USD 7.74 billion.

The market is expected to exhibit a CAGR of 8.53% during the forecast period.

The plastic segment led the market by material.

The key factors driving rising regulatory pressure & consumer demand for recyclable‒high-barrier materials.

Amcor plc, WestRock Company, and Sonoco Products, Constantia Flexibles, are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Integration of smart packaging with IoT for enhanced consumer engagement.

- 2021-2034

- 2025

- 2021-2024

- 123

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us