Surveillance Radars Market Size, Share, Growth, Russia-Ukraine War & Industry Analysis, By Platform (Airborne, Ground, Space, and Naval), By Radar Type (Short-Range, Medium-Range, and Long-Range), By Application (Commercial, Military, Homeland Security, and Others), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

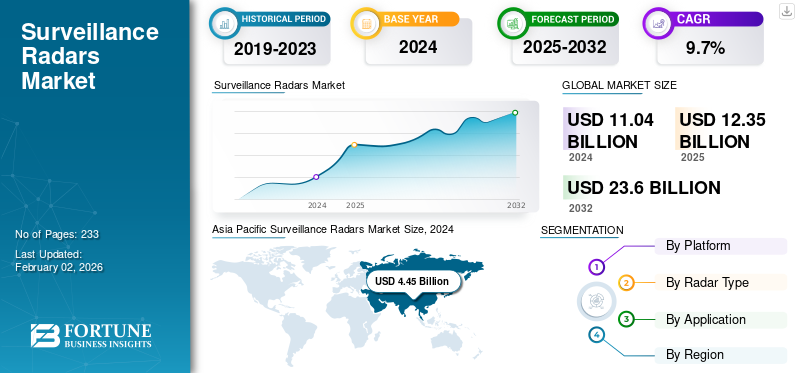

The global surveillance radars market size was valued at USD 11.04 billion in 2024. The market is projected to grow from USD 12.35 billion in 2025 to USD 23.60 billion by 2032, exhibiting a CAGR of 9.7% during the forecast period. Asia Pacific dominated the surveillance radars market with a market share of 40.31% in 2024.

Radars are essential for monitoring various activities in critical infrastructure and facilities such as airports, camps, borders, and ports. These systems are used to detect and track non-linear, cooperative, and moving targets for national security. They also play a key role in improving border security in both the commercial and defense sectors. Radar systems can operate across various platforms, including land, naval, air, and space, making them essential for border security operations.

Most radars operate within the S-band frequency range, primarily used for search and targeting functions. In addition, air-to-ground radars are valuable in aerospace and maritime security, enabling the detection of various targets, including aircraft, ultralight aircraft, stealth, Unscrewed Aerial Vehicles (UAV), and Unmanned Aerial Systems (UAS), helicopters, boats, and ships. These radar systems provide military and defense forces with critical support in tactical missions in unknown areas, operating within their line of sight.

Major players in the market include Northrop Grumman, Raytheon Technologies, Thales Group, Saab AB, Leonardo S.p.A., and Lockheed Martin, Northrop Grumman which offer advanced air and ground surveillance radars. Raytheon Technologies provides integrated radar platforms such as SENTINEL and AMDR systems. Thales Group specializes in multi-mode surveillance solutions for air, sea, and ground, including the Ground Master and STAR NG radars.

Download Free sample to learn more about this report.

SURVEILLANCE RADARS MARKET KEY TAKEAWAYS

- 2024 Market Size: USD 11.04 billion

- 2025 Market Size: USD 12.35 billion

- 2032 Forecast Market Size: USD 23.60 billion

- CAGR: 9.70% from 2026–2034

- Asia Pacific dominated the surveillance radars market with a market share of 40.31% in 2024.

- The military segment is projected to grow at the highest CAGR during the forecast period.

- The long-range segment held the largest market share and is expected to grow fastest over the forecast period.

North America

North America is projected to be the second-largest market, supported by strong defense budgets, coastline security requirements, and increasing procurement of advanced surveillance radar systems.

Europe

Europe is expected to witness significant growth due to rising defense investments, modernization of radar infrastructure, and increasing demand for customized threat detection systems.

Asia Pacific

Asia Pacific dominated the surveillance radars market with a market share of 40.31% in 2024.

U.S.

The U.S. market growth is supported by substantial military spending, modernization of defense equipment, and increasing deployment of advanced maritime and surveillance radar systems.

Japan

Japan is witnessing rising demand for advanced surveillance radar technologies due to increasing focus on national security, defense modernization, and regional threat monitoring.

Read More

RUSSIA-UKRAINE WAR IMPACT

Procurement of Surveillance Radars Raised Due to Russia-Ukraine War Impact

The war between Russia and Ukraine has disturbed the ability of the global economy to recover from the COVID-19 pandemic, at least in the short term. The war has resulted in economic sanctions from several countries, rising commodity prices, and supply chain disruptions that affected many markets worldwide. It has also changed how defense spending and purchases are approached. Many countries worldwide have reviewed their defense spending and procurement plans, adjusting them in response to situations such as the war between Russia and Ukraine. India, China, Canada, Estonia, Iraq, and Taiwan have prioritized their defense spending on the radar industry to build the necessary infrastructure to combat the growing security threats. Therefore, the war has driven a surge in global demand for radars.

- In June 2022, Blighter Surveillance Systems, a British designer and manufacturer of electronic scanning intelligence and surveillance solutions, supplied many of its A422 radars as part of an Anti-UAS capability to support Ukrainian forces in the ongoing conflict with Russia. The A422 is a medium-range military airborne radar capable of detecting and reporting air and ground targets up to 20 km away, with exceptional noise reduction near horizons, cities, and coastlines.

Countries involved in or affected by the conflict, such as Ukraine have focused on acquiring advanced surveillance radars to enhance their defense capabilities. For instance, in 2022 Ukraine received advanced radar systems such as the Blighter A422 radar from the Blighter Surveillance Systems. In addition, radar technology has become increasingly important for long-range targets and enhancing air defense systems.

- For instance, in May 2024, Sweden announced the donation of two Airborne Surveillance and Control (ASC) Radar aircraft to Ukraine as a part of a USD 1.3 million package to bolster the country’s defenses against Russia. This growing emphasis on surveillance radar systems in modern warfare further stimulates the growth of the market.

MARKET DYNAMICS

MARKET DRIVERS

Advancement in Border Surveillance System Increased Demand for Air Surveillance Radars

Border surveillance systems, such as autonomous drones and acoustic radar technologies, have evolved significantly and continue to advance. Mobile border security radars have enabled more effective border protection across various countries. These radars are used to increase the detection rate at strategic locations. In addition, state-of-the-art low-false-alarm radars have led countries facing border disputes, drug trafficking, and illegal immigration to these advanced radars to aid in border security. Thus, the radar market is expected to grow notably during the forecast period. Moreover, many countries are introducing surveillance radar systems to enhance their military capabilities.

- For instance, in February 2025, India unveiled a few new air surveillance radars at Aero India 2025, designed to enhance its military capabilities. One key system is the VHF SR RSV radar developed by the Electronics & Radar Development Establishment (LRDE) under the Defense Research and Development Organization (DRDO). This radar is specifically designed to detect stealth aircraft and operates within the 30–300 MHz frequency band.

Such developments and innovations are driving domestic industries to produce advanced air surveillance technologies and encouraging other countries to invest in similar indigenous technologies.

Expansion of New and Maintenance of Existing Airports to Propel Market Growth

Airport surveillance radars are in growing demand, primarily used in airports to reduce accidents. As radar technology advances, air travel becomes more efficient and safer. Governments have made enormous investments to increase internal security, introducing highly sophisticated airport radars. Additionally, the development of new and existing airports is one of the major factors driving the global surveillance radars market growth. In recent years, increased passenger air traffic has led to the development of airport radar systems to mitigate potential airport threats.

- In November 2022, Spanish technology and defense firm Indra was awarded a contract by German air navigation service provider DFS to upgrade the country's aerial radar network with new technology. The contract of more than USD 103 million will be realized within 13 years and contains an extension clause based on the release of various planned options.

Moreover, there is an increase in the construction of new airports across the globe to meet the rise in travel demand. The expansion of airport capacity, which results in increased air traffic, necessitates surveillance radars for efficient air traffic management. Numerous airports around the world are focusing on the installation of advanced surveillance radars for effective air traffic control.

- For instance, in December 2024, Thales secured a contract from the Dutch Air Navigation Services Provider to provide RSM NG, a digital Secondary Surveillance Radar at Schiphol Airport. The new radar replaced the current secondary radar, offering enhanced performance and reliability for safe and effective air traffic management.

MARKET RESTRAINTS

High Maintenance Cost is Hindering Market Growth

Radar requirements include high operational efficiency, advanced systems, cross-platform compatibility, and a wide frequency range. Radars can operate in very harsh environments, and failure of any battlefield equipment can cause catastrophic damage. In January 2023, Thales offered a USD 1850 million radar system along with supply and support services to French, Italian, and British Armies. Thales has signed a service contract with OCCAR (Organization for Joint Arms Cooperation) for the French, Italian, and British navies. This new significant service agreement covers three years with an optional two-year term.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence (AI) for Autonomous Target Recognition Present Opportunities for Market Growth

A key opportunity in the market is the integration of artificial intelligence technologies to enable autonomous target recognition and real-time data analysis. AI-powered radar systems can differentiate between objects, recognize patterns, and make rapid decisions without human intervention, significantly improving situational awareness and operational efficiency for both military and civilian applications. This capability addresses the growing demand for advanced border and infrastructure security, as well as air and maritime surveillance. Thus, the integration of AI for autonomous target recognition in radars to reduce response times and enhance detection accuracy presents significant opportunities for the growth of the market.

SURVEILLANCE RADAR MARKET TRENDS

Development of Active Electronically Steered Array Radar Production Drives Market Growth

Electronically Scanned Arrays (AESA) radar technology uses a new generation of Trans-Receive (TR) modules and high-performance Software-Defined Radios (SDRs), which can also be used for radio communications at very high data rates. AESA radars are extensively used to upgrade and replace older radar technologies. The AESA design uses a modular concept, increasing its reliability. Failure of a critical TR module does not render the entire radar unusable; the system can be restored by replacing the module quickly. As more key players invest in the production of AESA radar for modern surveillance applications, there is a rise in the growth of the market. For instance, companies such as Leonardo S.p.A. and Northrop Grumman provide active electronically scanned array radars in their product portfolio which are designed to detect and track various targets with high accuracy. These manufacturers continue to produce advanced AESA radar systems that provide fast scanning speeds, improved target tracking capabilities, and better resistance to jamming than traditional mechanical surveillance radars.

Furthermore, there is a rise in demand for AESA radar to obtain real-time situational awareness and long-range target detection. For instance, in June 2024, the Brazilian Air Force procured the Ground Master 200 Multi-Mission "All-in-One" (GM200 MM/A) radar to enhance its air surveillance and ground-based air defense capabilities. This radar features advanced 4D AESA technology, providing superior situational awareness and flexibility in detecting various threats.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Ground Segment Holds Leading Share due to Advancements in Surveillance

By platform, the market is classified into airborne, ground, space, and naval. In 2024, the ground segment dominated by holding the largest surveillance radars market share. Various countries are utilizing ground surveillance radar systems for protection against infiltration and identifying potential threats. For instance, in December 2024, Border Security Force (BSF) of India used a ground radar system and an anti-drone system for surveillance applications. The BSF is expected to employ surveillance radars to identify tunnels and stop intrusion activities across the Indo-Pakistan border in Jammu and Punjab.

The space segment is estimated to witness the fastest growth during the forecast period due to its technological advantage over other platforms. For instance, in March 2022, the Indian Space Research Organization (ISRO) announced the launch of a space-based radar for tracking space debris under the NETRA project. This project will be able to track debris over 1500 km of range. Moreover, there is an increase in demand for surveillance systems to protect space stations, satellites, and other space objects from high-speed space debris. For instance, in February 2025, Indra, a Spanish technology and defense company was awarded a contract from the German Air Force to supply a space surveillance radar to detect objects in low space orbits. The system is designed to protect operational satellites from potential collisions with debris from other space missions.

Increasing satellite targets and decreasing launch costs will further boost the growth of the space segment. The aviation and naval segments are also expected to grow marginally due to increased demand from airlines and navies or coastal forces.

To know how our report can help streamline your business, Speak to Analyst

By Radar Type

Long-Range Segment Dominated due to Increasing Defense Applications

Based on radar type, the market is trifurcated into short-range, medium-range, and long-range. The long-range segment held the largest market share and is expected to grow fastest over the forecast period. Rising applications in defense and space-based synthetic aperture radars will catalyze the growth of long-range radars. Moreover, there is an increase in demand for advanced long-range radar with high detection capabilities. For instance, in February 2024, Lockheed Martin promoted its TPY-4 ground-based long-range surveillance radar for the Republic of Singapore Air Force's (RSAF's) air-defense requirements. This radar offers improved detection range and performance compared to FPS-117 radars long-range surveillance radar.

Medium-range radars hold the second-highest share in the market, and the segment is anticipated to grow significantly due to upgrades and new procurements globally. Moreover, the increasing adoption of smart traffic management initiatives in several governments is backing the demand for short-range radars.

- In September 2022, the Iranian government announced the deployment of the horizon radar, capable of detecting targets within a range of 3,000 km.

By Application

Military Radars Segment to Dominate Due to Increased Defense Budget

Based on application, the market is divided into commercial, military, homeland security, and others. The military segment is projected to grow at the highest CAGR during the forecast period. Cross-border conflicts and increased defense budget are the main drivers for the growth of the military segment. Rising geopolitical tensions and regional modernization are fueling procurement and upgrade of radar systems for enhanced threat detection and multi-domain integration.

Business surveys are also expected to grow significantly due to increased demand from the aerospace industry.

Homeland security radars hold the third largest market share, with the growing focus on Artificial Intelligence (AI)-enabled traffic management systems driving the demand for home security radars.

The others segment includes radars used by wildlife departments, airlines, and many others to track animals, birds, and other moving entities.

Surveillance Radars Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

Asia Pacific Surveillance Radars Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is estimated to account for the highest market share during the forecast period. This market growth is attributed to the growing demand for advanced naval radars from developing countries such as India and China. In addition, the rise in the demand for enhanced national security and stable border integrity in the region has driven the need for sophisticated surveillance radar systems. For instance, in December 2024, India negotiated a USD 4 billion defense deal with Russia to procure the Voronezh radar system to strengthen India’s air defense and surveillance in Asia and the Indian Ocean. The advanced radar is expected to provide a strategic advantage to India by enhancing its situational awareness over critical regions, including China, South Asia, and the Indian Ocean. Therefore, the need to improve through advanced radar systems amid regional and global challenges is expected to drive the demand for surveillance radars.

North America is estimated to be the second-largest market. North American countries have large budgets for their defense departments. The U.S. has allocated significant military and defense spending to upgrade its aging fleet and procure advanced equipment for future endeavors. North America has an enormous coastline of about 8.5 lakh miles, which creates opportunities for deploying coast guard radar systems in the region. In addition, governments of the U.S. and Canada are allocating reasonable defense budgets to maintain their status as major powers, offering good opportunities to market players providing Coast Guard Radar Systems. Moreover, the defense forces of countries in the region collaborate with various radar manufacturing companies to manufacture radars that improve overall defense capabilities. For instance, in June 2024, the U.S. Navy awarded Raytheon Technologies Corporation a contract worth USD 677 million to produce AN/SPY-6(V) radars. Under this contract, the U.S. Navy would receive seven additional maritime surveillance radars, bringing the total number of radars for procurement to 38. Such strategies to produce surveillance radars on a large scale are expected to drive the surveillance radar market growth in the region.

Europe holds the third position and is expected to grow significantly during the study period due to increased investment in defense and commercial industries. Increasing investment by regional manufacturers to modernize production facilities and infrastructure will bring an advantage to companies operating in the radar sensor market. Additionally, the increase in industrial automation will positively impact market players, encouraging the development of new sensor technologies and helping them gain a high competitive advantage. There is also an increase in demand for customized radar systems in various countries of the region to achieve advanced threat detection at the frontline. For instance, in May 2023, the U.K. signed a contract with Elbit Systems UK to supply 90 GBSR systems between 2023 and 2024, with an option for an additional 40 systems. The radar will be customized and fitted with an optimized stabilization unit and capture software. Such developments to design and procure radar systems for improved frontline surveillance capabilities are expected to fuel the growth of the market in Europe.

In the Middle East & Africa, increased investments from the UAE, Saudi Arabia, and Israel are catalyzing the growth of the radar market. In August 2022, Spanish defense company Indra offered Saudi Arabia several radar systems for the Royal Saudi Air Defense Force (RSADF) and a Transfer of Technology (ToT) contract.

Latin America expects moderate growth due to new acquisitions from Brazil, Argentina, Chile, and other countries. For example, in April 2022, Thales announced it would install new air traffic radars in Calama, Chile, that will run entirely on solar energy. Moreover, the market for surveillance radar is expected to grow significantly in the region due to rise in investment in defense and security technologies. Brazil and Mexico are focusing on enhancing public safety and security. For instance, in December 2024, the Brazilian Army awarded a contract worth USD 16.6 million to Embraer for the supply of SABER M200 Vigilante S-band air surveillance radar to modernize its defense system.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Focusing on R&D Efforts to Develop Innovative Solutions

The global market is highly competitive with several major players dominating the market share. In recent years, the market has become highly competitive due to the rapid development of radar technology, with several companies focusing on research & development to create innovative solutions.

LIST OF KEY SURVEILLANCE RADARS COMPANIES PROFILED

- BAE Systems Plc (U.K.)

- Hensoldt AG (Germany)

- Leonardo S.p.A. (Italy)

- Honeywell International (U.S.)

- Lockheed Martin Corporation (U.S.)

- L3 Harris Technologies Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- SAAB AB (Sweden)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Israel Aerospace Industries (IAI) delivered its new C-catcher Multi-Mode, Multi-Role Airborne Surveillance Radar to a strategic customer, marking a significant advancement in airborne surveillance technology. The radar is equipped with GaN AESA technology which offers high performance and reliability in a compact package.

- December 2024: Saab received a contract worth USD 48 million for multiple Giraffe 4A radar systems from BAE Systems to support the U.S. Air Forces in Europe. The Giraffe 4A radar provides long-range surveillance and air base air defense capabilities in a highly mobile package.

- October 2024: BAE Systems and Leonardo UK successfully conducted the first flight test of the European Common Radar System Mark 2 (ECRS Mk2) on a UK Typhoon test aircraft. The ECRS Mk2 radar offers advanced capabilities, including traditional radar functions and electronic warfare.

- June 2023: BAE Systems awarded a USD 341 million (£270 million) contract to support, upgrade, and maintain critical radar systems for the Royal Navy. This 10-year contract covers the Artisan, Sampson, and Long-Range Radars used on various warships.

- March 2023: Blighter Surveillance Systems, a U.K.-based designer and manufacturer of electronic scanning radars and surveillance solutions, was awarded a contract to supply multi-modal A800 3D e-scanning radars to Raytheon UK for a laser weapons project with the U.K. Ministry of Defense.

- February 2023: Hensoldt won a contract from CAE Aviation to provide multi-functional surveillance radars for its surveillance aircraft.

- February 2022: SRC Inc. was awarded a contract worth USD 8.79 million from the U.K. to provide support services for the AN/TPQ-49 radar. The contract includes provisions for up to an additional USD 4.39 million in support services to be purchased.

REPORT COVERAGE

The research report offers a thorough analysis of the surveillance radars market. It focuses on essential factors such as the competitive landscape, key players in the market, top manufacturers, product categories, and popular uses for the service. The report includes several additional factors that have influenced the market's growth prospects in recent years. The report also identifies significant developments in the market and provides insights into market trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 9.7% from 2025 to 2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform · Airborne · Ground · Space · Naval |

|

By Radar Type · Short-Range · Medium-Range · Long-Range |

|

|

By Application · Commercial · Military · Homeland Security · Others |

|

|

By Region · North America o U.S. (By Platform) o Canada (By Platform) · Europe o U.K. (By Platform) o Germany (By Platform) o France (By Platform) o Italy (By Platform) o Russia (By Platform) o Rest of Europe (By Platform) · Asia Pacific o China (By Platform) o Japan (By Platform) o India (By Platform) o South Korea (By Platform) o Rest of Asia Pacific (By Platform) · Middle East & Africa o UAE (By Platform) o Saudi Arabia (By Platform) o Israel (By Platform) o Rest of Middle East & Africa (By Platform) · Latin America o Brazil (By Platform) o Argentina (By Platform) o Rest of Latin America (By Platform) |

Frequently Asked Questions

Fortune Business Insights states that the global market was valued at USD 11.04 billion in 2024 and is projected to reach USD 23.60 billion by 2032.

Registering a CAGR of 9.7%, the market will exhibit rapid growth during the forecast period.

The long-range segment dominated the market during the forecast period.

Raytheon Technologies, Thales Group, Lockheed Martin, and BAE Systems are the leading players in the global market.

Asia Pacific is expected to hold the largest market share.

The key factors driving the market growth are advancement in border surveillance system and increased demand for air surveillance radars.

The ground segment led the market by platform.

- 2019-2032

- 2024

- 2019-2023

- 233

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us