Agentic AI in Healthcare Market Size, Share & Industry Analysis, By Component (Software and Services), By Technology (Machine Learning, Natural Language Processing, and Others), By Application (Clinical Decision Support & Diagnostics, Clinical Documentation & Workflow Automation, Patient Access & Operational Efficiency, Revenue Cycle Management (RCM), Virtual Health Assistants & Monitoring, and Others), By Deployment (Cloud-based, On-Premise, and Hybrid), By End User (Healthcare Providers, Healthcare Payers, and Others), and Regional Forecast, 2026-2034

Agentic AI in Healthcare Market Size and Future Outlook

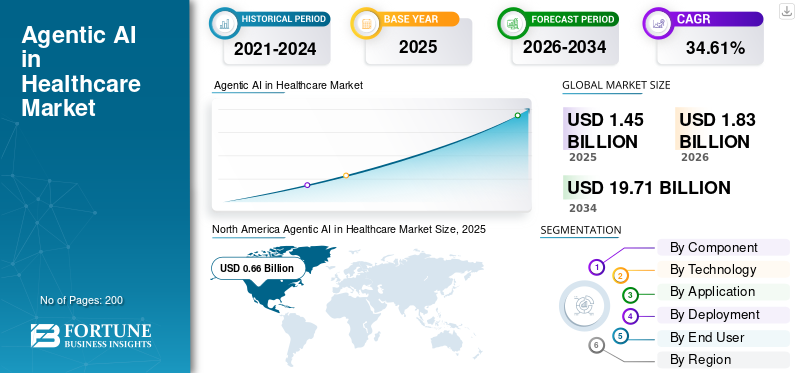

The global agentic AI in healthcare market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.83 billion in 2026 to USD 19.71 billion by 2034, exhibiting a CAGR of 34.61% during the forecast period. North America dominated the agentic AI in healthcare market with a market share of 45.52% in 2025.

Agentic AI in healthcare refers to AI systems that generate answers and plan, decide, and take actions over multiple steps to achieve a specific goal. This is often done by using tools under defined permissions and guardrails. This market is witnessing rapid growth driven by workforce shortages and burnout, the explosion of health data, and the increasing demand for personalized care.

Key players such as Microsoft, Oracle, Salesforce, Inc., Alphabet Inc., and Innovaccer are emphasizing on technological advancements in their product offerings to maintain their leading positions in the market.

Download Free sample to learn more about this report.

AGENTIC AI IN HEALTHCARE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.45 Billion

- 2026 Market Size: USD 1.83 Billion

- 2034 Forecast Market Size: USD 19.71 Billion

- CAGR: 34.61% from 2026–2034

- North America dominated the agentic AI in healthcare market with a 45.52% share in 2025.

- The software segment captured the largest market share in 2025.

- The natural language processing segment is projected to account for 50.2% of the market in 2026.

North America

North America generated USD 0.66 billion in 2025, driven by strong pharmaceutical and diagnostic sectors, growing healthcare data volumes, and AI adoption.

Europe

Europe is projected to grow at a CAGR of 34.33%, driven by clinical research capabilities, AI investments, and healthcare AI adoption.

Asia Pacific

Asia Pacific is projected to reach USD 0.36 billion in 2026, driven by rapid AI adoption across healthcare systems in China, India, and Japan.

U.S.

The agentic AI in healthcare market is projected to reach USD 0.76 billion in 2026.

Japan

The agentic AI in healthcare market is projected to reach USD 0.08 billion in 2026.

Read More

AGENTIC AI in HEALTHCARE MARKET TRENDS

Move from Chatbots to Action-Oriented Agents is a Prominent Market Trend

The transition from chatbots to action-driven agents represents a notable market trend, as purchasers are increasingly dissatisfied with tools that merely respond to inquiries or generate text, they seek systems capable of executing multi-step workflows comprehensively. Providers and payers are focusing on solutions that can extract data from EHR/RCM systems, generate appropriate documentation, assign tasks, initiate prior authorizations, correct claim issues, and raise exceptions with audit trails. Operational pressure is the driving force: staffing shortages, administrative burdens, and the demand for measurable ROI render work automation significantly more valuable than mere discussion. As deployments advance, organizations are transitioning to human-in-the-loop execution, where agents operate within specified permissions and gain insights from results. This also boosts stickiness as action agents integrate into daily workflows (billing work queues, authorizations, scheduling), rather than being confined to a standalone chat interface. These factors are supporting the overall global agentic AI in healthcare market growth.

- For instance, in February 2025, Salesforce announced Agentforce for Health, a library of pre-built agent skills and actions designed to go beyond chatbot Q&A and take workflow actions such as benefits verification, eligibility checks, and speeding care approvals via partner integrations.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Administrative Burden and Workforce Shortages is Propelling Market Growth

Increasing administrative pressure and workforce shortfalls are significantly driving the growth of Agentic AI in Healthcare, as hospitals and payers confront a growing disparity between work volume (documentation, coding, prior authorization, claims follow-up, scheduling, inbox tasks) and the skilled personnel available. As vacancy rates increase, organizations either tolerate delays and revenue losses or invest in automation that can perform repetitive tasks under human supervision. Agentic systems are appealing since they do more than merely “generate text”, they can spot gaps, prioritize task lists, initiate subsequent actions, and manage exceptions, effectively reducing manual involvement per case. This enhances productivity without necessitating a corresponding increase in headcount, simplifying the justification of ROI even during restricted budget periods. The driver is most effective in mid-cycle and back-office operations where a lack of staff directly leads to compliance risks, delays, and lost reimbursements. Gradually, the capability to expand operations through agents becomes a strategic tool to safeguard margins and clinician resources. All these factors cumulatively drive the overall market growth.

- For instance, in May 2025, AKASA launched CDI Optimizer, noting that mid-cycle operations (clinical documentation, coding, compliance) are under increasing pressure from acute staffing shortages and that the GenAI assistant is designed to review encounters at scale and surface documentation gaps for teams to act on.

MARKET RESTRAINT

Data Privacy, Security, And Data-Residency Constraints to Hamper Market Growth

Data privacy, security, and data-residency laws act as a market limitation due to the delicate nature of patient data, hindering numerous purchasers from moving it across borders or exchanging it among institutions. This requires vendors to establish hosting, consent management, and governance measures customized for particular regions, resulting in increased deployment times and higher costs. Healthcare providers and public programs need robust audit trails and strict access controls, which lead to longer procurement processes and a lower rate of pilot projects swiftly moving to widespread implementation. When organizations worry about breach risks or unclear downstream uses of genetic data, they may suspend data-sharing agreements, limit cloud usage, or restrict secondary purposes, leading to a direct reduction in platform usage and delaying revenue growth. This results in limiting the market growth to a certain extent.

MARKET OPPORTUNITIES

Administrative & Financial Optimization to Offer Market Growth Opportunities

Administrative & Financial Optimization is a strong market opportunity for agentic AI in healthcare, as non-clinical work consumes a disproportionate share of healthcare operating costs, and even small efficiency gains translate into meaningful margin improvement. Providers and payers are increasingly targeting agents that can execute end-to-end administrative workflows, such as eligibility checks, claim edits, denial prevention, collections follow-ups, and patient billing resolution, as these are high-volume, repeatable tasks with clear KPIs. This creates a scalable path to ROI: fewer manual touches per case, faster turnaround times, and reduced leakage from errors and rework. Agentic AI also enables continuous optimization by learning from outcomes and updating workflows without rebuilding entire systems. As reimbursement pressure and labor shortages persist, organizations will prioritize solutions that reduce administrative load while improving cash flow predictability. Over time, this expands from point tools into platform-led automation programs spanning front-, mid-, and back-office processes, driving larger enterprise contract sizes. All these factors would drive the market growth over the coming years.

- For instance, in November 2025, PwC announced a strategic collaboration with AWS to modernize healthcare revenue cycle management by making PwC’s Revenue Cycle Managed Services available on AWS by building AI agents and tools aimed to automate billing and processing, reduce administrative burden, and improve financial performance.

MARKET CHALLENGES

Integration Complexity Poses a Prominent Challenge to Market Growth

The complexity of integrating with EMR/RCM, healthcare workflows, and current bioinformatics frameworks poses a significant challenge in the market, as most purchasers cannot easily “rip and replace” their operational systems. Every end user generally maintains its own procedures for sample tracking, accessioning, QC standards, reporting templates, and data governance, making the implementation of an AI platform frequently dependent on tailored interfaces, data mapping, and validation processes. This lengthens implementation time, heightens service dependency, and may delay go-live, particularly in regulated clinical environments where workflow modifications must be recorded and audited. Integration challenges also pose an adoption risk: strong AI performance will not be effective if outcomes cannot seamlessly integrate into the daily tools of clinicians or laboratorians. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Component

Increasing Number of Software Deployments to Propel Software Segmental Growth

Based on the component, the market is divided into software and services.

The software segment captured the largest global agentic AI in healthcare market share. As sequencing volumes increase, laboratories and pharmaceutical teams focus on tools that automate manual assessments, standardize outcomes, and reduce turnaround times, leading to more extensive and frequent software agreements. Software also scales across locations and research with minimal additional costs, enabling companies to increase usage more rapidly than they can hire specialized bioinformatics personnel. Furthermore, vendors regularly enhance their algorithms and pipelines, leading to more frequent subscription and license renewals.

- For instance, in June 2025, Ellipsis Health closed a USD 45 million Series A and launched 'Sage', an AI care manager (voice-based, agentic), demonstrating commercial traction for agentic care agents.

The services segment is anticipated to rise with a CAGR of 30.64% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Natural Language Processing Segment Dominates Due to its High Usage in Various Applications

On the basis of technology, the market is divided into machine learning, natural language processing, and others.

The natural language processing segment dominated the global market in 2025. The highest-volume workflows are language-heavy, clinical notes, patient–provider conversations, in-basket messages, discharge summaries, referral letters, and prior-authorization narratives. NLP also fits naturally into copilot/agent experiences where automation happens through conversation and documentation, making adoption easier for clinicians and front-office teams. Furthermore, the segment is set to hold a 50.2% share in 2026.

- For instance, in March 2025, Oracle announced that its Oracle Health Clinical AI Agent (a voice- and screen-driven assistant that converts clinician interactions into documentation across 30+ specialties) helped physicians achieve a ~30% reduction in daily documentation time.

The machine learning segment is anticipated to grow with a CAGR of 32.73% over the forecast period.

By Application

High Usage in Revenue Cycle Management to Boost Segmental Growth

On the basis of application, the market is divided into clinical decision support & diagnostics, clinical documentation & workflow automation, patient access & operational efficiency, Revenue Cycle Management (RCM), virtual health assistants & monitoring, and others.

The Revenue Cycle Management (RCM) segment captured the highest market share in 2025. It is one of the largest, most repeatable, and most measurable workflow areas where agents can execute tasks end-to-end. In addition, RCM deployments can scale across large facility networks, resulting in large enterprise contracts and recurring software revenue. Furthermore, the segment is set to hold a 20.8% share in 2026.

- For instance, in January 2026, Waystar announced the introduction of agentic AI to advance toward an autonomous revenue cycle.

The clinical documentation & workflow automation segment is anticipated to grow with a CAGR of 38.54% over the forecast period.

By Deployment

Rising Shift Toward Cloud-based Solutions Supported the Segmental Dominance

Based on the deployment, the market is divided into on-premise, cloud-based, and hybrid.

The cloud-based segment is anticipated to capture the largest market share in 2025. This is due to cloud deployments enabling elastic acceleration (e.g., GPUs) for more demanding ML models and multi-omics analysis, helping customers reduce turnaround times. Moreover, cloud platforms simplify the standardization of pipelines across locations, enable centralized governance, and facilitate collaboration among distributed research and lab teams without the need to repeatedly copy datasets. Furthermore, the segment is set to hold 47.3% share in 2026.

- For instance, in April 2025, AWS announced workflow versioning support in AWS HealthOmics, a managed cloud service for biological data stores and workflows.

The hybrid segment is anticipated to rise with a CAGR of 30.90% over the forecast period.

By End User

High Demand from Healthcare Providers to Support Segment’s Leading Position

Based on end user, the market is segmented into healthcare providers, healthcare payers, and others.

In 2025, the healthcare providers segment held the leading position in the global market. They are the primary owners of clinical data and EHR workflows, so most agentic deployments naturally start where tool access, approvals, and audit trails can be embedded into care delivery systems. Large health systems can also scale deployments enterprise-wide, resulting in larger contract sizes than fragmented buyer groups. Moreover, provider demand is reinforced by the need to standardize workflows and improve patient experience, which agentic tools directly address. Furthermore, the segment is set to hold a 65.8% share in 2026.

- For instance, in October 2024, HCA Healthcare selected Commure as its exclusive partner to develop and deploy an ambient AI platform across its network of healthcare professionals.

In addition, healthcare payers are projected to grow at a CAGR of 37.74% during the forecast period.

Agentic AI in Healthcare Market Regional Outlook

By geography, the market is segmented into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

North America

North America Agentic AI in Healthcare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North American market size was USD 0.53 billion in 2024 and dominated the global market. The region also maintained its dominance in 2025, with USD 0.66 billion. Crucial elements such as robust pharmaceutical and diagnostic frameworks, increasing healthcare data volumes, and encouraging government policies for AI implementation are propelling regional supremacy.

U.S. Agentic AI in Healthcare Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 0.76 billion in 2026, accounting for roughly 41.7% of global market.

Europe

Europe market size is anticipated to grow at a CAGR of 34.33% during the forecast period. The region is anticipated to capture the second leading position among all regions. The European market is largely propelled by a strong presence of clinical research hubs and centers, rising investments in AI integration, and extensive adoption of AI technologies in healthcare.

U.K. Agentic AI in Healthcare Market

The U.K. market in 2026 is estimated at around USD 0.10 billion, representing roughly 5.3% of global revenues.

Germany Agentic AI in Healthcare Market

Germany market size is projected to reach approximately USD 0.11 billion in 2026, equivalent to around 6.2% of global sales.

Asia Pacific

Asia Pacific market size is projected to be valued at USD 0.36 billion in 2026 and secure the position of the third largest region in the global industry. Rapid adoption in China, India, and Japan is the primary driver of regional market growth.

Japan Agentic AI in Healthcare Market

The Japan market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 4.4% of global revenues.

China Agentic AI in Healthcare Market

China’s market is projected to reach revenues of around USD 0.09 million in 2026, representing roughly 5.0% of global sales.

India Agentic AI in Healthcare Market

The Indian market in 2026 is estimated at around USD 0.07 billion, accounting for roughly 3.8% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are anticipated to witness comparatively slower growth over the forecast period. The Latin America market size is set to reach a valuation of USD 0.11 billion in 2026. Prominent factors such as increased initiatives to build digital healthcare infrastructure and expanding AI adoption are expected to drive market growth. In the Middle East & Africa region, the GCC market in 2026 is estimated at around USD 0.02 billion, accounting for roughly 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Enterprise-grade Agent Platforms and Workflow Automation to Strengthen Key Players’ Market Position

The global agentic AI in healthcare sector is moderately fragmented, with competition spanning big tech platforms, EHR-native ecosystems, and specialized healthcare AI vendors. Key players such as Microsoft (Nuance), Epic Systems, Oracle Health, and Salesforce account for a significant share of the global market. These companies are focusing on agent-enabled clinical workflow automation, revenue-cycle modernization, and patient access automation, while also strengthening capabilities in integration, guardrails, and auditability to support production-scale rollouts. Strategic partnerships with EHRs, payers, and large health systems, along with new agent libraries and workflow-specific modules, are being used to expand the footprint and improve stickiness.

Other notable participants strengthening the competitive landscape include Google Cloud, AWS, Innovaccer, Notable, AKASA, Abridge, Ambience Healthcare, and Hippocratic AI, which are actively developing AI-driven interpretation and evidence automation capabilities.

- For instance, in February 2025, Innovaccer launched Agents of Care, a suite of pre-trained AI agents designed to automate repetitive administrative tasks and improve operational capacity across healthcare organizations.

LIST OF KEY AGENTIC AI IN HEALTHCARE COMPANIES PROFILED

- Microsoft (U.S.)

- Oracle (U.S.)

- Salesforce, Inc. (U.S.)

- Alphabet Inc. (U.S.)

- Innovaccer (U.S.)

- Notable (U.S.)

- Hippocratic AI (U.S.)

- Ambience Healthcare, Inc. (U.S.)

- Abridge Al, Inc. (U.S.)

- Epic Systems Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Greenway Health launched its “Agentic AI Factory” (built on AWS) to scale the building, deployment, and governance of AI agents across workflows from registration to payment.

- August 2025: Epic unveiled new AI agents at UGM25, including a revenue cycle management agent and other agentic capabilities to reduce admin burden and improve operations.

- July 2025: Ambience announced a USD 243 million Series C to scale its AI platform for health systems across documentation, coding, CDI and workflow support.

- June 2025: IQVIA launched new AI agents for life sciences/healthcare workflows and highlighted collaboration work with NVIDIA on custom models and agentic workflows to accelerate R&D and commercialization.

- June 2025: Cigna introduced AI-powered digital features to improve customer experience in common insurance interactions.

REPORT COVERAGE

The global agentic AI in healthcare market analysis includes a comprehensive study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements in products, the regulatory environment, and new product launches. Additionally, it details partnerships, mergers, and acquisitions, as well as key industry developments in the market. The market forecast report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 34.61% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Application, Deployment, End User, and Region |

| By Component |

|

| By Technology |

|

| By Application |

|

| By Deployment |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.45 billion in 2025 and is projected to reach USD 19.71 billion by 2034.

In 2025, the market value stood at USD 0.66 billion.

The market is expected to exhibit a CAGR of 34.61% during the forecast period.

By component, the software segment led the market.

The rapidly growing demand for personalized care and workforce shortages & burnout are the key factors driving the market.

Microsoft, Oracle, Salesforce, Inc., Alphabet Inc., and Innovaccer are some of the prominent players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us