Space Cybersecurity Market Size, Share & Industry Analysis, By Offering (Solution and Services), By Platform (Satellite, Launch Vehicles, Ground Stations, Spaceports & Launch Facilities, and Others), By End User (Government, Commercial, and Defense), and Regional Forecast, 2026–2034

KEY MARKET INSIGHTS

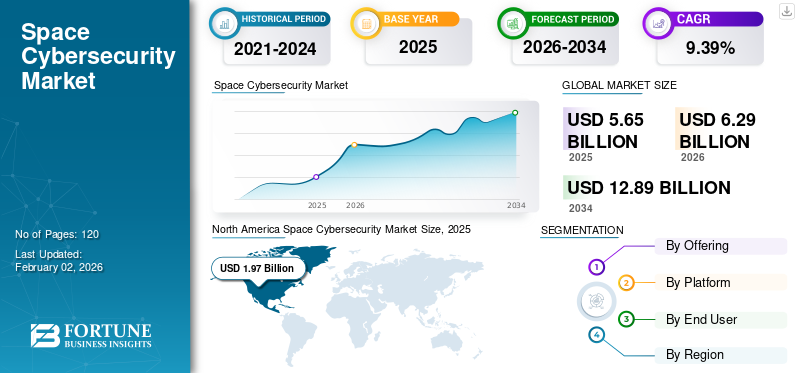

The global space cybersecurity market size was valued at USD 5.65 billion in 2025 and is projected to grow from USD 6.29 billion in 2026 to USD 12.89 billion by 2034, exhibiting a CAGR of 9.39% during the forecast period. North America dominated the space cybersecurity market with a market share of 34.97% in 2025.

Space cybersecurity is a process of protecting the systems, assets, and operations in the space domain from cyber threats. The goal is to ensure confidentiality, integrity, and availability of space-based services and assets, as well as resilience and recoverability in the face of cyber incidents. The number of satellites, small satellites, mega-constellations, ground stations, launch facilities, and associated links is growing rapidly across the globe. This factor plays a crucial role in driving the market's growth.

Integration of advanced technologies such as AI, ML for anomaly detection, software‑defined satellites, inter‑satellite links, and cloud infrastructure for the ground-based segment increases both capabilities and vulnerability. As these systems evolve, legacy systems become increasingly vulnerable, supply‑chain issues matter more, and security must keep pace. This factor is further driving market growth worldwide.

The market is dominated by established key players, such as Thales Group, Airbus Defence and Space GmbH, Northrop Grumman, Lockheed Martin, and Boeing. These players are continuously engaged in forming collaborations with satellite operators, ground‑station providers, and national space agencies to offer integrated cybersecurity suites. This allows them to embed services deeper into the space value chain and lock in long‑term contracts.

Download Free sample to learn more about this report.

Space Cybersecurity Market Key Takeaways

- 2025 Market Size: USD 5.65 billion

- 2026 Market Size: USD 6.29 billion

- 2034 Forecast Market Size: USD 12.89 billion

- CAGR: 9.39% from 2026-2034

- North America dominated the space cybersecurity market with a 34.97% share in 2025.

- The solution segment accounted for a 57.39% share in 2026.

- The satellite segment held a 32.74% share in 2026.

North America

North America reached USD 1.97 billion in 2025 and is projected to grow to USD 2.18 billion in 2026.

Asia Pacific

Asia Pacific stood at USD 1.56 billion in 2025 and is expected to reach USD 1.75 billion in 2026.

Europe

Europe accounted for USD 1.56 billion in 2025 and is projected to grow to USD 1.74 billion in 2026.

U.S.

The market is estimated to reach USD 1.29 billion in 2026.

Japan

The market is projected to reach USD 0.28 billion in 2026.

Read More

IMPACT OF GENERATIVE AI

Rising Adoption of Generative AI in Space Cybersecurity Boosts Market Efficiency

Generative AI is significantly influencing the market by enhancing both the capabilities and risks associated with space-based systems. It enables more advanced threat detection and anomaly analysis, as artificial intelligence (AI) models can analyze large datasets from satellites and ground stations to identify subtle patterns or potential breaches that traditional methods may overlook.

Additionally, it allows for increased operational efficiency through automation, including the generation of cybersecurity policies, incident response scripts, and training simulations. For instance,

- In March 2025, Lockheed Martin Corporation and Google Cloud announced a collaboration to integrate Google’s generative AI technologies into Lockheed Martin’s “AI Factory” ecosystem, aiming to enhance AI‑driven capabilities in aerospace, including secure operations in critical aerospace and defense‑adjacent domains.

MARKET DYNAMICS

Market Drivers

Increasing Cyber Threats and the Critical Dependence on Space Systems Driving Cybersecurity Demand

The growing threat of the space environment and the increasing mission-critical reliance on space systems are significant driving factors for the market. As space assets, such as satellites used for communication, navigation, and Earth observation, become increasingly vital to national security, economy, and everyday services, any disruption or compromise can have far-is projected to reach consequences. The rise in cyber threats, including hacking, jamming, spoofing, and malware attacks targeting these systems, has heightened the need for specialized cybersecurity measures. Additionally, the complexity and high value of space systems make them prime targets for state-sponsored actors and other adversaries, further elevating the urgency of securing these assets. This evolving threat landscape, combined with the increasing reliance on space infrastructure, creates a growing demand for robust cybersecurity solutions to protect space-based systems and ensure their operational integrity. Thereby, increasing the space cybersecurity market growth. For instance,

- In October 2025, Firefly Aerospace announced its strategic acquisition of SciTec for approximately USD 855 million, aiming to bolster its national‑security and space‑cyber capabilities.

Market Restraints

Complexity and Cost of Developing Space‑Specific Cybersecurity Technologies May Hinder Market Growth

The complexity and cost of developing space-specific cybersecurity technologies are significant restraints for the market, as space systems have unique operational and environmental constraints. Satellites and space assets often operate in harsh conditions, such as extreme radiation and limited computational resources, which require specialized, lightweight, and energy-efficient security solutions. Developing these space-grade cybersecurity technologies, such as secure communication links, on-orbit monitoring tools, and encryption mechanisms, is both technically challenging and costly. Additionally, the need for continuous innovation to counter evolving cyber threats in space further increases the financial and technical barriers, limiting the speed at which security solutions can be adopted across the industry.

Market Opportunities

Rising Space Activities in Asia-Pacific and the Middle East Creating Opportunities for Cybersecurity Providers

Emerging regions such as the Asia-Pacific and the Middle East are increasingly investing in space infrastructure, presenting significant opportunities for the market. Countries in these regions are ramping up their satellite launch capabilities, developing new spaceports, and expanding their commercial space activities, driving the need for robust cybersecurity solutions to protect critical space assets. As these regions continue to establish and grow their space programs, there is a rising demand for cybersecurity to safeguard against the unique threats associated with space operations, including satellite hacking and data breaches. Moreover, the evolving regulatory landscape in these regions is pushing for stricter cybersecurity compliance, creating further opportunities for vendors to offer tailored solutions. The combination of regional growth, regulatory advancements, and increasing reliance on space makes the Asia-Pacific and Middle East markets ripe for cybersecurity providers looking to expand their reach. For instance,

- In May 2025, Resecurity and Starlink announced a strategic partnership at GISEC Global 2025 to jointly enhance cybersecurity for satellite internet and space‑based communications networks.

Space Cybersecurity Market Trends

Rise of Commercial Space and the Expansion of the Private Sector are Fueling the Market Growth

The commercialization of space and the expansion of the private sector are significant drivers of growth in the market. More private companies are entering the space industry, including satellite operators, launch providers, and satellite-based internet services. The demand for cybersecurity solutions tailored to these commercial operations has surged. These new entrants often face unique security challenges compared to traditional government and defense entities, as they typically operate with fewer resources and less stringent security protocols. This creates an opportunity for cybersecurity providers to offer scalable, flexible, and cost-effective solutions that are tailored to the needs of commercial space ventures. Furthermore, the increased competition and rapid deployment of space infrastructure, such as mega‑constellations, further amplify the need for secure, resilient systems to safeguard critical commercial space assets and data. For instance,

- In November 2024, Space ISAC and iLAuNCH Trailblazer announced a partnership to enhance space industry cybersecurity by creating an Australia Global Hub for intelligence‑sharing and resilience in space operations.

SEGMENTATION ANALYSIS

By Offering

Growing Demand for Advanced Protection Solution Drives Dominance of the Segment

Based on offering, the market is bifurcated into solutions and services.

The solution segment is projected to dominate the space cybersecurity market, accounting for 57.39% of the global market share in 2026. This is due to the increasing demand for advanced, comprehensive cybersecurity measures to protect space assets, including satellites, ground stations, and communication links. The growing sophistication of cyber threats targeting space systems, combined with the need for robust protection mechanisms, led organizations to prioritize investing in integrated software and hardware solutions that can offer real-time monitoring, encryption, and threat detection capabilities.

Services are anticipated to grow at the highest CAGR of 12.3% during the forecast period, driven by increasing demand for managed security services, incident response, and specialized cybersecurity expertise as space operators seek to outsource complex security operations amid evolving cyber threats.

By Platform

Increased Reliance on Satellites and Rising Cyber Threats Propel Their Dominance in the Market

Based on platform, the market is divided into satellite launch vehicles, ground stations, spaceports & launch facilities, and others (command & control center, etc.).

Satellite segment is expected to lead by platform, contributing 32.74% globally in 2026. This is due to the critical role satellites play in global communications, navigation, and earth observation, making them prime targets for cyberattacks. As a result, there is a heightened need for robust cybersecurity measures to safeguard satellite operations from sophisticated threats such as hacking, jamming, and spoofing.

Spaceports & launch facilities are expected to grow at the highest CAGR of 13.9% during the forecast period. This is due to the increasing frequency of space missions, the expansion of commercial space activities, and the need to secure critical infrastructure involved in satellite launches and operations.

By End User

To know how our report can help streamline your business, Speak to Analyst

Government’s Need to Secure Space Assets Results in Capturing the Largest Share in the Market

Based on end user, the market is categorized into government, commercial, and defense.

Government accounted for the largest market share of USD 3.14 billion in 2025, owing to the strategic importance of space assets for national security, defense, and critical satellite communications. Governments invest heavily in securing space systems to protect sensitive data, military operations, and infrastructure from cyber threats, making them the largest and most consistent buyers of cybersecurity solutions.

Commercial is projected to grow at the highest CAGR of 14.1% during the forecast period, owing to the rapid expansion of satellite-based services, such as satellite internet and communications, and the increasing demand for secure, scalable solutions to protect these growing infrastructures.

SPACE CYBERSECURITY MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Space Cybersecurity Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 1.97 billion in 2025, representing 34.97% of total market revenue, and is projected to reach USD 2.18 billion in 2026. The factors behind the regional growth include the strong presence of government agencies such as NASA and the U.S. Department of Defense, which prioritize the protection of space assets. Additionally, North America's leadership in space innovation, with major commercial players such as SpaceX and Blue Origin, drives significant investment in cybersecurity solutions to safeguard both government and private space operations. The U.S. market is projected to reach USD 1.51 billion by 2026. For instance,

- In August 2025, IonQ finalized its acquisition of Capella Space and announced efforts to expand quantum‑secure communications into satellite networks, effectively enhancing space cybersecurity capabilities.

Download Free sample to learn more about this report.

In 2026, the U.S. market is estimated to reach USD 1.29 billion. The strong presence of commercial satellite and launch providers in the U.S., coupled with advanced domestic cybersecurity capabilities, reinforces America’s dominance in securing both government and commercial space systems.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe contributed approximately USD 1.56 billion to the global market in 2025, accounting for 27.55% share, and is expected to reach USD 1.74 billion in 2026. Europe is anticipated to witness a moderate growth in the coming years. During the forecast period, the European region is expected to record a CAGR of 8.2%, which is the fourth-highest among all regions, and reach a valuation of USD 1.03 billion by 2026. This is primarily due to increased investments in sovereign space infrastructure and the enforcement of stringent cybersecurity regulations targeted at space‑asset protection. Additionally, a rising number of commercial and defense space systems across Europe are moving to adopt advanced cybersecurity solutions as a response to evolving threat landscapes and the need for regional strategic autonomy. The UK market is projected to reach USD 0.47 billion by 2026 and the Germany market is projected to reach USD 0.36 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 1.56 billion, representing 27.60% of global demand, and is projected to grow to USD 1.75 billion in 2026 and it is expected to grow at the highest CAGR of 12.5% during the forecast period. The regional growth is fueled by rapidly increasing satellite deployments and expanding national space programs, especially in countries such as China, India, and Japan, creating a surge in demand for specialized cybersecurity solutions. Also, the region’s evolving regulatory frameworks, rising commercial space activities, and the need for secure ground and space‑segment infrastructure are further boosting investments in space cybersecurity. The Japan market is projected to reach USD 0.28 billion by 2026, the China market is projected to reach USD 0.44 billion by 2026, and the India market is projected to reach USD 0.32 billion by 2026.

South America

South America is expected to witness significant growth in this market. The South American market in 2026 is expected to reach USD 0.26 billion, driven by the expansion of national space programs and satellite infrastructure, which in turn elevates demand for advanced cybersecurity solutions to protect these emerging assets.

Middle East & Africa

The Middle East & Africa are estimated to reach USD 0.42 billion in 2025 and are expected to grow at a significant rate in the coming years, as governments increasingly launch national space programs and develop satellite and ground‑station infrastructure, thereby creating new security demands. In the region, the GCC is set to attain a value of USD 0.13 billion in 2026.

Rest of the World

Rest of the World recorded a market size of USD 0.56 billion in 2025, capturing 9.87% of the global market share, and is projected to reach USD 0.61 billion in 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Strong Geographic Presence, Along with a Various Range of Products by Key Players, Enhance Their Market Positions

The global market exhibits a semi-concentrated structure, with numerous small to mid-size companies actively operating globally. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Thales Group, Airbus Defence and Space GmbH, Northrop Grumman, Lockheed Martin, and Boeing are heavily involved in developing cutting-edge cybersecurity solutions to meet the increasing demands of space systems. This involves the continuous advancement of secure communication technologies, encryption methods, and real-time monitoring systems for space-based assets.

Apart from this, other prominent players in the market include RTX (Raytheon), L3Harris Technologies, BAE Systems, Leonardo S.p.A., General Dynamics, and others. These companies are investing heavily in R&D to develop advanced cybersecurity technologies. These investments help them stay ahead of emerging threats and enable the creation of more resilient space cybersecurity products.

Long List of Key Space Cybersecurity Companies Studied

- Thales Group (France)

- Airbus Defence and Space GmbH (Germany)

- Northrop Grumman (U.S.)

- Lockheed Martin (U.S.)

- RTX (Raytheon) (U.S.)

- Boeing (U.S.)

- L3Harris Technologies (U.S.)

- BAE Systems (U.K.)

- Leonardo S.p.A. (Italy)

- General Dynamics (U.S.)

- SpaceX (U.S.)

- Maxar Technologies (U.S.)

- Kratos Defense & Security Solutions (U.S.)

- Viasat (U.S.)

- Israel Aerospace Industries (Israel)

- Rafael Advanced Defense Systems (Israel)

- QinetiQ (U.K.)

- Kongsberg Defence & Aerospace (Norway)

- Parsons Corporation (U.S.)

- SpiderOak Inc. (U.S.)

….and more

KEY INDUSTRY DEVELOPMENTS

- July 2025: Leonardo S.p.A. acquired a 24.55 % stake in Finland’s cybersecurity company SSH, becoming its largest shareholder as it expands its cybersecurity offerings for hybrid‑cloud and quantum‑safe encryption in aerospace and defense.

- June 2025: Thales and telecom‑provider Proximus formed a strategic partnership under a contract with the NATO Communications and Information Agency (NCIA) to enhance the resilience and security of critical infrastructure networks, signaling the growth of Thales’s cybersecurity footprint in space‑adjacent communications systems.

- June 2025: Netgear acquired Bengaluru‑based cybersecurity startup Exium to enhance its integrated networking and security service offerings, although this development is broader than pure space cybersecurity.

- December 2024: The Space Development Agency (SDA) announced a contract extension with SpiderOak Inc. aimed at integrating zero‑trust cybersecurity architecture across both ground and space‑segment interactions. The extension underscores the critical importance of securing communications and access within the heavily distributed Proliferated Warfighter Space Architecture (PWSA) mesh network of ground and orbiting assets.

- November 2024: Booz Allen Ventures, LLC, announced a strategic investment in Starfish Space, a leader in satellite servicing technology, to strengthen its position in the growing space economy. The investment aims to advance Starfish's capabilities in space debris removal and satellite servicing, aligning with Booz Allen’s broader strategy to enhance cybersecurity and operational resilience in space.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the space cybersecurity market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Offering · Solution · Services By Platform · Satellite · Launch Vehicles · Ground Stations · Spaceports & Launch Facilities · Others (Command & Control Center, etc.) By End User · Government · Commercial · Defense By Region · North America (By Offering, By Platform, By End User, and By Country) o U.S. (By End User) o Canada (By End User) o Mexico (By End User) · South America (By Offering, By Platform, By End User, and By Country) o Brazil (By End User) o Argentina (By End User) o Rest of South America · Europe (By Offering, By Platform, By End User, and By Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Italy (By End User) o Spain (By End User) o Russia (By End User) o Benelux (By End User) o Nordics (By End User) o Rest of Europe · Middle East & Africa (By Offering, By Platform, By End User, and By Country) o Turkey (By End User) o Israel (By End User) o GCC (By End User) o North Africa (By End User) o South Africa (By End User) o Rest of Middle East & Africa · Asia Pacific (By Offering, By Platform, By End User, and By Country) o China (By End User) o India (By End User) o Japan (By End User) o South Korea (By End User) o ASEAN (By End User) o Oceania (By End User) o Rest of Asia Pacific |

|

Companies Profiled in the Report |

· Thales Group (France) · Airbus Defence and Space GmbH (Germany) · Northrop Grumman (U.S.) · Lockheed Martin (U.S.) · RTX (Raytheon) (U.S.) · Boeing (U.S.) · L3Harris Technologies (U.S.) · BAE Systems (U.K.) · Leonardo S.p.A. (Italy) · General Dynamics (U.S.) |

Frequently Asked Questions

The market is expected to reach USD 11.01 billion by 2034.

In 2025, the market was valued at USD 4.84 billion.

The market is expected to grow at a CAGR of 9.7% during the forecast period.

By end user, the government system led the market.

Increasing cyber threats and the critical dependence on space systems are driving cybersecurity demand.

Thales Group, Airbus Defence and Space GmbH, Northrop Grumman, Lockheed Martin, Boeing, RTX (Raytheon), L3Harris Technologies, BAE Systems, Leonardo S.p.A., and General Dynamics are the top players in the market.

North America held the highest market share.

By end user, the commercial segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us