ADAS Simulation Market Size, Share & Industry Analysis, By Simulation Type (Software-in-the-Loop (SiL), Hardware-in-the-Loop (HiL), Model-in-the-Loop (MiL), and Driver-in-the-Loop (DiL)), By Component (Software, Hardware, and Services), By Application (Autonomous Driving Testing, ADAS Function Validation, Sensor Fusion Testing, and Scenario & Environment Simulation), By Vehicle Type (Passenger Cars and Commercial Vehicles), By End User (Automotive OEMs, Tier 1 Suppliers, Technology Providers, and Research & Testing Institutions), and Regional Forecast, 2026–2034

(Offer valid till 15th Aug 2026)

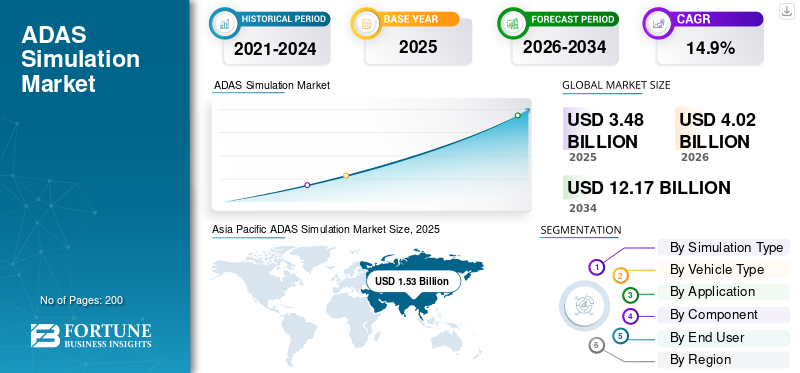

ADAS Simulation Market Size and Future Outlook

The global ADAS simulation market size was valued at USD 3.48 billion in 2025. The market is projected to grow from USD 4.02 billion in 2026 to USD 12.17 billion by 2034, exhibiting a CAGR of 14.9% during the forecast period. Asia Pacific dominated the adas simulation market with a market share of 43.97% in 2025.

ADAS simulation refers to the virtual testing and validation of advanced driver assistance systems using software models and simulated environments to assess performance, safety, and functionality under diverse driving scenarios. Market growth is driven by rising demand for vehicle safety, increasing adoption of autonomous technologies, stringent government regulations, and advancements in simulation software, and growing investments by automotive OEMs and technology providers in testing solutions.

Major players in the market include dSPACE, IPG Automotive, Siemens Digital Industries Software, ANSYS, Cognata, and VI-grade, competing through advanced simulation platforms, AI-driven scenario generation, real-time testing, and integrated validation solutions.

Download Free sample to learn more about this report.

ADAS Simulation Market Key Takeaways

- 2025 Market Size: USD 3.48 billion

- 2026 Market Size: USD 4.02 billion

- 2034 Forecast Market Size: USD 12.17 billion

- CAGR: 14.9% from 2026–2034

- Asia Pacific dominated the ADAS simulation market with a 43.97% share in 2025.

- The hardware-in-the-loop (HiL) segment is projected to grow at a 15.3% CAGR during the forecast period.

- The commercial vehicles segment is projected to grow at a 14.0% CAGR during the forecast period.

Asia Pacific

Asia Pacific led the market with USD 1.53 billion in 2025 and is projected to register the fastest growth during the forecast period.

Europe

Europe held the second-largest market share and is projected to grow at a 13.0% CAGR during the forecast period.

North America

North America ranked third globally, supported by strong R&D investments and increasing adoption of autonomous driving technologies.

U.S.

The ADAS simulation market is estimated at USD 0.77 billion in 2026, accounting for approximately 19.1% of global revenue.

Japan

The ADAS simulation market is estimated at USD 0.30 billion in 2026, representing approximately 7.6% of global revenue.

Read More

ADAS SIMULATION MARKET TRENDS

Rising Integration of AI and Digital Twins in Simulation Ecosystems to be a Significant Market Trend

The adoption of artificial intelligence and digital twin technology is emerging as a significant market trend. Companies are increasingly leveraging AI to generate complex driving scenarios and improve predictive accuracy, while digital twins enable real-time replication of vehicle behavior. This enhances ADAS validation efficiency and reduces physical testing costs. The trend supports continuous software updates and accelerates development cycles, aligning with evolving market trends focused on automation, precision, and scalable simulation environments across global automotive ecosystems.

- In March 2026, Synopsys launched an Electronics Digital Twin platform enabling up to 90% software validation before hardware availability, accelerating automotive development cycles, enhancing collaboration, reducing costs, and advancing AI driven simulation capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Regulatory Mandates for Vehicle Safety to Drive Simulation Adoption

Stringent government regulations related to vehicle safety and autonomous driving are a major driver of ADAS simulation market growth. Regulatory bodies across regions are mandating advanced safety features such as lane-keeping assist, collision avoidance, and emergency braking. This compels OEMs to adopt robust advanced driver assistance systems simulation tools for validation and compliance. The growing emphasis on standardized testing protocols is boosting market demand, as simulation enables faster, cost-effective certification processes while ensuring adherence to safety benchmarks during the market forecast period.

- In March 2026, NHTSA initiated a review of federal safety standards to assess their applicability to automated driving systems, aiming to support innovation while maintaining safety, with potential regulatory updates impacting vehicle design and evaluation.

MARKET RESTRAINTS

High Initial Investment and Complexity in Simulation Infrastructure

The adoption of ADAS simulation solutions is restrained by the high initial investment required for advanced software platforms, hardware integration, and a skilled workforce. Developing and maintaining high-fidelity simulation environments involves complex system architectures and continuous updates. Smaller players and emerging markets may face challenges in adopting such capital-intensive solutions. This cost barrier impacts market share distribution, limiting widespread penetration and slowing adoption rates, particularly among mid-sized automotive firms with constrained budgets and technical capabilities.

MARKET OPPORTUNITIES

Growing Shift toward Autonomous Mobility Creating New Testing Opportunities

The rapid evolution of autonomous vehicles presents significant opportunities for ADAS simulation providers. As vehicles move toward higher levels of autonomy, the need for extensive virtual testing environments increases exponentially. Simulation enables testing of rare and hazardous scenarios that are difficult to replicate physically. This creates strong market demand for scalable and cloud based simulation platforms. Companies can expand their offerings into fully autonomous validation ecosystems, supporting long-term market growth and innovation during the forecast period.

- In March 2026, NVIDIA announced the adoption of its DRIVE Hyperion platform by BYD, Geely, Isuzu, and Nissan to develop Level 4 autonomous vehicles, accelerating validation cycles, enabling scalable deployment, and advancing AI-driven simulation and autonomous mobility ecosystems globally.

MARKET CHALLENGES

Lack of Standardization in Simulation Scenarios and Validation Frameworks

A key challenge in the market is the absence of globally accepted standards for simulation scenarios and validation methodologies. Variations in testing requirements across regions and manufacturers create inconsistencies in results and benchmarking. This complicates the market analysis and slows interoperability between platforms. Companies must invest additional resources to customize solutions for different clients, increasing development time and costs while hindering streamlined adoption across the automotive value chain.

Segmentation Analysis

By Simulation Type

Increasing Need for Scalable and Early-Stage Validation to Drive Software-in-the-Loop (SiL) Segmental Dominance

Based on simulation type, the market is segmented into software-in-the-loop (SiL), hardware-in-the-loop (HiL), model-in-the-loop (MiL), and driver-in-the-loop (DiL).

The software-in-the-loop (SiL) segment dominates the market due to its ability to enable early-stage validation of ADAS algorithms in a cost-effective and scalable virtual environment. Software in the Loop allows developers to test multiple scenarios rapidly without physical hardware dependencies, reducing development timelines. Its flexibility and integration with AI-driven simulation tools further strengthen adoption among OEMs and technology providers.

- In January 2025, Stellantis partnered with dSPACE to integrate cloud-based Software-in-the-Loop simulation into its Virtual Engineering Workbench, enabling up to 85% virtual testing, accelerating software development cycles, and improving vehicle innovation and time-to-market.

The hardware-in-the-loop (HiL) segment is projected to grow at a CAGR of 15.3% over the forecast period. The increasing need for real-time system validation and hardware integration testing is driving HiL adoption, particularly for safety-critical ADAS functionalities and regulatory compliance requirements.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

High Adoption of ADAS Features and Large Production Volumes to Propel Passenger Cars Segmental Demand

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment dominates the market due to high production volumes and rapid integration of ADAS features across mid-range and premium vehicles. Increasing consumer demand for safety, comfort, and semi-autonomous functionalities is accelerating simulation requirements. OEMs extensively utilize simulation tools to validate diverse driving scenarios, ensuring compliance and performance, thereby strengthening the segment’s leading market share and supporting sustained market growth of passenger vehicles.

- In March 2026, Hyundai planned to launch 36 new or updated models in North America by 2030, supported by diverse powertrains and increased localization, strengthening production capabilities, and aligning with evolving mobility and automotive technology trends.

The commercial vehicles segment is projected to grow at a CAGR of 14.0% over the forecast period. Rising adoption of ADAS in logistics and fleet management, driven by safety regulations and operational efficiency needs, is fueling simulation demand in this segment.

By Application

Growing Complexity of Safety-Critical Features to Boost Demand for ADAS Function Validation

Based on application, the market is segmented into autonomous driving testing, ADAS function validation, sensor fusion testing, and scenario & environment simulation.

The ADAS function validation segment dominates the market due to the widespread deployment of safety-critical features such as adaptive cruise control, lane-keeping assist, and emergency braking. OEMs rely heavily on simulation to ensure system reliability, regulatory compliance, and performance across diverse conditions. The continuous evolution of safety standards further increases validation requirements, sustaining strong market demand and reinforcing its leading market share.

- In February 2026, SCANeR 2026.1 was launched with enhanced interoperability, AI integration, and large-scale validation capabilities, enabling improved simulation realism, automated testing, and efficient ADAS and autonomous vehicle validation workflows.

The autonomous driving testing segment is projected to grow at a CAGR of 15.9% over the forecast period. Increasing investments in higher levels of vehicle autonomy and the need to test complex real-world scenarios virtually are significantly accelerating demand for advanced simulation platforms.

By Component

Rising Dependence on Advanced Algorithms and Scalable Platforms to Advance Software Market Growth

Based on component, the market is segmented into software, hardware, and services.

The software segment dominates the market due to its critical role in enabling scenario generation, algorithm testing, and system validation within virtual environments. Increasing reliance on AI-driven simulation, cloud-based platforms, and digital twins is accelerating software adoption among OEMs and technology providers. Continuous updates, scalability, and integration capabilities make software the backbone of ADAS simulation, supporting strong market growth and expanding market demand.

- In February 2026, Keysight introduced a new assembly simulation software enabling early-stage validation of automotive body-in-white processes, improving distortion prediction, reducing physical testing, and accelerating manufacturing efficiency through advanced virtual validation engineering capabilities.

The hardware segment market is projected to grow from USD 1.35 billion in 2026, at a CAGR of 13.6% over the forecast period. The rising need for real-time processing, sensor interfacing, and physical system validation is driving demand for high-performance hardware solutions in simulation setups.

By End User

Strong In-house Development Capabilities to Propel Automotive OEMs' Segment

Based on end user, the market is segmented into automotive OEMs, tier 1 suppliers, technology providers, and research & testing institutions.

The automotive OEMs segment dominates the market due to their extensive involvement in ADAS development, validation, and integration processes. OEMs increasingly invest in advanced simulation tools to accelerate product development, ensure regulatory compliance, and reduce physical testing costs. Their strong financial capabilities and focus on innovation drive large-scale adoption of simulation platforms, reinforcing their leading market share and supporting comprehensive market analysis.

- In December 2025, Siemens launched Pave360 Automotive, a digital twin platform enabling early-stage virtual integration of hardware and software, accelerating software defined vehicles development, improving collaboration, and reducing time-to-market for ADAS and autonomous systems.

The technology providers segment is projected to grow at a CAGR of 16.2% over the forecast period. Rapid advancements in AI, cloud computing, and simulation software are enabling technology firms to expand capabilities, driving increased collaboration with OEMs and boosting demand for specialized simulation solutions.

ADAS Simulation Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific ADAS Simulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is projected to register the fastest-growing CAGR during the market forecast period. Strong automotive production hubs in China, Japan, and India, along with rising adoption of ADAS technologies, are driving market growth. Increasing government focus on vehicle safety regulations and smart mobility initiatives is boosting ADAS simulation market demand. Additionally, expanding investments in autonomous vehicle development and simulation infrastructure by OEMs and technology firms are shaping favorable market trends across the region.

- In January 2026, WeRide launched GENESIS1, an advanced simulation platform leveraging generative AI to create realistic driving scenarios, improving autonomous vehicle training efficiency, validation accuracy, and accelerating safe deployment across global markets.

China ADAS Simulation Market

The China market is estimated at around USD 0.98 billion in 2026, accounting for roughly 24.4% of global revenues. Strong automotive manufacturing base and autonomous technology investments drive growth.

Japan ADAS Simulation Market

The Japan market is estimated at around USD 0.30 billion in 2026, accounting for roughly 7.6% of global revenues. Advanced R&D capabilities and early ADAS adoption support steady market growth.

India ADAS Simulation Market

The India market is estimated at around USD 0.15 billion in 2026, accounting for roughly 3.7% of global revenues. Increasing safety awareness and growing automotive production accelerate market demand significantly.

Europe

Europe holds the second-largest ADAS simulation market share and is expected to grow at a CAGR of 13.0% over the forecast period. The region’s strong regulatory framework for vehicle safety and early adoption of ADAS technologies are key contributors to market growth. The presence of leading automotive OEMs and technology providers supports continuous innovation in simulation solutions. Increasing emphasis on sustainability, connected mobility, and standardized validation processes further strengthens market demand and supports comprehensive market analysis.

- In January 2026, TU Graz and Magna opened an Advanced Driving Simulation Center at Campus Inffeldgasse, Graz, Austria, featuring a high-fidelity simulator to enable realistic ADAS testing, accelerate vehicle development, and advance autonomous driving research.

Germany ADAS Simulation Market

The Germany market is estimated at around USD 0.35 billion in 2026, accounting for roughly 8.7% of global revenues. Strong OEM presence and regulatory focus on vehicle safety boost simulation adoption.

U.K. ADAS Simulation Market

The U.K. market is estimated at around USD 0.06 billion in 2026, accounting for roughly 1.4% of global revenues. Increasing autonomous trials and innovation ecosystems drive gradual market growth.

North America

North America represents the third-largest market, driven by strong technological advancements and early adoption of autonomous driving solutions. The presence of major technology companies and automotive innovators is accelerating simulation adoption. High investments in research and development, along with supportive regulatory initiatives, are contributing to market growth. The region also benefits from advanced digital infrastructure, enabling widespread use of AI-driven simulation tools and reinforcing evolving market trends.

- In March 2026, Flexcompute launched AutoInsight, an AI-driven simulation platform enabling real-time aerodynamic analysis, allowing engineers to evaluate design variations instantly, accelerate development cycles, and maximize the value of existing simulation and test data.

U.S. ADAS Simulation Market

The U.S. market is estimated at around USD 0.77 billion in 2026, accounting for roughly 19.1% of global revenues. Strong technology ecosystem and high autonomous vehicle investments accelerate simulation demand.

Rest of the World

The rest of the world is witnessing steady growth in the market, supported by increasing automotive modernization and the gradual adoption of safety technologies. Emerging economies in Latin America, the Middle East & Africa are investing in smart mobility and infrastructure development. While adoption rates are comparatively slower, rising awareness of vehicle safety and regulatory improvements are expected to drive market demand, contributing to overall market growth during the forecast period.

- In November 2025, Abu Dhabi planned the development of its Smart and Autonomous Mobility Systems Testing Centre, a state-of-the-art facility leveraging digital twin technologies to test and validate autonomous vehicles and advance smart mobility innovation.

COMPETITIVE LANDSCAPE

Key Industry Players

AI-Driven Simulation, Platform Integration, and Strategic Collaborations Define Competitive Intensity

The market is moderately consolidated, with key players such as dSPACE, IPG Automotive, Siemens Digital Industries Software, ANSYS, Cognata, and VI-grade competing through advanced simulation platforms and integrated validation ecosystems. Companies focus on AI-driven scenario generation, cloud-based simulation, and real-time testing capabilities to enhance performance. Strategic collaborations with OEMs and technology firms strengthen market positioning. Continuous software innovation, scalability, and end-to-end validation solutions enable competitive differentiation across evolving autonomous and ADAS development requirements.

- In March 2026, General Motors highlighted its use of generative AI to transform vehicle design, enabling rapid visualization, real-time aerodynamic testing through virtual wind tunnels, and significantly reducing development timelines from concept to production.

LIST OF KEY ADAS SIMULATION COMPANIES PROFILED IN REPORT

- dSPACE GmbH (Germany)

- IPG Automotive GmbH (Germany)

- Siemens Digital Industries Software (U.S.)

- ANSYS, Inc. (U.S.)

- Cognata Ltd. (Israel)

- VI-grade GmbH (Germany)

- MSC Software Corporation (U.S.)

- Hexagon AB (Sweden)

- Dassault Systèmes SE (France)

- NVIDIA Corporation (U.S.)

- MathWorks, Inc. (U.S.)

- AVL List GmbH (Austria)

- Elektrobit (Germany)

- TASS International (Netherlands)

- Foretellix Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- February 2026: dSPACE joined the SDVerse marketplace, enabling broader access to its AI-powered simulation, SIL/HIL validation, and cloud-based testing solutions, helping OEMs and suppliers accelerate the development of software-defined and autonomous vehicles.

- February 2026: VI-Grade installed its first HyperDock simulation system in North America at Multimatic’s facility in Novi, Michigan, enhancing driving simulator realism and enabling integrated development of vehicle dynamics and NVH performance.

- December 2025: dSPACE showcased AI-driven Software-in-the-Loop and Hardware-in-the-Loop solutions at CES 2026, enabling automated validation, cloud-based testing pipelines, and improved efficiency in software-defined vehicle development and ADAS simulation workflows.

- November 2025: IPG Automotive launched CarMaker 15.0, enhancing simulation fidelity, virtual ECU integration, and sensor modeling, enabling earlier and more precise ADAS and autonomous vehicle testing while accelerating development cycles and reducing costs.

- March 2025: dSPACE launched XSG Power Electronics Systems software, enabling high-frequency simulation for power electronics, supporting hardware-in-the-loop testing, improving fault analysis, and accelerating the development of advanced electric vehicle powertrain components.

- January 2025: Hexagon launched Virtual Test Drive X, a cloud-native ADAS simulation platform enabling automated testing across thousands of real-world scenarios, improving software validation efficiency and accelerating development of safe, software-defined vehicles.

- November 2024: IPG Automotive released CarMaker 14.0, enhancing simulation realism with advanced sensor models, weather effects, and traffic scenarios, enabling efficient virtual testing of ADAS and autonomous systems while reducing development time and costs.

REPORT COVERAGE

The global ADAS simulation market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.9% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Simulation Type, By Vehicle Type, By Application, By Component, By End User, and By Region |

| By Simulation Type |

|

| By Vehicle Type |

|

| By Application |

|

| By Component |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.48 billion in 2025 and is projected to reach USD 12.17 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.53 billion.

The market is expected to exhibit a CAGR of 14.9% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type.

Increasing regulatory mandates for vehicle safety to drive simulation adoption

Top players in the market include dSPACE, IPG Automotive, Siemens Digital Industries Software, ANSYS, Cognata, and VI-grade.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us