Aero Acoustic Wind Tunnel Market Size, Share & Industry Analysis, By Test Type (Jet Noise Tests, Airframe Noise Tests, Rotor/Propeller Noise, and others), By Facility Type (Large-scale aero-acoustic wind tunnels, Anechoic jet-noise rigs, Hybrid/multi-purpose tunnels, Dedicated UAM/rotorcraft acoustic rigs, and Cryogenic/high-Reynolds Number Tunnels With Acoustic Modules), By Service Mode (Government-funded facility, Commercial test service,, and Others), By End User (Airframe OEMs, engine OEMs, Rotorcraft OEMs, UAM/eVTOL OEMs/Startups, and others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

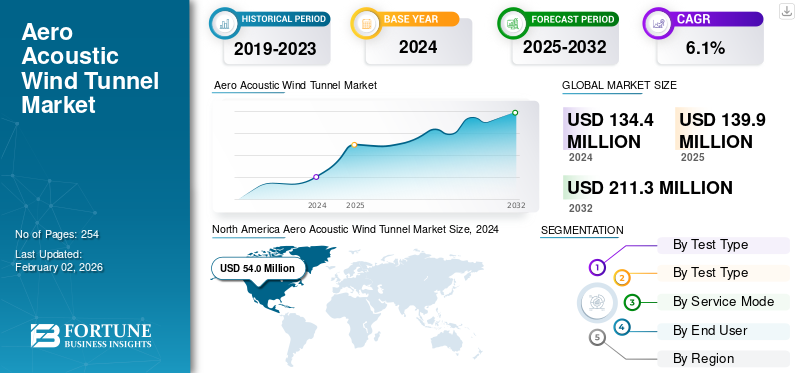

The global aeroacoustic wind tunnel market size was valued at USD 140 million in 2025. The market is projected to grow from USD 148 million in 2026 to USD 232.00 million by 2034, exhibiting a CAGR of 5.70% during the forecast period. North America dominated the global market with a share of 40.20% in 2025.

The market is central to designing the next generation of quieter and cleaner aircraft. Aeroacoustic wind tunnels are specialized tunnels that measure how airflow generates and transmits sound around engines, propellers, and airframes. This capability is critical as aviation shifts towards hybrid-electric propulsion, eVTOLs, and stricter global noise standards. Unlike traditional aerodynamic tunnels, they feature anechoic chambers, low-noise fans, and high-density microphone arrays to pinpoint noise sources with high precision.

In recent years, aerospace agencies and research institutes have increased their investments in advanced testing infrastructure. Key players such as NASA (USA), DLR (Germany), ONERA (France), NLR (Netherlands), ISAE-SUPAERO (France), CSIR-NAL/ISRO (India), JAXA (Japan), and KARI (South Korea) are leading the new tunnel developments and acoustic upgrades.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Tightening Global Noise Rules and Certification Mandates Fuel Aero Acoustic Wind Tunnel Demand

In recent years the aerospace industry has witnessed a growing convergence of regulatory pressure and technological requirement around aircraft noise compliance a dynamic that strongly favors increasing demand for aero-acoustic wind tunnel infrastructure. The International Civil Aviation Organization (ICAO) has long emphasized the “Balanced Approach” to aircraft noise management, which prioritizes reduction of noise at source, land-use planning, operational procedures, and restrictions. Meanwhile, the Federal Aviation Administration (FAA) in the U.S. continues its Noise Policy Review, with the establishment of an Aircraft Noise Advisory Committee under the 2024 Reauthorization Act, signaling that noise regulations are likely to become more stringent.

MARKET RESTRAINTS

High CapEx, Operational Costs, and Access Constraints Limit Market Expansion

The aero acoustic wind tunnel market growth faces a material restraint anchored through its high cost base, complexity, and limited accessibility. Constructing, outfitting and operating a wind tunnel capable of aero-acoustic testing solutions (including anechoic chambers, large microphone arrays, controlled acoustic backgrounds, high-speed flow, instrumentation for noise source localization, and data processing) represents a major capital investment. Industry estimates that even standard wind-tunnel infrastructures can require tens of millions of U.S. dollars, with supersonic/hypersonic or acoustic specialized tunnels costing significantly more.

MARKET OPPORTUNITIES

Emerging Urban Air Mobility, eVTOL and Supersonic Programmes Open New Aero-Acoustic Testing Frontiers

A compelling opportunity for the market lies in the rapidly growing domain of urban air mobility (UAM), electric vertical take-off and landing (eVTOL) aircraft, and the re-emergence of commercial supersonic transport, each of which places novel acoustic demands on aerospace developers and thus, on aero-acoustic test infrastructure.

eVTOL and UAM platforms typically operate in low-altitude urban environments where noise is one of the major acceptance issues in the community. Acoustic certification of rotorcraft-like operations, transition flight phases, multirotor wakes, electric propulsion, and vertical ascent/descent manoeuvres all require finely tuned aero-acoustic characterization. The physical complexity of rotor-wake interactions, fan/prop-noise coupling, and environment-driven acoustic propagation means aero-acoustic wind tunnels are increasingly relevant early in the design cycle.

MARKET CHALLENGES

Limited Accessibility and Scalability of Testing Infrastructure Pose as Challenges in Operations

A major challenge in the market growth lies in the limited accessibility and scalability of testing infrastructure. Most of the high-end acoustic tunnels are concentrated within government research centers or national laboratories, leaving smaller OEMs, startups, and universities dependent on restricted testing slots or costly outsourcing. The high technical complexity of maintaining ultra-low background noise levels, precise flow uniformity, and advanced acoustic instrumentation adds to scheduling bottlenecks and limited throughput. Moreover, the long lead times for tunnel bookings done often months in advance, slows down iterative design and certification processes. As aerospace development accelerates, especially with eVTOLs and hybrid propulsion programs, the gap between test demand and facility availability continues to widen.

AERO ACOUSTIC WIND TUNNEL MARKET TRENDS

Digital-Hybrid Test Approaches and Integrated Aero-Acoustic Workflows are the Latest Trends in the Market

A defining trend reshaping the aero acoustic wind tunnel market is the shift toward digital-hybrid testing which is a seamless integration of computational simulation, high-fidelity sensors, and physical wind tunnel experiments. This approach is transforming how aerospace developers design, test, and validate aircraft noise performance, merging the best of digital modeling and experimental realism. Traditionally, aero-acoustic wind tunnels were treated as the final step in validation, used to confirm or fine-tune results from analytical models. Testing is now a part of an iterative, data-rich loop where engineers start with CFD-based aero-acoustic simulations, predict noise propagation using digital twins, conduct targeted tunnel campaigns with instrumented models, and then feed real-world data back into simulation frameworks.

Download Free sample to learn more about this report.

Segmentation Analysis

By Test Type

Rising Demand for Low-Emission Propulsion and Strict Fan Noise Certifications Drives the Adoption of Jet Noise Testing Test Type

Based on test type, the market is categorized into jet noise tests, airframe noise tests, rotor/propeller noise, hybrid/electric propulsion acoustic tests, and supersonic & boom noise tests.

The jet noise test segment accounted for the dominating market share of 32.77% in 2026. Growing focus on quieter engines, energy efficiency and fuel efficiency of engines, and stricter ICAO/FAA noise standards is pushing OEMs to expand on jet noise testing for new high-bypass turbofans and hybrid-electric propulsion systems.

Hybrid/electric propulsion acoustic tests segment is projected to grow at the highest CAGR of 8.0% over 2025-2032.

By Facility Type

Deand for Noise Interactions Measurement in Propulsion Systems is Pushing the Dominance of Large-Scale Aero-Acoustic Wind Tunnels Segment

In terms of facility type, the market is categorized into large-scale aero-acoustic wind tunnels, anechoic jet-noise rigs, hybrid/multi-purpose tunnels, dedicated UAM/rotorcraft acoustic rigs, and cryogenic/high-reynolds number tunnels with acoustic modules.

The large-scale aero-acoustic wind tunnels captured the largest share of 38.94% in the market in 2026. The development of large anechoic and hybrid test tunnels enables accurate measurement of complex noise interactions in full-scale aircraft and propulsion systems, supporting the need for advanced certification programs.

Dedicated UAM/rotorcraft acoustic rigs segment is expected to grow at a highest CAGR of 8.4% over the forecast period.

By Service Mode

National Research Investments for Strategic Acoustic Testing Capabilities is Propelling the Demand in Government-Funded Facility Segment

Based on service mode, the market is segmented into government-funded facility, commercial test service, confidential proprietary contracts (OEM-exclusive), and university/academic access programs.

The government-funded facility segment held the dominating position in 2026 with a share of 38.55%. Governments are investing in acoustic modernization and new test complexes to maintain national competitiveness, reduce reliance on foreign infrastructure, and support domestic aerospace R&D.

The segment of commercial test service is set to flourish and is estimated to be growing at a CAGR of 5.6% growth across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

OEM-Led Innovation and Next-Gen Noise Limit Compliances are Boosting the Adoption of Product in the Airframe OEM Segment

As per end user, the market is studied into airframe OEMs, engine OEMs, rotorcraft OEMs, UAM/VTOL OEMs/startups, tier-1 suppliers, defense users, regulators, and research consortia/agencies.

The airframe OEMs segment led with the dominating position in 2026 with 36.45% share. Major airframe manufacturers are driving acoustic design validation across flaps, landing gear, and fuselage elements to meet next-generation community noise limits and enhance cabin comfort.

The engine OEMs segment will witness a growth rate of 5.6% across the forecast period.

Aero Acoustic Wind Tunnel Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Aero Acoustic Wind Tunnel Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 56.3 Million in 2025, accounting for a 40.20% share, and is expected to reach USD 59.7 Million in 2026. Growth of the market in North America is driven by the region’s long-standing leadership in aerospace research and defense testing. The U.S. government’s sustained funding to top-tier facilities such as the one in NASA is resulting in a stable and scaled wind-tunnel acoustic programmes. The U.S. market is valued at USD 34.53 billion by 2026.

Europe and Asia Pacific

Europe and Asia Pacific are set to observe a notable market growth in the coming years. During the forecast period, the Asia Pacific market accounted for USD 37.2 million in 2025, representing 26.60% of the global industry, and is expected to reach USD 39.9 million in 2026, which is the maximum out of all the regions. The region has emerging markets owing to rapid industrialization, expansion of aerospace manufacturing, and increasing investments in test infrastructure. For example, countries like China and India are allocating resources to expand their aero-acoustic facilities in national laboratories and universities to support indigenous air- and rotor-craft programmes. The Japan market is valued at USD 11.89 billion by 2026, the China market is valued at USD 11.17 billion by 2026, and the India market is valued at USD 10.47 billion by 2026.

After Asia Pacific, in 2025, Europe generated USD 36.2 million, contributing 25.90% to global market revenue, and is projected to grow to USD 38.1 million in 2026. In the region, the U.K. market is valued at USD 6.54 billion by 2026, and the Germany market is valued at USD 8.90 billion by 2026. Europe is projected to witness significant growth in the market because of its mature aerospace and automotive sectors, strong regulatory environment, and collaborative R&D frameworks.

Rest of the World

Rest of the World accounted for USD 10.3 million in 2025, representing 7.30% of the global market share, and is projected to reach USD 10.7 million in 2026. Over the forecast period, Latin America and Middle East & Africa would witness moderate growth rates. The market in the Middle East in 2025 is set to record USD 6.3 million as its valuation. Latin America is set to attain the value of USD 3.9 million 2025. Middle East & Africa and Latin America regions’ growth is driven by a focus on developing local capabilities along with a rise in government spending in defense and aerospace on aero acoustic wind tunnel capabilities.

COMPETITIVE LANDSCAPE

Key Market Players

Strategic Collaborations and Integrated Digital Workflows by Prominent Market Players are Defining Market Competition

The aero acoustic wind tunnel market is shaped by strategic partnerships, acoustic precision, and digital integration. Key facilities including NASA, DLR, ONERA, DNW, NRC Canada, NLR, and JAXA are leading through world-class acoustic fidelity and propulsion airframe integration. Universities including ISAE-SUPAERO, RWTH Aachen, and IIT-Kanpur are driving agile and specialized research, while new facilities including TAI’s TST (Turkey), AVIC FL-10 (China), and India’s CTWT are expanding their global capacities. Competition now centers on digital hybrid workflows, AI-assisted data systems, and fast turnaround rather than tunnel size. Collaboration with OEMs such as Airbus, Boeing, Safran, and GE is currently defining the market leadership and innovation momentum.

LIST OF KEY AERO ACOUSTIC WIND TUNNELS COMPANIES PROFILED

- NASA (National Aeronautics and Space Administration) (U.S.)

- DLR (German Aerospace Center) (Germany)

- ONERA (Office National d’Études et de Recherches Aérospatiales) (France)

- DNW (German–Dutch Wind Tunnels) (Germany)

- JAXA (Japan Aerospace Exploration Agency) (Japan)

- ETW GmbH (European Transonic Wind Tunnel) (Germany)

- NLR (Royal Netherlands Aerospace Centre) (Netherlands)

- RUAG International (Switzerland)

- CSIR–NAL (National Aerospace Laboratories) (India)

- CARDC (China Aerodynamics Research & Development Center) (China)

- TU Delft (Delft University of Technology) (Netherlands)

- University of Bristol (U.K.)

- University of Southampton (ISVR)

- Pennsylvania State University (Penn State) (U.S.)

- IIT Kanpur (Indian Institute of Technology Kanpur) (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: DNW signed a Letter of Intent (LoI) with aircraft manufacturer ATR to further explore the wind-tunnel testing collaboration.

- August 2025: NASA used its 14-by-22-Foot Subsonic Wind Tunnel at Langley to test a 7-foot wing model with multiple propellers in support of Advanced Air Mobility (AAM) The campaign was focused on propeller-wing interactions and will publicly release the data to support wind tunnel industry.

- January 2024: A framework agreement for a comprehensive testing plan from 2024 to 2028 was signed by Safran Aircraft Engines and ONERA, the national aerospace research organization of France.

- March 2023: China Aerodynamics Research and Development CARDC finished building and enlarging the ä300mm Ludwig Hypersonic Quiet Tunnel.

- March 2023: At the RUAG Large Subsonic Wind Tunnel in Emmen, Switzerland, Archer finished a six-week wind tunnel test campaign of its Midnight aircraft configuration. In order to stay on schedule for Midnight's next flight test program, Archer was able to collect useful data from the tests at RUAG that will help confirm the Midnight vehicle configuration, its aerodynamic tests models, external load predictions, aircraft performance, stability and control characteristics, and performance degradation in icing conditions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.70% from 2026 – 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Test Type, Facility Type, Service Mode, End User, and Region |

|

By Test Type |

· Jet Noise Tests · Airframe Noise Tests · Rotor/Propeller Noise · Hybrid/Electric Propulsion Acoustic Tests · Supersonic & Boom Noise Tests |

|

By Facility Type |

· Large-scale aero-acoustic wind tunnels · Anechoic jet-noise rigs · Hybrid/multi-purpose tunnels · Dedicated UAM/rotorcraft acoustic rigs · Cryogenic/high-reynolds number tunnels with acoustic modules |

|

By Service Mode |

· Government-funded facility · Commercial test service · Confidential proprietary contracts (OEM-exclusive) · University/academic access programs |

|

By End User |

· Airframe OEMs · Engine OEMs · Rotorcraft OEMs · UAM/eVTOL OEMs/Startups · Tier-1 Suppliers · Defense Users · Regulators · Research Consortia/Agencies |

|

By Region |

· North America (By Test Type, Facility Type, Service Mode, End User and Country) o U.S. (By End User) o Canada (By End User) · Europe (By Test Type, Facility Type, Service Mode, End User and Country/Sub-region) o U.K. (By End User) o Germany (By End User) o France (By End User) o Italy (By End User) o Russia (By End User) o Netherlands (By End User) o Rest of Europe (By End User) · Asia Pacific (By Test Type, Facility Type, Service Mode, End User and Country/Sub-region) o China (By End User) o India (By End User) o Japan (By End User) o South Korea (By End User) o Rest of Asia Pacific (By End User) · Rest of the World (By Test Type, Facility Type, Service Mode, End User and Country/Sub-region) o Middle East & Africa (By End User) o Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 140 million in 2025 and is projected to reach USD 232.00 million by 2034.

In 2025, the market value stood at USD 56.3 million.

The market is expected to exhibit a CAGR of 5.70% during the forecast period.

The jet noise tests segment led the market by test type.

Tightening global noise rules and certification mandates fuel the product demand in the market.

NASA (National Aeronautics and Space Administration) (US), DLR (German Aerospace Center) (Germany), ONERA (Office National d’Études et de Recherches Aérospatiales) (France) , DNW (German–Dutch Wind Tunnels) (Germany), and JAXA (Japan Aerospace Exploration Agency) (Japan) are the prominent market players.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2025

- 254

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us