Advanced Vehicle Diagnostics & Remote Services Market Size, Share & Industry Analysis, By Offerings (Predictive & Condition-Based Diagnostics, Remote Vehicle Health Monitoring & Fault Diagnostics, Over-the-Air (OTA) Software & Firmware Management, Remote Control, Calibration & Feature Activation, and Cybersecurity, Compliance & System Integrity Services), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By End User (Individual Vehicle Owners, Fleet Operators, Automotive OEMs & Tier-1 Suppliers, and Workshops & Service Networks), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

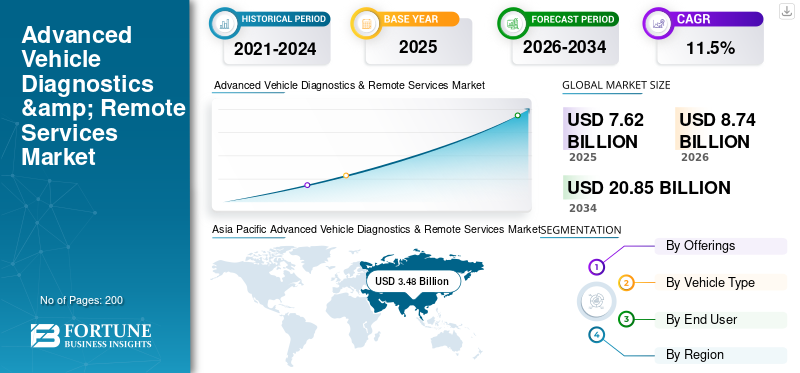

The global advanced vehicle diagnostics & remote services market size was valued at USD 7.62 billion in 2025. The market is projected to grow from USD 8.74 billion in 2026 to USD 20.85 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. Asia Pacific dominated the global market with a market share of 45.67% in 2025.

The rapid expansion of connected vehicles is a key driver of growth in the advanced vehicle diagnostics & remote services market, supported by rising software-defined vehicle (SDV) adoption, and increasing reliance on predictive maintenance to reduce downtime and warranty costs. OEMs are monetizing vehicle software through over-the-air (OTA) updates, remote troubleshooting, and feature activation, while fleets adopt continuous health monitoring to maximize uptime. Cybersecurity and regulatory compliance needs are also increasing as vehicles become more connected and updatable, accelerating demand for integrity monitoring and secure OTA operations.

- For instance, in April 2025, Geotab expanded its OEM partnerships, reporting collaboration with over 80% of leading OEMs to improve vehicle data harmonization and scale OEM telematics integrations. These efforts enable broader deployment of remote diagnostics, vehicle health insights, and mixed-fleet management capabilities. This supports higher penetration of remote services and recurring software-driven revenues across passenger and commercial vehicles.

The ecosystem is being strengthened through standardization initiatives aimed at enhancing interoperability in remote diagnostics and OTA operations. Collaboration efforts between ASAM and the eSync Alliance are advancing service-oriented diagnostics and OTA service-oriented vehicle frameworks, reducing integration friction and accelerating adoption across the automation value chain.

Major players in the global advanced vehicle diagnostics and remote services market include Bosch, Continental, ZF, Aptiv, Harman, Denso, Hyundai Mobis, Geotab, Verizon Connect, and Sibros Technologies. These companies compete through AI-enabled diagnostics, cloud-based remote monitoring, OTA software platforms, cybersecurity solutions, and strategic OEM partnerships supporting software-defined and connected vehicle ecosystems.

Download Free sample to learn more about this report.

Advanced Vehicle Diagnostics & Remote Services Market Trends

Rising Software-Defined Vehicle Architectures Boost Market Expansion

The shift toward software-defined vehicles is fundamentally reshaping how diagnostics and remote services are designed, delivered, and monetized. Vehicles are increasingly built around centralized computing architectures and service-oriented software layers, enabling continuous monitoring, remote fault resolution, and post-sale feature enhancement. Diagnostics have evolved beyond basic fault-code reading to support predictive analytics, system-level health assessments, and cross-domain visibility. This trend enables OEMs to enhance vehicle reliability throughout the lifecycle, reduce physical service interventions, and facilitate recurring digital revenue models through cloud-based platforms and OTA-enabled diagnostics ecosystems.

- In June 2024, Volkswagen Group expanded its Cariad software platform to support centralized vehicle diagnostics and OTA-based system monitoring across multiple brands.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Predictive Maintenance Drives Market Expansion

The rising focus on minimizing vehicle downtime and ownership costs is driving the adoption of advanced diagnostics and remote services across passenger and commercial vehicles. Predictive and condition-based diagnostics enable early detection of component degradation, allowing maintenance to be scheduled before failures occur. Fleet operators, in particular, benefit from reduced unplanned downtime, improved asset utilization, and lower total cost of ownership. OEMs also leverage predictive diagnostics to reduce warranty claims and improve product quality feedback loops. As vehicles incorporate more sensors, ECUs, and connectivity, predictive diagnostics are becoming a core requirement rather than an optional capability.

- In March 2025, Daimler Truck highlighted expanded use of predictive maintenance and remote diagnostics across its connected truck platforms to improve fleet uptime.

MARKET RESTRAINTS

High System Complexity and Integration Costs Limit Wider Adoption

Despite strong growth potential, the market faces restraint from the high complexity and cost of integrating advanced diagnostics and remote service centers across diverse vehicle platforms. Legacy vehicle architectures, fragmented ECU ecosystems, and a lack of standardized data models all contribute to increased development and deployment costs. Smaller OEMs and aftermarket service providers often struggle to justify investments in cloud infrastructure, cybersecurity frameworks, and continuous software updates. Additionally, integrating diagnostics across powertrain, ADAS, infotainment, and battery systems requires significant validation and testing, which slows deployment timelines and limits near-term adoption in cost-sensitive markets.

MARKET OPPORTUNITIES

Regulatory Push for OTA and Software Compliance Creates New Revenue Opportunities

Evolving automotive regulations related to software updates, cybersecurity, and vehicle safety are creating strong opportunities for advanced diagnostics and remote services providers. Regulators increasingly require OEMs to demonstrate end-to-end control over vehicle software integrity, update processes, and fault traceability throughout the vehicle's lifecycle. This drives demand for OTA management platforms, compliance monitoring, and secure remote diagnostics solutions. Service providers that enable regulatory compliance, auditability, and lifecycle software management are well-positioned to capture long-term, recurring revenues as regulations expand across regions and vehicle categories.

- For instance, in January 2021, UN Regulation No. 156 on Software Updates (SUMS) entered into force, mandating structured OTA and software management processes for vehicle type approval.

MARKET CHALLENGE

Cybersecurity Risks and Data Privacy Concerns Remain a Critical Challenge

As vehicles become increasingly connected and reliant on remote diagnostics and OTA services, cybersecurity and data privacy challenges intensify. Remote access points, cloud connectivity, and continuous data exchange increase the attack surface for cyber threats. A successful breach can compromise vehicle safety, disrupt fleet operations, and damage OEM brand trust. Ensuring end-to-end security across vehicle hardware, software, communication networks, and cloud platforms requires constant investment and expertise. Managing end-to-end cybersecurity at scale while maintaining system performance and regulatory compliance remains one of the most complex challenges facing the market.

- In July 2024, the U.S. National Highway Traffic Safety Administration reiterated its expectations for cybersecurity risk management in connected vehicles and OTA-enabled systems.

Download Free sample to learn more about this report.

Segmentation Analysis

By Offerings

Remote Vehicle Health Monitoring & Fault Diagnostics Segment Leads due to their Reduced Downtime

Based on offerings, the market is segmented into predictive & condition-based diagnostics, remote vehicle health monitoring & fault diagnostics, OTA software & firmware management, remote control & calibration, and cybersecurity services. Remote vehicle health monitoring & fault diagnostics dominate due to their immediate value in real-time fault detection, reduced downtime, and proactive service scheduling across passenger and commercial vehicles. OEMs and fleets rely heavily on continuous vehicle health insights to optimize maintenance and warranty costs.

OTA software & firmware management is the fastest-growing segment, with a CAGR of 14.1% during the forecast period.

- In April 2025, Geotab expanded OEM telematics integrations to enhance real-time vehicle health monitoring across mixed fleets.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Higher Penetration of ADAS Accelerated SUV Segment Growth

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs. SUVs represent the dominant segment due to their higher penetration of ADAS, infotainment systems, connected features, and multiple ECUs, which significantly increases the need for advanced diagnostics and remote services.

SUVs also command higher average software and service revenue per vehicle. The segment is also the fastest-growing, with a CAGR of 12.3%, supported by rising global SUV sales and increasing consumer demand for connected and feature-rich vehicles.

- In May 2024, Toyota highlighted expanding connected diagnostics and OTA capabilities across its global SUV portfolio.

By End User

Growing Ownership Base Boosted Individual Vehicle Owner Segment Leadership

Based on end user, the market is segmented into individual vehicle owners, fleet operators, automotive OEMs & Tier-1 suppliers, and workshops & service networks. Individual vehicle owners dominated the market due to the sheer volume of passenger vehicles adopting connected diagnostics, OTA updates, and remote health alerts. These services improve ownership experience and reduce unexpected repair events.

Fleet operators are the fastest-growing segment, with a CAGR of 13.8% during the forecast period.

- In March 2025, Daimler Truck emphasized expanded use of remote diagnostics to improve fleet reliability and maintenance planning.

Advanced Vehicle Diagnostics & Remote Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Advanced Vehicle Diagnostics & Remote Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America exhibits steady growth, driven by high connected-vehicle penetration, strong fleet telematics adoption, and the early commercialization of software-defined vehicle platforms. OEMs and fleet operators actively deploy remote diagnostics, predictive maintenance, and OTA updates to reduce downtime and warranty exposure. The region benefits from advanced cloud infrastructure, high EV adoption, and regulatory focus on vehicle cybersecurity, supporting continued demand for remote monitoring, OTA management, and compliance-oriented diagnostics across passenger and commercial vehicles.

U.S.

The U.S. leads regional demand due to large passenger and commercial vehicle fleets, widespread telematics adoption, and strong OEM investment in OTA and predictive diagnostics. Fleet-driven uptime optimization and EV software complexity continue to expand recurring remote services revenues.

Europe

Europe’s growth is shaped by strong regulatory frameworks around vehicle software updates, cybersecurity, and functional safety. OEMs increasingly rely on advanced diagnostics and OTA platforms to meet type-approval and compliance requirements while managing complex multi-brand vehicle portfolios. Rising electrification, centralized vehicle architectures, and cross-border fleet operations support demand for predictive diagnostics, secure OTA updates, and system integrity services. However, growth in the region is more measured due to market maturity.

U.K.

The U.K. benefits from strong adoption of connected fleets, insurance telematics usage, and OEM software development activity. The need for fleet optimization and the growing deployment of remote diagnostics across electric and connected passenger vehicles support demand.

Germany

Premium OEMs, advanced vehicle electronics, and early adoption of software-defined vehicle platforms drive Germany’s market. Strong focus on OTA compliance, cybersecurity, and system diagnostics sustains high per-vehicle service intensity.

Asia Pacific

Asia Pacific represents the fastest-growing region due to its massive vehicle parc, rapid EV adoption, expanding connectivity infrastructure, and strong domestic OEM ecosystems. The rising software content in vehicles, cost-efficient cloud deployment, and large-scale fleet digitization are accelerating the adoption of remote diagnostics and OTA services. Countries such as China, Japan, and India drive growth through a mix of advanced SDV strategies, manufacturing scale, and expanding connected-vehicle penetration.

China

China dominates regional demand due to the world’s largest vehicle and EV base, aggressive OTA deployment, and strong domestic software-centric OEMs. High EV penetration significantly increases demand for battery diagnostics, OTA updates, and cybersecurity monitoring.

Japan

Japan’s growth is supported by technologically advanced OEMs focusing on reliability, predictive maintenance, and gradual OTA rollout. Demand is driven by high vehicle quality standards, aging vehicle parc management, and increasing software integration.

India

India is the fastest-growing major market, driven by rising vehicle production, rapid adoption of connectivity, and increasing fleet digitization. Expanding EV launches and cost-focused predictive diagnostics accelerate the uptake of remote services across mass-market vehicles.

Rest of the World

The Rest of the World market is expected to grow steadily as emerging economies enhance their digital infrastructure, fleet management practices, and connected-vehicle penetration. Adoption is strongest in commercial fleets and premium passenger vehicles, where remote diagnostics reduce operating costs. OEM OTA rollouts and smartphone-based connectivity solutions drive early adoption, while regulatory alignment and EV growth remain longer-term catalysts across Latin America, the Middle East & Africa.

COMPETITIVE LANDSCAPE

Key Industry Players

Software-Centric Platforms Shape Advanced Vehicle Diagnostics & Remote Services Competitiveness

The global advanced vehicle diagnostics & remote services market trends are characterized by rapid adoption of software-centric architectures, cloud-based analytics, and secure over-the-air platforms. Leading players, including Bosch, Continental, ZF, Aptiv, Harman, Denso, Hyundai Mobis, Geotab, and Verizon Connect, compete through integrated diagnostics software, predictive maintenance algorithms, and scalable telematics platforms. Companies enhance competitiveness by investing in AI-driven fault analytics, expanding global software engineering centers, and forming partnerships with cloud and cybersecurity providers. Modular service center platforms, OEM-specific customization, and compliance-focused solutions strengthen differentiation.

LIST OF KEY ADVANCED VEHICLE DIAGNOSTICS & REMOTE SERVICES COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Aptiv PLC (Ireland)

- HARMAN International (U.S.)

- Denso Corporation (Japan)

- Valeo SA (France)

- Hyundai Mobis (South Korea)

- Visteon Corporation (U.S.)

- Panasonic Automotive Systems (Japan)

- Garmin Ltd. (Switzerland)

- Geotab Inc. (Canada)

- Trimble Inc. (U.S.)

- Verizon Connect (U.S.)

- TomTom Telematics (Webfleet) (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- June 2025- Geotab and Mercedes-Benz USA launched an integrated telematics solution that unifies factory-installed telematics data from Mercedes-Benz EVs and ICE vehicles into the MyGeotab platform, enhancing real-time vehicle health diagnostics, GPS tracking, and fleet insights. This integration eliminates the need for aftermarket hardware installation and streamlines visibility and operations for mixed fleets.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.5% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Offerings, By Vehicle Type, By End User, and By Region. |

|

By Offerings |

· Predictive & Condition-Based Diagnostics · Remote Vehicle Health Monitoring & Fault Diagnostics · Over-the-HCV (OTA) Software & Firmware Management · Remote Control, Calibration & Feature Activation · Cybersecurity, Compliance & System Integrity Services |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By End User |

· Individual Vehicle Owners · Fleet Operators · Automotive OEMs & Tier-1 Suppliers · Workshops & Service Networks |

|

By Geography |

· North America (By Offerings, By Vehicle Type, By End User, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Offerings, By Vehicle Type, By End User, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Offerings, By Vehicle Type, By End User, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World ( By Offerings, By Vehicle Type, and By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.62 billion in 2025 and is projected to reach USD 20.85 billion by 2034.

In 2025, the market value stood at USD 3.48 billion.

The market demand is expected to grow at a CAGR of 11.5% during the forecast period (2026-2034).

The individual vehicle owners segment led the market by end-user.

Increasing demand for predictive maintenance is the key factor driving market expansion.

Top players in the market include Bosch, Continental, ZF, Aptiv, Harman, Denso, Hyundai Mobis, Geotab, and Verizon Connect.

Asia Pacific accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us