AI in Medical Writing Market Size, Share & Industry Analysis, By Component (Software and Services), By Technology (Machine Learning & Deep Learning, Natural Language Processing, and Others), By Deployment (Cloud-Based, On Premise, and Hybrid), By Therapeutic Area (Oncology, Central Nervous System, Infectious Diseases, Rare Diseases, Immunology, Cardio-metabolic, and Others), By Application (Regulatory writing, Clinical writing, Scientific Publications & Medical Communications, Safety/Pharmacovigilance Writing, & Others), By End User, and Regional Forecast, 2026-2034

AI in Medical Writing Market Size and Future Outlook

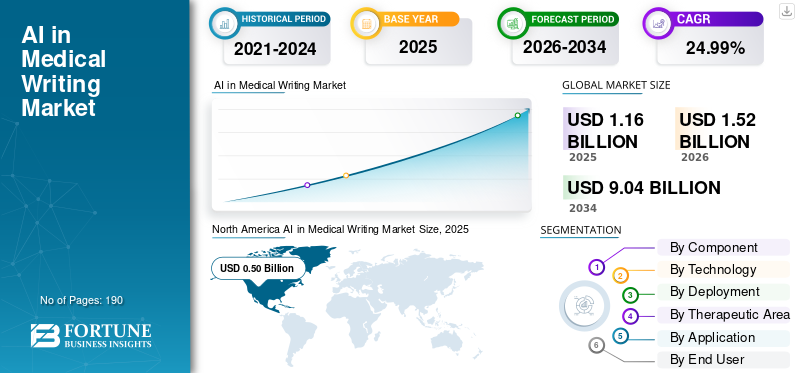

The global AI in medical writing market size was valued at USD 1.16 billion in 2025. The market is projected to grow from USD 1.52 billion in 2026 to USD 9.04 billion by 2034, exhibiting a CAGR of 24.99% during the forecast period. North America dominated the AI in medical writing market with a market share of 43.10% in 2025.

The global AI in medical writing market is expected to grow steadily over the coming years, driven by the need to accelerate document creation across clinical and regulatory workflows. Pharmaceutical and biotechnology companies are adopting these AI tools to reduce manual effort and improve consistency for high-volume documents such as clinical study reports, regulatory submissions, and medical content. Additionally, rising pressure to improve compliance, reduce turnaround time, and control costs is encouraging these companies to adopt AI-supported writing platforms with human oversight.

As more companies focus on launching new specialized solutions for regulated writing, the market is expected to gain stronger adoption across the pharmaceutical industry.

- For instance, in July 2025, Indegene launched NEXT Medical Writing Automation, a generative AI-enabled platform designed to streamline complex medical writing workflows across clinical development and regulatory submissions. The platform helped accelerate the creation of high-quality, compliant documents, improve consistency, and support scale in medical writing operations. Such product launches are expected to strengthen confidence in AI-led medical writing tools and support overall growth in the market.

Leading players in the industry, such as Indegene, Certara, IQVIA, and Veeva Systems Inc., are focusing on expanding their offerings to strengthen their market positions.

Download Free sample to learn more about this report.

AI IN MEDICAL WRITING MARKET TRENDS

Growing Preference for Human-in-the-Loop AI Writing Models is a Significant Market Trend

The growing preference for human-in-the-loop AI writing models is emerging as a key trend in the global market. Medical writing in the life sciences industry requires high accuracy, scientific clarity, and strong compliance control. These factors make full automation difficult in regulated workflows. Due to this, companies are increasingly adopting AI models that support writers, enabling teams to improve speed while maintaining expert review and decision-making. This balance between automation and human oversight is increasing trust in AI tools and is helping the market move from experimentation toward practical adoption in regulatory and clinical writing.

Key companies are focusing on novel product launches to enhance their offerings and strengthen their market position.

- For instance, in July 2025, Indegene launched NEXT Medical Writing Automation, a generative AI-enabled platform designed to streamline complex medical writing workflows across clinical development and regulatory submissions. The company stated that the platform helps accelerate the creation of high-quality, compliant documents, improve consistency, and support scale in medical writing operations. Such product launches are expected to strengthen confidence in AI-led medical writing tools and support overall global AI in medical writing market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Consistent and High-Quality Scientific Documentation to Drive Market Growth

The rising demand for consistent, high-quality scientific and clinical documentation is driving the growth of the global market. Medical, regulatory, and clinical documents need to follow a clear structure, use accurate scientific language, and adhere to strict compliance and regulatory standards, which makes consistency across the writing process very important. However, manual writing and review often lead to delays, variation in document quality, and rework across teams and regions. As a result, life sciences companies are increasingly adopting AI-enabled medical writing tools that help standardize content, improve document quality, and reduce turnaround time while maintaining human oversight. This is expected to increase the use of the product across the regulated workflow.

- For instance, in July 2025, Indegene launched NEXT Medical Writing Automation, a generative AI-enabled platform designed to streamline complex medical writing workflows across clinical development and regulatory submissions. The company stated that the platform helps accelerate the creation of high-quality, compliant documents while improving consistency and enabling scale. Such developments are expected to support greater adoption of AI tools for scientific and regulatory documentation.

MARKET RESTRAINTS

Data Privacy and Governance Concerns Restraining Growth of Global Market

Data privacy and governance concerns are restraining the growth of the global market. Medical writing often involves sensitive clinical, regulatory, and product-related information, so companies cannot adopt AI tools unless they are confident in their data security, access controls, and compliance oversight. Due to this, many organizations move carefully and take longer to validate new AI platforms before using them in regulated workflows. This increases implementation time, raises deployment costs, and slows wider market adoption, especially among companies handling highly confidential submission and trial-related content.

- For instance, in May 2024, Yseop announced that it had developed an enhanced generative AI application for regulatory document generation across the biopharma industry, with support from AWS, and specifically highlighted security and scalability as key elements of the solution. This shows that vendors in the market must address privacy and governance requirements robustly before customers can use AI in regulated medical writing environments.

MARKET OPPORTUNITIES

Growing Investments in Specialized AI Platforms for Life Sciences Documentation Creating a Strong Market Growth Opportunity

Medical writing in life sciences involves highly structured, scientific, and compliance-driven documents, so generic AI tools are often not enough to meet industry-specific needs. Due to these reasons, companies are increasingly investing in purpose-built AI platforms that can connect clinical data, regulatory content, and document workflows in a more controlled and usable way. This is improving the practical value of AI in regulated writing environments and creating new growth opportunities for vendors that offer specialized solutions tailored to life sciences documentation needs.

- For instance, in August 2025, Altasciences announced a strategic collaboration with Evidence Matters to advance AI-enhanced text engineering for regulatory writing in life sciences. The company stated that Evidence Matters' RegulatoryFlow platform and specialized services help unify clinical data and documents, simplify workflows, and accelerate the work of medical writers and regulatory specialists. This reflects how rising investment in specialized AI platforms is opening new growth opportunities in the medical writing market.

MARKET CHALLENGES

Risks Associated with Clinical Accuracies Pose Significant Challenges for Market Expansion

One of the key challenges faced by the market is clinical accuracy and AI hallucinations in medical writing. Additionally, the continued need for clinical review and human-in-the-loop workflows is challenging the growth of the global market. Medical and regulatory documents require precise scientific language, accurate interpretation of data, and robust compliance controls. Even small AI-generated errors can create serious review and regulatory risks. As a result, companies cannot rely on AI outputs alone and must keep experienced medical, regulatory, and clinical reviewers involved throughout the writing process. This reduces the level of automation achievable, increases the review burden, and slows broader adoption of the service, especially for high-stakes submissions and scientific content.

- For instance, in January 2025, Apple suspended its AI-generated news summary feature in beta software after the system produced inaccurate and fabricated summaries. This was a negative example of how AI-generated content can appear reliable while still being wrong, which highlights why life sciences companies remain cautious about using AI without strong human review in medical writing workflows.

Segmentation Analysis

By Component

Software Segment Led the Segment due to Rising Investment in Platforms to Improve Drafting Speed

Based on component, the market is categorized into software and services.

The software segment accounted for the largest share of the global market. Software is estimated to hold a dominant market share as most buyers first invest in platforms that can directly improve drafting speed, document consistency, review workflows, and compliance control across multiple writing tasks. Software tools are easier to scale across teams and geographies than service-heavy models, and they deliver repeatable productivity gains by connecting templates, content libraries, workflows, and AI capabilities in a single environment. Due to this, companies have shown a stronger interest in AI-enabled writing platforms that can be embedded into existing regulatory, clinical, and medical content processes.

- For instance, in December 2025, Ennov introduced Ennov 11.0, which integrated AI into its platform for Regulatory, Clinical, Quality, and Pharmacovigilance teams. The company highlighted capabilities such as document Q&A, eCTD auto-classification, and case narrative summarization inside a secure, traceable environment. Such platform-led launches support the dominance of software in this market.

The services segment is expected to grow at a CAGR of 22.18% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Natural Language Processing Segment Led due to its Ability to Reduce Manual Drafting Effort

Based on technology, the market is segmented into machine learning & deep learning, natural language processing, and others.

In 2025, natural language processing dominated the market, as medical writing is largely built around language-intensive tasks such as drafting, summarizing, reusing content, checking consistency, and converting structured data into readable scientific text. Compared with traditional ML-only approaches, NLP/GenAI can work more directly on narratives, regulatory sections, literature-based content, and response documents, which makes the technology more immediately useful for real writing workflows. As these tools can reduce manual drafting effort while still allowing reviewer oversight, adoption has been stronger in this segment than in more limited automation approaches. Key companies are focusing on technologically advanced offerings and the regulatory approvals that accompany them to strengthen their market position.

- For instance, in April 2025, Veeva Systems announced Veeva AI, adding AI Agents and AI Shortcuts across the Veeva Vault Platform and applications spanning clinical, regulatory, safety, quality, medical, and commercial functions. The company announced that the initiative is designed to automate industry-specific tasks and improve productivity, which reflects the strong momentum behind NLP/GenAI-led solutions in medical writing environments.

The machine learning & deep learning segment is projected to grow at a CAGR of 23.83% during the forecast period.

By Deployment

Cloud-Based Segment Led owing to its Ability to Integrate Data Sources

Based on deployment, the market is segmented into cloud-based, on-premises, and hybrid.

In 2025, the cloud-based deployment accounted for the largest market share. Cloud-based deployment dominated the market as AI medical writing tools work better when teams can access shared content, central workflows, and updated models across multiple functions and locations. Cloud environments also make it easier to integrate data sources, standardize templates, support collaboration, and roll out upgrades faster than on-premise systems. As life sciences companies increasingly seek scalable, interoperable digital environments, cloud-based deployment has become the preferred model for many new AI-enabled writing and content programs.

- For instance, in May 2025, Salesforce announced a certified partner network to accelerate customer migration to Life Sciences Cloud, which it described as a HIPAA-ready, pre-validated, GxP-compliant platform. The company also highlighted how customers can deploy Agentforce and connect data across clinical, medical, and commercial units.

The hybrid segment is projected to grow at a CAGR of 17.35% over the study period.

By Therapeutic Area

High Documentation Density and Elevated Use Case of Oncology Led the Segment Growth

Based on therapeutic area, the market is segmented into oncology, central nervous system, infectious diseases, rare diseases, immunology, cardio-metabolic, and others.

In 2025, oncology dominated the market as it generates a very high volume of clinical trials, regulatory activity, scientific publications, compared with most other therapeutic areas. The therapeutic area is also scientifically complex, which increases the need for detailed protocols, CSRs, safety narratives, and specialized scientific communications. Due to this high document intensity, oncology creates a stronger use case for AI-enabled writing support than many smaller therapy areas.

Additionally, key companies in the market are focusing on strategic collaboration, underscoring their high importance.

- For instance, in March 2025, Abridge announced that Memorial Sloan Kettering Cancer Center would expand use of its AI platform for oncology clinical documentation after a pilot found that the system accurately captured complex oncology terminology across specialties. While this example focuses on oncology documentation rather than regulatory writing alone, it still reflects that oncology is one of the earliest and strongest adopters of AI-supported medical language workflows due to its complexity and documentation burden.

The central nervous system segment is projected to grow at a CAGR of 24.33% during the study period.

By Application

Increasing Regulatory Writing Volumes Fueled Segment Growth

Based on application, the market is segmented into regulatory writing, clinical writing, scientific publications & medical communications, safety/pharmacovigilance writing, medical information/response letters, Health Economics and Outcomes Research (HEOR)/grant/market access writing, and others.

Regulatory writing accounted for the largest AI in medical writing market share during the forecast period. Regulatory writing involves some of the most repetitive, structured, high-volume, and compliance-sensitive documents in the life sciences industry. Submission dossiers, summaries, CMC documents, and agency-facing materials require tight formatting, standardized language, and extensive traceability, which makes them highly suitable for AI-supported drafting and workflow automation. As the return on time savings is clearer in regulatory work than in many other applications, companies have prioritized AI investment in this segment first.

- For instance, in July 2025, Celegence announced that its CAPTIS platform had successfully automated the creation of CMC Module 3 documents using generative AI in a pilot project with Kenvue for FDA and MHRA submissions. The company described this as the first time generative AI had delivered high-quality, submission-ready CMC documentation at scale. Such developments strongly support regulatory writing as the leading application segment.

The medical information/response letters segment is projected to grow at a CAGR of 25.12% during the study period.

By End User

Increasing Demand in Medtech/Pharma Companies to Lead Growth in the Segment

Based on end user, the market is segmented into CROs & CDMOs, medtech/pharma companies, med comms agencies, academic / research institutes, and others.

The medtech/pharma companies segment is estimated to hold the dominant market position as they generate the highest volume of regulated writing work across discovery, development, submissions, safety, labeling, and medical affairs. These companies also face strong pressure to shorten timelines, improve compliance, and manage growing document complexity across global programs, which makes AI adoption more valuable and easier to justify. Since they own the majority of core writing workflows and budgets, they are likely to remain the largest end-user group in the market.

- For instance, in March 2026, TrialAssure launched its AI in Medical Writing Certification (AIMWC) Program to support greater adoption of AI across pharma and biotech. The company announced that the program is designed to help medical writers, sponsors, and CRO teams integrate AI into workflows through practical guidance and real-world use cases. This reflects how pharma and biotech organizations are leading adoption and shaping global market demand.

The CROs & CDMOs segment is projected to grow at a CAGR of 24.59% over the study period.

AI in Medical Writing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Medical Writing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.38 billion and maintained its leading position in 2025 at USD 0.50 billion. The market in the region is expected to grow significantly over the forecast period. The region has a large pharmaceutical and biotechnology base, high regulatory-document volume, and faster adoption of AI across life sciences workflows. Additionally, strong investment in AI by life sciences executives and the presence of specialized software vendors are driving growth in the region.

U.S. AI in Medical Writing Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 0.61 billion in 2026, accounting for roughly 40.10% of global sales.

Europe

Europe is projected to grow at 22.94% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.38 billion by 2026. The region is expected to grow due to an increasingly supportive policy environment for the use of data and AI in medicines regulation.

U.K. AI in Medical Writing Market

The U.K.’s market is estimated to reach around USD 0.07 billion in 2026, representing roughly 4.73% of the global market sales.

Germany AI in Medical Writing Market

Germany market is projected to reach approximately USD 0.09 billion in 2026, equivalent to around 5.94% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.34 billion by 2026 and secure the position of the third-largest region in the market. The market is growing due to increased demand for clinical and regulatory documentation for clinical trials. As trial activity and biopharma operations expand, companies are adopting AI tools to manage higher writing volumes more efficiently.

Japan AI in Medical Writing Market

The Japanese market is estimated to reach around USD 0.05 billion by 2026, accounting for approximately 3.14% of the global market.

China AI in Medical Writing Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.08 billion, representing approximately 5.00% of global sales.

India AI in Medical Writing Market

The Indian market is estimated to touch around USD 0.10 billion by 2026, accounting for roughly 6.77% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.08 billion in 2026. The region is experiencing growth supported by rising clinical research activity and digital transformation, fueling demand for faster and more standardized medical writing support. In the Middle East & Africa, the GCC is set to reach USD 0.03 billion by 2026.

South Africa AI in Medical Writing Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.62% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Strategic Collaborations to Strengthen Their Market Position

The global AI in medical writing market is highly consolidated, with companies such as Indegene, Ltd., Certara, IQVIA, Veeva Systems Inc., Yseop, and Parexel International holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in July 2025, Indegene launched the NEXT medical writing automation platform in collaboration with GenAI.

Other notable players in the global market include Trilogy Writing & Consulting, GENINVO, Syneos Health, and Teladoc Health. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY AI IN MEDICAL WRITING COMPANIES PROFILED

- Indegene (India)

- Certara (U.S.)

- IQVIA (U.S.)

- Veeva Systems Inc. (U.S.)

- Yseop (France)

- Parexel International (U.S.)

- Trilogy Writing & Consulting (Germany)

- GENINVO (India)

- Syneos Health (U.S.)

- Teladoc Health (U.S.)

- Phreesia, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: TrialAssure launched its AI in Medical Writing Certification (AIMWC) Program, a new initiative designed to help medical writers and their organizations properly integrate artificial intelligence into their workflows. The program was part of the company's on-site presence during the DIA Medical Affairs and Scientific Communications Forum in Boston.

- January 2026: Arya Health entered into a definitive agreement to acquire HippoAI, a clinical decision support platform powered by advanced artificial intelligence. The acquisition brings together Arya's operational EMR with HippoAI's medical knowledge engine to deliver an integrated solution that enhances both administrative efficiency and clinical decision-making for healthcare providers.

- August 2025: Altasciences collaborated with Evidence Matters, a pioneer in clinical trial data science and document engineering. This partnership combined Altasciences' real-world drug development expertise with Evidence Matters Text Engineering technology that delivers near-deterministic accuracy in regulatory writing by reducing variability and improving the quality, consistency, and speed of documentation.

- July 2025: Indegene launched NEXT Medical Writing Automation, an advanced platform that combines deep medical writing expertise with generative AI (GenAI) to accelerate the creation of high-quality, compliant documents across clinical development, regulatory submissions, and beyond.

- June 2024: Certara, Inc. unveiled its next-generation CoAuthor regulatory writing software for medical writers. The solution combined generative AI, document templates, Microsoft Word integration, and structured content authoring tools.

REPORT COVERAGE

The report provides a comprehensive global AI in medical writing market analysis of market size and forecast across all major segments covered in the study. It includes detailed insights into key market dynamics, growth drivers, restraints, opportunities, and emerging trends expected to influence market expansion over the forecast period. The report also covers key industry developments, including technological advancements, new product launches, partnerships, collaborations, and mergers and acquisitions. In addition, it offers a detailed competitive landscape, including market share analysis and profiles of major companies operating in the global market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 24.99% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Deployment, Therapeutic Area, Application, End User, and Region |

| By Component |

|

| By Technology |

|

| By Deployment |

|

| By Therapeutic Area |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.16 billion in 2025 and is projected to reach USD 9.04 billion by 2034.

In 2025, the market value stood at USD 0.50 billion.

The market is expected to grow at a CAGR of 24.99% over the forecast period.

By component, the software segment led the market.

Rising demand for consistent and high-quality scientific documentation is the key factor driving market growth.

Indegene, Ltd., Certara, IQVIA, Veeva Systems Inc., and Yseop are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us