Aerospace Sealants Market Size, Share & Industry Analysis, By Resin (Polysulfide, Silicone, Fluorosilicone, Polyacrylate, Polyurethane, Polythioether, and Others), By Application (Fuel Tank, Airframe, Flight Line Repair, Aircraft Windshield & Canopy, Fuselage, and Others), By End-Use (Commercial Aviation, Military Aviation, and Others), By Formulation Technology (Solvent-Based, Water-Based, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

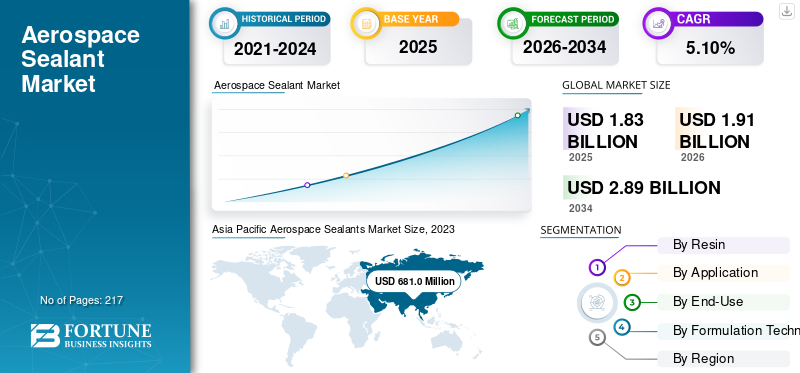

The global aerospace sealants market size was valued at USD 1.83 billion in 2025. The market is projected to grow from USD 1.91 billion in 2025 to USD 2.89 billion by 2034 at a CAGR of 5.10% during the 2024-2032 forecast period. Asia Pacific dominated the global market with a share of 34.30% in 2025.

Aerospace sealants are a unique class of adhesive formulations specially designed to reinforce and seal different parts of the aircraft to improve structural integrity. These products are manufactured by using different resins such as polysulfide, silicone, fluorosilicone, polyacrylate, polyurethane, and polythioether and are used for different sealing applications in the aircraft, including fuel tanks, airframes, flight line repair, aircraft windshields & canopy, and fuselage. These products are essentially used in the manufacturing and maintenance of aircraft used for military and commercial purposes.

The COVID-19 pandemic had a detrimental impact on several industries and the aerospace sealants industry was no exception. Many countries across the world, including the U.S., Canada, Germany, France, the U.K., Italy, Spain, China, India, Brazil, and South Africa, announced lockdowns, leading to restrictions on the movement. This factor severely affected the supply chain of the manufacturers operating in the market. Since both raw material supply and finished goods distribution were affected, the pandemic rigorously distressed the revenue generation of aerospace sealants manufacturers.

Download Free sample to learn more about this report.

Global Aerospace Sealants Market Overview

Market Size & Forecast:

- 2025 Market Size: USD 1.83 billion

- 2026 Market Size: USD 1.91 billion

- 2034 Forecast Market Size: USD 2.89 billion

- CAGR: 5.10% from 2026–2034

Market Share:

- Asia Pacific dominated the aerospace sealants market with a 34.30% share in 2025, driven by rising air travel demand, expanding airline fleets, and increasing aircraft production across China, India, and Japan.

- The U.S. aerospace sealants market is projected to reach USD 490.28 million by 2032, propelled by strong aircraft manufacturing and growing demand for advanced sealing technologies.

Regional Insights:

- Asia Pacific: Held the largest share at USD 0.628 billion in 2026, led by robust aircraft manufacturing in China, India, and Japan, and increasing MRO activities.

- North America: Growth driven by defense spending, commercial fleet expansion, and space exploration—supported by strong OEM presence.

- Europe: Anchored by key aerospace manufacturers in Germany, the U.K., and Italy, with innovation and sustainability at the forefront.

- Latin America: Brazil’s expanding civil and defense aviation sectors are boosting regional sealant demand.

- Middle East & Africa: Growth supported by rising MRO operations, fleet expansions, and demand for sealants with high weather resistance.

Aerospace Sealants Market Trends

Increasing Demand for Military Applications to Present Lucrative Market Opportunities

The increasing demand for military applications driven by advanced aircraft development, harsh operating environments, and innovations & customizations present lucrative opportunities for the market. The military forces of many countries are investing heavily in the development and procurement of advanced aircraft, including transport planes, unmanned aerial vehicles, and fighter jets, which require high-performance sealants for their structural integrity and functionality. The growth is attributed to the ability of sealants to encounter harsh environments, such as extreme temperatures, high speed, and exposure to corrosive substances. In addition, they can withstand these conditions and are becoming crucial for ensuring the reliability and longevity of military aircraft. This factor is creating a steady demand for specialized products such as corrosion-inhibiting aerospace sealants. Hence, such factors are expected to flourish the market growth during the forecast period.

Download Free sample to learn more about this report.

Aerospace Sealants Market Growth Factors

Rapid Growth of Aerospace Industry to Surge Sealants Demand

The aerospace industry is experiencing significant growth driven by increasing global air travel, fleet modernization, and increased aircraft usage & advancements in military aviation. This growth of the aerospace industry is resulting in the rise in demand for aerospace sealants, which are essential for ensuring the safety, efficiency, and longevity of the aircraft. The rise in global air travel, particularly in emerging economies, coupled with the expansion of airline fleets to accommodate more passengers and enhance route networks, is slated to promote the aerospace sealants market growth. In addition, new aircraft models are designed to be more fuel-efficient and environmentally friendly, creating a high demand for sealants to maintain structural integrity, prevent leaks, and protect against extreme temperatures and corrosion. Therefore, such a growing number of factors, along with the expansion of the aerospace industry, are expected to fuel the market growth.

RESTRAINING FACTORS

Increasing Production Cost Coupled with Stringent Environmental Regulations May Limit Market Growth

The increasing production cost and stringent environmental regulations can limit the market growth. The need for advanced materials and complex manufacturing processes are making sealants more expensive, reducing profit margins for the manufacturers. Furthermore, the implementation of stringent environmental regulations by governments and associations due to rising environmental issues has also forced several countries to incorporate a new set of rules that limit the adoption of sealants. Hence, these factors are expected to impede the growth of the market.

Aerospace Sealants Market Segmentation Analysis

By Resin Analysis

Polysulfide Segment Dominated Owing to Increasing Use in Fuel Tank Application

Based on resin, the market is classified into polysulfide, silicone, fluorosilicone, polyacrylate, polyurethane, polythioether, and others.

The polysulfide segment will account for 42.29% market share in 2026 and is estimated to record a significant growth rate during the forecast period. Polysulfide sealants possess a variety of properties that are highly advantageous for aerospace applications. One significant benefit is their exceptional resistance to jet fuel and other fuels, making them an ideal choice for sealing fuel tanks. In addition, they serve as effective insulators and can be used to pot or seal electronic components within tanks. The flexibility of cured polysulfide allows them to endure vibration, joint movement, and impact during travel.

The silicone segment is experiencing significant growth in the overall market. In the aerospace industry, silicone is used for sealing devices due to its strength and excellent temperature resistance. Furthermore, designing and engineering in the aerospace sector is highly complex, requiring reliable materials and strong execution to ensure the safety of large objects in the air. Consequently, silicone has proven to be a trusted material capable of handling these challenging applications.

By Application Analysis

Fuel Tank Segment Dominates Market Driven by Stringent Safety Needs

In terms of application, the market is segmented into fuel tank, airframe, flight line repair, aircraft windshield & canopy, fuselage, and others.

The fuel tank segment will account for 63.21% market share in 2026. The use of sealants in fuel tanks is crucial for ensuring the integrity and safety of aircraft. The aerospace industry's stringent safety and performance requirements, along with rising demand for technologically advanced aircraft and the increasing number of aircraft in service, are poised to continue to drive the growth of sealants in fuel tank applications. The segment is set to capture 63.1% of the market share in 2025.

The airframe segment is anticipated to showcase robust CAGR of 5.00% during the forecast period. In the airframe application, the adoption of sealants can be majorly seen in the fuselage, wings, empennage (tail assembly), and landing gear. The use of sealants in airframes is essential for maintaining structural integrity and ensuring the longevity and safety of aircraft.

By End-Use Analysis

Growing Aerospace Industry to Foster Commercial Aviation Segment Expansion

In terms of end-use, the market is segmented into commercial aviation, military aviation, and others.

The commercial aviation segment is expected to account for 44.44% of the market in 2026. Sealants are crucial in commercial aircraft for ensuring the integrity and safety of aircraft. They are used extensively in various parts of an aircraft to prevent air and fluid leaks, enhance structural strength, and protect against environmental factors such as moisture, temperature fluctuations, and chemical exposure. The common applications of the sealants include sealing fuel tanks, fuselage sections, wings, windows, and doors to maintain pressurization and prevent corrosion. The growing technological innovation coupled with rapid growth in the aerospace industry is likely to influence the segment growth during the forecast timeframe. The segment is poised to hold 44% of the market share in 2025.

The military aviation segment held a significant market share in 2023. The growing need for enhanced durability and reliability in harsh operational environments, along with the necessity of maintaining high levels of aircraft readiness and safety, is fueling the demand for sealants to contribute significantly to mission success and operational efficiency. This segment is foreseen to register a CAGR of 5.00% during the forecast period (2024-2032).

To know how our report can help streamline your business, Speak to Analyst

By Formulation Technology Analysis

Others (Chemical-Reactive) Segment to Witness Highest CAGR Owing to Growing Demand in Structural Bonding Applications

In terms of formulation technology, the market is segmented into solvent-based, water-based, and others.

The others segment is poised to grow at the highest CAGR during 2024-2032. The segment includes chemical reactive sealants such as polysulfide, silicone, polyurethane, and silane-modified polymers. Polysulfide sealants are ideal for their characteristics such as durability, chemical resistance, adhesion to various substrates, and ability to withstand the extreme environmental conditions experienced during flight. Such properties make them essential for ensuring safety, performance, and longevity in aircraft and spacecraft. On the other hand, polyurethane sealants are ideal for their robust adhesion, flexibility, durability, and resistance to environmental factors. They find their adoption in structural bonding, window and windshield sealing, repair & maintenance, and exterior sealing including galleys, lavatories, and seating areas. Additionally, the growing demand for these polymers in structural bonding applications owing to their high strength and durability is expected to surge the segment growth during the forecast period.

Solvent-based sealants are widely used in the aerospace industry due to their excellent adhesion properties and ability to create durable and flexible bonds. These sealants are formulated with solvents that evaporate during the curing process, leaving a resilient and weather-resistant seal. They are particularly effective in sealing aircraft fuel tanks, fuselage seams, and other critical components exposed to extreme environmental conditions and varying pressures. The Solvent-based segment is expected to document a substantial CAGR of 21.02% in 2026.

The water-based segment is set to hold 9.80% of the market share in 2025.

REGIONAL INSIGHTS

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Aerospace Sealants Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, Asia Pacific generated USD 0.6 billion, contributing 34.30% to global market revenue, and is projected to grow to USD 0.63 billion in 2026. The region is set to document a significant CAGR of 5.50% during the forecast period (2024-2032). The growth is mainly driven by a significant increase in air travel demand, expanding airline fleets, and the development of indigenous aircraft manufacturing capabilities. The Chinese market is poised to gain USD 0.354 billion in 2025. Countries such as China, India, and Japan are investing heavily in aerospace infrastructure, including new aircraft production and Maintenance, Repair, and Overhaul (MRO) facilities. This surge in activity has spurred the demand for advanced aerospace sealants, which are critical for ensuring aircraft safety, performance, and durability. India is set to be valued at USD 31.42 million in 2025, while Japan is anticipated to be worth USD 0.171 billion in 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

The North America region captured 22.40% of the global market in 2025, generating USD 0.41 billion in revenue, and is projected to reach USD 0.43 billion in 2026. The growth of the aerospace industry in North America is propelled by several factors, including advancements in technology, increased defense spending, rising demand for commercial air travel, and the expansion of space exploration initiatives. This growth drives the increasing use of sealants, as these materials are essential for ensuring the reliability, safety, and longevity of aerospace components and structures. The U.S. market is likely to hit USD 0.369 billion in 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 0.74 billion in 2025, accounting for 40.40% share, and is expected to reach USD 0.77 billion in 2026. The strong presence of major aerospace manufacturers and suppliers in Germany, the U.K., and Italy, coupled with a focus on innovation and high-quality production standards, is propelling market expansion in Europe. The U.K. market is foreseen to grow with a valuation of USD 0.104 billion in 2025. The country's robust industrial base and emphasis on research and development foster advancements in aerospace sealant technologies. Germany is set to reach USD 0.145 billion in 2026, while France is poised to hit USD 102.52 million in the same year.

Latin America

The Latin America market generated USD 0.04 billion in 2025, representing 2.10% of the global market landscape, and is expected to reach USD 0.04 billion in 2026. The expanding commercial aviation sector in Latin America, particularly in Brazil, along with ongoing investments in defense modernization initiatives, including the Brazilian Air Force's (FAB) fleet upgrades, is fueling the country’s growth. Moreover, advancements in aerospace manufacturing technologies and materials require sealants that can meet stringent performance standards for durability, safety, and operational efficiency, further driving the market growth in the region.

Middle East & Africa

Middle East & Africa recorded a market size of USD 0.02 billion in 2025, capturing 3.80% of the global market share, and is projected to reach USD 0.02 billion in 2026. The Middle East & Africa market for aerospace sealants is expanding rapidly, supported by a growing aerospace manufacturing sector and increasing aircraft maintenance activities. The region's aviation industry, bolstered by both defense and civil aviation sectors, drives demand for sealants that can withstand harsh environmental conditions and stringent safety standards. The UAE market is expected to stand at USD 5.28 million in 2025.

KEY INDUSTRY PLAYERS

Key Players to Adopt Investment and Research & Development Strategies to Maintain Dominance in Market

In terms of the competitive landscape, the market depicts the presence of established and emerging companies. PPG Industries, Inc., 3M, Solvay, Henkel Corporation, and Arkema are some of the key players in this market. For instance, Henkel Corporation focuses on heavy investments in research and development in the aerospace industry to tackle any maintenance and manufacturing needs by providing BONDERITE and LOCTITE products.

List of Top Aerospace Sealants Companies:

- 3M (U.S.)

- Solvay (Belgium)

- PPG Industries, Inc. (U.S.)

- Henkel Corporation (Germany)

- Beacon Adhesives, Inc. (U.S.)

- Master Bond Inc. (U.S.)

- H.B. Fuller Company (U.S.)

- Arkema (France)

- Flamemaster Corp. (U.S.)

- Aerospace Sealants (U.S.)

- Chemetall (Germany)

KEY INDUSTRY DEVELOPMENTS:

- September 2022: Solvay entered a long-term agreement with Avio SpA to supply advanced composites and adhesive materials for demanding aerospace applications. The products supplied by Solvay would be used in a range of aerospace programs, including the Vega space programs and the European Space Agency’s satellite launch vehicles designed to send payloads into low Earth orbit (LEO).

- January 2022: H.B. Fuller finalized the purchase of Apollo, the U.K. manufacturer of liquid adhesives, sealants, coatings, and primers for the roofing, industrial, and construction markets. Apollo will operate within H.B. Fuller’s existing Construction Adhesives and Engineering Adhesives business units and is expected to enhance H.B. Fuller’s position in key high-value, high-margin markets in the U.K. and Europe.

- April 2020: PPG collaborated with Dow and its Sustainable Future Program to accelerate the adoption of low-carbon technologies. The partnership focuses on anti-corrosion coating products for steel designed to deliver reduced Greenhouse Gas (GHG) emissions through increased energy efficiency while helping to lessen the high maintenance costs of steel infrastructure.

- November 2019: Chemetall announced it had completed the expansion of its production site based in Langelsheim, Germany. The company reported an increase in the production of Naftoseal aircraft sealants in order to cater to the rising market demand. As part of this expansion, the company inaugurated a new office building and a laboratory at this site.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, forging types, compositions used to produce these products, and end-use industries of the product. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) and Volume (Ton) |

|

Growth Rate |

CAGR of 5.10% from 2026 to 2034 |

|

Segmentation |

By Resin

|

|

By Application

|

|

|

By End-Use

|

|

|

By Formulation Technology

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.91 billion in 2026 and is projected to reach USD 2.89 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 0.602 billion.

Recording a CAGR of 5.10%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By application, the fuel tank segment led in 2025.

The rapid growth of the aerospace industry is set to surge sealant demand during the projected timeframe, impelling market growth.

Asia Pacific held the highest market share in 2025.

The growing expansion of aerospace industry worldwide coupled with rising manufacturing of advanced aircraft is expected to drive the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 217

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us