Air and Missile Defense Radar Market Size, Share, Growth & Industry Analysis, By Platform (Airborne, Land, and Naval), By Radar Type (X Band Radars and S Band Radars), By Application (Conventional and Ballistics Missile Defense), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

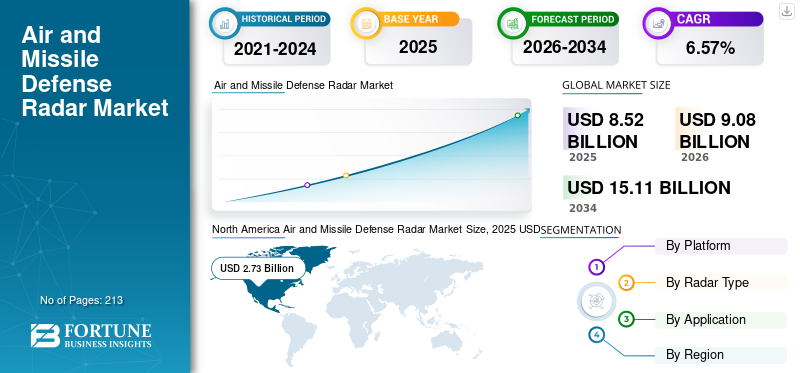

The global air and missile defense radar market size was valued at USD 8.52 billion in 2025. The market is projected to grow from USD 9.08 billion in 2026 to USD 15.11 billion by 2034, exhibiting a CAGR of 6.57% during the forecast period. North America dominated the air and missile defense radar market with a market share of 32.09% in 2025.

The COVID-19 pandemic has been unprecedented and staggering, with air and missile defense radars experiencing lower-than-anticipated demand across all regions compared to pre-pandemic levels. Based on our analysis, the global market exhibited a decline of 36.51% in 2020 as compared to 2019.

Armed forces across the globe utilize the air and missile defense radars to track aircraft, jets, destroyers, UAVs, weapon-carrying vehicles, and many more. Radars usually operate on a broad range of frequency bands such as HF, P, UHF, L, S, C, Ku, K, Ka, and many more. The frequencies of these bands range from 3 MHz to over 110 GHz. The air and missile defense radars consist of X band and S band radars only. X band usually comes with a smaller antenna and can be utilized over smaller platforms such as boats, aircraft, and so on. S band radars are utilized for specific applications to track targets in harsh environmental conditions. The S band radars' antenna is larger than the X band radars antenna. SPY-6 is a well-known AMDR system developed by Raytheon Technologies, which comes in several variants having X band, S band, or both frequencies.

Download Free sample to learn more about this report.

Global Air and Missile Defense Radar Market Overview

Market Size:

- 2025 Value: USD 8.52 billion

- 2026 Value: USD 9.08 billion

- 2034 Forecast Value: USD 15.11 billion, with a CAGR of 6.57% from 2026–2034

Market Share:

- North America led the air and missile defense radar market with a 32.09% share in 2025, driven by heavy investments in radar modernization, naval upgrades, and homeland defense systems.

- By radar type, the X band segment is projected to generate USD 6,949.5 million in revenue by 2025.

- By platform, the airborne segment is expected to hold an 18% share in 2025.

Key Country Highlights:

- The air and missile defense radar market in Japan is expected to reach USD 277.5 million by 2025.

- India is projected to witness a strong CAGR of 9.12% during the forecast period, while Europe is anticipated to grow at a CAGR of 5.61%.

- In July 2022, the U.K. Air Force announced an investment of nearly USD 2.8 billion to upgrade Eurofighter Typhoons with advanced ECRS Mk2 radars.

Air and Missile Defense Radar Market TRENDS

Technological Advancements in Fully/Hybrid Digital Beam Forming will Propel the Market Growth

Recent technological advancements in AMDR are the implementation of fully/hybrid beam forming for tracking targets in azimuth and elevation. The analog to digital converters installed in radars enhanced the range of target detection and operating flexibility compared to conventional radars. Developments in Gallium Nitride (GaN) paved the way for affordable, lightweight, and compact systems for AMDR. The quest to track more targets simultaneously has led to the development of high-density arrays installed over radars. This enables the radar to operate in a broad range of frequencies with enhanced operational efficiency. North America witnessed air and missile defense radar market growth from USD 2.73 Billion in 2025 to USD 2.91 Billion in 2026.

Download Free sample to learn more about this report.

DRIVING FACTORS

Developments in Hypersonic Missiles will Pave the Way for Advanced Air and Missile Defense Radars

Recent advancements in hypersonic missiles by countries such as the U.S., China, and Russia have posed major challenges to the detection of such high-speed objects before the impact. Other countries, such as India, Japan, Germany, France, and Australia, have also invested in the development of hypersonic missiles. In March 2022, Russia claimed to utilize hypersonic missiles against Ukraine. The Russian hypersonic missile has the capability to reach a top speed of Mach 10 and range over 1900 kilometers. The Chinese variant of a hypersonic missile is said to have a top speed of Mach 12 and a range of 1,500 kilometers. In October 2022, China claimed to develop a smaller variant of the existing hypersonic missile that can be launched through aircraft. To counteract such threats, countries across the globe have tested several measures. For example, the U.S. had tried to use a combination of SPY-6 radar and SM-6 missiles. Therefore, advancements in hypersonic missiles will catalyze the growth of technologically advanced air and missile defense radars.

Increasing Cross-border Tensions and Rising Defense Budget for Air and Missile Defense Radars to Catalyze the Growth of Market

Over the last decade, increasing cross-border conflicts, such as a conflict between China-Taiwan, Russia-Ukraine, Israel-Palestine, and many more, have changed governmental strategies of neighboring countries as well. For instance, in June 2022, the government of Canada planned to invest USD 4.9 billion to strengthen decade-old radar systems across Canada. Besides new procurements, countries have also started collaborating with each other to have a strategic advantage over rivalries. For example, in September 2022, the Indian government urged Bangladesh to speed-up the installation of coastline radars in Bangladesh. India had offered USD 500 million lines of credit to Bangladesh for the same in October 2019. Hence, rising conflicts have increased the demand for AMDR across the globe.

RESTRAINING FACTORS

Component Failures, Design Limitations, and Increased Costs of Maintenance & Upgrade Restrain Market Growth

Radar systems need to have higher operational efficiency, compatibility with different platforms, user-oriented advanced systems, and a broad frequency band. Sometimes, radars have to operate in harsh environmental conditions, which may lead to the failure of onboard components. For example, the U.S. Department of Defense has requested nearly USD 200 million for the upgrade, repair, and maintenance of 12 radars under Ballistic Missile Defense Systems (BMDS) program for FY 2023.

Besides repair and maintenance, the North Atlantic Treaty Organization (NATO) reformed the military standards for radar systems in 2020. So, to match NATO standards, all the members have to install/update new capabilities to allow full interoperability during joint operations with other NATO countries. Therefore, evolving military standards and maintenance costs of defense radars may hamper the Air and Missile Defense Radar Market growth.

SEGMENTATION Analysis

By Platform Analysis

To know how our report can help streamline your business, Speak to Analyst

Ground-based Air and Missile Defense Radars to be the Fastest Growing due to Higher Demand

By platform, the market is divided into airborne, land, and naval. In 2021, the naval segment dominated the market by having the air and missile defense radar market largest share. Land-based radars are estimated to be the fastest growing during the forecast period due to higher demand from Canada, Taiwan, Japan, India, and many more. The airborne segment is also anticipated to grow marginally due to higher demand for new fighter jets and the upgrade of onboard radars across the globe. The airborne segment is expected to hold a 19.63% share in 2021.

- In July 2022, the Irish government announced to spend USD 200.84 million for the procurement of land-based defense radars.

- In July 2022, the U.K. Air Force announced to invest nearly USD 2.8 billion to upgrade its fleet of Eurofighter Typhoon jets with ECRS Mk2 radars.

By Radar Type Analysis

Rising Demand for Long Range Radars will Boost Growth of S band Radars

Based on radar type, the market is divided into X band radars and S band radars. The S band segment is expected to be the fastest growing in the forecast period due to its technological advantage over X band radars. In April 2022, the U.S. awarded a five-year contract worth USD 3.2 billion to Lockheed Martin for AN/TPQ 53 radar. The X band segment is also anticipated to grow notably during the forecast period. In September 2022, Iran planned to install a horizon radar having 3,000 km of range. The X-band segment is projected to generate USD 6,949.5 million in revenue by 2025.

By Application Analysis

Ballistic Missile Defense to be the Fastest Growing during the Forecast Years due to Rising Ballistics Missiles Threats

Based on application, the market is divided into conventional and ballistic missile defense. The ballistic missile defense segment is projected to grow at the highest CAGR over the period of 2022-2029. Technological advancements in ballistic missiles and the rising use of such weapons will propel the growth of the segment. In March 2022, under a contract worth USD 700 million, the U.K. announced the procurement of one S band ballistic missile defense radar from the U.S. Conventional radars are expected to grow marginally due to increased investment from defense agencies across the globe. For instance, after the Russia-Ukraine war, several European countries have accelerated the procurement of air defense systems. Germany was the first country to buy an Arrow 3 missile interceptor from Israel after the war. The Czech Republic and several other countries are also planning to buy the Iron Dome system from Israel.

REGIONAL Analysis

The global market is segmented into North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America

North America Air and Missile Defense Radar Market Size, 2025 USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 2.73 billion in 2025 and USD 2.91 billion in 2026. North America is estimated to be the largest market. Land-based radars in North America are anticipated to be the fastest-growing in the region. Canada announced to invest USD 4.9 billion in improving the radar defense system across Canada. The growth of the naval segment is attributed to a higher investment of the U.S. navy in the procurement and upgrade of a fleet of destroyers. In April 2022, the U.S. Navy announced to equip every warship with SPY-6 radars to track missiles and planes.

Asia Pacific

The Asia Pacific market is expected to be the fastest-growing market due to higher defense spending by countries such as China, India, and Japan. Along with the defense budget, rising cross-border tensions between China-Taiwan, India-China, South & North Korea, and so on will propel the growth of the market in the forecast period. In August 2022, Taiwan signed a contract worth USD 83 million with the U.S. for Patriot 3 air defense system. Under the contract, existing systems would be upgraded from Patriot-2 to Patriot-3, having long-range missiles.

- The air and missile defense radar market in Japan is expected to reach USD 277.5 million by 2025.

- India is projected to witness a strong CAGR of 9.12% during the forecast period.

Europe

The Europe market is estimated to be the second largest market in 2021 and is expected to grow notably on account of increasing procurements of radars as a precautionary measure against Russia-Ukraine war-like situation. In March 2022, France appointed Indra to supply PSR2 radars at three air bases located in France. PSR2 is an S band radar, and it can also operate in rugged terrain and poor weather conditions. Europe is anticipated to grow at a CAGR of 5.61% during the forecast period.

Middle East & Africa

In the Middle East & Africa region, countries such as the UAE, Saudi Arabia, and Israel have emerged as potential markets and catalyzed the growth of radars in the region. In September 2022, Iraq inaugurated GM400 defense radar manufactured by Thales. GM400 is an S band radar with a range capability of 470 kilometers.

The South America region is expected to grow at a significant rate due to procurements from Brazil, Argentina, Colombia, Chile, and other countries. In September 2022, the Brazilian Army received two SABER M60 radars from Embraer, which can track 60 targets at a time with a range of 60 kilometers.

KEY INDUSTRY PLAYERS

Key Market Players are Focused on Providing Advanced Air and Missile Defense Radars

The competitive landscape and the continuously evolving market is consolidated in nature due to the presence of major players such as Thales Group, Israel Aerospace Industries, Lockheed Martin, Leonardo SPA, and Northrop Corporation. These major players are focusing on providing an advanced and compact AMDR for simultaneous tracking of multiple targets.

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- Hensoldt AG (Germany)

- Israel Aerospace Industries (Israel)

- Leonardo S.P.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Rheinmetall AG (Germany)

- SAAB AB (Sweden)

- Terma (Denmark)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS:

- In October 2022, the U.S. announced the sale of the National Advanced Surface-to-Air Missile System (NASAMAS) to Kuwait at USD 3 billion. NASAMAS will be manufactured by Kongsberg Defense and Aerospace and Raytheon Technologies.

- In July 2022, the Defense Ministry of U.K. planned to spend USD 2.7 billion to upgrade radars and other systems on Typhoon jets. Typhoon jets will be upgraded with ECRS Mk 2 radars.

- In May 2022, India claimed to procure 12 Swathi radars for tracking and surveillance of weapons near the India-China border. Swathi has the capability to track shells, mortars, and rockets within 50 kilometers of range.

- In April 2021, Germany injected over USD 126 million to install a radar warning system on its Tornado fleet of fighter aircraft.

- In March 2022, the U.K. announced the procurement of Ballistic Missile Defense Radar (BMDR) as a part of a USD 700 million deal from the U.S. Lockheed Martin is the prime contractor of this deal.

REPORT COVERAGE

The research report covers detailed information on the global market and focuses on aspects such as product types, recent developments, and key players. The report also provides insights into market trends in radar technologies, market competition, and market conditions by considering several ongoing and upcoming factors. Besides the above factors, the report has included several other factors to estimate the global market size.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2024 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform, By Radar Type, By Application, and By Region |

|

By Platform

|

|

|

By Radar Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights stated that the global market size was USD 9.08 billion in 2026 and is projected to reach USD 15.11 billion by 2034.

Registering a CAGR of 6.57%, the market will exhibit rapid growth during the forecast period.

The ballistic missile defense segment is expected to be the fastest-growing segment during the forecast period.

Thales Group, Lockheed Martin, IAI, Leonardo, and Northrop Corporation are the leading players in the global market.

North America topped the market in terms of share in 2026.

- 2021-2034

- 2025

- 2021-2024

- 213

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us