Agriculture Tractor Market Size, Share & Industry Analysis, By Engine Power (Upto 30 HP, 31 – 40 HP, 41 – 60 HP, 61 – 80 HP, 81 – 100 HP, 101 – 120 HP, 121 – 150 HP, 151 -180 HP, and 181 HP & Above), By Type (Orchard Tractors, Row Crop Tractors, and Others) and Regional Forecast, 2026-2034

Agriculture Tractor Market Size

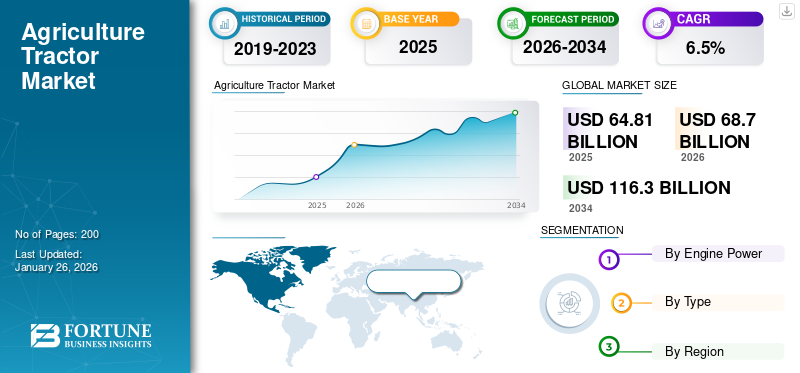

The global agriculture tractor market size was valued at USD 64.81 billion in 2025. The market is projected to grow from USD 68.70 billion in 2026 to USD 116.30 billion by 2034, growing at a CAGR of 6.8% during the forecast period. Asia Pacific dominated the global market with a share of 49.64% in 2025.

An agricultural tractor is a powerful vehicle designed to deliver high torque at low speeds, enabling farmers to perform various field operations efficiently. It serves as the backbone of modern farming by reducing manual labor and enhancing productivity. Tractors are used for plowing, harrowing, sowing, tilling, spraying, and transporting agricultural materials. Their adaptability with multiple implements makes them essential for both small and large-scale farming. The increasing focus on farm mechanization, labor shortages, and rising demand for higher crop yields are driving the adoption of modern tractors. Technological advancements and government support further accelerate their global market growth.

Key players in the market include John Deere, Mahindra, TurkTraktor, CNH Industrial, AGCO Corporation, and Kubota Corporation. The market is highly competitive, with companies focusing on innovation, efficiency, and regional expansion to gain an edge. Leading players are investing in smart and autonomous tractor technologies to enhance precision and reduce operational costs. Many firms are also strengthening dealer networks, offering flexible financing, and expanding manufacturing bases in emerging markets. Sustainable design, electric and hybrid models, and integration of IoT-based monitoring systems are becoming key differentiators. Continuous product upgrades and after-sales services help companies build strong brand loyalty and maintain long-term competitiveness.

Download Free sample to learn more about this report.

Global Agricultural Tractor Market Overview

Market Size:

- 2025 Value: USD 64.81 billion

- 2026 Value: USD 68.70 billion

- 2034 Forecast Value: USD 116.30 billion, reflecting a CAGR of 6.8% during 2026–2034

Market Share & Segmentation

- Top Tractor Type: Row‑crop tractors commanded the largest market share in 2025.

- Regional Leader: Asia Pacific region led the global tractor market in 2025, fueled by mechanization efforts in India, China, and Southeast Asia.

- High‑Growth Focus: Adoption of tractors in high-population agricultural economies continues to drive volume growth.

Industry Trends

- Rapid expansion of precision farming technologies, such as GPS, telematics, IoT-enabled connectivity, and smart farming tools.

- Rising interest in electric, CNG, hybrid, and autonomous tractors, aligned with environmental regulations, labor shortages, and equipment-sharing platforms.

Driving Factors

- Mechanization Push:Governments are promoting farm mechanization and modernization via subsidies and credit programs.

- Growing Global Food Demand:Rising populations underscore the need for efficiency and productivity in crop cultivation.

- Policy Support:Favorable agricultural policies and subsidy frameworks in emerging economies encourage tractor purchases.

- Technological Leap:Launches of efficient mid-HP tractors, rental models, and sustainable powertrain variants fuel growth.

- New Ownership Models:Digital rental and sharing platforms increase tractor access for smallholder and medium-sized farms.

Market Dynamics

Market Drivers

Government Support and Subsidy Programs are Fueling Market Expansion

Government initiatives and subsidy programs play a crucial role in shaping the growth of the market. Many countries are promoting farm mechanization through financial assistance, low-interest loans, and direct subsidies to help farmers purchase tractors and related equipment. These programs make modern machinery more accessible, especially for small and medium-scale farmers who otherwise struggle with high upfront costs. In India, for example, schemes such as the Sub-Mission on Agricultural Mechanization (SMAM) have significantly boosted tractor adoption. Similarly, governments in Africa and Southeast Asia are encouraging tractor imports and local assembly to strengthen rural productivity. This policy-driven support enhances crop yields and operational efficiency and stimulates rural employment and manufacturing activities. As a result, companies are aligning their strategies with these government programs to expand market reach and solidify their competitive positions globally.

Market Restraints

High Initial Investment Costs to Restrict Market Growth

One of the key challenges hindering the agriculture tractor market growth, is the high initial cost of ownership. Tractors, especially those equipped with advanced technologies such as GPS, automation, and telematics, require substantial investment that often exceeds the financial capacity of small and marginal farmers. In developing regions, limited access to credit and high interest rates further discourage farmers from purchasing new equipment. Additionally, maintenance, fuel, and spare parts costs add to the long-term financial burden. While leasing models and government subsidies help mitigate these issues, they are not universally accessible or consistent across regions. As a result, many farmers continue relying on older machinery or shared tractor services, which slows the overall pace of modernizing agriculture. To overcome this restraint, manufacturers are focusing on developing low-cost models, offering flexible financing options, and expanding rural service networks to make tractors more affordable and accessible.

Market Opportunities

Growing Adoption of Electric and Smart Tractors to Create New Market Opportunities

The increasing adoption of electric and smart tractors presents a major opportunity for the future growth of the market. Rising fuel costs and growing environmental concerns are encouraging manufacturers to develop eco-friendly alternatives powered by batteries and hybrid systems. Electric tractors reduce operational expenses and align with global sustainability goals, attracting both farmers and policymakers. At the same time, smart tractors equipped with GPS navigation, IoT sensors, and data analytics are transforming farm management by enabling precision farming and real-time monitoring. Companies such as John Deere, Sonalika, and Kubota are already investing in connected and autonomous tractor technologies to gain an early-mover advantage. The combination of sustainability and digital innovation offers a new growth path for the industry, enhancing productivity while minimizing resource consumption and carbon emissions, key priorities in the modernization of the global agriculture sector.

Market Challenges

Shortage of Skilled Operators Posing a Major Challenge to Market Growth

A significant challenge facing the market is the shortage of skilled and trained operators. While the adoption of modern and technologically advanced tractors is rising, many farmers lack the technical knowledge required to operate and maintain these machines efficiently. The growing use of GPS-based navigation, automation, and smart control systems demands specialized training, which is often unavailable in rural areas. As a result, tractors are sometimes underutilized or operated inefficiently, leading to higher maintenance costs and reduced productivity. In developing countries, limited access to formal training programs and poor awareness about equipment handling worsen the problem. Manufacturers and governments are gradually addressing this issue through farmer education programs, demonstration drives, and operator training centers. However, bridging the skills gap remains critical for ensuring safe operations and maximizing the benefits of mechanization in the global agricultural sector.

Agriculture Tractor Market Trends

Integration of Precision Farming Technologies to Emerge as a Key Market Trend

One of the most prominent trends shaping the agriculture tractor market is the integration of precision farming technologies. Modern tractors are increasingly being equipped with GPS guidance, telematics, and automated control systems that enable farmers to optimize inputs such as seeds, fertilizers, and water with high accuracy. This shift reduces operational costs and improves yield quality and sustainability. Manufacturers such as John Deere, CNH Industrial, and Mahindra & Mahindra are focusing on developing connected tractors capable of real-time data collection and remote diagnostics. The growing availability of affordable sensors and digital tools is also making precision farming accessible to mid-sized farms. As climate challenges and resource constraints intensify, demand for data-driven farming solutions is expected to rise sharply. This trend is transforming tractors from traditional machines into intelligent farming systems, driving efficiency and profitability across the agricultural value chain.

Download Free sample to learn more about this report.

Segmentation Analysis

By Engine Power

41–60 HP Segment to Lead, Driven by Farm Mechanization and Versatility

Based on engine power, the market is classified into upto 30 HP, 31 -40 HP, 41 – 60 HP, 61 – 80 HP, 81 – 100 HP, 101 – 120 HP, 121 – 150 HP, 151 – 180 HP, and 181 HP and above.

The 41–60 HP segment is expected to capture the largest market share and register the highest CAGR during the forecast period. with a share of 24.92% in 2026. The segment is witnessing strong growth due to its ideal balance of power, affordability, and adaptability for diverse farming operations. These tractors are well-suited for medium-sized farms, capable of performing tasks such as plowing, seeding, spraying, and haulage efficiently. Increasing farm mechanization, particularly in developing economies such as India, Brazil, and African nations, is fueling their adoption. Farmers prefer this power range as it supports multiple implements while maintaining fuel efficiency and lower maintenance costs. Government subsidies and easy financing options have also made these tractors more accessible to small-scale farmers. Additionally, manufacturers are introducing technologically upgraded models with enhanced comfort, hydraulic systems, and emission-compliant engines to attract buyers. The combination of cost-effectiveness, versatility, and supportive policies positions the 41–60 HP segment as one of the most dynamic growth drivers in the market.

By Type

Growing Demand for Precision Agriculture Products to Drive Row Crop Segment Growth

In terms of type, the agriculture tractor market is categorized into orchard tractors, row crop tractors, and others.

Row crop will capture the largest market share within the forecast period. with a share of 74.76% in 2026. Demand for row crop tractors is increasing as farmers shift toward precision agriculture products and high-value crop cultivation such as corn, soybeans, and cotton. These tractors offer superior ground clearance, adjustable track widths, and compatibility with modern implements, making them ideal for large-scale farming. Advancements such as GPS guidance and automated controls enhance productivity and reduce labor needs. Leading manufacturers, including John Deere, CNH Industrial, and AGCO, are developing fuel-efficient and smart tractor models to meet evolving farm requirements.

Others segment will grow at the highest CAGR during the forecast period. The expansion of vegetable cultivation and greenhouse farming is boosting the segment’s growth. Farmers are investing in smaller, maneuverable machines for tilling, spraying, and harvesting in tight spaces. Increasing demand for fresh produce and labor shortages are further encouraging mechanization in the vegetable farming sector.

To know how our report can help streamline your business, Speak to Analyst

Agriculture Tractor Market Regional Outlook

By geography, the market is categorized into North America, Europe, CIS, Asia, Oceania, Southeast Asia, South America, Central America, the Middle East, and Africa.

Asia

Asia Agriculture Tractor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific maintained a strong presence in the global market, reaching USD Asia - 32.17 billion in 2025, accounting for Asia - 49.64% share, and is expected to reach USD Asia - 34.16 billion in 2026. The agriculture tractor market in Asia is expanding rapidly, driven by the growing need for farm mechanization and improved agricultural productivity. Countries such as India, China, and Indonesia are witnessing a strong shift from manual labor to mechanized farming due to rising rural wages and labor shortages. Government initiatives, including subsidies, low-interest loans, and machinery promotion schemes, are making tractors more accessible to small and medium farmers. Additionally, the expansion of credit facilities and cooperative financing programs has further boosted tractor purchases across rural areas. Leading manufacturers such as Mahindra & Mahindra, Kubota, and Yanmar are strengthening their local production and dealer networks to meet growing regional demand. Increasing awareness about efficient farming techniques, coupled with the rise of contract and commercial farming, further supports growth. Overall, favorable policies, affordability improvements, and technological advancements are positioning Asia as the fastest-growing market for agricultural tractors globally. The Japan market is projected to reach USD 0.58 billion by 2026, the China market is projected to reach USD 12.96 billion by 2026, and the India market is projected to reach USD 19.89 billion by 2026.

North America

In 2025, the North America market stood at USD 13.09 billion, representing 20.20% of global demand, and is projected to grow to USD 13.84 billion in 2026. North America shows steady growth in agriculture tractor market. The market in North America is driven by the rapid adoption of precision farming and smart technologies. Farmers are increasingly using GPS-enabled and autonomous tractors to improve accuracy, reduce labor dependency, and enhance productivity. Increased demand for high-horsepower models in large-scale commercial farms further supports market growth. Additionally, government incentives promoting sustainable and energy-efficient farming practices are encouraging the adoption of electric and hybrid tractors. The United States market is projected to reach USD 12.61 billion by 2026.

U.S.

The U.S. agriculture tractor market is growing steadily due to increasing adoption of advanced mechanization and precision farming technologies. Farmers are investing in GPS-guided, autonomous, and telematics-enabled tractors to boost efficiency and reduce input costs. Rising labor shortages and the need for higher productivity on large commercial farms are accelerating this shift. Additionally, government support for sustainable agriculture and the growing interest in electric and hybrid tractors are shaping purchasing decisions. Major players such as John Deere and CNH Industrial are expanding digital solutions and localized production, positioning the U.S. as a global leader in smart agricultural machinery.

Europe

The Europe region captured 14.74% of the global market in 2025, generating USD 9.55 billion in revenue, and is projected to reach USD 10.05 billion in 2026. The agriculture tractor market share is considerable in Europe and advancing due to the region’s strong focus on sustainability, precision farming, and automation. Farmers are increasingly adopting advanced tractors integrated with GPS, telematics, and autonomous technologies to enhance productivity and meet stringent environmental regulations. The European Union’s support for green farming and emission reduction initiatives further encourages the use of fuel-efficient and electric tractors. Additionally, modernization of aging farm machinery and rising demand for high-performance equipment in countries such as Germany, France, and Italy are boosting sales. Continuous innovation by manufacturers such as CLAAS, CNH Industrial, and AGCO strengthens regional market growth. The United Kingdom market is projected to reach USD 5.26 billion by 2026, and the Germany market is projected to reach USD 1.68 billion by 2026.

Southeast Asia

The market in Southeast Asia is growing rapidly due to rising farm mechanization and supportive government programs promoting modern agricultural practices. Countries such as Thailand, Vietnam, and Indonesia are encouraging farmers to adopt tractors to improve efficiency and reduce dependency on manual labor. Increasing rural incomes and the availability of affordable financing options are further driving sales. Additionally, expanding rice, palm oil, and sugarcane cultivation creates a strong demand for medium-horsepower tractors suited to local conditions.

COMPETITIVE LANDSCAPE

Innovation, Regional Expansion, and Sustainability Define the Competitive Landscape

The agriculture tractor market is highly competitive, characterized by global and regional players focusing on technological innovation, product diversification, and strategic market expansion. Leading tractor manufacturers such as John Deere, CNH Industrial, Mahindra & Mahindra, Kubota, and AGCO dominate the global landscape through continuous investments in research and development. These manufacturers are prioritizing smart and autonomous tractors integrated with GPS guidance, IoT connectivity, and precision farming systems to meet the growing demand for efficiency and productivity. At the same time, collaborations with agri-tech startups and digital platform integration are becoming central to enhancing customer experience and operational control.

Key players from Asia and Eastern Europe are expanding aggressively through cost-effective models and localized manufacturing to serve small and mid-scale farmers. Companies are also focusing on sustainability, introducing electric and hybrid tractor models to align with emission norms and global climate goals. Expanding aftersales service networks, flexible financing programs, and region-specific product customization further strengthen competitive positioning. With agriculture shifting toward data-driven and sustainable operations, competition is intensifying on performance and price and on technology leadership and lifecycle value delivery, defining the next phase of global tractor industry evolution.

LIST OF KEY AGRICULTURE TRACTOR COMPANIES PROFILED:

- John Deere (U.S.)

- Mahindra Tractors (India)

- TAFE (India)

- TurkTraktor (Turkey)

- AGCO Corporation (U.S.)

- Kubota Corporation (Japan)

- CNH Industrial (United Kingdom)

- YTO (China)

- ARGO SpA (Italy)

- Yanmar Co., Ltd. (Japan)

- SDF Group (Italy)

KEY INDUSTRY DEVELOPMENTS:

- In September 2025, CNH Industrial announced plans for a new tractor manufacturing facility in Greater Noida, India, making the country a strategic hub for both manufacturing and R&D. The plant will boost production capacity to serve Asia and export markets.

- In August 2025, AGCO announced the merger of Allegiance Ag & Turf with True Ag & Turf and the opening of a new Iowa facility. The move aims to streamline sales operations, strengthen dealership presence, and improve aftersales service accessibility across North America.

- In August 2025, Fendt introduced the fourth-generation 1000 Vario tractor alongside the new Optimum planter. The models feature improved engine efficiency, digital controls, and precision planting capabilities aimed at professional farming operations.

- In January 2025, John Deere introduced new autonomous tractors and related equipment using second-generation autonomy kits, showcasing its push into driverless farming solutions.

- In January 2025, John Deere displayed its E-Power battery electric tractor (approx. 130 HP prototype), signaling its commitment toward electrification in agriculture.

REPORT COVERAGE

The global agriculture tractor analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.8% from 2026 to 2034 |

|

Unit |

Value (USD Million) Volume (Units) |

|

Segmentation |

By Engine Power

By Type

By Region

|

Frequently Asked Questions

The global agriculture tractor market size is projected to grow from 68.70 billion in 2026 to $116.30 billion by 2034, growing at a CAGR of 6.80%

In 2025, the market value stood at USD 64.81 billion.

The market is expected to exhibit a CAGR of 6.8% during the forecast period (2026-2034).

By type, the row crop tractors segment is predicted to dominate the market during the forecast period (2026-2034)

Farm mechanization and technological advancements are key factors driving the market.

Leading companies include John Deere, Mahindra, TurkTraktor, CNH Industrial, AGCO Corporation, and Kubota Corporation.

Asia held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us