Airplane Survivability Equipment Market Size, Share & Industry Analysis, By Platform (Combat aircraft, Combat helicopter, Special mission aircraft, UAV), By Fit (Line fit, Forward fit) And Regional Forecast, 2026-2034

Aircraft Survivability Equipment Market Size and Future Outlook

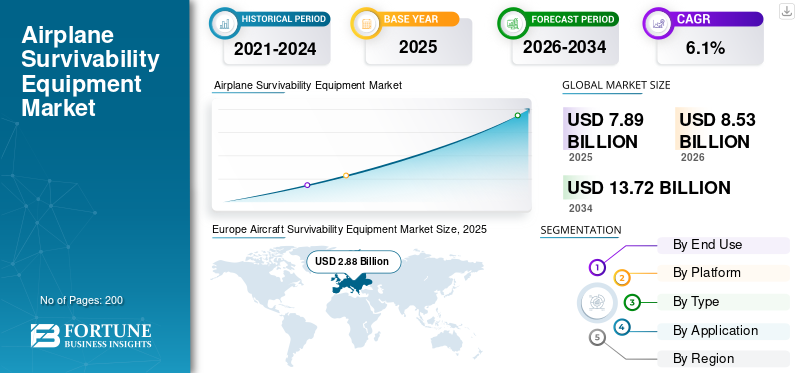

The global aircraft survivability equipment market size was valued at USD 7.89 billion in 2025. The market is projected to grow from USD 8.53 billion in 2026 to USD 13.72 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period. Europe dominated the aircraft survivability equipment market with a market share of 36.5% in 2025.

The aircraft survivability equipment (ASE) market encompasses systems and subsystems designed to protect aircraft from hostile threats such as radar‑guided and infrared missiles, electronic attacks, and other battlefield hazards. It includes radar warning receivers, missile approach warning systems, electronic countermeasures, countermeasure dispensers, and integrated defensive suites deployed across combat aircraft, helicopters, special‑mission platforms, and unmanned aerial vehicles. The market is characterized by continuous technology upgrades, strong defense‑modernization demand, and a focus on integrating advanced sensors, AI‑enabled processing, and modular architectures to enhance real‑time threat detection and survivability in contested environments.

Key players include Northrop Grumman, Raytheon Technologies, BAE Systems, Leonardo, L3Harris Technologies, General Dynamics, Thales Group, Hensoldt, Elbit Systems, and Lockheed Martin. These companies are shaping the market by delivering integrated self-protection suites, missile/threat warning sensors, electronic warfare and countermeasure systems, mission-data/software updates, and scalable retrofit-to-sustainment support across allied fixed-wing, rotary-wing, and UAV fleets.

Download Free sample to learn more about this report.

AIRCRAFT SURVIVABILITY EQUIPMENT MARKET TRENDS

Shift toward Highly Integrated and AI‑Enabled Defensive Suites is Shaping the Market Trend

The aircraft survivability equipment market growth is shifting toward highly integrated, modular, and AI‑enabled defensive systems that combine radar warning, missile approach warning, electronic warfare, and countermeasure dispensers into unified suites. Manufacturers are also focusing on lightweight, compact designs with improved power efficiency and multi‑mission compatibility across fixed‑wing aircraft, helicopters, and unmanned platforms. Growing emphasis on cyber‑resilient architectures and support for directed‑energy countermeasures is further shaping the technological roadmap of survivability suites.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Threat Environment and Defense Modernization Programs to Drive Market Growth

The primary driver is the intensifying threat landscape, including advanced infrared and radar‑guided missiles, electronic warfare tactics, and asymmetric tactics that put aircraft at higher risk. Persistent geopolitical tensions and ongoing regional conflicts are prompting nations to prioritize force protection, leading to increased procurement of sophisticated survivability suites for existing and new platforms. Concurrently, defense modernization campaigns and extended service lives of legacy aircraft are fueling demand for upgrades in electronic support measures, countermeasures, and integrated defensive systems.

MARKET RESTRAINTS

High Development Costs and Complex Certification Requirements Hinder Market Growth

High development and integration costs, along with long certification and qualification cycles, constrain widespread adoption, especially for smaller air forces and budget‑constrained customers. Limited availability of end‑to‑end survivability solutions from a small set of specialized suppliers can restrict design flexibility and increase procurement timelines. Dependence on complex global supply chains and export‑control regimes for sensitive electronic components also adds execution risk and delays for OEMs and defense integrators.

MARKET OPPORTUNITIES

Growth in Fleet Modernization and Retrofits across Platforms Presents Several Growth Opportunities

Expanding global fleets of combat, special‑mission, and unmanned aircraft are creating substantial demand for both new installations and retrofits of survivability equipment. Rising defense modernization programs, especially in regions with high‑intensity threat environments, drive orders for upgraded warning systems, decoy dispensers, and cockpit‑friendly human‑machine interfaces. There is also a growing opportunity in commercial and paramilitary rotorcraft, maritime patrol, and search‑and‑rescue platforms that are adopting higher levels of survivability to meet evolving safety and security standards.

MARKET CHALLENGES

Evolution of Adversary Tactics And Weapons to Challenge Market Growth

A key challenge is the continuous evolution of adversary tactics and weapons, which forces survivability systems to keep pace with emerging threats and electronic‑warfare techniques. Ensuring seamless interoperability across heterogeneous fleets, legacy platforms, and multi‑national coalition architectures complicates system design and integration. Maintaining cybersecurity and spectrum effectiveness in increasingly contested electromagnetic environments, while balancing weight, power, and reliability requirements, further raises technical and operational hurdles for manufacturers and operators.

Segmentation Analysis

By End Use

Government Segment to Dominate due to the Military's Fund for Urgent Survivability Upgrades

Based on end use, the market is segmented into government and defense contractors.

The government segment is anticipated to account for the largest market share. Government demand leads due to militaries fund urgent need for survivability upgrades to protect crews and high-value aircraft. Budget cycles favor multi-year programs, while operational feedback drives rapid refresh of threat libraries and countermeasure inventories.

The defense contractors segment is anticipated to rise with a CAGR of 6.7% over the forecast period.

By Platform

Fixed-Wing Aircraft Segment Led, Driven by Modernization Packages

Based on platform, the market is segmented into fixed-wing aircraft and rotary-wing aircraft.

In 2025, the fixed-wing aircraft segment dominated the global market. Fixed-wing demand remains the largest as fighters, bombers, transports, and ISR aircraft face long-range missiles and radar networks. Modernization packages bundle RWR/MWS, jammers, dispensers, and mission software upgrades at scale worldwide today.

The rotary-wing aircraft segment is projected to grow at a CAGR of 6.5% over the forecast period.

By Type

Electronic Warfare Systems Segment to Lead owing to its Ability to Defeat Smarter Radars

Based on type, the market is segmented into electronic warfare systems, countermeasure systems, survivability software, and sensor systems.

The electronic warfare systems segment is anticipated to witness a dominant market share over the forecast period. Electronic warfare systems demand climbs as aircraft detect, classify, and defeat smarter radars and datalinks. Buyers prioritize digital receivers, adaptive jamming, and open architectures that update quickly as threats evolve.

The survivability software segment is projected to grow at the highest CAGR of 7.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Military Aircraft Segment Led due to Retrofit Programs on Legacy Aircraft

Based on application, the market is segmented into military aircraft, commercial aircraft, and unmanned aerial vehicles.

The military aircraft segment captured the key aircraft survivability equipment market share. Military aircraft dominate as combat and support fleets operate in contested zones and must survive first contact. Retrofit programs on legacy aircraft and protections for UAV control links sustain continuous procurement.

The unmanned aerial vehicles segment is projected to grow at a CAGR of 7.1% during the study period.

Aircraft Survivability Equipment Market Regional OutlooK

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

Europe Aircraft Survivability Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is estimated to reach USD 2.46 billion by 2026 and secure the position of the second-largest region in the market. The region's demand stays strong as modernization budgets favor rapid survivability upgrades for fighters, tankers, ISR, and helicopters. Heavy sustainment spends, and fast retrofit cycles keep EW, DIRCM, and dispensers moving.

U.S. Aircraft Survivability Equipment Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.17 billion in 2026, accounting for roughly 5.8% of global sales. U.S. demand is driven by large active fleets and continuous upgrades across fighters, bombers, tankers, and special-mission aircraft. Open-architecture EW, DIRCM scaling, and sustainment contracts keep spending resilient through 2034.

Europe

Europe held the dominant share in 2024, valued at USD 2.61 billion, and also maintained the leading share in 2025, with USD 2.88 billion. The regional demand accelerates as proximity to contested airspace pushes urgent protection fits across legacy fleets and new deliveries. NATO readiness, joint exercises, and munitions-heavy planning raise requirements for sensors, jammers, and countermeasures.

U.K. Aircraft Survivability Equipment Market

The U.K. market in 2026 is estimated at around USD 0.50 billion, representing a roughly 5.5% CAGR of global sales. U.K. demand focuses on protecting high-value platforms and deployable air power, aligning upgrades with NATO operations. Strong emphasis on electronic support measures, countermeasures, and mission-data software sustains procurement increasingly now.

Germany Aircraft Survivability Equipment Market

Germany’s market is projected to reach approximately USD 0.57 billion by 2026. Germany's demand grows as readiness initiatives and procurement reform accelerate the modernization of fighters, helicopters, and transport fleets. Integration of advanced sensors and jammers, plus European industrial collaboration, expands retrofit volume.

Asia Pacific

Asia Pacific is projected to record a growth rate of 6.8% during the forecast period, which is the third-highest among all regions, and reach a valuation of USD 2.20 billion by 2026. The region demand rises with expanding fighter, maritime patrol, and rotorcraft fleets, plus higher UAV adoption. Countries invest in indigenous EW and software-defined upgrades to counter missiles and dense air defenses.

Japan Aircraft Survivability Equipment Market

The Japanese market is estimated at around USD 0.31 billion by 2026, accounting for roughly 5.5% of the CAGR during the forecast period. Japan's demand centers on defending airspace with advanced fighters and patrol assets, emphasizing early warning sensors, towed decoys, and jamming. High interoperability standards and rigorous testing extend timelines but sustain budgets.

China Aircraft Survivability Equipment Market

China’s market is projected to be one of the largest in the Asia Pacific, with 2026 revenues estimated at around USD 0.70 billion. China's demand is shaped by rapid platform production and a push for integrated EW suites across fighters, bombers, and UAVs. Indigenous electronics capacity supports scale, with a focus on countering modern air defenses.

India Aircraft Survivability Equipment Market

The Indian market in 2026 is estimated at around USD 0.40 billion. India's demand rises from fleet expansion, upgrades on legacy aircraft, and heightened border threat perceptions. Local production and offsets drive sensor and EW buys, while sustainment needs boost recurring spend.

Rest of the World

The rest of the world includes the Middle East & Africa, and Latin America. These regions are expected to witness moderate growth in the market during the forecast period. The Middle East & Africa and Latin America markets are set to reach a valuation of USD 0.48 billion and USD 0.30 billion, respectively, in 2026. The rest of the world's demand concentrates in the Middle East and parts of Africa, where missile and drone threats are immediate. Latin America grows more slowly, prioritizing border security aircraft and affordable countermeasure packages.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Advancements to Gain Competitive Advantage

The aircraft survivability equipment market is being reshaped by a fast-changing threat environment where missiles, drones, and modern air-defense sensors evolve more quickly than traditional hardware refresh cycles. Operators are moving from single-box purchases to integrated protection suites combining threat warning, electronic warfare, countermeasures, and mission-data updates as survivability now depends on how well systems fuse, respond, and update in real time. Retrofit demand is rising alongside new aircraft deliveries, while sustainment spend grows as libraries, software, and spares require continuous refresh.

LIST OF KEY AIRCRAFT SURVIVABILITY EQUIPMENT COMPANIES PROFILED IN REPORT

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies (U.S.)

- BAE Systems (Great Britain)

- Leonardo (Italy)

- L3Harris Technologies (U.S.)

- General Dynamics (U.S.)

- Thales Group (France)

- Hensoldt (Germany)

- Elbit Systems (Israel)

- Saab AB (Sweden)

KEY INDUSTRY DEVELOPMENTS

- February 2026- BAE FalconWorks and SURVICE Engineering signed a framework agreement to work together on next-generation UAS technologies. It supports BAE Systems’ broader push to speed up uncrewed solutions that satisfy U.K. and international defence and security needs.

- February 2026- BAE Systems secured additional U.S. Army Foreign Military Sales orders worth USD 137 million to supply AN/AAR-57 CMWS to allied countries, strengthening aircraft and crew protection against missile and other advanced threats.

- April 2022- BAE Systems won a USD 22 million U.S. Foreign Military Sales award, executed through the U.S. Army, to manufacture and deliver AN/AAR-57 Common Missile Warning System kits and related equipment for Apache helicopter fleets.

- September 2021- Leonardo signed a Strategic Partnering Arrangement with the RAF, DE&S, and Dstl. Under the deal, Leonardo UK would collaborate with the MOD, Dstl scientists, and other U.K. partners to advance aircraft-level integrated protection systems.

- July 2021- KBR secured two follow-on awards worth over USD 120 million combined to deliver advanced engineering support for U.S. Navy training systems and aircraft survivability equipment. KBR received a USD 64.9 million task order to design, enhance, and modernize training system hardware and software, along with electronic classroom materials and interactive courseware for the E-2/C-2 Airborne Command and Control Systems Program Office (PMA-231).

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By End Use, By Platform, By Type, By Application, and Region |

| By End Use |

|

| By Platform |

|

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 7.89 billion in 2025 and is projected to reach USD 13.72 billion by 2034.

In 2025, the market value stood at USD 2.88 billion.

The market is expected to exhibit a CAGR of 6.1% during the forecast period.

By end use, the government segment is expected to dominate the market.

Rising threat environment and defense modernization programs is a key factor driving the market.

Northrop Grumman, Raytheon Technologies, BAE Systems, Leonardo, L3Harris Technologies are few major players in the global market.

Europe dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us