Aircraft Engine Blade Market Size, Share & Industry Analysis, By Type (Compressor Blades, Turbine Blades, and Fan Blades), By Material (Titanium Alloys, Nickel-based Alloys, and Composite), By Application (Commercial and Military), and Regional Forecast, 2026-2034

Aircraft Engine Blade Market Size And Industry Overview

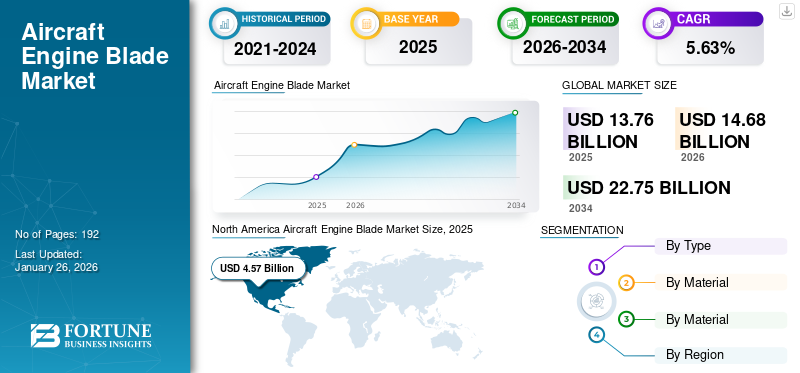

The global aircraft engine blade market size was valued at USD 13.76 billion in 2025 and is projected to grow from USD 14.68 billion in 2026 to USD 22.75 billion by 2034, exhibiting a CAGR of 5.63% during the forecast period. North America dominated the aircraft engine blade market with a market share of 33.21% in 2025.

An aircraft engine blade is a component of an aircraft engine designed to rotate and convert the hot energy and gases into rotational mechanical energy which is used to power the engine. There are three types of engine blade, compressor blades, turbine blades, and fan blades. The compressor blades are located in the compressor section of engine. They play a vital role in compressing the incoming air which creates the required pressure for combustion and energy extraction. Moreover, turbine blades are curved metal components fixed to the rotor of the turbine which are designed to extract energy from the hot gases by rotating in response to the flow of the gases.

In addition, fan blade is a structure that is part of the fan section of a turbofan engine. It consists of an airfoil shape with leading and trailing edges, pressure and suction sides, and extends radially outward from a central hub. General Electric, Safran, and Raytheon Technologies are some of the prominent market leaders in designing and manufacturing advanced engine blades, with GE and Safran jointly operating CFM International, which produces the widely used CFM56 and LEAP engines. These companies focuses on innovation and sustainability to strengthen while manufacturing engine blades their presence in the market.

Download Free sample to learn more about this report.

Aircraft Engine Blade Market Key Takeaways

- 2025 Market Size: USD 13.76 billion

- 2026 Market Size: USD 14.68 billion

- 2034 Forecast Market Size: USD 22.75 billion

- CAGR: 5.63% from 2026–2034

- North America dominated the aircraft engine blade market with a 33.21% share in 2025.

- The fan blade segment is projected to lead the market with a 43.78% share in 2026.

- The titanium alloy segment is expected to dominate with a 65.84% market share in 2026.

North America

Generated USD 4.57 billion in 2025, supported by aerospace innovation and strong commercial aviation demand.

Europe

Accounted for USD 4.17 billion in 2025, driven by advanced manufacturing and lightweight engine technologies.

Asia Pacific

Reached USD 3.60 billion in 2025, fueled by rising air travel and aerospace investments.

U.S

Projected to reach USD 4.08 billion by 2026, supported by aircraft deliveries and demand for fuel-efficient technologies.

Japan

Expected to reach USD 0.93 billion by 2026, driven by aviation expansion and adoption of advanced engine technologies.

Read More

Market Dynamics

Market Drivers

Rise in Aircraft Deliveries to Augment Market Growth

The growing need for high-speed data connectivity is one of the key drivers of growth in the market. The demand for air travel is significantly increasing. According to the International Air Transport Association (IATA) the aviation industry expecting a sustained period of growth over the next 20 years, with global passenger numbers anticipated to double to 8.2 billion by 2037. In October 2024, global air travel demand rose by 7.1% compared to the same month in 2023, as reported by the International Air Transport Association (IATA).

As air travel increases, there is a rise in need for expansion of airline fleets to accommodate more passengers. Thus, various airlines are ordering new aircraft at an increasing rate. For instance, Airbus, a Europe based aircraft manufacturer delivered 735 commercial aircraft in 2023, an 11% increase over 2022. In 2023, Boeing received a total of 1,314 net new orders (1,456 gross orders) prior to ASC 606 adjustments, marking an increase from the 774 net new orders (935 gross orders) recorded in 2022. Moreover, the number of aircraft orders is expected to increase gradually in 2024 due to rise in air traffic globally. For instance, in December 2024, Pegasus Airlines, a low cost airline based in Turkey orders up to 200 Boeing 737-10 aircraft to expand and modernize its single-aisle fleet.

This increase in aircraft production directly correlates with a higher demand for aircraft engine blades, which are essential components of aircraft engine. Therefore, the rise in aircraft deliveries due to increasing air traffic acts as a significant driver.

Market Restraints

High Material Costs and Strict Regulatory Standards May Hamper Market Growth

Engine blades in the aircraft are predominantly made from advanced materials such as nickel-based super alloys and titanium alloys. These materials are important for withstanding extreme temperatures and stresses during operation. Moreover, the manufacturing of engine blades involves complex processes that require precision and advanced technology.

Techniques such as CNC machining, casting, and electrochemical machining are used to achieve the necessary tolerances and surface finishes. The manufacturing of blade complex and intricate shape of blades of requires sophisticated machinery thus escalating the production costs. In addition, the industry is operated by strict regulations and standards regarding aviation safety. While these regulations are essential for ensuring safety, they can also slow down innovation and increase compliance costs for manufacturers.

Market Challenges

Environmental and Regulatory Pressures May Pose Challenges for Market

Environmental and regulatory pressures in the market stem from increasingly strict global standards aimed at reducing emissions and improving sustainability. Regulatory bodies such as FAA, EPA, and ICAO have introduced new rules limiting carbon particle, nitrogen oxide, and particulate matter emissions from aircraft engines, pushing manufacturers to adopt advanced materials and technologies that enhance fuel efficiency and lower environmental impact.

Market Opportunities

Stringent Emission Norms and Rise in Demand for Fuel-Efficient Engines Present Growth Opportunities

Various countries and regions across the world are implementing stringent emission norms to reduce greenhouse gas emissions. The Federal Aviation Administration (FAA) enforces standards set by the International Civil Aviation Organization (ICAO), which include a CO2 standard requiring new aircraft to achieve a 4% reduction in fuel consumption starting in 2028 compared to 2015 levels. Moreover, ICAO has set a long-term aspirational goal for its member states to achieve net-zero carbon emissions from international aviation by 2050. Emission standards encourage manufacturers to innovate and enhance the design of engine components, including turbine blades, compressor blades, and fan blades. This leads to the development of advanced materials and technologies that improve fuel efficiency and reduce emissions, ultimately boosting the demand for high-performance engine blades that meet new regulations. As manufacturers strive to enhance fuel efficiency, there is a growing focus on developing advanced materials for blade, such as lightweight composites and alloys. These materials help reduce overall engine weight, improve performance, and comply with stringent emission norms, driving innovation in the engine blade

Aircraft Engine Blade Market Trends

Adoption of Composite Material Aircraft Engine Blades

The use of composite materials in blades is becoming a significant trend, driven by the need for enhanced performance, weight reduction, and improved fuel efficiency. Composite materials, particularly Ceramic Matrix Composites (CMCs) and metal matrix composites, offer significant weight savings compared to traditional materials such as titanium and nickel-based super alloys. The reduced weight is critical for the improvement of aircraft efficiency and performance. Composites can withstand higher temperatures than conventional materials. This capability allows for higher operating temperatures in engine designs. Moreover, the demand for fuel-efficient aircraft is driving the need for lightweight and advanced engine blade designs.

Therefore, there is a rise in implementation of composite material to reduce the aircraft’s total weight. For instance, in February 2020, Rolls & Royce started manufacturing of fan blades made from composite material for its UltraFan demonstrator engine. The fan blades are constructed from hundreds of layers of Carbon Fiber Reinforced Polymer (CFRP), combined with toughness-enhanced resin materials and can reduce weight on twin-engine aircraft by 700kg.

Furthermore, in 2020, United Engine Corporation (UEC) together with relevant research institutes completed the development and manufactured the first prototypes of composite fan blades for the PD-35 engine. The first stage of testing of the PD-35 fan blade demonstrator took place on 27 June 2020 in Perm as part of the PD-14 engine. Therefore, the rise in use of composite material such as carbon fiber is expected to drive aircraft engine blade market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Fan Blade Segment Held the Largest Market Share Due to Development of Advanced High Temperature Resistant and High Performance Fan Blades

On the basis of type, the market includes compressor blade, turbine blade, and fan blade.

Fan blade segment is anticipated to hold the largest share of the market with a share of 43.78% in 2026. Moreover, the use of hybrid materials, such as 3D-woven composites combined with titanium increases the overall efficiency of engine which is further driving the demand for advanced engine fan blades.

The turbine blade market segment is expected to grow faster during the forecast period owing to the rise in upgradation of the blade structure. The rising volume of passengers and air cargo that airlines carry is increasing the need for new aircraft and spare parts, including compressor blades.

To know how our report can help streamline your business, Speak to Analyst

By Material

Titanium Alloys Segment Held Largest Share Due to Its High Strength, Heat Resistance, and Light Weight Properties

On the basis of material, the market is classified into titanium alloys, nickel-based alloys, and composite.

The titanium alloy segment is projected to remain the dominant component in the global aircraft engine blade market with a share of 65.84% in 2026. Titanium alloy is known for its high strength, low weight, and excellent heat resistance. Titanium alloys are capable of operating at temperatures from subzero to 600°C which makes them ideal for withstanding high temperature condition in engines. Numerous engine models such as CF6, GE90, and Rolls Royce Trent Series Engines are installed with engines made from titanium alloy material.

The composite segment is estimated to grow at a significant CAGR in the forecast period. Composite materials are multi-component materials made from two or more different constituents that when combined. Some current types of composite material used for aircraft engine blade is carbon fiber reinforced polymer (CFRP), ceramic matrix composite, boron fiber composite. These composites have high strength to weight ratio and are lighter than traditional materials used in aviation industry which has resulted in an increasing trend of use of composite material in manufacturing of engine fan blades.

For instance, in January 2025, Shanghai Aero Engine Composites Co., Ltd. (Shangfa Composites), a subsidiary of AVIC Composites celebrated the production of its first composite fan blade at a ceremony held in Lingang, Shanghai, China. Such developments are expected to fuel the growth of the aircraft engine blade industry in upcoming years.

By Application

Commercial Segment Holds Largest Share Due to Rising Air Travel and Passenger Traffic

On the basis of application, the market is classified into commercial and military.

Commercial segment is anticipated to hold the highest share of the aircraft engine blade market with a share of 68.34% in 2026, due to the increase in passenger traffic across the world. According to International Air Transport Association (IATA), global passenger demand for November 2024 witnessed 8.1% increase as compared to November 2023. Domestic air travel also experienced growth, with a 3.1% rise in demand and a 1.5% increase in capacity compared to November 2023. With the rise in air travel, airlines are encouraged to upgrade their commercial aircraft fleet to accommodate the meet the air traffic requirements which further increases the demand for aircraft engine and its components such as engine blades. Increasing demand for air travel and aircraft deliveries are boosting the growth of the aircraft engine blade industry.

The military segment is estimated to depict the fastest-growth owing to the increase in defense budget due to security concerns and current geopolitical tension. Many countries are significantly increasing their defense budgets to modernize and expand their air force capabilities. This investment creates a strong demand for advanced military aircraft engines, as governments seek to enhance their operational readiness and technological edge. Such factors are expected to drive the demand for aircraft engine blades in the military segment of the market.

Aircraft Engine Blade Market Regional Outlook

The global market is segmented on the basis of region into North America, Europe, Asia Pacific, and the rest of the World.

North America

North America Aircraft Engine Blade Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America currently holds the largest aircraft engine blade market share and is likely to remain dominant throughout the forecast period.The North America market generated USD 4.57 billion in 2025, representing 33.21% of the global market landscape, and is expected to reach USD 4.82 billion in 2026. The region benefits from a robust aerospace manufacturing base, with major companies such as Boeing, GE Aviation, and Pratt & Whitney leading the way in innovation and production. Increased defense spending and a strong demand for commercial air travel are driving growth. Moreover, there is a rise in significant development carried out by the major engine manufacturers in the region.

For instance, in October 2023, CFM International, a 50-50 joint venture between GE Aerospace and Safran Aircraft Engines announced launch of new High-Pressure Turbine (HPT) blade that is designed to extend the time on wing for the popular jet engine, the CFM56. Such developments are anticipated to drive the growth of the market in the region. Moreover, the rising demand for fuel-efficient aircraft in military sector is a key factor propelling the military aircraft engine blade demand. The U.S. market is experiencing strong growth, driven by rising aircraft deliveries, increased air travel, and the need for fuel-efficient, cost-effective planes. Major U.S.-based players such as General Electric, CFM International, Raytheon Technologies, and Albany International are investing in advanced composite materials and 3D printing to produce lighter, more durable blades. The U.S. market is valued at USD 4.08 billion by 2026.

Europe

Europe contributed 30.30% to the global market in 2025, with a valuation of USD 4.17 billion, and is projected to reach USD 4.46 billion in 2026. The aircraft engine blade market is dominated by North America and Europe due to the presence of key aircraft manufacturers such as General Electric, Pratt & Whitney, and others. Europe is expected to witness a steady growth in the aircraft engine blade market. The growth is attributed to strong aerospace manufacturers such as Rolls-Royce and Safran. The focus of various engine manufacturers in the region on the development of next-generation engines that meet stringent environmental standards is driving demand for lightweight and efficient engine blades. The European Union is committed to reducing carbon emissions. The current European Green Deal aims to reduce transport emissions by 90% by 2050. Such missions encourage adoption of material such as Ceramic Matrix Composites (CMCs) and advanced alloys to reduce emissions by improving aircraft efficiency. The UK market is valued at USD 1.43 billion by 2026, and the Germany market is valued at USD 1.48 billion by 2026.

Asia Pacific

Asia Pacific accounted for USD 3.6 billion in 2025, representing 26.19% of the global market share, and is projected to reach USD 3.9 billion in 2026. Asia Pacific is witnessing rapid growth in the market due to rising air travel demand and rise in investments in aerospace manufacturing. China and India are expanding their aviation industry which leads to more number of aircraft deliveries and the requirement for advanced engine technologies. Shanghai Aero Engine Composites' launch of composite fan blades in 2025 showcases the commitment of engine manufacturers in the region toward innovation of aircraft engines. Such initiatives aimed at enhancing aircraft engine efficiency are likely to drive further growth. The Japan market is valued at USD 0.93 billion by 2026, the China market is projected to valued at USD 1.61 billion by 2026, and the India market is projecte to valued at USD 0.68 billion by 2026.

Rest of the World

In 2025, the Rest of the World market stood at USD 1.42 billion, representing 10.29% of global demand, and is projected to grow to USD 1.5 billion in 2026. In rest of the world including regions such as Latin America and the Middle East & Africa, the market is growing at a moderate pace. The rising demand for aircraft engine blades is driven by increasing air passenger traffic in the region. Surge in investments in aviation infrastructure and rising passenger traffic are driving factors. Countries in these regions are gradually modernizing their fleets to improve efficiency and reduce operational costs. For instance, in October 2024, Boeing and LATAM Airlines Group, a passenger and cargo airline group in South America announced the purchase of 10 Boeing 787 Dreamliners with options for five more airplanes. Moreover, key players in the aircraft engine blade market are investing in research and development to innovate and improve blade technology, thereby driving market growth. Thus, as airlines seek to expand their fleet, there will be a growing demand for advanced engine blades that enhance performance and reliability which drives the growth of the market.

Competitive Landscape

Key Industry Players

Key Players Focus on Development of Technologically Advanced Products and Acquisition Strategies to Drive Growth

The prominent market players are prioritizing the advancement of their product offerings. The development of a diverse range of products and the rise in investment in research and development are key factors contributing to the market dominance of these players. The market is led by several players operating in this industry. Moreover, ley players in the aircraft engine blade are actively engaging in various strategies such as revenue analysis to enhance their market presence and respond to the growing demand for aircraft engines.

LIST OF KEY AIRCRAFT ENGINE BLADE COMPANIES PROFILED

- General Electric Company (U.S.)

- CFM International (U.S.)

- Safran SA (France)

- Raytheon Technologies Corporation (U.S.)

- Albany International Corp. (U.S.)

- Alcoa Corporation (U.S.)

- Rolls-Royce Holdings plc (U.K.)

- GKN Aerospace (U.K.)

- MTU Aero Engines AG (Germany)

- IHI AEROSPACE Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2024: GE Aerospace announced the expansion of its AI-enabled Blade Inspection Tool (BIT) to include two new inspection tools for the CFM LEAP and GE9X engines, as revealed during the 2024 MRO Europe Conference in Barcelona, Spain. The BIT leverages artificial intelligence to enhance the efficiency and precision of blade inspections.

- February 2024: Safran Aircraft Engines announced plans to establish a new foundry in Rennes, Brittany, dedicated to manufacturing turbine blades for its key engine programs, specifically the M88 used in defense applications and the CFM International LEAP engine utilized in commercial aviation.

- October 2023: CFM International introduced an upgraded High-Pressure Turbine (HPT) blade for its CFM56-5B and CFM56-7B engines, aimed at enhancing the durability and performance of these widely used commercial aircraft engines. This new blade design is informed by extensive field data collected over millions of engine flight hours, allowing for targeted improvements.

- December 2022: Safran Aero Boosters announced the establishment of a new production plant for compressor blades and vanes in the Walloon region of Belgium, specifically in the province of Liège. This initiative, revealed by CEO François Lepot, represents a significant investment of USD 56.77 million and aims to enhance the company's capabilities in manufacturing titanium compressor blades, including those used in the LEAP engine.

- February 2020: Rolls-Royce commenced production of the world's largest fan blades for its UltraFan demonstrator engine, which aims to set new benchmarks in efficiency and sustainability. The composite blades feature a remarkable 140-inch diameter, nearly matching the size of a narrowbody aircraft fuselage, and are being manufactured at the company's technology hub in Bristol, U.K.

REPORT COVERAGE

The report provides a detailed analysis of the sector and focuses on important aspects such as key players in the aircraft engine blade industry, component, platform, end-user, and applications depending on various regions. Moreover, the research report offers deep insights into the market trends, competitive landscape, revenue analysis, market competition, and market status and highlights key industry developments. Also, it encompasses several direct and indirect factors that have contributed to the sizing of the aircraft engine blade in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 5.63% from 2026 to 2034 |

|

Segmentation

|

By Type

|

|

By Material

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 14.68 billion in 2026 and is projected to reach USD 22.75 billion by 2034.

Registering a CAGR of 5.63%, the market will exhibit significant growth over the forecast period (2026-2034).

By material, the titanium alloy segment led the market.

General Electric Company is the leading player of the market.

North America dominate the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 192

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us