Airbag Electronics Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Component Type (Airbag ECU, Crash Sensors, Diagnostic Modules, and Harness & Connectors), By Airbag Type (Front Airbag, Side Airbag, Curtain Airbag, Knee Airbag, and Far-side Airbag), By Vehicle Class (Entry Level, Mid-range, and Premium), By Vehicle Propulsion (ICE and Electric), and Regional Forecast, 2026-2034

Airbag Electronics Market Size and Future Outlook

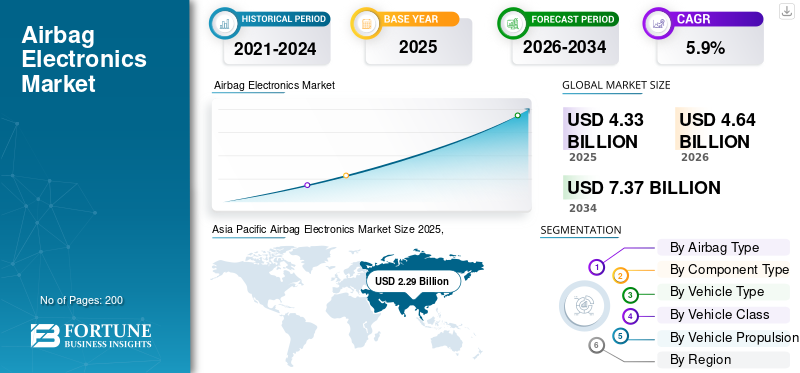

The global airbag electronics market size was valued at USD 4.33 billion in 2025. The market is projected to grow from USD 4.64 billion in 2026 to USD 7.37 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. Asia Pacific dominated the airbag electronics market with a market share of 52.88% in 2025.

Airbag electronics refer to the integrated control units, sensors, and microprocessors that detect collision impacts and activate airbag deployment. They ensure precise timing, system diagnostics, occupant detection, and overall coordination of vehicle passive safety mechanisms during crash events. The market is driven by stricter vehicle safety regulations, rising road accident concerns, and growing demand for advanced occupant protection. Increasing adoption of ADAS, sensor innovations, and expanding vehicle production further accelerate the need for sophisticated airbag control systems.

Key players in the global automotive market include Bosch, Continental AG, ZF Friedrichshafen, Denso Corporation, and Autoliv. These companies focus on developing advanced airbag control units, crash sensors, and integrated safety electronics. Strategic partnerships with automakers, along with investments in sensor fusion, real-time diagnostics, and AI-driven crash detection, strengthen their role in enhancing occupant protection and meeting evolving global vehicle safety regulations.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stricter Global Safety Regulations Accelerate Market Adoption

Growing pressure from regulatory bodies such as NCAP programs and government mandates for enhanced occupant protection is driving demand for advanced safety features. Automakers must integrate sophisticated crash sensors, multi-stage airbag control units, and diagnostic modules to meet evolving compliance standards. This push toward standardized safety performance increases reliance on electronic intelligence within passive safety systems, supporting continuous technological enhancement and broader market penetration.

- In August 2024, the state of Missouri passed Senate Bill 1276, making it a felony to install non-functional or counterfeit airbags, reinforcing legal enforcement of airbag components.

MARKET RESTRAINTS

High System Costs Restrict Wider Market Penetration

Despite rising vehicle safety awareness, the high cost of airbag electronic components, including precision sensors, microcontrollers, and redundant safety circuits, acts as a restraint. Manufacturers face increased expenses tied to regulatory compliance, testing, and product validation. These costs are especially challenging for low-cost vehicles and price-sensitive markets, slowing adoption. The complexity of ensuring reliability under extreme conditions further elevates R&D investments, limiting widespread integration of airbags in budget segments.

MARKET OPPORTUNITIES

AI-Enabled Crash Detection Creates Growth Opportunities

The integration of AI and machine-learning algorithms into airbag electronics is creating new market opportunities. AI enables real-time crash pattern recognition, occupant posture assessment, and predictive deployment strategies, significantly improving safety outcomes. Automakers and electronics suppliers are exploring advanced sensor fusion to support precision protection in autonomous and electric vehicles. As cabins evolve with new seating layouts, demand for intelligent safety systems continues to rise, opening avenues for innovation.

- In September 2024, ROADMEDIC unveiled the smart airbags 9-1-1 deployment chip, designed to link electronics with real-time emergency response. This allows deployment data to be sent immediately to first responders in collaboration with drone systems, expanding smart-airbag functionality.

AIRBAG ELECTRONICS MARKET TRENDS

Growing Use of MEMS Sensors Shapes Technology Trends

A significant trend shaping the industry is the increasing adoption of MEMS-based accelerometers and pressure sensors in airbags. These sensors offer superior precision, durability, energy efficiency, and faster response times, enhancing deployment accuracy. Their compact size supports modular safety system designs suitable for next-generation vehicles. As electronics suppliers optimize MEMS for multi-impact and rollover detection, the trend is accelerating adoption in both premium and mid-range vehicles. For instance, MEMS sensors developed by Bosch enable faster deployment of airbags. MEMS sensors are optimized for airbag control units and roll-over detection, enabling faster crash event detection and improved occupant protection via high-accuracy accelerometers and gyroscopes.

MARKET CHALLENGES

Complex Integration with Vehicle Architectures Poses Market Challenges

Modern vehicles incorporate increasingly complex electronic architectures, requiring seamless coordination between airbag electronics, ADAS modules, and vehicle control units. Ensuring compatibility, cybersecurity integrity, and reliable communication across multiple ECUs remains a major technical challenge. Additionally, the shift toward centralized vehicle computing demands redesigning legacy airbag systems for new electrical/electronic (E/E) platforms. These integration complexities slow development cycles and require extensive engineering validation.

Download Free sample to learn more about this report.

Segmentation Analysis

By Airbag Type

Mandatory Frontal Protection Standards Sustain Front Airbag Segment Dominance

Based on airbag type, the market is segmented into front airbag, side airbag, curtain airbags, knee airbag, and far-side airbag.

Front airbags dominate the market as they are mandated in most vehicles and upgraded with multi-stage deployment, seat-occupant sensing, and advanced control algorithms. Their installed base expands with rising global vehicle production and refresh cycles, driving airbag electronics market growth over the airbag electronics market forecast period.

- In September 2025, Tesla added vision-assisted front airbag deployment via software update 2025.32.3 for newer Model 3 and Model Y cars.

Far-side airbags are the fastest-growing segment, supported by new Euro NCAP far-side impact protocols and automakers focus on centre airbags to reduce occupant interaction injuries in lateral crashes and rollovers, thereby stimulating market expansion.

By Component Type

Advanced Crash-Sensing Architectures Reinforce Airbag ECU Segment Leadership

In terms of component type, the market is divided into airbag ECU, crash sensors, diagnostic modules, and harness & connectors.

The airbag electronic control unit (ECU) segment is both the dominating and fastest-growing component type in the automotive market. It holds the largest share since the ECU is the central module managing crash detection, algorithmic deployment, and system diagnostics across multiple airbag systems; simultaneously, it shows the significant growth rate due to rising demand for multi-loop, multi-sensor ECUs integrated with advanced features for electric, autonomous, and connected vehicles, thus driving market growth.

- For instance, Bosch Mobility’s AB Premium, a scalable airbag control unit platform, is capable of up to 48 firing loops and 18 peripheral crash-sensor interfaces, enabling high-performance integration of roll-over and multi-impact detection across segments.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Strong Consumer Preference and Enhanced Safety Integration Uphold SUV Segment Demand

On the basis of vehicle type, the market is categorized into hatchback/sedan, SUVs, LCVs (light commercial vehicles), and HCVs.

The SUV segment remains both the dominating and fastest-growing category in the automotive market. Higher global demand for SUVs, combined with their larger cabin structures and increased focus on occupant protection, drives greater installation of advanced airbag systems, including side-curtain, rollover, and multi-impact protection. Automakers continue enhancing SUV safety architectures to meet evolving crash-test protocols, further strengthening segment momentum and driving market growth.

- In March 2025, the Mahindra XUV700 achieved a 5-star adult and 4-star child safety rating from Global NCAP, reflecting its extensive airbag systems and occupant-protection features, boosting confidence in advanced restraint electronics.

By Vehicle Class

Strong Global Production Volumes and Mandatory Safety Compliance Uphold Entry-Level Vehicle Market Share

By vehicle class, the market is segmented into entry level, mid-range, and premium.

Entry-level vehicles dominate the automotive market due to their high production volumes across emerging and developed economies. Increasing enforcement of minimum safety standards, such as compulsory front airbags, continues to push for greater installation of essential airbag ECUs and sensors in compact cars. Automakers are also adopting cost-optimized yet reliable electronics platforms to meet regulatory benchmarks without significantly increasing vehicle prices, thereby sustaining segment leadership and driving market growth.

Premium vehicles represent the fastest-growing segment as they rapidly integrate advanced airbag electronics, including center airbags, multi-stage deployment algorithms, occupant-position sensing, and AI-enabled crash evaluation systems. Rising demand for luxury EVs and premium SUVs further accelerates adoption, supporting strong segment expansion.

By Vehicle Propulsion

Established Production Scale and Mature Safety Integration Drive ICE Vehicle Segment

By vehicle propulsion, the market is segregated into ICE and electric.

ICE vehicles dominate the automotive airbag electronics market share, due to their long-standing global production base and widespread availability across all price segments. Their well-established safety integration frameworks, mature supply chains, and consistent regulatory compliance requirements support large-scale adoption of airbag ECUs, sensors, and deployment modules. As developing regions continue to rely heavily on ICE passenger cars and SUVs, demand for standardized airbag electronics remains strong, sustaining segment leadership and driving market growth.

Electric vehicles are the fastest-growing segment as EV architectures increasingly incorporate advanced airbag electronics tailored to new platform layouts, battery placement, and evolving crash-test protocols. Rising EV adoption worldwide accelerates the integration of next-generation safety systems, fostering rapid segment expansion. In 2024, global electric car sales exceeded 17 million units, representing over 20% of all new passenger cars sold globally.

Airbag Electronics Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

The Asia Pacific region leads in both market size and growth, thanks to its status as a global automotive manufacturing hub and rising safety awareness. High vehicle production in China, India, and Southeast Asia, plus the adoption of multi-airbag solutions and new safety mandates, is fueling the adoption of advanced airbag electronics. Manufacturers are also establishing local production and R&D facilities to serve regional OEMs more effectively, driving market growth. In July 2023, ZF Friedrichshafen AG announced an investment in an airbag production base and R&D centre in Wuhan, China.

Asia Pacific Airbag Electronics Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America holds the region’s second-largest share, underpinned by strong vehicle safety regulations, high vehicle unit volumes, and established automaker-supplier ecosystems. Continuous updates in crash-sensing electronics and airbag system architecture, especially in side-impact and multi-airbag modules, support steady airbag electronics market demand. While growth is slower than in Asia, the region benefits from upgrade cycles and new vehicle safety technologies, thereby driving regional market expansion.

The U.S. is the predominant national market within North America. Its durable vehicle fleet, rigorous safety standards, and high safety-feature content per vehicle propel demand for advanced airbag electronics. Automakers integrate more smart sensors, diagnostic modules, and multi-module airbags, curtain, knee, and side, to meet occupant-protection expectations. The upward shift in EV and autonomous vehicle production further accelerates system complexity and thereby boosts uptake of next-gen airbag electronics. In December 2024, the National Highway Traffic Safety Administration (NHTSA) announced it would extend a probe rather than mandate an immediate recall of about 50 million U.S. vehicles containing suspect air-bag inflators, citing further engineering evaluation needed.

Europe

Europe’s market is mature yet resilient. Strong regulatory frameworks such as Euro NCAP, consumer awareness for high safety, and a sizable premium-vehicle base contribute to sustained volume. Although production growth is slower than in emerging regions, technology upgrades, such as far-side airbags, multi-stage ECUs, and integration with ADAS, drive incremental expansion. The regional market growth is supported as manufacturers refresh platforms and adapt to evolving occupant-safety architectures. In June 2025, Infineon Technologies AG introduced expanded automotive-grade semiconductor modules for both entry-level and high-end airbag systems compliant with ASIL-D, supporting comprehensive electronics architectures.

Rest of the World

In the Rest of the World, including South America and the Middle East & Africa, growth is gradual but gaining traction. Increased vehicle ownership, improvements in safety legislation, and rising demand for safer vehicles help raise the installation of basic electronics for airbags. However, cost sensitivity and lower baseline safety content slow penetration of advanced modules. As local OEMs upgrade safety standards and aftermarket retrofit activity grows, the segment is supporting wider future growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Crash-Sensing Electronics and Safety Innovation Shape Competitive Landscape

The global automotive market has a concentrated competitive landscape, led by Autoliv, Bosch, ZF Friedrichshafen, Continental, and DENSO. These suppliers develop advanced airbag ECUs, crash sensors, and integrated passive-safety platforms aligned with evolving NCAP protocols and EV architectures. Collaborations with automakers and regional electronics firms support localized production, software calibration, and cost optimization. In October 2025, Autoliv and China’s Hangsheng Electric agreed to form a safety-electronics joint venture for the Chinese market, reinforcing innovation and scale.

LIST OF KEY AIRBAG ELECTRONICS COMPANIES PROFILED

- Autoliv Inc. (Sweden)

- Robert Bosch GmbH (Germany)

- ZF Friedrichshafen AG (Germany)

- Continental AG / Aumovio SE (Germany)

- DENSO Corporation (Japan)

- Joyson Safety Systems (U.S.)

- Daicel Corporation (Japan)

- ARC Automotive Inc. (U.S.)

- Hyundai Mobis Co., Ltd. (South Korea)

- Toyoda Gosei Co., Ltd. (Japan)

- NXP Semiconductors N.V. (Netherlands)

- Infineon Technologies AG (Germany)

- Texas Instruments Inc. (U.S.)

- Analog Devices, Inc. (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Onsemi Corporation (U.S.)

- Ashimori Industry Co., Ltd. (Japan)

- Nihon Plast Co., Ltd. (Japan)

- Veoneer (Sweden)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Tata Motors announced that the all-new Tata Sierra SUV will launch on 25 November, returning the iconic nameplate with modern tech, multiple powertrains including ICE and EV, and advanced safety features such as six airbags and Level 2 ADAS.

- July 2025: Toyota Kirloskar Motor announced six airbags as standard across all Toyota Glanza variants, significantly strengthening occupant protection with full front, side, and curtain airbag coverage. This upgrade enhances the hatchback’s safety profile and aligns with rising demand for advanced airbag systems.

- April 2025: Maruti Suzuki India Limited announced that all its models will come equipped with six airbags as standard by the end of 2025, aligning with rising safety demands and regulatory trends.

- June 2023: Autoliv, Inc. unveiled its Bernoulli Airbag module, a new passenger-airbag system that uses Bernoulli’s fluid-dynamics principle to draw in ambient air for faster inflation, enabling larger cushions with a smaller single-stage inflator and reducing development time by over 30%.

- August 2021: Continental AG released details of its “Allround Protection” airbag control unit, which integrates pre-crash data and occupant-position monitoring to adapt airbag deployment strategy and adjust filling levels via a new valve technology.

REPORT COVERAGE

The global airbag electronics market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

Vehicle Type

Component Type

Airbag Type

Vehicle Class

Vehicle Propulsion

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.33 billion in 2025 and is projected to reach USD 7.37 billion by 2034.

In 2025, the market value stood at USD 2.29 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period.

The airbag ECU segment led the market by component type.

Stricter global safety regulations accelerate market adoption.

Key players in the global automotive market include Bosch, Continental AG, ZF Friedrichshafen, Denso Corporation, and Autoliv.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us