Advanced Air Mobility Market Size, Share & Industry Analysis, and Russia-Ukraine War Impact Analysis, By Component (Hardware and Software), By Product (Fixed Wing, Rotary Blade, and Hybrid), By Propulsion Type (Gasoline, Electric, and Hybrid), By Application (Cargo Transport, Passenger Transport, Mapping & Surveying, Special Mission, Surveillance & Monitoring, and Others), By End-Use (Commercial and Government & Military), and Regional Forecast Report, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

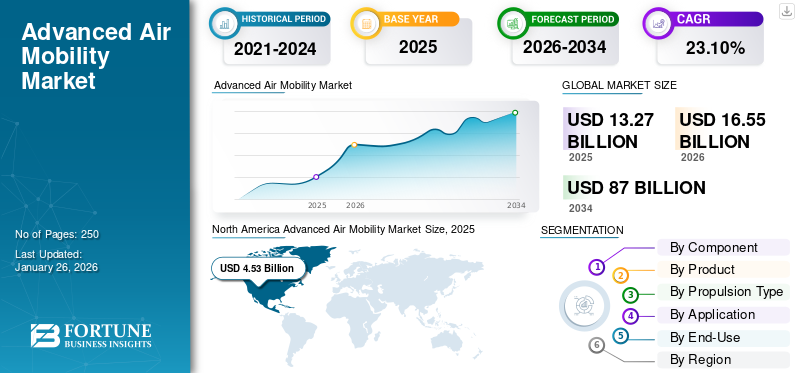

The global advanced air mobility market size was valued at USD 13.27 billion in 2025 and is projected to grow from USD 16.55 billion in 2026 to USD 87.00 billion by 2034, exhibiting a CAGR of 23.10% during the forecast period. North America dominated the advanced air mobility market with a market share of 34.12% in 2025. Rising investments in electric propulsion technologies, regional air connectivity, and autonomous flight systems are accelerating growth in the advanced air mobility market.

Advanced Air Mobility (AAM) is poised to revolutionize transportation by integrating novel aircraft designs, propulsion systems, and air traffic management technologies into existing airspace. It envisions a network of aircraft operating in urban, suburban, and rural areas, offering services such as Urban Air Mobility (UAM) for intra-city transport, Regional Air Mobility (RAM) connecting smaller communities, and efficient cargo transportation.

Key players are diverse, spanning aircraft manufacturers, infrastructure providers, technology companies, and operators. On the aircraft front, Joby Aviation leads with its eVTOL design, followed by Archer Aviation, partnering with United Airlines. Vertical Aerospace, EHang, Lilium, and Volocopter are also major contenders. Incumbents such as Airbus and Boeing are leveraging their expertise to explore AAM. Infrastructure is being developed by Skyports and Ferrovial, focusing on vertiport construction. Technology companies such as Honeywell and Collins Aerospace provide essential avionics and control systems. Finally, airlines such as United Airlines and American Airlines are partnering with AAM companies, signaling a future where these services are integrated into traditional air travel.

The COVID-19 pandemic had a mixed impact on the market. Initially, it caused disruptions in supply chains, leading to manufacturing delays for AAM aircraft and components. Investment slowed down as investors became more cautious. Travel restrictions further hampered crucial testing and certification processes.

However, the pandemic also acted as a catalyst in several ways. The need for contactless solutions boosted the adoption of drone delivery services, increasing public awareness and acceptance of AAM technologies. The focus shifted toward automation and efficiency in logistics and transportation, driving further interest in AAM. Recognizing the potential for job creation and economic stimulus, governments provided financial support for AAM development. As the initial shock subsided, investor confidence returned, with AAM companies attracting significant funding rounds.

The long-term outlook for AAM is positive, spurred by increased awareness, government support, and renewed investor confidence. The pandemic accelerated the adoption of adjacent technologies, including drone delivery, paving the way for broader AAM acceptance. The global focus on sustainability aligns well with the development of electric and hybrid-electric aircraft, a core element of the AAM ecosystem.

Download Free sample to learn more about this report.

Advanced Air Mobility Market Key Takeaways

- 2025 Market Size: USD 13.27 billion

- 2026 Market Size: USD 16.55 billion

- 2034 Forecast Market Size: USD 87.00 billion

- CAGR: 23.10% from 2026–2034

- North America dominated the advanced air mobility market with a 34.12% share in 2025.

- The rotary blade segment held the largest market share of 70.94% in 2026.

- The electric propulsion segment accounted for a 70.66% market share in 2026.

North America

North America was valued at USD 4.53 Billion in 2025 and is projected to reach USD 5.61 Billion in 2026, supported by strong investments in eVTOL development and infrastructure planning initiatives.

Asia Pacific

Asia Pacific was valued at USD 4.03 Billion in 2025 and is projected to reach USD 5.09 Billion in 2026, supported by government-backed innovation programs and rising regional connectivity projects.

Europe

Europe was valued at USD 3.13 Billion in 2025 and is projected to reach USD 3.9 Billion in 2026, driven by sustainability goals and supportive aviation regulations.

U.S.

The U.S. market is projected to reach USD 5.16 Billion in 2026, owing to FAA-led regulatory development and commercial eVTOL deployment activities.

Japan

The Japan market is projected to reach USD 0.7 Billion in 2026, driven by investments focused on reducing urban congestion and improving regional air connectivity.

Read More

RUSSIA-UKRAINE WAR IMPACT

Advanced Air Mobility Demand has Disturbed Globally Due to Russia-Ukraine War

The Russia-Ukraine war significantly impacts the advanced air mobility (AAM) market, creating challenges and potential shifts. The most immediate consequence is supply chain disruption. AAM relies on critical materials such as titanium and aluminum, often sourced from Russia or Ukraine. The war's disruption increases costs, delays production, and potentially affects AAM solution affordability. Component sourcing from Eastern Europe is also impacted, causing further delays. Rising fuel prices exacerbate transportation costs for materials, adding to overall expenses.

Economic uncertainty is another significant factor. The war contributes to fears of a global recession, making investors more risk-averse, potentially reducing investment in long-term AAM projects. Reduced consumer spending could dampen initial demand for AAM services. Governments may also re-prioritize spending, shifting funds away from AAM development toward defense or social programs. The war can also impact key players and partnerships. AAM companies with ties to Russian or Ukrainian businesses may face disruptions due to sanctions or operational issues. Market access to Russia and Ukraine, while limited, could be restricted.

Geopolitical tensions increase scrutiny of AAM operations, potentially resulting in stricter regulations and heightened safety requirements. Managing airspace safely amidst increased military activity also presents a complex challenge. Sanctions and trade restrictions further limit access to certain technologies and materials. However, the war also presents some indirect opportunities. The crisis accelerates the global focus on energy security, potentially increasing investment in electric propulsion technologies crucial for AAM sustainability. The need for resilient supply chains could encourage building more localized and diversified networks for AAM components. The war also highlights potential military applications of AAM, potentially driving government funding toward related research and development.

In conclusion, the Russia-Ukraine war presents a complex mix of challenges and potential shifts for the AAM market. Navigating this uncertain environment requires companies to assess the risks and adapt their strategies accordingly and carefully.

ADVANCED AIR MOBILITY MARKET TRENDS

Emergence of Regional Air Mobility with Commercial Applications Drives Market Growth

While Urban Air Mobility (UAM) often dominates the headlines with visions of air taxis zipping between skyscrapers, a significant and increasingly important trend in the AAM market is the rise of Regional Air Mobility (RAM). RAM focuses on connecting smaller communities with regional hubs and even direct point-to-point transportation between smaller cities, offering a compelling alternative to traditional ground transportation for distances typically considered too short for conventional airlines but too long or inconvenient for driving.

Several factors fuel this trend. Firstly, RAM addresses a real need for improved connectivity in underserved regions. Many smaller towns and cities lack frequent or convenient access to major airports and economic centers, hindering economic development and limiting access to healthcare and other essential services. RAM offers the potential to bridge this gap, providing faster, more convenient, and often more affordable transportation options.

RAM aircraft designs are evolving to meet the specific demands of regional routes. This often translates to aircraft with longer ranges, greater passenger capacity compared to UAM concepts, and improved operational efficiency for longer flights. Hybrid-electric and even hydrogen-powered propulsion systems are gaining traction for RAM applications due to their potential for greater range and lower operating costs.

- North America witnessed advanced air mobility market growth from USD 3.35 Billion in 2023 to USD 3.92 Billion in 2024.

RAM benefits from a potentially less congested regulatory landscape than UAM in densely populated urban areas. Operating in less crowded airspace and utilizing existing regional airports or smaller landing strips can simplify regulatory approvals and accelerate deployment timelines. Furthermore, noise concerns, often a major hurdle for UAM acceptance, are typically less pronounced in rural and suburban environments.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Technological Advancements in Electric Propulsion and Autonomous Flight to Boost Market Growth

The advanced air mobility market growth is driven by the relentless pace of technological advancements in two key areas: electric propulsion and autonomous flight. Significant strides in battery technology, including increased energy density, faster charging times, and improved safety, are making electric vertical takeoff and landing (eVTOL) aircraft a viable and increasingly attractive option for short- to medium-range flights.

Simultaneously, advancements in autonomous flight systems, including sophisticated sensors, advanced algorithms, and robust control systems, are paving the way for safer and more efficient AAM operations. These technologies are converging to create aircraft that are not only environmentally friendly and cost-effective but also capable of operating with minimal human intervention, lowering operational costs and improving scalability. The continuous improvements in these core technologies are attracting significant investment and driving the development of innovative AAM solutions.

Growing Urban Congestion and Need for Efficient Transportation Alternatives to Drive Market Growth

The escalating problem of urban congestion in cities globally is a powerful driver fueling the demand for AAM. Traditional ground transportation systems are struggling to cope with increasing population and traffic volume, leading to longer commute times, increased pollution, and reduced productivity. AAM offers a compelling solution by providing a fast, efficient, and environmentally friendly alternative to congested roads and public transportation systems. By leveraging the vertical dimension, AAM can bypass ground-based traffic and offer direct point-to-point transportation, significantly reducing travel times and improving overall urban mobility. As cities continue to grow and congestion worsens, the need for innovative transportation solutions such as AAM will only intensify, further driving market growth.

MARKET RESTRAINTS

Stringent Regulatory and Certification Hurdles to Hamper Market Growth

A significant restraint hindering the widespread adoption of AAM lies in the complex and stringent regulatory and certification hurdles that must be overcome. Developing clear, comprehensive, and globally harmonized regulations for AAM aircraft, operations, and airspace management is a challenging and time-consuming process. Aviation regulatory bodies, including the FAA and EASA, are working to adapt existing regulations to accommodate the unique characteristics of eVTOL aircraft and other AAM technologies.

However, the process involves extensive testing, evaluation, and public consultation to ensure safety and security. Furthermore, securing type certification for new aircraft designs is a rigorous and costly process that can take several years. These hurdles can significantly delay the commercialization of AAM solutions and increase the financial risk for companies operating in this space. Until clear regulatory frameworks are established and streamlined certification processes are implemented, the AAM market will remain constrained by uncertainty and limited operational capabilities. Overcoming these challenges will require close collaboration between industry stakeholders, regulatory bodies, and government agencies to develop practical and effective regulations that balance innovation with safety.

MARKET OPPORTUNITIES

Leveraging Existing Aviation Infrastructure for Accelerated Market Entry Has Created Several Opportunities

A significant market opportunity for AAM lies in strategically leveraging existing aviation infrastructure, particularly regional airports and smaller general aviation airfields, to accelerate market entry and reduce initial capital expenditure. Instead of solely focusing on the development of entirely new vertiport networks, AAM companies can capitalize on the widespread availability of existing airports to establish operational hubs and passenger pick-up/drop-off points.

This approach offers several key advantages. Firstly, it significantly reduces the financial burden associated with building entirely new infrastructure from the ground up. Vertiports require substantial investments in land acquisition, construction, charging infrastructure, and air traffic management systems. By utilizing existing airports, AAM operators can minimize these upfront costs, allowing them to focus resources on aircraft development, certification, and operational scaling.

Leveraging existing infrastructure can streamline regulatory approvals and accelerate deployment timelines. Airports already have established safety protocols, air traffic control procedures, and regulatory frameworks in place. AAM operators can integrate their operations into these existing systems, simplifying the certification process and reducing the time required to obtain necessary permits.

Existing airports often have established ground transportation links, such as taxi services, public transportation, and parking facilities. This provides seamless connectivity for passengers transitioning to and from AAM flights, enhancing the overall convenience and accessibility of AAM services. Furthermore, airports often have existing security infrastructure and personnel, which can be leveraged to ensure the safety and security of AAM operations.

MARKET CHALLENGES

Concerns about Safety, Noise, and Privacy Challenge Market Growth

A critical challenge facing the AAM market is achieving widespread public acceptance and effectively addressing public concerns related to safety, noise pollution, and privacy. Unlike traditional aviation, AAM operations are envisioned to take place in close proximity to urban populations, increasing the potential for negative impacts and public scrutiny. Concerns about the safety of eVTOL aircraft, particularly in densely populated areas, need to be addressed through rigorous testing, robust safety protocols, and transparent communication.

Noise pollution from AAM aircraft is another significant concern, as the constant hum of electric motors or the whir of rotors could disrupt the peace of urban neighborhoods. Moreover, the potential for AAM aircraft to collect data and monitor individuals raises privacy concerns that need to be carefully managed through appropriate policies and technologies. Overcoming these challenges requires proactive engagement with communities, transparent communication about safety measures, and the development of quieter and more privacy-preserving AAM technologies. Building public trust and demonstrating the benefits of AAM will be essential for ensuring its long-term success and integration into urban environments.

SEGMENTATION ANALYSIS

By Component

High Demand for Specialized & High-Performance Hardware Fueled Segment Growth

By component, the market is bifurcated into hardware and software.

The hardware segment is projected to dominate the market with a share of 13.51% in 2026. This dominance is primarily due to the increasing demand for AAM hardware, including electric motors, batteries, sensors, rotor blades, and airframes, among others. Furthermore, innovations in battery design are projected to contribute to a reduction in the weight of AAM aircraft, enhancing their maneuverability. Similarly, the advent of lighter electric motors is anticipated to extend the flight range of AAM aircraft, thereby fostering segment growth.

Conversely, the software segment is expected to experience the highest CAGR during the forecast period. This growth is driven by continuous technological advancements, prompting AAM manufacturers to adopt sophisticated software solutions to ensure safe and efficient flight operations. Additionally, the rising integration of artificial intelligence and machine learning in software development is likely to elevate the demand for AAM software. The trend toward fully autonomous flight operations, utilizing cutting-edge software alongside modern technologies, is also expected to enhance the growth of this segment significantly.

By Product

Rotary Blade Segment Led Due to Its Distinctive Ability to Hover and Maneuver Adeptly

By product, the market is classified into fixed wing, rotary blade, and hybrid.

The rotary blade segment is projected to dominate the market with a share of 70.94% in 2026. The anticipated rise in demand for rotary blade AAM solutions is attributed to their distinctive ability to hover and maneuver adeptly while maintaining visual surveillance of specific targets for extended durations. Furthermore, AAM aircraft equipped with rotary blades can operate in compact and confined environments without special requirements for takeoff and landing, as they are capable of vertical takeoff and landing. Additionally, rotary blade AAM solutions provide superior control compared to hybrid and fixed-wing alternatives, which is expected to contribute to segment growth significantly.

The hybrid segment is projected to experience the highest CAGR throughout the forecast period. This growth is primarily due to the advantages offered by hybrid AAM solutions, which combine the features of both fixed-wing and rotary blades, enhancing their efficiency and practicality. Moreover, hybrid AAM aircraft can improve efficiency and power by utilizing both battery and fuel capabilities, allowing them to operate for extended periods while carrying heavier payloads, even under challenging weather conditions. This is anticipated to propel the growth of the segment.

By Propulsion Type

Electric Segment Dominated Owing to Sustainability, Cost Reduction, and Noise Minimization

Based on propulsion type, the market is classified into gasoline, electric, and hybrid.

The electric segment is projected to dominate the market with a share of 70.66% in 2026. This dominance is linked to the increasing popularity of electric AAM products that utilize rechargeable batteries. The segment has gained significant traction and widespread acceptance owing to numerous benefits, including operations powered by rechargeable batteries, a safer flying environment, quieter operations, improved flight efficiency, extended flight durations, and ease of maintenance. These factors are expected to stimulate growth in this segment during the forecast period.

The hybrid segment is projected to experience the highest compound annual growth rate (CAGR) from 2025 to 2032. This growth is primarily due to AAM solutions that employ a mix of various power sources for propulsion. Typically, this segment integrates an electric motor with an additional power source, such as a combustion engine or fuel cell, to deliver a cost-efficient power and flight solution. Consequently, this leads to enhanced flight performance and greater operational efficiency, which is anticipated to propel segment growth throughout the forecast period.

By Application

Cargo Transport Segment Led Market by Supply Chain Efficiency

Based on application, the market is segregated into cargo transport, passenger transport, mapping & surveying, special mission, surveillance & monitoring, and others.

In 2024, the cargo transport segment represented the largest revenue share. This segment's prominence is due to its ability to provide rapid and efficient delivery of goods directly to customers' residences. The increasing trend of one-day deliveries, frequently offered by e-commerce platforms, is propelling the adoption of AAM solutions in cargo transport. Furthermore, businesses are leveraging AAM solutions to alleviate warehousing constraints and improve supply chain efficiency.

Meanwhile, the surveillance & monitoring segment is projected to experience the highest CAGR during the forecast period. This growth is driven by applications in monitoring, surveillance, and security, particularly in areas with elevated crime rates. AAM solutions, including autonomous drones, are extensively utilized in search and rescue operations, particularly for inspecting high infrastructure that may have compromised electrical wiring and unstable roofs in hazardous and hard-to-reach locations. These drones are equipped with advanced high-resolution cameras and sensors to facilitate effective surveillance and monitoring activities.

To know how our report can help streamline your business, Speak to Analyst

By End-Use

Rising Trend of Aerial Deliveries by E-commerce Companies Boosted Commercial Segment Expansion

Based on end-use, the market is bifurcated into commercial and government & military

The Commercial segment is projected to dominate the market with a share of 73.88% in 2026. The increasing trend of aerial deliveries by e-commerce companies is projected to enhance the demand for commercial applications of AAM solutions. For example, in May 2023, Amazon.com, Inc. completed one hundred cargo aerial deliveries through its Prime Air division. Likewise, the emergence of passenger AAM aircraft fleets for transportation services by private enterprises is expected to stimulate growth in this segment further.

The government and military sector is anticipated to experience a notable compound annual growth rate (CAGR) throughout the forecast period. This growth is primarily driven by the expanding applications of AAM solutions, which encompass firefighting and disaster management, search and rescue operations, maritime security, border patrol, police activities, and traffic monitoring, among others. AAM aircraft enable law enforcement and emergency personnel to respond swiftly and facilitate safe evacuation processes, thereby contributing to market expansion. Furthermore, the increasing complexity of rescue and emergency operations has led to a greater deployment of AAM solutions, as they provide enhanced safety and timely response capabilities.

ADVANCED AIR MOBILITY MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Advanced Air Mobility Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 4.53 billion in 2025, representing 34.12% of total market revenue, and is projected to reach USD 5.61 billion in 2026. The U.S., in particular, is witnessing intense activity in eVTOL aircraft development, regulatory framework creation (led by the FAA), and infrastructure planning. Companies, including Joby Aviation and Archer Aviation, are at the forefront, aiming for commercial operations within the next few years. Canada is also emerging as a key player, focusing on regional connectivity and leveraging its expertise in aerospace. Key challenges include navigating complex regulatory pathways, securing public acceptance, and developing robust air traffic management systems. The U.S. market is projected to reach USD 5.16 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 4.03 billion, representing 30.39% of global demand, and is projected to grow to USD 5.09 billion in 2026. The Asia Pacific region presents a dynamic AAM market with diverse opportunities and challenges. China is a major player, driven by government support for technological innovation and rapid urbanization. Companies, including EHang, are focusing on autonomous aerial vehicles for various applications. South Korea and Japan are also actively investing in AAM, aiming to alleviate traffic congestion and improve regional connectivity. Key challenges include navigating complex regulatory landscapes, securing airspace access, and addressing public concerns about noise and safety. The region's diverse geography and varying levels of infrastructure development require tailored AAM solutions. The Japan market is projected to reach USD 0.7 billion by 2026, the China market is projected to reach USD 1.74 billion by 2026, and the India market is projected to reach USD 1.07 billion by 2026.

Europe

Europe contributed approximately USD 3.13 billion to the global market in 2025, accounting for 23.57% share, and is expected to reach USD 3.9 billion in 2026. Europe is rapidly advancing in the AAM sector, characterized by strong government support for green technologies and a focus on sustainable transportation solutions. Germany, France, and the U.K. are leading the charge with companies including Lilium and Vertical Aerospace developing innovative eVTOL aircraft. The European Union Aviation Safety Agency (EASA) is actively working on harmonized regulations to enable cross-border AAM operations. Challenges include balancing ambitious sustainability goals with safety requirements, securing funding for infrastructure development, and integrating AAM into existing urban environments. Collaboration between industry, government, and academia is crucial for the European market's success. The UK market is projected to reach USD 0.84 billion by 2026, while the Germany market is projected to reach USD 0.61 billion by 2026.

Rest of the World

The AAM market in the Rest of the World is in its nascent stages but holds significant potential. Regions, including the Middle East and Latin America, are exploring AAM as a solution to address transportation challenges and improve connectivity. UAE, particularly Dubai, is actively pursuing AAM initiatives, focusing on air taxi services and smart city development. Brazil also presents opportunities, leveraging Embraer's expertise and addressing the need for regional connectivity. Key challenges include attracting investment, establishing regulatory frameworks, and adapting AAM solutions to local contexts. Collaboration with international AAM leaders will be crucial for driving growth in these emerging markets.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Partnerships and Strategic Acquisitions to Boost Market Growth

The advanced air mobility market is a rapidly evolving ecosystem spearheaded by a diverse set of players ranging from established aerospace giants to agile startups. Airbus and Boeing, leveraging their decades of aviation expertise, are exploring AAM through partnerships, internal R&D, and strategic acquisitions, aiming to integrate AAM into their existing portfolio. Bell Textron, with its long history in rotorcraft, is developing innovative VTOL concepts. Embraer, through its Eve Urban Air Mobility Solutions subsidiary, is actively designing eVTOL aircraft and developing related infrastructure.

Pure-play AAM companies are driving innovation. Joby Aviation, a leading eVTOL developer, is focused on building a commercially viable air taxi service. Aurora Flight Sciences, a Boeing subsidiary, contributes advanced autonomy and aircraft design expertise.

LIST OF KEY ADVANCED AIR MOBILITY COMPANIES PROFILED

- Airbus S.A.S. (France)

- Aurora Flight Sciences (U.S.)

- Bell Textron Inc. (U.S.)

- The Boeing Company (U.S.)

- Guangzhou EHang Intelligent Technology Co., Ltd. (China)

- Embraer S.A. (Brazil)

- Joby Aviation (U.S.)

- Lilium GmbH (Germany)

- Neva Aerospace (U.K.)

- Opener, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2025 - Wisk Aero, a prominent AAM company pioneering the first U.S. all-electric, self-flying air taxi, has secured a new five-year partnership with NASA through a Non-Reimbursable Space Act Agreement (NRSAA). The agreement supports NASA's Air Traffic Management Exploration (ATM-X) project, concentrating on vital research to enable autonomous aircraft operation under Instrument Flight Rules (IFR) within the National Airspace System (NAS).

- January 2025 - Tata Elxsi, an Indian technology firm, and CSIR-National Aerospace Laboratories (CSIR-NAL) in India partnered through a Memorandum of Understanding (MoU) to advance the AAM field. According to a joint statement, the strategic alliance will concentrate on pioneering developments in Unmanned Aerial Vehicles (UAVs), Urban Air Mobility (UAM), and electric vertical takeoff and landing (eVTOL) aircraft.

- June 2024 - Airbus and Avincis, a leading European helicopter services provider, signed a Memorandum of Understanding (MoU) to advance Advanced Air Mobility (AAM) jointly. The partnership will focus on identifying potential operational opportunities for electric vertical takeoff and landing (eVTOL) aircraft across the European continent.

- February 2024 - Airbus and LCI, a prominent aviation firm, forged a partnership to cultivate ecosystems for Advanced Air Mobility (AAM). The collaboration will center on crafting joint venture opportunities and financial frameworks within three key aspects of AAM: strategic planning, market introduction, and investment strategies.

- October 2023 - The Federal Aviation Administration (FAA) announced a partnership with the U.S. Air Force on October 26 to work together on safely integrating Advanced Air Mobility (AAM) aircraft into the existing National Airspace System.

REPORT COVERAGE

This advanced air mobility market research report offers a comprehensive market analysis, identifying key players, product categories, and primary applications. It also details market trends and significant industry developments. Moreover, the report highlights various factors that have fueled the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 23.10% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Product

|

|

|

By Propulsion Type

|

|

|

By Application

|

|

|

By End-Use

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 13.27 billion in 2025 and is estimated to reach USD 87.00 billion by 2034.

The market will grow steadily at a CAGR of 23.10% during the projection period.

By product, the rotary blade segment led the market.

Airbus S.A.S. (France), Aurora Flight Sciences (U.S.), Bell Textron Inc. (U.S.), The Boeing Company (U.S.), and Guangzhou EHang Intelligent Technology Co., Ltd. (China) are some of the leading players in the market.

North America holds the highest market share.

- 2021-2034

- 2025

- 2021-2024

- 250

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us