AI in Endoscopy Market Size, Share & Industry Analysis, By Component (Hardware/Devices and Software & Services), By Deployment (Cloud-based, On-Premise and Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing and Others), By Type (CADe (Computer-Aided Detection), CADx (Computer-Aided Diagnosis) and Others), By Application (Gastrointestinal Endoscopy, Bronchoscopy, Urological Endoscopy, Gynecological Endoscopy, and Others), By End User (Hospitals & ASCs, Specialty Clinics, Academic & Research Institutes and Others), and Regional Forecast, 2026-2034

AI IN Endoscopy Market Size and Future Outlook

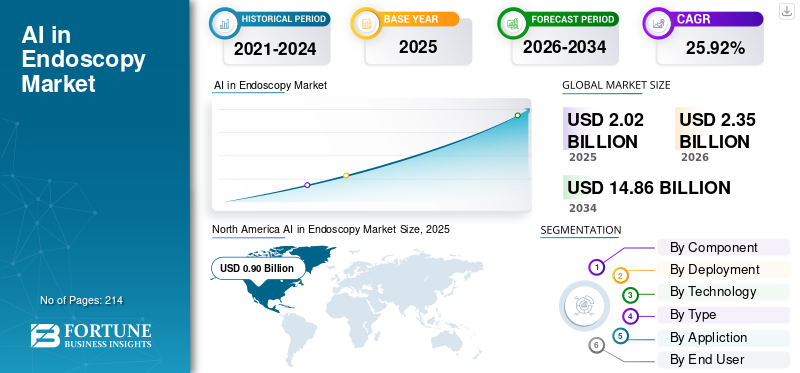

The global AI in endoscopy market size was valued at USD 2.02 billion in 2025. The market is projected to grow from USD 2.35 billion in 2026 to USD 14.86 billion by 2034, exhibiting a CAGR of 25.92% during the forecast period. North America dominated the AI in endoscopy market with a market share of 44.55% in 2025.

AI in endoscopy entails utilizing artificial intelligence, primarily machine learning/deep learning-driven computer vision to a growing extent, natural language processing to assess endoscopy video and procedural data in real-time or nearly real-time. It aids healthcare professionals by enhancing lesion/polyp identification (CADe), facilitating optical characterization (CADx), and bolstering the quality of procedures and workflow consistency through tools such as bowel-prep evaluation, coverage/withdrawal quality reminders and automated documentation/reporting.

Key elements influencing this market growth consists of rising volumes of colorectal cancer screenings and the necessity to enhance adenoma detection rates. This is mounting pressure on endoscopy units to boost throughput without compromising quality and greater incorporation of AI into current endoscopy systems with adaptable cloud/edge deployment models to facilitate quicker software updates and multi-site expansion.

Significant firms including Medtronic, Olympus, FUJIFILM, PENTAX Medical (HOYA) and Iterative Health, are prioritizing product validation, regulatory approvals and enhanced integration within endoscopy ecosystems to boost commercial uptake and capture market presence.

Download Free sample to learn more about this report.

AI IN ENDOSCOPY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.02 Billion

- 2026 Market Size: USD 2.35 Billion

- 2034 Forecast Market Size: USD 14.86 Billion

- CAGR: 25.92% from 2026–2034

- North America dominated the AI in endoscopy market with a 44.55% share in 2025.

- The machine learning & deep learning segment is projected to account for 74.9% of the market in 2026.

- The CADe (computer-aided detection) segment is expected to hold a 68.6% share in 2026.

North America

North America generated USD 0.90 billion in 2025 and remained the largest regional market.

Europe

Europe is projected to grow at a CAGR of 24.91% during the forecast period, supported by strong CRC screening adoption.

Asia Pacific

Asia Pacific is expected to reach USD 0.52 billion by 2026, driven by rising procedure volumes and AI adoption in hospitals.

U.S.

The AI in endoscopy market is projected to reach USD 0.93 billion by 2026, accounting for 39.7% of global revenue.

Japan

The AI in endoscopy market is projected to reach USD 0.11 billion by 2026, representing 4.7% of global revenue.

Read More

AI IN ENDOSCOPY MARKET TRENDS

Integration with Existing Endoscopy Platforms and Cloud/Edge Deployment Models is Emerging Market Trend

Integration with existing endoscopy platforms and flexible cloud/edge deployment is becoming a clear market trend as hospitals want AI that upgrades current rooms without ripping and replacing equipment, while still enabling fast software updates and fleet-wide rollout. Vendors are therefore designing solutions that either plug into existing video chains at the clinical edge (low latency, no workflow disruption) or run in the cloud with remote update capability. This reduces IT friction, speeds procurement decisions and helps providers scale AI across networks rather than single rooms. At the same time, hybrid architectures are gaining traction where hospitals keep sensitive video processing on premises, but use cloud for updates, analytics, and centralized monitoring. These factors are supporting the overall global AI in endoscopy market growth.

- For instance, in September 2024, Odin Medical (Olympus) received the U.S. FDA 510(k) clearance for CADDIE, which is the first cloud-based AI endoscopy system for colonoscopy.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Colorectal Cancer Screening Programs is Boosting Market Growth

Growing Colorectal Cancer (CRC) screening initiatives are broadening the yearly colonoscopy availability, which directly boosts the need for tools that can maintain quality consistently at scale. As more individuals at average risk begin screening (such as USPSTF suggests at age 45), endoscopy units encounter increased throughput demands and more variability among endoscopists, elevating the Adenoma Detection Rate (ADR) as a crucial operational KPI. AI-driven CADe systems are utilized as an effective method to enhance the consistency of polyp/adenoma detection in routine practice, helping to lower miss rates and promote improved screening results within extensive programs. With growing screening volumes, hospitals seek technologies that ensure consistent quality across multiple sites and among less experienced operators, enhancing the ROI argument for AI enhancements. All these factors cumulatively drive the overall market growth.

- For instance, in March 2025, the American Gastroenterological Association (AGA) published guidance on the use of CADe in colonoscopy, reflecting that AI-assisted detection has become mainstream enough to warrant formal guidance and evaluation.

MARKET RESTRAINTS

Regulatory Complexity and Variable Reimbursement Pathways to Hamper Market Growth

Regulatory complexity and inconsistent reimbursement continue to pose significant challenges for AI in endoscopy, as vendors must manage varying evidence criteria, documentation demands, and post-market modification regulations across regions, particularly when models undergo frequent updates. In reality, this delays product releases, raises compliance expenses and complicates the establishment of a unified global regulatory approach for CADe/CADx and workflow AI. From the payer perspective, numerous health systems continue to face challenges regarding the funding of the AI layer, and reimbursement regulations differ significantly by country and even among payers within a country, resulting in inconsistent ROI and postponing procurement. In the U.S., payment for colonoscopy is influenced by coding regulations when screening turns into diagnostic, modifiers and cost-sharing guidelines, resulting in administrative challenges and causing providers to hesitate in adopting add-on technologies without clear reimbursement routes. This results in limiting the market growth to certain extent.

- For instance, In June 2025, the EU’s AI Board and Medical Device Coordination Group (MDCG) issued a document on the interplay between the EU Medical Device Regulations (MDR/IVDR) and the EU AI Act, highlighting additional layers of requirements and coordination for AI medical devices.

MARKET OPPORTUNITIES

Increased Investment by OEMs and AI Vendors to Commercialize Validated Products Offer Market Growth Opportunities

Rising funding from endoscopy OEMs and AI suppliers presents a significant market opportunity, as it facilitates the transition of AI from pilot projects into verified, regulated products suitable for large-scale deployment. OEM funding speeds up clinical validation, regulatory submissions, and "fit-to-workflow" integration, enabling hospitals to implement AI smoothly while maintaining their current endoscopy rooms. Simultaneously, AI providers gain from OEM distribution, service networks, and access to installed bases, lowering the time and expense to market across various areas. This also facilitates a transition from single-use CADe to more extensive portfolios, boosting revenue for each installed location. With the introduction of regulated solutions into standard procurement processes, uptake extends from early adopters to community hospitals and ASCs, broadening the market potential. All these factors would drive the market growth in the coming years.

- For instance, in March 2024, FUJIFILM Healthcare Americas announced it received the U.S. FDA 510(k) clearance for CAD EYE, describing it as an AI detection system integrated with Fujifilm’s endoscopy ecosystem and commercially launched after limited market evaluation, illustrating OEM-led investment to commercialize validated AI products.

MARKET CHALLENGES

High Implementation Costs Pose a Prominent Challenge to Market Growth

High implementation costs and IT-readiness are market challenges, especially for smaller hospitals. Healthcare sites often need capital for the AI module/device, ongoing software subscriptions, plus integration work. Many smaller hospitals also have lean IT teams, so validating connectivity, data governance, and downtime-risk can slow approvals and increase total cost of ownership. A recent clinical implementation review in gastroenterology highlights that cost-effectiveness and reimbursement and associated implementation hurdles remain major barriers to deploying AI in routine practice. In parallel, healthcare cybersecurity risk is rising, pushing providers to spend more on secure infrastructure, an added hurdle for resource-constrained sites. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Component

Increasing Demand from Hospitals to Propel Hardware/Devices Segmental Growth

Based on the component, the market is divided into software & services and hardware/devices.

The hardware/devices segment captured the largest global AI in endoscopy market share. This is due to most buyers including hospitals prefer a turnkey, validated device that plugs into existing endoscopy towers with minimal workflow disruption, which accelerates procurement versus building custom IT stacks. Additionally, increasing number of collaborations & partnerships between operating players also supported the segment growth.

- For instance, in November 2024, Medtronic announced that the U.S. Department of Veterans Affairs awarded a 3-year contract for GI Genius AI-powered endoscopy units, enabling installation of nearly 100 additional units across VA medical centers.

The software & services segment is anticipated to rise with a CAGR of 29.46% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

High Number Installations of On-premise Solutions Supported Segmental Dominance

Based on the deployment, the market is divided into on-premise, cloud-based, and hybrid.

The on-premise segment captured largest market share in 2025. This is attributed to the fact that hospitals prefer on-premise setups to keep endoscopy video within their own network for data governance, cybersecurity review and clinical risk control, rather than routing feeds externally. Integration is simpler as well as many solutions are designed to sit in line with existing endoscopy towers/processors, so IT changes are limited and uptime is easier to manage. Furthermore, the segment is set to hold 49.6% share in 2026.

- For instance, in May 2025, the U.S. FDA provided clearance letter for Iterative Health’s SKOUT system, classifying it as a gastrointestinal lesion software detection system. It is a workflow typically deployed to support real-time detection in the endoscopy suite, reinforcing on-premise deployments resulting in its dominant mode.

The cloud-based segment is anticipated to rise with a CAGR of 39.64% over the forecast period.

By Technology

High Usage in Various Applications to Enable Segmental Dominance of Machine Learning & Deep Learning

In terms of technology, the market is divided into natural language processing, machine learning & deep learning and others.

The machine learning & deep learning segment dominated the global market in 2025. ML/DL based tasks rely on computer vision models that can process high-frame-rate images with low latency in the procedure room, which is where deep learning performs best. As hospitals scale screening, they need consistent detection performance across operators and ML/DL models can be trained on large annotated video datasets to reduce miss risk and standardize outcomes. Furthermore, the segment is set to hold 74.9% share in 2026.

- For instance, in April 2024, Medtronic announced the launch of ColonPRO, the latest-generation AI software for the GI Genius intelligent endoscopy system.

The natural language processing segment is anticipated to rise with a CAGR of 35.78% over the forecast period.

By Type

Increasing Focus on Screening Programs to Boost Segmental Growth of CADe

In terms of type, the market is divided into CADe (computer-aided detection), CADx (computer-aided diagnosis) and others.

The CADe (computer aided detection) segment captured the highest share of the global market in 2025. The segment addresses the most frequent, scalable pain point in routine practice. It is also easier to standardize operationally as CADe works as a real-time second observer on the video feed and doesn’t require deep changes to clinical decision pathways. Additionally, new product launches by operating players also supported the segment growth. Furthermore, the segment is set to hold 68.6% share in 2026.

- For instance, in September 2025, Olympus announced the U.S. commercial launch of the OLYSENSE platform with CADDIE, its first computer-aided detection (CADe) solution for colonoscopy.

The CADx (computer-aided diagnosis) segment is anticipated to rise with a CAGR of 33.67% over the forecast period.

By Application

High Usage in Gastrointestinal Endoscopy to Boost Segmental Growth

On the basis of application, the market is divided into gastrointestinal endoscopy, bronchoscopy, urological endoscopy, gynecological endoscopy and others.

The gastrointestinal endoscopy segment captured the highest share of the global market in 2025. This is owing to the fact that it has the largest, most standardized procedure base where AI can be deployed at scale, especially colonoscopy for CRC screening. GI workflows are also highly repeatable making it easier to train, validate and commercialize ML/DL models compared to more fragmented non-GI endoscopy pathways. Moreover, hospitals and ASCs prioritize GI as improving detection in high-volume screening directly supports clinical outcomes and quality metrics, which strengthens procurement decisions. Furthermore, the segment is set to hold 80.2% share in 2026.

- For instance, in October 2024, GI Alliance announced a strategic collaboration with Medtronic to make the GI Genius intelligent endoscopy module available across more than 400 sites.

The urological endoscopy segment is anticipated to rise with a CAGR of 34.45% over the forecast period.

By End User

High Utilization by Hospitals & ASCs to Support Segment’s Leading Position

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, academic & research institutes and others.

In 2025, the hospitals & ASCs segment held the leading position in the global market. These run the highest procedure volumes and therefore capture the strongest ROI from AI. As adoption expands, hospitals and ASCs remain the primary buyers as they can scale installations across networks and negotiate bundled device, software and service contracts. Furthermore, the segment is set to hold 69.0% share in 2026.

- For instance, in August 2024, Northside Hospital announced it began using Medtronic’s GI Genius during colonoscopies and stated the AI-assisted colonoscopy would be available across all five Northside hospitals and six outpatient endoscopy centers.

In addition, specialty clinics are projected to witness a 30.61% growth rate during the forecast period.

AI In Endoscopy Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America AI in Endoscopy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 0.78 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 0.90 billion. Prominent factors such as high CRC screening volumes, faster hospital/ASC purchasing cycles, and higher willingness to pay for device, subscription, services bundles have propelled the market growth.

U.S. AI in Endoscopy Market

The U.S. dominated North American market and can be analytically approximated at around USD 0.93 billion in 2026, accounting for roughly 39.7% of global market.

Europe

Europe market is anticipated to grow at 24.91% CAGR during the forecast period. Europe’s growth is supported by wide CRC screening coverage, strong adoption in large public hospital systems and academic centers, and other factors.

U.K. AI in Endoscopy Market

The U.K. market in 2026 is estimated at around USD 0.13 billion, representing roughly 5.3% of global revenues.

Germany AI in Endoscopy Market

Germany market is projected to reach approximately USD 0.16 billion in 2026, equivalent to around 6.7% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 0.52 billion by 2026, making it the third largest region in the worldwide sector. The Asia Pacific regional growth is driven by large and growing procedure volumes, rising number of private hospital chains and urban specialty centers adopting AI, and increasing uptake in advanced markets such as Japan, South Korea, Australia, and China.

Japan AI in Endoscopy Market

The Japan market in 2026 is estimated at around USD 0.11 billion, accounting for roughly 4.7% of global revenues.

China AI in Endoscopy Market

China’s market is projected to reach revenues of around USD 0.13 million in 2026, representing roughly 5.5% of global sales.

India AI in Endoscopy Market

The India market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 3.6% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are expected to experience slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.14 billion by 2026. Key elements such as gradual expansion of endoscopy capacity, increasing healthcare infrastructure investments, rising burden of GI diseases and preventive care initiatives are anticipated to propel market expansion.

In the Middle East and Africa region, the GCC market is projected to reach approximately USD 0.04 billion by 2026, representing about 1.7% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on OEM Ecosystem Integration and Regulatory-Cleared CADe/CADx Portfolios to Strengthen Market Share

The competitive landscape of the market is moderately fragmented, with large endoscopy OEMs and medtech incumbents competing alongside specialist AI software vendors. Prominent players include Medtronic, Olympus Corporation, FUJIFILM Holdings Corporation, PENTAX Medical, and AI-focused specialists such as Iterative Health and Odin Medical. These companies are increasingly emphasizing regulatory clearances, enterprise-scale rollouts and cloud/edge deployment flexibility to reduce adoption friction and strengthen their installed base across GI endoscopy first, then adjacent endoscopy applications.

- For instance, in October 2024, Olympus announced CE approval (under EU MDR) for three cloud-based AI endoscopy devices—CADDIE, CADU, and SMARTIBD—via its group company Odin Medical, and outlined plans to launch an AI-powered endoscopy ecosystem.

Other significant players include AI Medical Service Inc., Wision A.I., Body Vision Medical, Endovision, and others. These players are increasingly focusing on new product launches, AI platform expansion, and partnerships to widen adoption across hospitals networks.

LIST OF KEY AI IN ENDOSCOPY COMPANIES PROFILED

- Medtronic (U.S.)

- Olympus Corporation (Japan)

- FUJIFILM Holdings Corporation (Japan)

- PENTAX Medical (Japan)

- Iterative Health (U.S.)

- AI Medical Service Inc. (Japan)

- Wision A.I. (China)

- Body Vision Medical (U.S.)

- Endovision (India)

- MAGENTIQ EYE (Israel)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Olympus Corporation reported EAGLE trial results showing its CADDIE AI solution aids detection of high-risk and hard-to-detect colorectal lesion.

- February 2026: PENTAX Medical announced a strategic presence at Connect Labs by Wexford (The Pearl Innovation District) to advance endoscopic innovation and clinical education.

- July 2025: Olympus Corporation entered an agreement with Revival Healthcare Capital to co-found Swan EndoSurgical to develop endoluminal GI robotics for less invasive therapeutic endoscopy.

- April 2025: PENTAX Medical announced partnership with IRCAD Africa to advance flexible endoscopy training in Rwanda, including equipment support.

- January 2025: Iterative Health announced Unio Specialty Care is implementing SKOUT to bring AI-enhanced colorectal cancer screenings across California ASCs.

REPORT COVERAGE

The global AI in endoscopy market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global AI in endoscopy market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 25.92% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Type, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.02 billion in 2025 and is projected to reach USD 14.86 billion by 2034.

In 2025, the North America market value stood at USD 0.90 billion.

The market is expected to exhibit a CAGR of 25.92% during the forecast period of 2026-2034.

By component, the hardware/devices segment is expected to lead the market.

Rising colorectal cancer screening programs and demand to improve adenoma detection rates are primarily driving market expansion.

Medtronic, Olympus Corporation, FUJIFILM Holdings Corporation, and PENTAX Medical are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 214

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us