Thermal Interface Materials Market Size, Share & Industry Analysis, By Type (Pads & Gap Fillers, Greases & Pastes, and Others), By End-use (Automotive, Consumer Electronics, Data Center & Telecom, Industrial & Energy, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

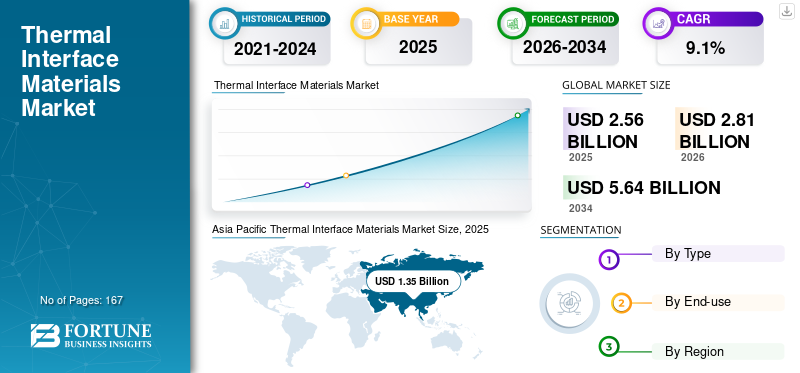

The global thermal interface materials market size was valued at USD 2.56 billion in 2025. The market is projected to grow from USD 2.81 billion in 2026 to USD 5.64 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period. Asia Pacific dominated the global thermal interface materials market with a market share of 52.37% in 2025.

Thermal Interface Materials (TIMs) are thermally conductive substances positioned between heat-generating electronic components and heat spreaders or heat sinks to eliminate air gaps, enhance surface contact and decrease interface thermal resistance. Commercial categories of TIMs comprise gap-filler pads and sheets, thermal greases and pastes, phase change materials, as well as films, tapes and graphite-based interfaces designed for slim form factors. Basically, available as sheets, pads, disposable pastes and gels, or preforms, TIMs are required to meet stringent standards for thermal performance, electrical insulation, processability and long-term reliability under thermal cycling and vibration conditions.

A principal factor driving market growth is the increasing thermal load and power density in semiconductors, data centers, and telecommunications infrastructure, as well as vehicle electrification. The World Semiconductor Trade Statistics (WSTS) project predicts that the global semiconductor market will reach USD 700.9 billion in 2025, representing an 11.2% year-over-year increase, and USD 760.7 billion in 2026, up 8.5% year-over-year, thereby supporting the ongoing scaling of high-heat-flux computing and advanced packaging.

Furthermore, the market is dominated by several major players, including Henkel, Dow, 3M, Shin-Etsu Chemical, and Parker Hannifin, which are at the forefront. A broad portfolio, innovative product launches and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Thermal Interface Materials Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.56 billion

- 2026 Market Size: USD 2.81 billion

- 2034 Forecast Market Size: USD 5.64 billion

- CAGR: 9.1% from 2026–2034

- Asia Pacific dominated the market with a 52.37% share in 2025.

- Pads & Gap Fillers segment held the largest market share in 2025.

- Data Center & Telecom segment is projected to grow at a CAGR of 13.1%.

Asia Pacific

USD 1.35 billion in 2025. Dominated by large-scale electronics, semiconductor packaging, and consumer device manufacturing.

North America

USD 0.62 billion in 2026. Growth driven by AI/cloud data centers, aerospace, and advanced electronics demand.

Europe

USD 0.52 billion in 2026. Supported by EV electrification, industrial applications, and strict quality standards.

U.S.

USD 0.54 billion in 2026. Driven by data centers, aerospace, defense, and advanced electronics industries.

Japan

USD 0.20 billion in 2026. Demand supported by electronics manufacturing and high-performance industrial applications.

Read More

THERMAL INTERFACE MATERIALS MARKET TRENDS

Reliability-First, High-Conductivity, and Processable TIMs for High-Power Electronics Are Emerging Market Trends

A notable market trend is the transition from traditional "commodity” gap-filling pads and greases to advanced TIMs that offer enhanced thermal conductivity, coupled with improved manufacturability, including dispensing stability, reduced cycle times and compatibility. Additionally, automation and increased reliability under rigorous thermal cycling and vibrational conditions also reshapes the market growth. This trend is particularly prominent in automotive power electronics and Advanced Driver-Assistance Systems (ADAS)/computing controllers, where escalating operating temperatures and power densities are observed.

MARKET DYNAMICS

MARKET DRIVERS

AI/Cloud Infrastructure and Power Electronics Are Increasing TIM Intensity per System

The consumption of TIM is increasingly driven not only by unit volumes, such as servers, vehicles, and industrial converters, but also by rising material intensity per system as heat flux and component count increase. In the data and telecommunications sectors, larger heat sources, including high-TDP CPUs and GPUs, HBM stacks and power delivery components, heighten the demand for engineered greases, dispensable gap fillers and thicker, highly conformable pads that ensure contact across various tolerances.

Macro demand signals corroborate this trajectory as WSTS forecasts sustained growth in the semiconductor industry through 2026, whereas the IEA reports an accelerating adoption of electric vehicles and increasing demand for data-center power across various scenarios, both of which fundamentally elevate thermal management requirements. Consequently, thermal interface materials market growth is positively affected by both increased unit volumes and enhanced thermal management content per platform.

MARKET RESTRAINTS

Qualification Cycles, Cleanliness Requirements and Reliability Validation Can Slow Market Growth

TIMs are frequently validated at both the module and system levels, especially within the automotive and mission-critical industrial & energy sectors. The transition between different TIM chemistries (e.g., varying filler systems, Greases & Pastes versus non-Greases & Pastes) may necessitate new qualification procedures for thermal cycling, vibration, outgassing, dielectric performance and long-term aging, thereby delaying supplier transitions even when performance enhancements are achieved.

Furthermore, process constraints, including dispensing repeatability for gap fillers, maintaining a stable bondline for greases, and ensuring consistent compression behavior for pads, establish a significant “process risk” barrier for the adoption of new materials. Consequently, extensive validation requirements and stringent cleanliness and reliability standards may hinder the prompt substitution of materials.

MARKET OPPORTUNITIES

Automation-Ready and Rework-Friendly TIMs Enable Higher Yields and Faster Assembly

A substantial opportunity presents itself for TIMs designed for high-volume manufacturing: pads compatible with robotic placement, cure-in-place or dispensable gels exhibiting stable rheology, and low-bleed, low-volatility materials that sustain performance over broad operating ranges. This directly benefits Electric Vehicle (EV) battery production lines, power-module assembly, and server manufacturing, where take time and yield are of utmost importance.

Suppliers are also progressing toward the implementation of “design-for-service” methodologies through the utilization of TIMs that facilitate controlled debonding or clean rework within electronic repair cycles, all while maintaining in-use reliability. Consequently, automation-optimized and rework-friendly TIM systems have the potential to unlock incremental volume and value in applications experiencing high growth.

MARKET CHALLENGES

Filler Cost, Supply Risk, and Narrow Process Windows Create Margin and Adoption Pressure

The cost structure of numerous TIMs is affected by specialty polymers and high-load thermally conductive fillers. As conductivity objectives increase, formulations frequently necessitate costlier filler systems and stricter quality control measures, potentially reducing margins in price-sensitive consumer electronics or high-volume automotive platforms.

Furthermore, numerous deployments necessitate strict process constraints such as precise control of thickness (pads/PCMs), consistent dispensing patterns and void management (gels), as well as stable long-term properties under cyclic conditions. Consequently, achieving an optimal balance between cost, manufacturability and reliability at scale continues to represent a significant operational challenge.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Pads & Gap Fillers Dominate the Market Supported by Gap-Tolerance Requirements

Based on type, the market is segmented into pads & gap fillers, greases & pastes and others.

The pads & gap fillers segment led the thermal interface materials market share in 2025, supported by its ability to bridge larger tolerances and uneven surfaces in EV battery packs, power modules, and electronics enclosures, while also providing vibration damping.

Other TIMs (PCM/graphite/tapes) are anticipated to experience the most rapid growth within the model, primarily due to their adoption in thin form factors and high-heat-flux interfaces where maintaining consistent bondline control and ensuring low contact resistance are significant. Consequently, the segment growth is also projected in advanced computing applications and select automotive electronics as designs evolve to accommodate higher power densities.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Data Center & Telecom Segment to grow with the Fastest CAGR Due to AI-Driven Compute Expansion and Rising Rack Power Density

In terms of end-use, the market is categorized into automotive, consumer electronics, data center & telecom, industrial & energy and others.

The data center & telecom segment is expected to grow with the fastest CAGR, driven by the AI-driven compute expansion and rising rack power density that increase TIM requirements per server and per accelerator. The IEA’s analysis of energy demand from AI highlights rapid growth in data-centre electricity consumption across scenarios, supporting the structural expansion of this segment. Additionally, it is projected that this segment will expand at a CAGR of 13.1% over the study period.

The automotive sector is experiencing significant growth, as EV platforms increase TIM intensity across batteries, inverters, onboard chargers and thermal management system. The IEA reported electric car sales exceeding 17 million in 2024, which increases the installed base of platforms using high volumes of gap fillers and pads.

Thermal Interface Materials Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Thermal Interface Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the dominant share in 2024, valued at USD 1.21 Billion, and also took the leading share in 2025 with USD 1.35 billion. Asia Pacific leads global TIM consumption, driven by large-scale production of smartphones, PCs, consumer devices, and the world’s largest semiconductor packaging and electronics manufacturing clusters.

China Thermal Interface Materials Market

In 2026, the China market is estimated to reach USD 0.67 billion. China is the largest demand center in Asia Pacific region, driven by the scale of electronics manufacturing, high-volume consumer devices, and accelerating deployment of EV powertrains and charging infrastructure.

To know how our report can help streamline your business, Speak to Analyst

Japan Thermal Interface Materials Market

The Japan market in 2026 is estimated to be around USD 0.20 billion, accounting for roughly 7.2% of the global revenues.

India Thermal Interface Materials Market

The India market in 2026 is estimated at around USD 0.12 billion, accounting for roughly 4.5% of global revenues.

Europe

Europe is expected to experience significant growth in the market in the coming years. During the forecast period, the European region is projected to record a growth rate of 7.6% and reach the valuation of USD 0.52 billion in 2026. Europe is characterized by automotive electrification and high-reliability industrial applications where documentation and qualification standards are rigorous.

U.K. Thermal Interface Materials Market

The U.K. market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 2.0% of global revenues.

Germany Thermal Interface Materials Market

Germany’s market in 2026 is estimated at around USD 0.11 billion, accounting for roughly 3.8% of global revenues.

North America

The market in North America is estimated to reach USD 0.62 billion in 2026 and secure the position of the second-largest region in the market. North America is a high-value regional market supported by AI/cloud data-center deployment, advanced electronics and aerospace/defense and industrial applications.

U.S. Thermal Interface Materials Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.54 billion in 2026, accounting for roughly 19.3% of global sales.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2026 is expected to reach a valuation of USD 0.10 billion. Latin America and the Middle East & Africa are comparatively smaller markets but are growing with electronics assembly, industrial systems, and renewable energy infrastructure.

GCC Thermal Interface Materials Market

The GCC market in 2026 is estimated to be around USD 0.03 billion, accounting for approximately 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Application Engineering, Reliability Data, and Local Supply Footprint Aids in Key Players Dominance

The market exhibits moderate fragmentation, with global materials suppliers competing alongside specialist thermal-management formulators. Competitive advantage is built on application engineering (bondline control, dispensing/placement process design), reliability testing support (thermal cycling, pump-out/bleed resistance, vibration stability), and a regional manufacturing footprint near electronics production clusters. Large incumbents also leverage broad portfolios across pads, gels, greases, and phase-change systems to provide platform-level solutions. Henkel, Dow, 3M, Shin-Etsu Chemical, and Parker Hannifin are some of the key players in the market.

LIST OF KEY THERMAL INTERFACE MATERIALS COMPANIES PROFILED

- Henkel (Germany)

- 3M (U.S.)

- Parker Hannifin (U.S.)

- Dow (U.S.)

- Shin-Etsu Chemical (Japan)

- Wacker Chemie (Germany)

- Momentive (U.S.)

- Fujipoly (Japan)

- Honeywell Electronic Materials (U.S.)

- Indium Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Henkel introduced Bergquist TGF 10000, a 10 W/mK liquid gap filler positioned for high-power electronics across automotive, telecom, computing and network infrastructure.

- November 2025: Parker Chomerics introduced THERM-A-GAP GEL 120, a dispensable thermal gap filler gel positioned as a very-high-conductivity option for demanding electronics cooling.

- June 2025: WACKER announced SEMICOSIL 9649 TC, a new thermally conductive gap filler for EV power electronics, at Battery Show Europe 2025.

- March 2025: Indium Corporation announced the introduction of Heat-Spring HSx, a metal TIM pattern designed for large-area dies with warpage/pressure constraints, to be showcased at TestConX 2025.

- October 2024: Dow and Carbice announced a strategic partnership to develop multi-generational thermal interface materials using aligned carbon nanotube (CNT) technology for mobility, industrial, consumer and semiconductor

REPORT COVERAGE

The global thermal interface materials market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market shares and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.1% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Type, End-use and Region |

|

By Type |

· Pads & Gap Fillers · Greases & Pastes · Others |

|

By End-use |

· Automotive · Consumer Electronics · Data Center & Telecom · Industrial & Energy · Others |

|

By Geography |

· North America (By Type, End-use, and Country) o U.S. (By End-use) o Canada (By End-use) · Europe (By Type, End-use, and Country/Sub-region) o Germany (By End-use) o U.K. (By End-use) o France (By End-use) o Italy (By End-use) o Rest of Europe (By End-use) · Asia Pacific (By Type, End-use, and Country/Sub-region) o China (By End-use) o Japan (By End-use) o India (By End-use) o South Korea (By End-use) o Rest of Asia Pacific (By End-use) · Latin America (By Type, End-use, and Country/Sub-region) o Brazil (By End-use) o Mexico (By End-use) o Rest of Latin America (By End-use) · Middle East & Africa (By Type, End-use, and Country/Sub-region) o GCC (By End-use) o South Africa (By End-use) o Rest of the Middle East & Africa (By End-use) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.56 million in 2025 and is projected to reach USD 5.64 million by 2034.

The market is projected to grow at a CAGR of 9.1% during the forecast period of 2026-2034.

The automotive end-use segment led in 2025.

Asia Pacific held the highest market share in 2025.

Growing demand for EV, power inverters, and battery thermal management solutions is accelerating the adoption of thermal interface materials.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us