NLP In Healthcare and Life Sciences Market Size, Share & Industry Analysis, By Component (Software & Services), By Deployment (Cloud-based, On-Premise, & Hybrid), By Type (Text-based NLP, Speech-based NLP, and Multimodal/Hybrid NLP), By Technique (Named Entity Recognition (NER)/Information Extraction, Speech Recognition/Ambient Voice AI, & Others), By Application (Clinical Documentation, Computer-Assisted Coding/CDI, Clinical Decision Support, & Others), By End User (Healthcare Providers, Healthcare Payers, Pharmaceutical & Biotechnology Companies, & Others), and Regional Forecast, 2026-2034

NLP in Healthcare and Life Sciences Market Size and Future Outlook

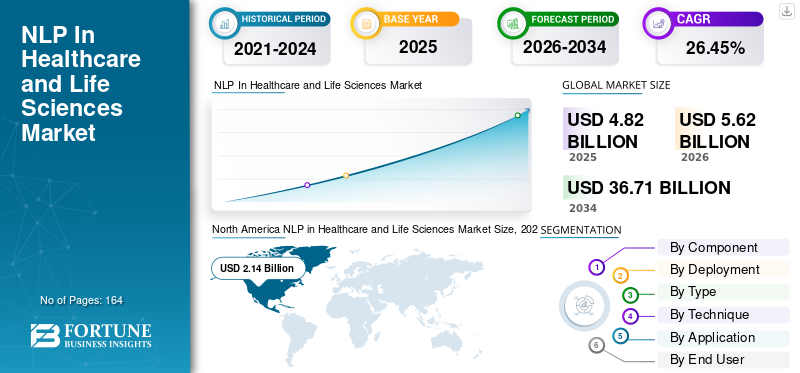

The global NLP in healthcare and life sciences market size was valued at USD 4.82 billion in 2025. The market is projected to grow from USD 5.62 billion in 2026 to USD 36.71 billion by 2034, exhibiting a CAGR of 26.45% during the forecast period. North America dominated the NLP in healthcare and life sciences market with a market share of 44.4% in 2025.

NLP in healthcare and life sciences involves leveraging natural language processing to analyze various data. It facilitates essential workflows, in turn helping healthcare providers and other end users improve efficiency. Market growth is fueled by the increasing burden of clinical documentation, the necessity to derive structured data from unstructured records, the proliferation of ambient voice tools for care provision, and the heightened application of NLP in pharmaceutical research, safety monitoring, and evidence creation.

Notable companies in the global market consist of Microsoft, Amazon Web Services, Oracle, IQVIA, and Clarivate. The competitive environment is influenced by a combination of major cloud and enterprise software companies, healthcare workflow experts, and life sciences analytics firms. These players are integrating automation, summarization, extraction, and conversational AI to enhance clinician efficiency, research output, and data-driven decision-making.

Download Free sample to learn more about this report.

NLP In Healthcare and Life Sciences Market KEY TAKEAWAYS

- 2025 Market Size: USD 4.82 Billion

- 2026 Market Size: USD 5.62 Billion

- 2034 Forecast Market Size: USD 36.71 Billion

- CAGR: 26.45% from 2026–2034

- North America dominated the NLP in healthcare and life sciences market with a 44.4% share in 2025.

- The software segment captured the largest market share in 2025.

- The cloud-based segment is projected to account for 59.1% of the market in 2026.

North America

North America generated USD 2.14 billion in 2025, driven by healthcare IT adoption and AI-enabled clinical workflows.

Europe

Europe is projected to grow at a CAGR of 25.43%, driven by health-data infrastructure and interoperability initiatives.

Asia Pacific

Asia Pacific is projected to reach USD 1.12 billion in 2026, driven by digital health growth and AI adoption.

U.S.

The NLP in healthcare and life sciences market is projected to reach USD 2.31 billion in 2026.

Japan

The NLP in healthcare and life sciences market is projected to reach USD 0.17 billion in 2026.

Read More

NLP IN HEALTHCARE AND LIFE SCIENCES MARKET TRENDS

Increasing Demand for Literature Mining, Drug Discovery Insights and Regulatory Intelligence is a Key Market Trend

Increasing demand for literature mining, drug discovery insights, and regulatory intelligence is emerging as a key market trend in NLP in healthcare and life sciences. This is driven by pharmaceutical and biotech companies managing growing volume of scientific papers, clinical evidence, safety updates, and changing regulatory requirements. Manual review of this information is slow, costly, and difficult to scale. As a result, organizations are increasingly adopting NLP tools to search, extract, summarize, and connect relevant insights faster. This is especially important in drug discovery, where faster review of biomedical literature and research signals can improve target identification and development decisions. It is also important in regulatory intelligence, where companies need timely visibility into evolving rules, submission requirements, and compliance expectations across multiple countries. As a result, buyers are moving toward AI-enabled platforms that combine trusted content with advanced search, summarization, and question-answering capabilities. This trend is supporting stronger demand from pharmaceutical companies, CROs, and regulatory teams, while expanding the market beyond provider-focused use cases into high-value life sciences workflows. These factors collectively support the overall global NLP in healthcare and life sciences market growth.

- For instance, in December 2025, Clarivate launched the Cortellis Regulatory Intelligence AI Assistant. It is designed to help life sciences professionals access and apply regulatory information more effectively and strengthen decision-making in safety and compliance workflows.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Adoption of EHRs and Clinical Digital Records to Propel Market Growth

The swift implementation of electronic health records (EHRs) and digital clinical records is a key factor propelling the NLP market in healthcare and life sciences, as it generates a significantly expanded foundation of digitized, text-heavy clinical data suitable for AI analysis. With the growth of EHR usage, healthcare institutions produce vast amounts of physician notes, discharge summaries, lab reports, referral letters, and other unstructured documents that are challenging to assess manually at scale. NLP transforms this unprocessed text into organized insights for documentation, programming, patient summaries, interoperability, and support for clinical workflows.

- For instance, in January 2025, Microsoft announced the general availability of FHIR structuring in Azure Text Analytics for Health, designed to help healthcare organizations turn unstructured clinical text into structured FHIR data for better interoperability and downstream analytics.

MARKET RESTRAINTS

Fragmented IT Ecosystems and Integration Complexity with EHRs and Lab Systems to Hamper Market Growth

Fragmentized IT ecosystems and the complexity of integration with EHRs and laboratory systems continue to be significant barriers for the NLP market in healthcare and life sciences, as these solutions rely on seamless access to clinical notes, lab reports, medication records, and workflow data across various platforms. In numerous healthcare organizations, data remains in isolated systems, limiting input standardization and restricting the broader deployment of NLP tools. This extends implementation duration, elevates integration expenses, and may postpone ROI for hospitals, laboratories, and life sciences professionals. It also creates difficulties in converting unstructured text into applicable formats for subsequent analytics, coding, summarization, and decision-making support.

- For example, in May 2025, the Financial Times stated that a significant portion of patient data within the U.K.’s NHS remains paper-based or scattered across various IT systems, making merging into a single record complex.

MARKET OPPORTUNITIES

Rising Investments in Healthcare AI, Emergence of Medical LLMs, and Ambient Clinical Intelligence to Offer Market Growth Opportunities

Rising investments in healthcare AI, the emergence of medical LLMs, and the expansion of ambient clinical intelligence are creating a strong market opportunity for NLP in healthcare and life sciences. These trends are enabling vendors to move beyond basic transcription and text extraction toward higher-value use cases such as real-time documentation, chart summarization, clinical search, coding support, and workflow automation. As more capital flows into this space, companies are improving model accuracy, expanding integrations with EHR systems, and scaling deployments across large health systems faster. Medical LLMs are also making healthcare NLP more useful as they can understand clinical language better and generate more contextual outputs from complex medical data. At the same time, ambient clinical intelligence is gaining traction as providers aim to reduce administrative burden and improve clinician productivity without disrupting patient interactions. This is opening new revenue opportunities across provider organizations, digital health platforms, and life sciences workflows that rely on clinically tuned language AI. Overall, these developments are expanding both the addressable market and the commercial value of NLP platforms in healthcare.

- For instance, in February 2026, Abridge received a USD 250 million Series D investment. In the same announcement, the company reported surpassing 100 deployments across some of the largest and most complex health systems in the U.S.

MARKET CHALLENGES

Regulatory Uncertainty and Data Privacy Challenges Pose a Prominent Challenge to Market Growth

Regulatory ambiguity and data protection issues pose significant obstacles for NLP in healthcare and life sciences, as these solutions manage extremely sensitive clinical, patient, and research information that needs to adhere to stringent privacy and security regulations. Healthcare organizations often hesitate to scale NLP deployments due to uncertainty around regulatory ill perspectives on AI outputs, training data, storage methods, auditability, and the use of third-party models. This is particularly crucial for generative AI and medical LLMs, where issues regarding transparency, data governance, and suitable usage are still developing. Privacy issues also raise implementation expenses, since vendors and purchasers must invest in enhanced security measures, legal assessments, access restrictions, and verification prior to deployment.

- For instance, in January 2026, the U.S. Department of Health and Human Services issued a Request for Information seeking public input on how it should use its regulatory, reimbursement, and R&D levers to enable AI adoption in clinical care.

Segmentation Analysis

By Component

Wider Adoption of Cloud-based NLP Platforms Propelled the Software Segment’s Dominance

In terms of component, the market is divided into software and services.

The software segment captured the largest global NLP in healthcare and life sciences market share. The segment’s growth can be attributed to the wider adoption of cloud-based NLP platforms, ambient clinical documentation tools, medical text extraction software, and AI-powered workflow applications across providers and life sciences companies. Software solutions generate stronger recurring revenue as they are typically sold through subscriptions, platform licenses, API usage, and enterprise contracts. Their scalability, easier integration into digital workflows, and growing use in documentation, coding, patient summaries, pharmacovigilance, and research analytics have also contributed to this segment’s dominance.

- For instance, in April 2025, Suki announced the industry’s first ambient orders staging capability for its AI Assistant, allowing clinicians to generate and stage prescription orders directly from ambient visits.

The services segment is anticipated to rise with a CAGR of 28.86% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Rising Preference for Scalable Platforms Supported the Cloud-based Segment’s Growth

On the basis of deployment, the market is divided into on-premise, cloud-based, and hybrid.

The cloud-based segment accounted for the largest global NLP in healthcare and life sciences market share in 2025. The segment’s growth can be attributed to the rising preference for scalable and subscription-based NLP platforms that can be deployed faster across hospitals, payers, and life sciences organizations. Cloud-based solutions reduce the need for heavy upfront infrastructure investment and make it easier to update models, add new users, and integrate AI features across multiple sites. They also support large-scale processing of clinical notes, conversations, and research documents, which is important as healthcare data volumes continue to rise. Their flexibility, easier remote access, and stronger support for enterprise-wide rollout have further contributed to this segment’s dominance. Furthermore, the segment is set to hold 59.1% share by 2026.

- For instance, in March 2025, Oracle announced that physicians using Oracle Health Clinical AI Agent were witnessing nearly a 30% reduction in daily documentation time. This highlights how cloud-enabled AI tools are helping healthcare organizations improve workflow efficiency while scaling deployment more easily across clinical settings.

The hybrid segment is anticipated to rise with a CAGR of 28.76% over the forecast period.

By Type

Large Volume of Clinical Notes and Records Supported the Text-based NLP Segment’s Growth

Based on type, the market is classified into speech-based NLP, text-based NLP, and multimodal/hybrid NLP.

The text-based NLP segment dominated the global market in 2025. The segment’s growth is driven by the large amount of healthcare data already available in written form, such as physician notes, discharge summaries, lab reports, radiology reports, case notes, and trial documents. These text-heavy records are generated every day across hospitals, payers, pharmaceutical companies, and research organizations, creating strong demand for tools that can extract, organize, and analyze information quickly. Text-based NLP is also easier to deploy at scale as it fits directly into existing EHR, claims, regulatory, and research workflows. Its broad use in coding, clinical summaries, pharmacovigilance, literature mining, and document review has further contributed to this segment’s dominance. Furthermore, the segment is set to hold 47.6% share in 2026.

- For instance, in January 2026, Microsoft highlighted an Azure AI workflow that uses Text Analytics for Health to process PDFs and text documents, identify medical entities, structure data into FHIR format, and generate clinical insights.

The speech-based NLP segment is anticipated to rise with a CAGR of 32.49% over the forecast period.

By Technique

Growing Need to Reduce Clinical Documentation Supported the Speech Recognition/Ambient Voice AI Segment’s Growth

In terms of technique, the market is divided into named entity recognition (NER)/information extraction, speech recognition/ambient voice AI, summarization/generative AI, rule-based/hybrid nlp, and others.

The speech recognition/ambient voice AI segment captured the highest share of the global market in 2025. Key factors such as the rising need to reduce clinician documentation time and convert patient-clinician conversations into usable notes in real-time are anticipated to boost the segmental growth. They are also becoming more important as hospitals and health systems want faster documentation, lower administrative burden, and better workflow efficiency. Furthermore, the segment is set to hold 27.2% share by 2026.

- For instance, in March 2025, Rush University System for Health expanded its partnership with Suki for an enterprise-wide ambient AI rollout after a successful launch. The announcement highlighted how ambient and dictation technology can reduce after-hours administrative work and improve clinical documentation workflows.

The summarization/generative AI segment is anticipated to rise with a CAGR of 33.70% over the forecast period.

By Application

High Volume of Daily Physicians' Notes Supported the Clinical Documentation Segment Growth

On the basis of application, the market is divided into clinical documentation, computer-assisted coding/CDI, clinical decision support & patient summaries, pharmacovigilance & safety case intake, regulatory & medical affairs document review, patient engagement, messaging, and conversational AI, clinical trial matching/ recruitment, drug discovery/research text analytics, and others.

The clinical documentation segment captured the highest share of the global market in 2025. The segment’s growth is driven by the high volume of daily physician notes, visit summaries, referral letters, and follow-up documentation generated across hospitals and clinics. Healthcare providers are increasingly using NLP tools to reduce manual charting work, improve note quality, and save clinician time. These solutions also help turn patient-clinician conversations into structured records more quickly, which supports better workflow efficiency and reduces administrative burden. Their broad use across specialties and care settings has further contributed to this segment’s dominance. Furthermore, the segment is set to hold 23.1% share by 2026.

- For instance, in February 2025, the Cleveland Clinic announced the rollout of Ambience Healthcare’s AI platform for documentation, clinical documentation integrity, and point-of-care coding. The company announced that the technology is intended to give caregivers more time for personal interaction during visits while reducing administrative workload.

The patient engagement, messaging, and conversational AI segment is anticipated to rise with a CAGR of 30.90% over the forecast period.

By End User

Broad Use Across Hospitals and Health Systems Supported the Healthcare Providers Segment’s Leading Position

Based on end user, the market is segmented into healthcare providers, healthcare payers, pharmaceutical & biotechnology companies, CROs/CDMOs, academic & research institutes, and others.

In 2025, the healthcare providers segment held the leading position in the global market. The segment’s growth can be attributed to the high daily volume of clinical documentation, patient summaries, coding support, and workflow tasks handled by hospitals, clinics, and physician groups. Providers are the largest direct users of NLP tools as they need to process unstructured clinical notes, conversations, lab-related information, and visit records in real-time. These solutions help reduce administrative burden, improve documentation quality, and support faster clinical workflows. Their broad use across multiple specialties and care settings has further contributed to this segment’s dominance. Furthermore, the segment is set to hold 48.4% share by 2026.

- For instance, in September 2025, Highmark Health announced an enterprise-wide collaboration with Abridge to deploy ambient clinical documentation technology across its payer-provider ecosystem.

The CROs/CDMOs are projected to withness 29.26% growth rate during the forecast period.

NLP in Healthcare and Life Sciences Market Regional Outlook

By geography, the market is divided into North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

North America

North America NLP in Healthcare and Life Sciences Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market reached USD 1.86 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 2.14 billion. The region’s growth is driven by the presence of a mature healthcare IT base, high EHR penetration, and early large-scale adoption of ambient clinical documentation and workflow AI.

U.S. NLP in Healthcare and Life Sciences Market

The U.S. market dominated the North American market and is expected to reach around USD 2.31 billion in 2026, accounting for roughly 41.1% of the global market.

Europe

Europe market is anticipated to grow at 25.43% CAGR during the forecast period. Europe’s growth is being supported by stronger cross-border health-data infrastructure, rising interoperability requirements, and a more formal policy framework for secondary use of health data in research and innovation.

U.K. NLP in Healthcare and Life Sciences Market

The U.K.’s market in 2026 is estimated at around USD 0.32 billion, representing roughly 5.6% of global revenues.

Germany NLP in Healthcare and Life Sciences Market

Germany’s market size is projected to reach approximately USD 0.35 billion in 2026, equivalent to around 6.3% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 1.12 billion by 2026, making it the third-largest region in the global NLP in healthcare and life sciences industry. The region is being driven by rapid digital-health expansion, large patient volumes, and increasing interest in AI-enabled health-system modernization.

Japan NLP in Healthcare and Life Sciences Market

The Japanese market in 2026 is estimated at around USD 0.17 billion, accounting for roughly 3.0% of global revenues.

China NLP in Healthcare and Life Sciences Market

China’s market is projected to reach revenues of around USD 0.37 million in 2026, representing roughly 6.6% of global sales.

India NLP in Healthcare and Life Sciences Market

The Indian market in 2026 is estimated at around USD 0.17 billion, accounting for roughly 3.0% of global revenues.

Latin America and the Middle East & Africa

The Middle East & Africa and Latin America regions are expected to experience slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.28 billion by 2026. Prominent factors such as broader digital-health transformation, stronger focus on interoperability, and rising regional interest in applying AI to the workforce are boosting market growth in these regions.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.09 billion by 2026, representing about 1.6% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Participants Focus on Ambient Documentations to Improve Clinician Productivity

The global market features a moderately fragmented competitive landscape. Key contributors include Microsoft, Amazon Web Services, Oracle, IQVIA, Clarivate, and Abridge. These companies are increasingly focusing on ambient documentation, medical text extraction, coding and workflow automation, pharmacovigilance literature monitoring, and research text analytics to improve clinician productivity and extract value from unstructured data.

- For instance, in December 2025, Clarivate launched its Cortellis Regulatory Intelligence AI Assistant, designed to help life sciences professionals access and apply regulatory information more effectively in safety and compliance workflows.

Key contributors include Solventum, Suki, Inc., Tempus, Wolters Kluwer, and others. Emphasis on new product expansion, enterprise partnerships, clinical workflow integration, and life sciences-focused automation are key strategies undertaken by these players.

LIST OF KEY NLP IN HEALTHCARE AND LIFE SCIENCES COMPANIES PROFILED

- Microsoft (U.S.)

- Alphabet Inc. (U.S.)

- Oracle (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Abridge Al, Inc. (U.S.)

- Suki AI, Inc. (U.S.)

- TEMPUS (U.S.)

- IQVIA Inc. (U.S.)

- Solventum (U.S.)

- Averbis (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: UCHealth expanded Abridge across 2,300+ providers, showing continued enterprise-scale growth for ambient AI documentation.

- January 2026: HealthEdge and Suki partnered to bring ambient clinical intelligence into health plan care management workflows, extending NLP beyond provider documentation into payer operations.

- January 2026: Solventum became an Accelerator partner in the MEDITECH Alliance, enabling direct integration of Fluency Align with MEDITECH Expanse for ambient AI documentation.

- October 2025: Microsoft expanded Dragon Copilot with an ambient experience for nursing workflows and new partner extensibility, broadening clinical NLP use across care teams.

- August 2025: Clarivate launched the beta AI-powered Regulatory Assistant within Cortellis Regulatory Intelligence, aimed at improving regulatory productivity and easing review burden.

REPORT COVERAGE

The global NLP in healthcare and life sciences market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 26.45% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Type, Technique, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Type |

|

| By Technique |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.82 billion in 2025 and is projected to reach USD 36.71 billion by 2034.

In 2025, the market value stood at USD 2.14 billion.

The market is expected to exhibit a CAGR of 26.45% during the forecast period (2026-2034).

By component, the software segment is expected to lead the market.

Rapid adoption of EHRs and clinical digital records is the key factor driving market expansion.

Microsoft, Amazon Web Services, Oracle, IQVIA, Clarivate, and Abridge are some of the top players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 164

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us