Aerospace Cybersecurity Market Size, Share & Industry Analysis, By Deployment (On-premises and Cloud), By Security Type (Network Security, Application Security, Endpoint Security, Cloud Security, and Data Security), By End User (Airlines, Aerospace Manufacturers, Aircraft Operators, and Government & Defense), and Regional Forecast, 2026-2034

Aerospace Cybersecurity Market Size and Future Outlook

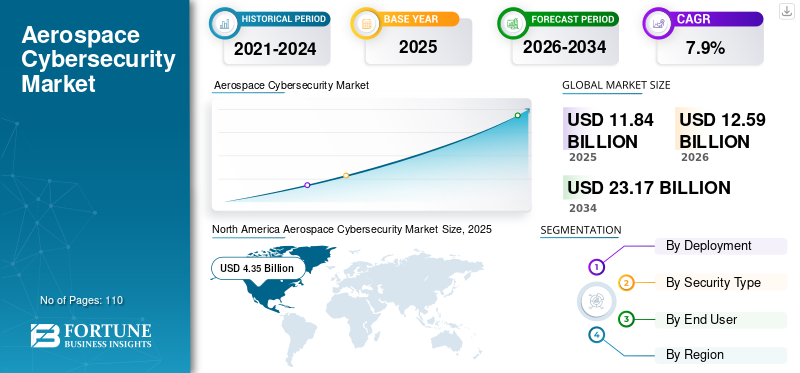

The global aerospace cybersecurity market size was valued at USD 11.84 billion in 2025. The market is projected to grow from USD 12.59 billion in 2026 to USD 23.17 billion by 2034, exhibiting a CAGR of 7.9% during the forecast period. North America dominated the aerospace cybersecurity market with a market share of 36.73% in 2025.

Aerospace cybersecurity involves protecting digital systems, networks, software, and data used across aviation, defense, and space operations. The purpose of securing these areas is to prevent cyber threats and operational disruptions to aircraft, satellites, land-based infrastructure, mission-critical communication systems, and others. As digitalization of the above-mentioned categories increases and greater connectivity exists between these systems, the potential for cybercrime (the attack surface) also increases. Organizations are becoming more dependent upon real-time information, cloud-based platforms, and other secure communications, therefore driving up demand for more sophisticated and advanced cybersecurity solutions. This factor plays an important role in fueling the market growth.

Furthermore, many key industry players, such as Thales Group, Honeywell International, Airbus, BAE Systems, and Lockheed Martin, operating in the market, are focusing on integrated, end-to-end security architectures by bundling cybersecurity with avionics, mission systems, ground infrastructure, and managed services to provide a single accountable solution for operators.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Rising Adoption of Generative AI in Aerospace Operations Driving Advanced Cybersecurity Investments

The use of generative AI is changing the landscape in aerospace with regard to security. Generative AI can create new and scalable ways to commit crimes such as phishing and social engineering, and it can quickly develop malware. Security teams can leverage generative AI to improve defensive operations by speeding up the triage of incidents, creating playbooks, correlating telemetry between operational technology (OT) and information technologies (IT), and reducing the workload on analysts.

- In May 2025, Thales reported 73% of organizations are investing in AI-specific security tools, highlighting the shift toward securing GenAI usage and data pipelines.

Finally, the acceleration of digital workflow processes (maintenance, engineering, and mission analytics) as a result of the use of generative AI will create a higher demand for organizations in aerospace to have proper cybersecurity measures as these processes deal with regulated and safety-critical data.

AEROSPACE CYBERSECURITY MARKET TRENDS

Growing Cyber Threats and Skill Gaps Driving SOC Outsourcing in Aerospace

With an increasing demand for managed security services and Security Operations Center (SOC) outsourcing in the aviation industry, organizations such as airlines, airports, maintenance, repair, and operations (MROs), and defense-related operators require 24/7 security monitoring but have a continuing challenge of hiring qualified security analysts. Outsourced SOCs provide organizations with the ability to more quickly identify threats in complex, distributed environments such as terminals, baggage systems, aircraft connectivity, as well as at remote locations without requiring them to develop a large in-house security team.

The use of an outsourced SOC also helps standardize compliance, incident response, and vulnerability management across multiple locations and/or vendors. The demand for SOC services is further driven by organizations that are expanding their use of cloud-based services and connected operations as the pace of growth creates an increased need for security telemetry and response that can scale in real-time.

- For example, in April 2025, 66% of airlines and 73% of airports ranked cybersecurity among their top three focus areas, reinforcing why many shift to managed security and SOC-led models.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Cyber Threats Targeting Aviation Drives Market Growth

The aerospace cybersecurity market growth is being driven by increasing threats of cybercrime aimed at airlines, airports, and aerospace operators that depend on inter-connected systems that are unable to have any type of downtime from their systems. This includes check-in/boarding systems, flight operations and maintenance networks, and others, which are the target of increasing attacks by criminals using ransomware, theft of credentials and compromise to the supply chain, where a breach within a system can impact the ability to operate thousands of flights worldwide and expose large amounts of sensitive data related to the operation of the airline and the passenger's journey, both in terms of operational and mission-related data.

As such, the aviation industry has been investing in increasing levels of investment in many areas including continuous monitoring, identity security, network segmentation, incident response services and increasing the number of people within their organization dedicated to these functions due to the fact that many aviation ecosystems share a number of vendors or platforms therefore if there is a vulnerability from one vendor to another vendor, the ability to operate will be impacted.

- In June 2025, Thales reported the aviation sector saw a 600% year-on-year increase in cyberattacks, citing 27 major attacks by 22 ransomware groups from January 2024 to April 2025.

MARKET RESTRAINTS

High Integration and Compliance Cost May Hinder Market Growth

The high level of integration and cost of compliance acts as a barrier to growth in the aviation cybersecurity marketplace, as the required cybersecurity controls have to be implemented over a highly fragmented environment, such as aircraft connectivity, airport OT systems, airline enterprise IT, and multiple third-party service providers. Each upgrade within this complex cyber environment generally requires significant validation, documentation, and alignment with both operationally safe and operationally continuous requirements, all of which add to the increased engineering and program management cost and effort required to implement those upgrades. The cost to implement compliance also continues to occur on an ongoing basis as organizations need to perform governance/audits/incident reporting/the risk management process, in addition to the purchase of tools. These factors will generally lengthen the time it takes operators to adopt the required upgrades to their systems and force many operators to only deploy the most at-risk systems first.

MARKET OPPORTUNITIES

Accelerating ATM and Airport OT Modernization Creating New Cybersecurity Growth Opportunities

The modernization of Air Traffic Management (ATM) and airport operational technology (OT) systems provides an opportunity due to increased connectivity that leads to exposure in cyberspace. Airports must digitize Operationally Technology (OT) heavy environments where if there were a failure in these systems would impact the safety and continuity of business functions such as baggage handling, access control, building management and airfield operations. As systems are being modernized they require OT aware security controls including segmentation, continuous monitoring, secure identification and incident response that are non-disruptive to operations. In addition, many of today’s modern ATM systems emphasize secure data sharing and connectivity with elements of Cybersecurity included in the requirements for procurement of an architecture that was designed and certified for security.

- For example, in April 2025, the Air Traffic Control Association (ATCA) supported a proposed USD 15 billion investment aimed at U.S. air traffic control modernization and infrastructure improvement, reinforcing the scale of modernization programs that require cybersecurity hardening.

Segmentation Analysis

By Deployment

Strict Safety and Classified Data Requirements Sustaining Dominance of On-Premises in Market

Based on the deployment, the market is divided into on-premises and cloud.

On-premises are anticipated to account for the largest market share. This is owing to a large number of aerospace & defense systems operating in a governed environment with safety-critical systems, as well as having classified systems, with the requirement to have physical isolation and control over the data. Also, organizations prefer on-premises infrastructure to maintain tighter control over mission systems, avionics networks, and sensitive operational data while complying with strict certification and security requirements.

Cloud is anticipated to grow at the highest CAGR of 10.6% over the forecast period. This is owing to airlines, airports, and aerospace manufacturers accelerate digital transformation, adopting scalable cloud platforms to support real time analytics, remote operations, and integrated security monitoring across distributed environments.

By Security Type

Growing Network-Based Threats Driving Dominance of Network Security in Market

Based on security type, the market is categorized into network security, application security, endpoint security, cloud security, and data security.

Network security is anticipated to witness a dominating market share in 2025. This is due to the reliance of aerospace on interconnected systems (aircraft-to-ground communications, satellite links, air traffic networks, and defense command infrastructures) where there are a continuous need for perimeter protection and internal network protection. Ransomware and intrusions are growing in frequency and attacking networks through various means (e.g., signal based) and have created urgency for organizations to implement foundational security controls such as firewalls, intrusion detection devices, secure gateways and network segmentation.

Cloud security is projected to grow at the highest CAGR of 12.4% over the forecast period. This is due to aerospace organizations increasingly migrating mission support systems, analytics platforms, and collaborative environments to cloud infrastructures, requiring advanced protection for distributed workloads and sensitive data.

By End User

Rising Digital Dependency and Threat Exposure Driving Airlines’ Dominance in Aviation Cybersecurity Spending

Based on the end user, the market is classified into airlines, aerospace manufacturers, aircraft operators, and government & defense.

Airlines are anticipated to witness a dominating market share in 2025. This is due to the reason that they operate highly connected digital ecosystems spanning reservations, flight operations, maintenance systems, crew management, and passenger services, all of which require continuous cybersecurity protection. The rising frequency of ransomware and data breach incidents targeting airline IT infrastructure has further accelerated investment in network security, identity management, and real-time threat monitoring.

Aerospace manufacturers are anticipated to grow at the highest CAGR of 10.1% during the forecast period. As they increasingly securing digital engineering platforms, connected production systems, and complex global supply chains against rising cyber and intellectual property risks.

To know how our report can help streamline your business, Speak to Analyst

Aerospace Cybersecurity Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

North America

North America held the largest aerospace cybersecurity market share in 2024, valuing at USD 4.16 billion, and also maintained the leading share in 2025, with USD 4.35 billion. The market in North America is expected to increase, owing to its strong concentration of major aerospace OEMs, defense contractors, airlines, and space agencies with high cybersecurity budgets. In addition to this, the region has also been the leader in both defense modernization programs, as well as having the most stringent regulations, which continually creates an opportunity for ongoing capital investments in advanced cyber protection globally across both aviation systems and military systems.

- For example, in January 2026, the US Air Force awarded General Dynamics Information Technology (GDIT) a contract to deploy a zero-trust security solution across nearly 200 bases, reinforcing sustained cyber modernization spend tied to defense aviation infrastructure.

These factors play a significant role in fueling the market growth.

North America Aerospace Cybersecurity Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

U.S. Aerospace Cybersecurity Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.74 billion in 2026, accounting for roughly 29.7% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is projected to record a growth rate of 6.9% in the coming years, which is the second highest among all regions, and reach a valuation of USD 2.76 billion by 2026. Regulatory agencies such as NIS2 directive and EASA are creating new, more demanding cyber safety regulatory requirements for aviation and aerospace companies around the world, creating opportunities in both aerospace and defense market segments. As we witness national defense budgets increase, while large-scale satellite systems are being developed to support commercial businesses (i.e., NASA), there is a growing demand for secure communication systems as well as protection for data.

- In June 2025, Thales and Palantir Technologies expanded their partnership to provide cybersecurity solutions for the European Space Surveillance and Tracking program, a key component of Europe’s growing space resilience needs

U.K. Aerospace Cybersecurity Market

The U.K. market in 2026 is estimated at around USD 0.54 billion, representing roughly 4.3% of global revenues.

Germany Aerospace Cybersecurity Market

Germany’s market is projected to reach approximately USD 0.51 billion in 2026, equivalent to around 4.1% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 3.78 billion in 2026 and expected to grow at the highest CAGR during the forecast period. This is owing to increased air travel and defense modernization in countries such as China, India, and Japan, which are heavily investing in securing their aviation and defense sectors. Additionally, expanding satellite constellations and space programs in the region are driving the demand for secure communication and data protection solutions to support space missions and satellite connectivity.

- In December 2025, Noida International Airport partnered with Tech Mahindra to establish and operate an integrated Network and Security Operations Centre (NOC-SOC) with continuous monitoring for critical airport IT and digital platforms.

In the region, India and China are both estimated to reach USD 0.51 billion and USD 0.88 billion, respectively, in 2026.

Japan Aerospace Cybersecurity Market

The Japan market in 2026 is estimated at around USD 0.71 billion, accounting for roughly 5.6% of global revenues. This is owing to increase in military spending and national defense initiatives that require a greater emphasis put on securing military aviation assets, satellite systems and critical infrastructure. Furthermore, as part of an overall commitment to space exploration and satellite communication, along with a rapidly expanding aviation sector, Japan has an increasing demand for advanced cyber security solutions. These solutions are needed to secure its own sensitive data and communication channels of its own.

China Aerospace Cybersecurity Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.88 billion, representing roughly 7.0% of global sales.

India Aerospace Cybersecurity Market

The Indian market size in 2026 is estimated at around USD 0.51 billion, accounting for roughly 4.1% of global revenues.

South America

South America is expected to witness moderate growth in this market space during the forecast period. The South America market is set to reach a valuation of USD 0.65 billion in 2026. This is owing to increased government and defense spending, with several countries modernizing their aviation and defense sectors to bolster national security. Furthermore, there has also been an increase in air travel, coupled with the addition of new infrastructure that will require further investment in cyber security solutions to protect critical aviation systems and communications. There is also an increase in the volume that targets these systems and networks from cyber-attacks.

Middle East and Africa

The Middle East and Africa is estimated to reach USD 0.83 billion in 2026 and expected to grow at a prominent growth rate in the coming years. This is owing to modernization, defense investments, and the growth of the wider aerospace industry in the region, such as the increase in air travel and military aviation. Moreover, the need for adequate cyber defense against possible threats to critical infrastructure such as airports, air traffic control systems, and satellite communications will create an increase in demand for these market segments. In the Middle East & Africa, the GCC is set to reach a value of USD 0.25 billion in 2026. For instance,

- In May 2025, Saudi Arabia allocated $5 billion for cybersecurity enhancements in the defense sector, part of its Vision 2030 plan, to ensure the protection of aerospace systems and infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Portfolio by Key Players to Propel Market Progress

The global aerospace cybersecurity market holds a semi-consolidated market structure, constituting prominent players such as Thales Group, Honeywell (Aerospace), Airbus, BAE Systems, and Lockheed Martin holding significant positions. These companies are driving market growth through continuous strategic initiatives, including the integration of secure satellite communication services, expansion of defense-oriented IoT security solutions, and advanced data analytics platforms. Partnerships with telecom operators, cloud service providers, and infrastructure developers are crucial in this expansion, particularly for securing communication networks and mission-critical systems. For instance,

- In October 2025, Boeing announced the launch of a cybersecurity-as-a-service platform for commercial airlines, designed to protect both onboard communication systems and ground-based operations from emerging threats.

Other notable players in the global market include Northrop Grumman, Boeing, L3Harris, RTX (Collins Aerospace), and Leonardo. These companies are expected to increase focus on next-generation satellite communication security, space-based cybersecurity solutions, and long-term support for mission-critical systems to reinforce their market positioning and expand their global presence throughout the forecast period.

LIST OF KEY AEROSPACE CYBERSECURITY COMPANIES PROFILED

- Thales Group (France)

- Honeywell (Aerospace) (U.S.)

- Airbus (Netherlands)

- BAE Systems (U.K.)

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- Boeing (U.S.)

- L3Harris (U.S.)

- RTX (Collins Aerospace) (U.S.)

- Leonardo(Italy)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Boeing Defense, Space & Security, and Palantir announced a partnership to expand AI adoption across defense and classified programs, increasing the need for secured data environments and cyber-resilient architectures around AI-enabled operations.

- June 2025: Honeywell unveiled its new aerospace cybersecurity services, offering managed security solutions for aircraft and ground operations, aimed at real-time cyber threat monitoring and aviation infrastructure resilience.

- May 2025: Leidos acquired Kudu Dynamics, a provider of advanced cybersecurity solutions for USD 300 million. This acquisition strengthens Leidos' portfolio in aerospace and defense cybersecurity, enhancing its capabilities in securing mission-critical systems and data for government and commercial clients.

- April 2025: Thales launched a new cybersecurity platform tailored for aerospace and defense, integrating AI-driven threat detection and secure satellite communications for global aviation.

- March 2025: Lockheed Martin and Google Cloud announced a collaboration to integrate Google’s GenAI into Lockheed’s AI Factory ecosystem for national security and aerospace use cases, reinforcing demand for high-assurance AI deployment and security.

- January 2025: SITA partnered with Palo Alto Networks to enhance aviation cybersecurity, with SITA running management and operations through its CyberSOC as part of a managed security service edge offering.

- November 2024: GE Aerospace, Microsoft, and Accenture unveiled a generative AI-powered solution to help airlines and lessors access maintenance records much faster, showing how GenAI is being embedded into aviation workflows that require strong data security controls.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.9% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Deployment, Security Type, End User, and Region |

|

By Deployment |

|

|

By Security Type |

|

|

By End User |

|

|

By Region |

North America (By Deployment, Security Type, End User, and Country)

South America (By Deployment, Security Type, End User, and Country)

Europe (By Deployment, Security Type, End User, and Country)

Middle East & Africa (By Deployment, Security Type, End User, and Country)

Asia Pacific (By Deployment, Security Type, End User, and Country)

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.84 billion in 2025 and is projected to reach USD 23.17 billion by 2034.

In 2025, the market value stood at USD 4.35 billion.

The market is growing at a CAGR of 7.9% during the forecast period.

By end user, the airlines segment is expected to lead the market.

The increasing cyber threats targeting aviation drive the market growth.

Thales Group, Honeywell (Aerospace), Airbus, BAE Systems, and Lockheed Martin are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us