Aircraft De Icing Market Size, Share & Industry Analysis, By Operation Mode (Ground Spray and In-Flight Systems), By De-Icing Method (Fluids (Type I, Type II, Type III, Type IV, and Fluid (Weeping Wing) De-Icing), Pneumatic De-Icing Boots, Thermal [Bleed Air] De-Icing, Electro-Thermal Heating Systems, and Others), By Equipment (High-Reach Spray Trucks, Automated Pad/Gantry Sprayers, Compact/Towable Units, and Others), By Application (Commercial, Military, and General Aviation), By End User (Airports, Airlines, Aircraft OEMs, and Defense & Government Operators), and Regional Forecast, 2026-2034

Aircraft De Icing Market Size and Future Outlook

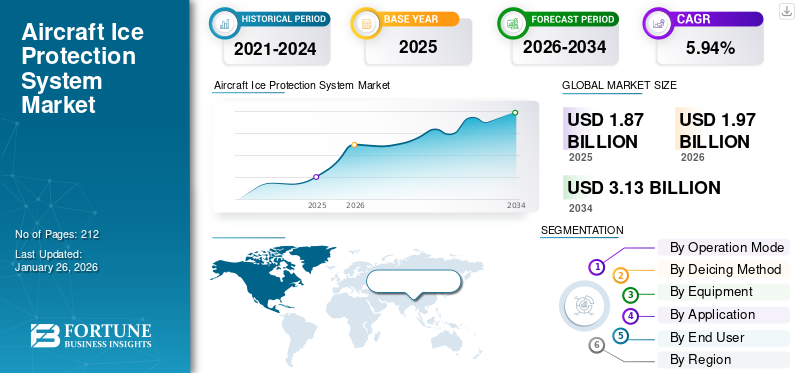

The global aircraft de-icing market size was valued at USD 1.87 billion in 2025 and is projected to grow from USD 1.97 billion in 2026 to USD 3.13 billion by 2034, registering a CAGR of 5.94% over the forecast period. North America dominated the aircraft de-icing market with a market share of 38.74% in 2025.

Aircraft de icing refers to the process, equipment, and chemical systems used to remove or prevent the accumulation of ice, frost, and snow on aircraft surfaces such as wings, fuselage, propellers, and control surfaces to ensure safe flight operations. The aircraft de-icing process typically involves specialized fluids (Type I, II, III, and IV) and ground-based or onboard systems that maintain aerodynamic performance and prevent ice-induced drag or lift loss.

Regulatory bodies such as the Federal Aviation Administration (FAA), the European Union Aviation Safety Agency (EASA), and Transport Canada Civil Aviation (TCCA) enforce strict operational and safety standards for deicing procedures, fluid usage, and environmental management. These regulations drive innovation in eco-friendly deicing formulations, automated ground handling systems, and efficient anti-icing technologies that minimize glycol runoff and environmental impact.

Leading industry participants including BASF SE, Clariant AG, Kilfrost Ltd, Vestergaard Company, and Textron Ground Support Equipment are at the forefront of developing next-generation aircraft de-icing solutions. These include glycol-free and bio-based fluids, infrared and electro-thermal deicing systems, and advanced deicing vehicles integrated with digital sensors and automation controls. In parallel, airport operators and airlines are investing in centralized deicing facilities, predictive weather analytics, and IoT-enabled monitoring systems to enhance operational efficiency and turnaround time during winter operations.

Download Free sample to learn more about this report.

Aircraft De-Icing Market Key Takeaways

- 2025 Market Size: USD 1.87 Billion

- 2026 Market Size: USD 1.97 Billion

- 2034 Forecast Market Size: USD 3.13 Billion

- CAGR: 5.94% from 2026–2034

- North America dominated the aircraft de-icing market with a 38.74% share in 2025.

- Ground spray systems held the largest market share by operation mode in 2025.

- Fluid-based de-icing dominated the market by deicing method due to its broad applicability and cost efficiency.

North America

North America generated USD 0.72 billion in 2025, accounting for 38.74% of global market revenue.

Europe

Europe reached USD 0.64 billion in 2025 and represented 34.25% of the global market.

Asia Pacific

Asia Pacific accounted for 20.49% of global revenue in 2025, with a market size of USD 0.38 billion.

U.S.

The U.S. aircraft de-icing market is projected to reach USD 0.63 billion by 2026.

Japan

The Japan aircraft de-icing market is projected to reach USD 0.09 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Frequency of Extreme Winter Conditions Driving Market Growth

The growing incidence of severe winter weather events caused by climate change is a primary factor propelling the aircraft de icing market forward. Increasing snowfall, freezing rain, and frost accumulation are compelling airlines and airports to adopt advanced deicing solutions to ensure operational safety and flight reliability. As air traffic continues to expand, particularly in North America and Europe, the demand for efficient deicing systems capable of handling high passenger volumes and larger aircraft has surged. Modern aircraft designs with complex aerodynamic surfaces also require precise and high-performance deicing equipment. Therefore, equipment manufacturers continue to develop technologically advanced aircraft de icing systems.

- In September 2024, Vestergaard Company launched OPTIM-ICE, a semi-automatic, LIDAR-guided deicing system designed to enhance operational safety and efficiency for narrowbody aircraft.

Governments and regulatory agencies such as the FAA and EASA are enforcing stringent safety regulators mandating deicing before takeoff, further boosting market adoption.

MARKET RESTRAINTS:

High Operational and Environmental Compliance Costs Restraining Market Expansion

One of the most significant restraints for the aircraft de icing market is the high operational and maintenance cost associated with deicing processes and environmental management. Deicing fluids, particularly glycol-based types, are expensive and must be replenished frequently during peak winter operations. Moreover, regulatory mandates require proper collection, treatment, and recycling of used fluids to prevent water contamination, increasing airport expenditure. Establishing fluid recovery and drainage systems adds substantial infrastructure and maintenance costs. Smaller regional airports often struggle to justify such investments, limiting the overall market penetration of advanced deicing systems.

MARKET OPPORTUNITIES:

Emergence of Eco-Friendly Systems and Glycol-Free Deicing Solutions Creating Market Opportunities

The development of sustainable and glycol-free de icing fluids presents a major opportunity for innovation and market expansion. With growing global focus on reducing environmental impact, chemical manufacturers are investing in bio-based and biodegradable formulations that minimize pollution while maintaining high deicing performance. These next-generation fluids can significantly lower the cost of recovery systems and wastewater treatment, offering long-term economic benefits to airports and airlines. Collaborative initiatives between aviation authorities, environmental agencies, and fluid producers are facilitating the approval and commercialization of green deicing alternatives. Moreover, the shift toward sustainable, energy-efficient, and low-maintenance deicing systems is presenting significant opportunities for market growth.

- In December 2023, Air Canada became the first airline to adopt De-Ice’s gallium nitride (GaN)-based electromagnetic de-icing technology, which replaces traditional glycol spraying with lightweight, tape-like heating strips that melt ice using high-frequency current

MARKET CHALLENGES:

Operational Complexity and Time Sensitivity Posing Major Challenges

A critical challenge for the aircraft de icing market growth is the need to maintain operational efficiency under highly constrained time windows during severe winter conditions. Coordinating deicing activities for multiple aircraft within limited turnaround times requires precise scheduling and communication among ground crews, pilots, and air traffic controllers. Any delay or inefficiency can cascade into flight disruptions and air traffic congestion. Moreover, the short holdover time of deicing fluids under extreme cold conditions necessitates swift and accurate application to ensure aircraft safety. Airports with limited infrastructure or insufficient deicing capacity face additional logistical challenges during peak winter periods.

AIRCRAFT DE ICING MARKET TRENDS:

Integration of Digital and Automated Technologies Emerging as a Key Market Trend

The adoption of digitalization, automation, and predictive analytics is emerging as a transformative trend in the aircraft de icing market. Airports and ground service providers are deploying IoT-enabled deicing trucks equipped with smart sensors that track fluid temperature, flow rate, and spray precision in real time. AI-driven weather analytics platforms are being integrated to predict frost and ice formation, allowing preemptive planning of deicing operations. Centralized digital command systems enable seamless coordination among multiple vehicles, optimizing scheduling and resource allocation. Drones and thermal imaging tools are also being introduced for quick detection of ice accumulation on aircraft surfaces. Furthermore, the transition toward electric and hybrid-powered deicing vehicles supports both sustainability and cost efficiency.

- In October 2025, Textron GSE launched the Safeaero 220E, an all-electric aircraft deicer featuring a lithium battery system, one-person operation, and advanced fluid management for enhanced efficiency.

Download Free sample to learn more about this report.

Segmentation Analysis

By Operation Mode

Ground Spray Systems Dominate Due to Established Use across Airports and Airlines

Based on operation mode, the market is bifurcated into ground spray systems and in-flight de-icing systems.

The ground spray segment holds the largest share, driven by its extensive deployment at commercial and military airports worldwide. These systems use glycol-based fluids dispensed through high-reach trucks or automated gantry systems to remove ice accumulation on aircraft surfaces prior to takeoff. The segment benefits from strict aviation safety regulations, increased winter flight operations, and expansion of ground handling infrastructure in colder regions.

- In December 2024, Vestergaard Company A/S introduced its next-generation Elephant Beta electric de-icing vehicle, designed to reduce glycol consumption and emissions at European airports.

The in-flight systems segment is expected to witness the fastest growth, driven by increasing adoption of electro-thermal and bleed-air systems in modern aircraft. OEMs are integrating these solutions into newer fleets to ensure continuous ice protection during flight and reduce turnaround delays.

By Deicing Method

Fluid-Based De-Icing Leads Owing to Broad Applicability and Cost Efficiency

Based on deicing method, the market is segmented into fluids, pneumatic de-icing boots, thermal (bleed-air) systems, electro-thermal heating systems, and others. Fluids is further divided into Type I, Type II, Type III, Type IV, and Fluid (Weeping Wing) De-Icing.

The fluid-based de-icing segment dominates the market, primarily due to its wide-scale use across airports and ease of application on various aircraft types. Demand for eco-friendly and less-corrosive glycol blends is further stimulating innovation among chemical suppliers such as Clariant and Kilfrost.

- Clariant AG provides SAFEWING® MP IV LAUNCH fluid in its product portfolio formulated for extended holdover times and reduced environmental impact.

Electro-thermal heating systems are anticipated to record the fastest growth, as airlines and OEMS move toward lightweight, energy-efficient alternatives that eliminate chemical use. Integration of gallium nitride (GaN)-based electromagnetic de-icing technologies such as that adopted by Air Canada in 2025 highlights the shift toward next-generation thermal systems.

By Equipment

Rising Fleet Modernization Expected to Propel High-Reach Spray Trucks Segment Growth

On the basis of equipment, the market is divided into high-reach spray trucks, automated pad/gantry sprayers, compact/towable units, and others.

The high-reach spray trucks segment accounted for the largest share in 2024, supported by their extensive use in large and medium-sized airports for de-icing narrow- and wide-body aircraft. These vehicles offer mobility, operational flexibility, and advanced fluid control systems.

- In June 2025, Textron Ground Support Equipment Inc. introduced the Premier TT4000 tanker truck, designed to rapidly refill active de-icers on the ramp to minimize downtime and boost airport productivity.

The automated pad/gantry sprayers segment is poised for the fastest growth as airports invest in automated, fixed-base systems to minimize turnaround times, improve fluid recovery, and meet sustainability goals.

By Application

Commercial Aviation Segment Dominates with Rising Global Passenger and Fleet Operations

By application, the market is segmented into commercial, military, and general aviation.

The commercial aviation segment holds the largest share, attributed to the increasing number of commercial aircraft movements in winter-prone regions and strict de-icing compliance protocols set by aviation authorities. The expansion of low-cost carriers and international routes is further amplifying demand. There is a rise in demand for efficient deicing services for smooth operations during winter operations.

- In September 2024, dnata, a global air travel services provider, secured a multi-year ground handling contract with easyJet at Zurich Airport (ZRH), Switzerland for providing ground handling services including deicing services.

The military aviation segment is projected to grow at the fastest rate, driven by the need for operational readiness in adverse weather conditions. Defense fleets are increasingly equipping aircraft with in-flight anti-icing systems to maintain mission continuity and reduce maintenance downtime.

To know how our report can help streamline your business, Speak to Analyst

By End User

Airports Dominate Owing to Large-Scale De-Icing Infrastructure and Operational Responsibility

Based on end user, the market is segmented into airports, airlines, aircraft OEMS, and defense & government operators.

The airport segment commands the largest market share as most de-icing operations are conducted by airport authorities or contracted ground service providers. Major hub airports across North America and Europe are investing in centralized de-icing pads and glycol recycling systems to enhance efficiency and reduce environmental footprint. Moreover, with increase in traffic there is an increase in demand for ground support and efficient de-icing services at airports, which is driving segment growth.

For instance, Aviator Airport Alliance signed a new three-year contract with easyJet to provide ground handling and de-icing services at Tromsø Airport (TOS), starting November 11, 2024. The winter schedule includes 14 weekly flights connecting Tromsø to major European cities such as Amsterdam (AMS), Bristol (BRS), Berlin (BER), London-Gatwick (LGW), Geneva (GVA), Manchester (MAN), and Paris (CDG).

Moreover, airlines represent the fastest-growing end user segment. Many carriers are increasingly internalizing de-icing operations to control costs, improve turnaround reliability, and align with sustainability goals. The growing use of real-time weather analytics and AI-based de-icing scheduling systems further supports this shift.

Aircraft De Icing Market Regional Outlook

North America Aircraft De-Icing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market was valued at USD 0.72 billion in 2025, capturing 38.74% of global revenue, and is estimated to reach USD 0.77 billion in 2026. North America holds the largest global aircraft de icing market share and is expected to maintain its dominance and significant growth over the forecast period. The region generated USD 0.68 billion in 2024, supported by the presence of major aircraft manufacturers, established airline operators, and stringent regulatory standards enforced by the Federal Aviation Administration (FAA) and Transport Canada Civil Aviation (TCCA). Frequent snowstorms and freezing rain across the U.S. and Canada drive strong demand for efficient and environmentally compliant deicing systems. Leading players such as BASF SE, Clariant AG, Kilfrost Ltd., and Vestergaard Company Ltd. have a strong operational presence in the region, focusing on advanced fluid formulations, automated deicing vehicles, and centralized deicing facilities. Moreover, equipment manufacturers are focused on development of efficient, space-saving ground support equipment for deicing due to increase in air traffic. The U.S. market is projected to reach USD 0.63 billion by 2026.

- In September 2025, Oshkosh AeroTech unveiled the Tempest-si, a compact, durable, and corrosion-resistant deicer designed for efficient operation on congested ramps, featuring intuitive controls and enhanced operator visibility for improved spray accuracy.

Europe

In 2025, Europe held 34.25% of the global market, reaching a valuation of USD 0.64 billion, and is projected to grow to USD 0.68 billion in 2026. Europe is projected to witness substantial growth in the aircraft de icing market, driven by stringent environmental regulations, widespread adoption of sustainable aviation practices, and continuous innovation in deicing technology. The European Union Aviation Safety Agency (EASA) mandates strict guidelines for deicing operations, encouraging airports and airlines to adopt eco-friendly, biodegradable fluids and advanced waste recovery systems. The U.K., Germany, France, and the Nordic nations experience severe winter conditions, necessitating high-performance, energy-efficient deicing systems. The UK market is projected to reach USD 0.13 billion by 2026 and the Germany market is projected to reach USD 0.14 billion by 2026. As airlines seek to reduce delays and improve operational efficiency during harsh winter conditions, there is increased demand for advanced de-icing solutions and professional ground handling services in Europe.

- In June 2025, Aviator Airport Alliance extended its partnership with Finnair to provide de-icing and winter services at Helsinki Airport through the 2025-2028 seasons, continuing its role using 9 de-icing units operating at two pads. The agreement also includes winter-specific operations such as aircraft heating and engine covering.

Asia Pacific

The market in Asia Pacific reached USD 0.38 billion in 2025, representing 20.49% of total market revenue, and is projected to reach USD 0.4 billion in 2026. Asia Pacific is anticipated to be the fastest-growing market for Aircraft De Icing during the forecast period. Rising air traffic, expanding airline fleets, and increasing occurrence of winter conditions in northern regions of China, Japan, and South Korea are driving the need for modern deicing infrastructure. Governments are investing heavily in airport development projects and cold-weather flight safety measures to support the rapidly growing aviation sector. The Japan market is projected to reach USD 0.09 billion by 2026, the China market is projected to reach USD 0.17 billion by 2026, and the India market is projected to reach USD 0.02 billion by 2026.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 0.07 billion in 2025, accounting for 3.66% share, and is expected to reach USD 0.07 billion in 2026. Latin America is experiencing gradual but consistent growth in the market, supported by expanding aviation infrastructure and growing awareness of flight safety in adverse weather conditions. While the region’s tropical climate limits widespread icing incidents, Chile, Argentina, and southern Brazil regularly face frost and snow in high-altitude or winter seasons, necessitating reliable deicing capabilities.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 0.05 billion, representing 2.86% of global demand, and is projected to grow to USD 0.06 billion in 2026. The Middle East & Africa (MEA) is poised for steady growth, driven by expanding aviation hubs, growing international air traffic, and the modernization of airport infrastructure in colder high-altitude and desert-night environments. While most Middle Eastern nations experience mild winters, countries such as Turkey, Iran, and parts of northern Saudi Arabia are investing in preventive deicing and anti-icing systems for safety assurance.

COMPETITIVE LANDSCAPE

Key Industry Players

Chemical Innovation, Equipment Integration & Airport Service Alliances Strengthen Market Leadership

The global aircraft de-icing market is driven by the rising imperative of operational safety and regulatory compliance in cold-weather aviation operations. Airlines and airports worldwide are investing heavily to ensure timely flight departures, avoid ice-related disruptions and comply with environmental mandates concerning de-icing fluid usage and runoff management. Aircraft De Icing market growth is further propelled by the convergence of chemical innovation (for advanced de-icing/anti-icing fluids), ground support equipment (GSE) modernization (e.g., self-propelled de-icing trucks, hybrid/electric systems), and digital/automation enhancements (such as predictive weather analytics, fluid-holdover time monitoring and telemetry).

Key players shaping the ecosystem include BASF SE, Clariant AG, Kilfrost Ltd., Textron Ground Support Equipment Inc., Global Ground Support LLC, Vestergaard Company A/S, and JBT Corporation. These chemical and equipment vendors are complemented by specialist service providers and airport ground handling companies that enable integrated de-icing solutions. Similarly, companies such as Textron and Vestergaard are developing next-generation de-icing trucks with electric or hybrid drives, automated spray booms, and real-time telemetry that deliver faster application, improved safety, and lower fluid usage. The competition is increasingly shaped by who can deliver the most efficient, environmentally compliant and operationally cost-effective de-icing solution rather than price alone.

LIST OF KEY AIRCRAFT DE ICING COMPANIES PROFILED:

- BASF SE (Germany)

- Clariant AG (Switzerland)

- Kilfrost Ltd. (U.K.)

- Textron Ground Support Equipment Inc. (U.S.)

- JBT Corporation (U.S.)

- Vestergaard Company A/S (Denmark)

- Integrated Deicing Services (IDS) (U.S.)

- Cryotech Deicing Technology (U.S.)

- Menzies Aviation (U.K.)

- Dow Inc (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- August 2025: Aviator Airport Alliance, a provider of aviation services at 15 Nordic airports and part of Avia Solutions Group extended its partnership with Wizz Air for three more years, continuing to provide ground handling services including de-icing services at Copenhagen Airport, Gothenburg Landvetter Airport, and Malmö Airport.

- July 2025: Boeing entered an exclusive master distribution agreement with Ice Shield, a leading provider of de-icing products, to enhance safety and operational efficiency in the Business and General Aviation (BAGA) and regional carrier markets.

- January 2025: Pulkovo Airport in Russia started using domestically manufactured de-icing equipment for the first time, marking a shift toward local sourcing that cut costs by 3-4 times compared to foreign alternatives.

- November 2024: Clariant expanded its storage capacity at its Uddevalla facility in Sweden to support increased use of recycled mono propylene glycol (MPG) in aircraft de-icing fluids. This expansion includes two new storage tanks and a truck unloading station,

- February 2023: Vestergaard Company received an order for six additional fully electric Elephant e-BETA deicers for Calgary International Airport, adding to the 12 units purchased in 2022.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics, and market trends expected to drive the market in the forecast period. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. The market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.94% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Operation Mode, By Deicing Method, By Equipment, By Application, By End User, and Region |

| By Operation Mode |

|

| By Deicing Method |

|

| By Equipment |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global size was valued at USD 1.87 billion in 2025 and is projected to grow from USD 1.97 billion in 2026 to USD 3.13 billion by 2034

In 2025, the market value stood at USD 0.72 billion.

The market is growing at a CAGR of 5.94% during the forecast period of 2026-2034.

The ground spray segment led the market by operation mode.

The market is expected to grow owing to factors such as rising frequency of extreme winter conditions.

BASF SE (Germany), Clariant AG (Switzerland), Kilfrost Ltd. (U.K.), Textron Ground Support Equipment Inc. (U.S.), and others are some of the prominent players in the market.

North America dominated the market in 2024 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 212

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us