Additive Manufacturing Equipment Market Size, Share & Industry Analysis, By Equipment (Material Extrusion (FDM/FFF), Powder Bed Fusion (SLS, SLM, DMLS, EBM), Vat Photopolymerization (SLA, DLP), and Others), By End-Use Industry (Aerospace & Defense, Automotive, Healthcare (Medical & Dental), and Others), By Material Type (Polymers, Metals, and Others), and Regional Forecast, 2026 – 2034

Additive Manufacturing Equipment Market Size and Future Outlook

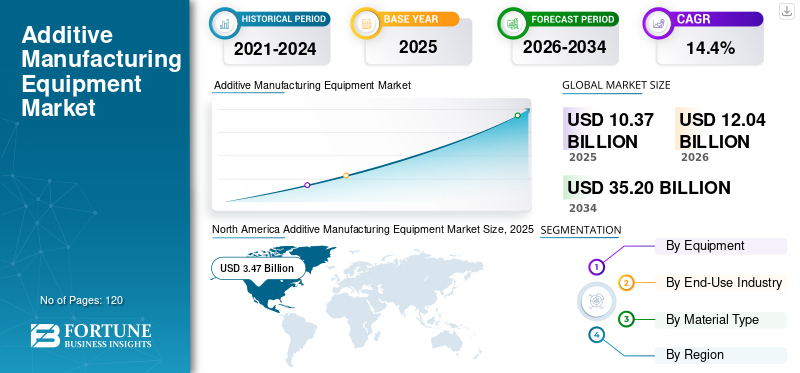

The global additive manufacturing equipment market size was valued at USD 10.37 billion in 2025. The market is projected to grow from USD 12.04 billion in 2026 to USD 35.20 billion by 2034, exhibiting a CAGR of 14.4% during the forecast period. North America dominated the additive manufacturing equipment market with a market share of 33.46% in 2025.

Additive manufacturing equipment refers to industrial systems used to fabricate three-dimensional components layer-by-layer using digital design files and specialized materials such as metals, polymers, and composites. These systems are widely utilized across aerospace, healthcare, automotive, and industrial sectors for rapid prototyping, tooling, and end-use part manufacturing.

The market is witnessing strong growth driven by increasing adoption of industrial 3D printing technologies, rising demand for lightweight and customized components, and advancements in metal additive manufacturing systems. Industries are increasingly integrating additive manufacturing into production workflows to reduce material waste, shorten production cycles, and enable complex geometries that are difficult to achieve using conventional manufacturing methods.

Major players such as Stratasys Ltd., 3D Systems Corporation, EOS GmbH, GE Additive, Nikon SLM Solutions, Desktop Metal Inc., HP Inc., Renishaw plc, TRUMPF Group, and Materialise NV are continuously investing in advanced additive manufacturing technologies and industrial-scale printing systems.

- For instance, in April 2024, Nikon SLM Solutions introduced its large-scale NXG XII 600 metal additive manufacturing platform for aerospace and energy applications, supporting high-productivity industrial printing.

Download Free sample to learn more about this report.

ADDITIVE MANUFACTURING EQUIPMENT MARKET Key Takeaways

- 2025 Market Size: USD 10.37 billion

- 2026 Market Size: USD 12.04 billion

- 2034 Forecast Market Size: USD 35.20 billion

- CAGR: 14.4% from 2026–2034

- North America dominated the additive manufacturing equipment market with a market share of 33.46% in 2025.

- The vat photopolymerization (SLA, DLP) segment is expected to register the highest CAGR of 14.6% during the forecast period.

- The healthcare (medical & dental) segment is expected to register the highest CAGR of 15.7% over the forecast period.

North America

The region led the global market in 2025 with a 33.46% share, supported by advanced manufacturing capabilities, strong aerospace and defense industries, and continued investments in industrial 3D printing and digital manufacturing technologies.

Europe

Europe remains a key market, driven by robust automotive, aerospace, and industrial manufacturing sectors, with ongoing investments in advanced manufacturing technologies and automation initiatives.

Asia Pacific

The region is expected to witness the highest CAGR during the forecast period, supported by rapid industrialization, expanding electronics manufacturing, government-backed digitization initiatives.

U.S.

The U.S. additive manufacturing equipment market is estimated at USD 3.37 billion in 2026, accounting for approximately 28% of global revenue, driven by strong demand from the aerospace, defense, and healthcare sectors.

Japan

Japan's market is estimated at USD 0.64 billion in 2026, representing around 5.3% of global revenue, supported by advanced precision manufacturing and increasing adoption across the automotive and electronics industries.

Read More

ADDITIVE MANUFACTURING EQUIPMENT MARKET TRENDS

Industrialization of Metal Additive Manufacturing for Serial Production Applications to be a Significant Market Trend

A major trend shaping the market is the increasing industrialization of metal additive manufacturing technologies for serial production applications. Aerospace, healthcare, and automotive manufacturers are increasingly adopting metal 3D printing systems to produce lightweight, high-performance components with reduced lead times.

Additionally, integration of AI-driven process monitoring, automation, and digital manufacturing platforms is improving printing precision, repeatability, and scalability across industrial production environments.

- For instance, in 2024, EOS GmbH expanded its automated metal additive manufacturing ecosystem through integration of advanced process monitoring software, enhancing industrial production efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Lightweight and Complex Components Driving Market Growth

The increasing demand for lightweight, high-strength, and geometrically complex components across aerospace, defense, and automotive industries is a key driver of the additive manufacturing equipment market growth. Additive manufacturing enables efficient production of optimized parts while reducing material consumption and assembly complexity.

Furthermore, the growing adoption of digital manufacturing and rapid prototyping technologies is accelerating equipment deployment across industrial sectors.

- For instance, in 2024, GE Additive expanded collaborations with aerospace manufacturers to support large-scale metal additive manufacturing for aircraft engine

MARKET RESTRAINTS

High Equipment Costs and Material Qualification Challenges Limiting Adoption

Industrial additive manufacturing systems, particularly metal printing equipment, involve significant capital investment and operational costs. Small and medium-sized manufacturers may face financial barriers when adopting advanced additive manufacturing technologies.

Additionally, qualification and certification requirements for aerospace, medical, and industrial applications increase implementation complexity and production timelines.

- For instance, in March 2024, Desktop Metal announced restructuring initiatives aimed at reducing operational costs amid challenging industrial equipment market conditions.

MARKET OPPORTUNITIES

Expansion of Medical and Dental 3D Printing Creating New Opportunities

The growing adoption of additive manufacturing in medical and dental applications is creating substantial growth opportunities for equipment providers. Customized implants, prosthetics, and dental devices increasingly rely on high-precision additive manufacturing technologies.

Moreover, advancements in biocompatible materials and patient-specific manufacturing workflows are expected to further accelerate adoption.

- For instance, in 2024, 3D Systems expanded its healthcare additive manufacturing solutions portfolio through new medical device production partnerships, strengthening its position in medical 3D printing applications.

Segmentation Analysis

By Equipment

Powder Bed Fusion (SLS, SLM, DMLS, EBM) Segment Dominates Due to High Precision and Industrial Metal Printing Adoption

By equipment, the market is segmented into material extrusion (FDM/FFF), powder bed fusion (SLS, SLM, DMLS, EBM), vat photopolymerization (SLA, DLP), and others.

The powder bed fusion (SLS, SLM, DMLS, EBM) segment holds the highest additive manufacturing equipment market share, as the equipment enables high-precision manufacturing of complex metal and polymer components for aerospace, medical, and industrial applications. Its ability to deliver superior mechanical properties, dimensional accuracy, and production scalability has significantly accelerated adoption across advanced manufacturing industries.

- For instance, EOS GmbH and Nikon SLM Solutions continue expanding industrial powder bed fusion platforms for aerospace and energy applications, strengthening market demand.

The vat photopolymerization (SLA, DLP) segment is also expected to register the highest CAGR of 14.6% during the forecast period, driven by increasing adoption of industrial metal additive manufacturing and serial production applications.

By Material Type

Metals Segment Dominates Owing to Rising Industrial and Aerospace Applications

Based on material type, the market is segmented into polymers, metals, and others.

The metals segment holds the highest market share, driven by growing adoption of titanium, aluminum, stainless steel, and nickel-based alloys in aerospace, healthcare, and energy applications. Metal additive manufacturing enables production of high-strength, lightweight parts with enhanced design flexibility and reduced material wastage.

- For instance, TRUMPF Group expanded its metal additive manufacturing systems portfolio for industrial-scale applications, strengthening its market presence.

The polymers segment is also expected to register the highest CAGR of 13.3% during the forecast period, supported by increasing demand for industrial metal printing in aerospace and healthcare industries.

To know how our report can help streamline your business, Speak to Analyst

By End-Use Industry

Aerospace & Defense Sector Leads Due to Demand for Lightweight High-Performance Components

In terms of end-use industry, the market is segmented into aerospace & defense, automotive, healthcare (medical & dental), and others.

The aerospace & defense segment holds the highest market share, as additive manufacturing enables production of lightweight and geometrically optimized components that improve fuel efficiency and operational performance. Aerospace manufacturers are increasingly integrating additive manufacturing into engine, structural, and tooling applications to reduce production lead times and material waste.

- For instance, GE Aerospace continues deploying additive manufacturing technologies for aircraft engine component production, supporting large-scale industrial adoption.

The healthcare (medical & dental) segment is expected to register the highest CAGR of 15.7% over the forecast period, driven by rising demand for patient-specific implants, dental restorations, and customized medical devices.

Additive Manufacturing Equipment Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Additive Manufacturing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the highest market share in the global market in 2025, supported by advanced industrial manufacturing capabilities, strong aerospace and defense sectors, and early adoption of industrial 3D printing technologies. The region benefits from significant investments in digital manufacturing and rapid prototyping across aerospace, healthcare, and automotive industries.

Additionally, the presence of major additive manufacturing equipment manufacturers and extensive R&D activities are strengthening technological innovation and industrial adoption across the region.

U.S. Additive Manufacturing Equipment Market

The U.S. market is estimated at around USD 3.37 billion in 2026, representing approximately 28% of global revenues. Strong aerospace, defense, and healthcare industries continue driving large-scale adoption of industrial additive manufacturing systems.

Increasing investments in metal 3D printing and advanced manufacturing technologies are further accelerating market growth.

Europe

Europe represents a significant market for additive manufacturing equipment, supported by strong automotive, aerospace, and industrial manufacturing sectors. Germany and the U.K. are actively investing in advanced manufacturing technologies and industrial automation initiatives.

Furthermore, increasing focus on sustainable manufacturing and localized production capabilities is strengthening adoption of additive manufacturing systems across the region.

U.K. Additive Manufacturing Equipment Market

The U.K. market is estimated at around USD 0.53 billion in 2026, representing approximately 4.4% of global revenues. Increasing adoption of additive manufacturing across aerospace and healthcare sectors is driving market expansion.

Government-supported innovation programs and research initiatives are further supporting industrial deployment.

Germany Additive Manufacturing Equipment Market

Germany’s market is estimated at around USD 0.86 billion in 2026, representing approximately 7.1% of global revenues. The country’s strong industrial and automotive manufacturing base supports high adoption of industrial 3D printing technologies.

Continuous investments in Industry 4.0 and advanced production systems are further strengthening equipment demand.

Asia Pacific

Asia Pacific is expected to register the highest CAGR during the forecast period, driven by rapid industrialization, growing electronics manufacturing, and increasing investments in advanced manufacturing technologies. China, Japan, and India are significantly expanding industrial additive manufacturing capabilities across automotive, aerospace, and healthcare industries.

Additionally, supportive government initiatives promoting domestic manufacturing and industrial digitization are accelerating regional market growth.

Japan Additive Manufacturing Equipment Market

Japan’s market is estimated at around USD 0.64 billion in 2026, representing approximately 5.3% of global revenues. Advanced precision manufacturing capabilities and strong industrial automation expertise support additive manufacturing adoption.

Increasing integration of additive manufacturing in automotive and electronics sectors is further strengthening demand.

China Additive Manufacturing Equipment Market

China’s market is estimated at around USD 1.44 billion in 2026, representing approximately 12.0% of global revenues. Rapid industrial manufacturing expansion and increasing adoption of metal additive manufacturing technologies are driving strong equipment demand.

Government-backed advanced manufacturing initiatives and rising aerospace production are further supporting market growth.

India Additive Manufacturing Equipment Market

India’s market is estimated at around USD 0.51 billion in 2026, representing approximately 4.2% of global revenues. Growing industrial digitization and expanding healthcare manufacturing are driving adoption of additive manufacturing systems.

Government initiatives promoting local manufacturing and advanced production technologies are further accelerating growth.

Middle East & Africa and South America

The Middle East & Africa and South America are gradually emerging as growth markets for additive manufacturing equipment, supported by industrial diversification initiatives and increasing investments in advanced manufacturing capabilities. Aerospace, energy, and healthcare sectors are witnessing gradual adoption of industrial 3D printing technologies.

Additionally, increasing awareness regarding localized manufacturing and reduced supply chain dependency is expected to support long-term market growth across these regions.

GCC Additive Manufacturing Equipment Market

The GCC market is estimated at around USD 0.34 billion in 2026, representing approximately 2.8% of global revenues. Industrial diversification programs and investments in aerospace and healthcare infrastructure are supporting additive manufacturing adoption.

Increasing focus on advanced manufacturing and digital production technologies is further strengthening market opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players

Industrial Metal Printing Innovation and Automation Strengthening Competitive Positioning of Key Players

The additive manufacturing equipment market is highly competitive, with leading companies focusing on high-speed metal printing systems, automation integration, and scalable industrial production platforms. Manufacturers are investing heavily in advanced powder bed fusion technologies, software integration, and automated workflow solutions to improve production efficiency and repeatability.

Strategic partnerships with aerospace, healthcare, and automotive companies, along with investments in industrial-scale additive manufacturing ecosystems, remain key differentiators shaping market competition.

LIST OF KEY ADDITIVE MANUFACTURING EQUIPMENT COMPANIES PROFILED IN REPORT

- Stratasys Ltd. (U.S.)

- 3D Systems Corporation (U.S.)

- EOS GmbH (Germany)

- GE Additive (U.S.)

- Nikon SLM Solutions (Germany)

- Desktop Metal Inc. (U.S.)

- HP Inc. (U.S.)

- Renishaw plc (U.K.)

- TRUMPF Group (Germany)

- Materialise NV (Belgium)

KEY INDUSTRY DEVELOPMENTS

- February 2025: EOS GmbH announced expansion of its industrial metal additive manufacturing portfolio with new automated production solutions designed for serial aerospace and automotive manufacturing applications.

- January 2025: Stratasys Ltd. launched upgraded industrial polymer 3D printing systems featuring enhanced throughput and multi-material capabilities for manufacturing and tooling applications.

- October 2024: 3D Systems Corporation expanded its healthcare additive manufacturing operations through new partnerships focused on personalized medical devices and dental applications.

- July 2024: TRUMPF Group introduced advanced laser metal fusion systems with integrated automation features aimed at improving productivity in industrial additive manufacturing environments.

- April 2024: Nikon SLM Solutions launched the upgraded NXG XII 600 metal additive manufacturing platform targeting high-volume aerospace and energy sector applications with enhanced productivity and larger build capacity.

REPORT COVERAGE

The global report on additive manufacturing equipment market analysis includes a comprehensive study of market size & forecast across all major segments covered in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence market growth during the forecast period. The report also covers technological advancements in industrial 3D printing systems, metal additive manufacturing technologies, automated production workflows, and advanced software integration platforms.

In addition, the study includes analysis of key strategic developments such as partnerships, consumer product launches, facility expansions, and acquisitions undertaken by major market participants. Furthermore, it offers regional insights and competitive landscape analysis, highlighting the market positioning, technological capabilities, and strategic initiatives of leading additive manufacturing equipment providers globally.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material Type, End-Use Industry, By Equipment, and Region |

| By Equipment |

|

| By Material Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 10.37 billion in 2025 and is projected to reach USD 35.20 billion by 2034.

In 2025, the North America’s market value stood at USD 3.47 billion.

The market is expected to exhibit a CAGR of 14.4% during the forecast period of 2026-2034.

By end-use industry, the aerospace & defense segment is expected to lead the market.

Rising demand for lightweight and complex components is the key factor driving the market growth.

Stratasys Ltd., 3D Systems Corporation, EOS GmbH, GE Additive, and Nikon SLM Solutions are the major players in global smart factory market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us