Thermal Imaging Market Size, Share & Industry Analysis By Type (Handheld and Fixed/Mounted), By Technology (Cooled, Uncooled), By Product (Thermal Camera, Thermal Scopes, Thermal Module), By Wavelength (Shortwave Infrared (SWIR), Mid-wave Infrared (MWIR)), By Application (Border Surveillance, Vehicle Targeting, C-UAS), By Vertical (Aerospace and Defense, Law Enforcement, Healthcare, Automotive), and Regional Forecast, 2026-2034

Thermal Imaging Market Size and Industry Overview

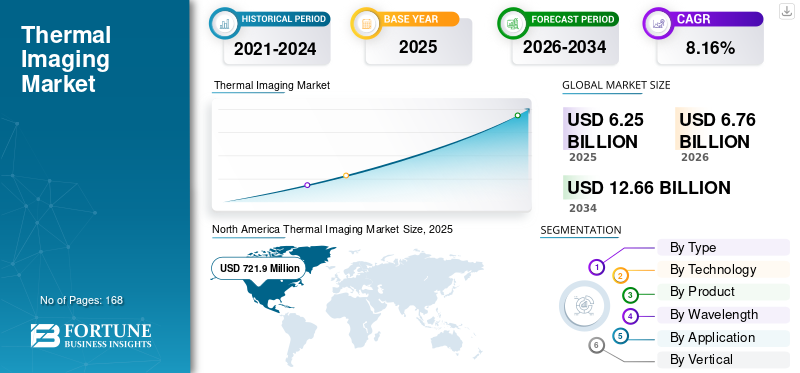

The global thermal imaging market size was valued at USD 6.25 billion in 2025. The market is projected to grow from USD 6.76 billion in 2026 to USD 12.66 billion by 2034, exhibiting a CAGR of 8.16% during the forecast period. North America dominated the thermal imaging market, accounting for a 31.8% market share in 2025. Defense modernization, industrial safety requirements, the adoption of healthcare diagnostics, automotive sensor integration, and the expansion of global surveillance infrastructure drive this industry growth.

The market growth is primarily driven by the rising demand for advanced thermal imaging solutions in end-use verticals, including military and defense, manufacturing, and healthcare & life sciences. In addition to this, the increasing penetration of advanced driver-assistance systems (ADAS) and growing demand for wireless temperature sensors are expected to boost the growth of the market during the forecast period.

The thermal imaging market continues to expand as infrared sensing becomes integral to safety, security, diagnostics, and automation across both civilian and defense domains. Thermal imaging systems convert heat differentials into visual data, enabling visibility in low-light, obscured, or zero-visibility conditions. This functional advantage positions thermal imaging as a mission-critical sensing technology rather than a discretionary enhancement. As a result, the thermal imaging market size growth remains structurally supported across multiple verticals.

Defense and security applications remain foundational. Border surveillance, vehicle targeting, and counter-unmanned aerial systems (C-UAS) rely heavily on thermal imaging to detect, classify, and track threats, regardless of lighting or weather conditions. Governments continue modernizing surveillance and situational-awareness systems, sustaining demand for both cooled and uncooled thermal technologies. These procurement programs help maintain the long-term stability of thermal imaging market share among established vendors.

Commercial and industrial adoption broadens the demand base. In automotive systems, thermal imaging supports advanced driver-assistance systems and night-vision capabilities. In healthcare, infrared imaging enables non-contact temperature screening, vascular assessment, and the detection of inflammation. Industrial users utilize thermal cameras for predictive maintenance, electrical inspections, and process monitoring, thereby reducing downtime and safety risks. These applications extend the thermal imaging industry beyond traditional defense dependence.

Technology evolution shapes competitive dynamics. Advances in uncooled microbolometers reduce cost and size, supporting mass-market adoption. At the same time, cooled infrared systems maintain relevance where range, sensitivity, and precision are paramount. Buyers are increasingly evaluating systems based on resolution, sensitivity, wavelength compatibility, and software integration, rather than relying solely on hardware.

Thermal imaging market trends reflect diversification rather than substitution. Defense sustains volume and margins, while automotive, healthcare, and industrial segments drive incremental growth. Vendors capable of balancing performance, cost efficiency, and regulatory compliance will secure durable positions as thermal imaging becomes embedded across global sensing ecosystems.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Thermal Imaging Market TRENDS

Thermal Camera is Widely Used to Measure Body Temperature to Help Control the Spread of Disease

The COVID-19 pandemic has created a significant demand for thermal imaging solutions across various industries, including healthcare, life sciences, transportation, and others. Several businesses and facilities are implementing temperature screening systems in their spaces to reduce the spread of disease.

The Chinese police are using thermal cameras and goggles to identify pedestrians with high temperatures. Even the Dubai police are using AI-based thermal smart helmets to scan and identify individuals with high body temperatures. As several countries begin to ease COVID-19 lockdowns, businesses are looking towards products as a fever screening tool to keep staff and customers safe from viruses. North America's thermal imaging market grew from USD 683.7 million in 2018 to USD 721.9 million in 2019.

- For example, in April 2020, the e-commerce giant Amazon installed thermal cameras equipped with this technology in six U.S. facilities situated in Seattle and Los Angeles to screen employees’ health.

Uncooled thermal technology continues to gain share due to declining costs and improving resolution. Advances in microbolometer fabrication enable the development of smaller, lighter, and more power-efficient devices, supporting applications in handheld and automotive environments.

Sensor fusion represents a key trend, as thermal imaging is increasingly integrated with visible cameras, radar, and artificial intelligence-based analytics. This fusion improves object classification and situational awareness, especially in autonomous and surveillance systems. Software-driven differentiation grows in importance. Image processing, analytics, and edge computing enhance detection accuracy and reduce operator workload. Vendors that invest in embedded software platforms strengthen their competitive positioning.

Miniaturization also shapes market trends. Compact thermal modules enable integration into drones, vehicles, and portable medical devices. This trend expands use cases without compromising performance. Across various applications, buyers are shifting their focus from standalone hardware to integrated sensing solutions. Thermal imaging is increasingly used as a component within broader perception and monitoring architectures.

Thermal Imaging Market Growth Drivers

Proliferation of Thermal Cameras for Border Surveillance Management to Propel the Market Growth

The market growth is attributed to the increasing adoption of advanced thermal imaging cameras in the military and defense industries, which cater to the demand for combat operations and nighttime patrolling. These cameras can identify targets at extremely long range, even during poor weather conditions. In border surveillance, equipment such as binoculars, monoculars, and military vehicles is used for perimeter surveillance, as well as remotely operated turrets.

- For instance, in March 2020, FLIR Systems, Inc. launched a high-definition midrange surveillance system called “Ranger HDC MR” to detect illegal activities even in degraded weather conditions.

Defense and security modernization remains the most influential driver within the thermal imaging industry. Armed forces and border agencies rely on thermal imaging for persistent surveillance, target acquisition, and threat detection under adverse conditions. Ongoing investments in border control, maritime security, and counter-drone systems directly support sustained demand for high-performance thermal sensors.

Industrial safety and maintenance requirements further accelerate adoption. Thermal imaging enables early detection of overheating components, electrical faults, and mechanical stress. Utilities, manufacturing plants, and energy operators utilize thermal cameras to minimize unplanned outages and enhance worker safety. This preventative value proposition continues to justify capital expenditure even during broader economic uncertainty.

Automotive integration represents a growing structural driver. Thermal imaging supports night-vision systems and pedestrian detection, particularly in premium and autonomous vehicle platforms. As regulatory frameworks emphasize the use of advanced safety systems, thermal sensors gain relevance in complementing radar and visible cameras.

Healthcare adoption reinforces market momentum. Non-contact diagnostic imaging reduces the risk of infection and supports the early detection of circulatory or inflammatory conditions. Hospitals and clinics are increasingly viewing thermal imaging as a supplementary diagnostic tool, rather than a novelty for screening purposes. Together, these drivers reflect a market grounded in functional necessity. Thermal imaging addresses visibility, safety, and diagnostic challenges that conventional sensors cannot reliably solve, anchoring long-term market growth.

RESTRAINING FACTORS

Export Restrictions Imposed on these Products to Limit the Market Growth

Thermal imaging products have always had an export sensitivity issue. Exporting thermal and infrared cameras to certain countries is restricted by the U.S. Government, and these export restrictions fall under the International Traffic in Arms Regulations (ITAR). Some cameras fall under specific Export Control Classification Number (ECCN) codes, which are governed by the Bureau of Industry and Security, an agency of the U.S. Department of Commerce. Manufacturing companies need to follow all the rules and regulations imposed by the government; otherwise, they will have to pay a huge penalty.

- For instance, in May 2018, FLIR Systems Inc., the infrared and these imaging systems, was accused of violating the International Traffic in Arms Regulations (ITAR) and the Arms Export Control Act (AECA). The company was hit with USD 30 million in civil penalties for this major deemed export compliance case.

This might slow the adoption of these devices, such as thermal cameras and scopes, in the market.

High system cost remains a persistent restraint, particularly for cooled thermal imaging technologies. Precision optics, cryogenic cooling, and advanced detector materials elevate pricing, limiting adoption to defense and high-end industrial users. Budget constraints can delay procurement cycles, especially in emerging economies.

Regulatory controls also influence market accessibility. Export restrictions on high-resolution thermal sensors complicate international sales and supply-chain planning. Compliance requirements add administrative overhead and constrain addressable markets for certain vendors.

Technical limitations persist in some use cases. Thermal imaging does not provide fine visual detail or color differentiation, requiring integration with visible-spectrum sensors for complete situational awareness. This dependency increases system complexity and total cost of ownership.

In healthcare, reimbursement uncertainty slows adoption. While thermal imaging offers diagnostic value, inconsistent regulatory approval and reimbursement frameworks limit widespread clinical integration. These restraints do not negate market growth but shape purchasing behavior. Buyers prioritize clear operational justification, lifecycle cost transparency, and regulatory alignment before committing to large-scale deployments.

Market Opportunities

Automotive safety systems present a significant growth opportunity. As advanced driver-assistance systems evolve toward autonomy, thermal imaging offers complementary sensing for low-visibility scenarios. Wider adoption beyond premium vehicles could materially expand the market size.

Healthcare diagnostics remain underpenetrated. Standardization of clinical protocols and reimbursement frameworks could accelerate adoption across hospitals and outpatient facilities. Thermal imaging’s non-invasive nature aligns with preventive care trends.

Industrial automation creates additional opportunities. Integration with predictive maintenance platforms and digital twins increases value beyond inspection, positioning thermal imaging as an analytics input rather than a standalone tool. Emerging markets offer long-term potential. Infrastructure expansion, border security investment, and industrialization increase demand for cost-effective thermal solutions.

Vendors that align product development with affordability, integration, and regulatory compliance are well-positioned to capture these opportunities as thermal imaging use cases continue to broaden.

Segmentation Analysis

By Type Analysis

Handheld Segment is Anticipated to Exhibit a Higher Growth Rate in the Coming Years

Based on device type, the market is segmented into handheld and fixed/mounted devices. The handheld sub-segment is further categorized into thermal weapon sights, handheld surveillance sights, and others.

The handheld segment is projected to be the fastest-growing segment owing to its portability and ease of use characteristics. The growth is attributable to the integration of thermal imaging tools in smartphones. Handheld thermal imaging devices hold a significant position within the thermal imaging market due to their portability, rapid deployment, and ease of use.

Defense personnel, law enforcement officers, firefighters, and industrial inspectors rely on handheld units for real-time situational awareness. These devices support patrol operations, search and rescue missions, and on-site diagnostics without requiring fixed infrastructure. Advances in battery efficiency, display resolution, and ergonomic design continue to improve operational usability. As costs decline for uncooled sensors, handheld thermal imaging expands beyond specialist users into broader industrial and utility applications.

The fixed/mounted segment holds the largest market share. The growth is attributed to the increasing demand for fixed CCTVs for surveillance and security purposes. A fixed or mounted device position eliminates the need for a person to scan and detect objects or living creatures.

Fixed or mounted thermal imaging systems dominate applications requiring continuous monitoring and long-range detection. Border surveillance, perimeter security, critical infrastructure protection, and vehicle-mounted defense systems rely heavily on fixed installations. These systems integrate with command-and-control platforms and operate continuously in harsh environments. Mounted solutions often support higher-resolution sensors and advanced optics, improving detection range and accuracy. Growth in smart city surveillance and transportation infrastructure reinforces demand. Fixed systems remain capital-intensive but deliver sustained value through reliability and integration capabilities.

By Technology Analysis

Uncooled Segment is Expected to Grow Significantly in the Forecast Period

Based on the technology, the market is further segregated into cooled and uncooled.

The cooled segment captures the maximum thermal imaging market share, as cooled devices can detect smaller temperature variations due to their highly sensitive nature. Cooled thermal imaging systems deliver superior sensitivity, longer detection ranges, and higher image fidelity. Defense and aerospace platforms depend on cooled sensors for target acquisition, missile guidance, and long-range surveillance. These systems perform well in extreme conditions where precision is critical.

However, cryogenic cooling increases cost, size, and maintenance requirements. As a result, cooled technology remains concentrated in military, border security, and high-end scientific research applications. Despite limited volume, cooled systems contribute disproportionately to the thermal imaging market value.

The uncooled segment exhibited a high growth rate during the forecast period. Uncooled thermal devices are much less expensive than their counterparts and can be manufactured in fewer steps with higher yields. These types of devices are primarily suited for applications where the monitoring area is within a range of 4-5 km.

Uncooled thermal imaging technology represents the fastest-growing segment by unit volume. Microbolometer-based sensors operate without cryogenic cooling, reducing cost and power consumption. This enables widespread adoption across automotive, industrial inspection, healthcare, and handheld security devices. Continuous improvements in resolution and sensitivity narrow the performance gap with cooled systems for short- to mid-range applications. Uncooled technology underpins mass-market expansion, making it a core driver of thermal imaging market growth during the forecast period.

By Product Analysis

To know how our report can help streamline your business, Speak to Analyst

Thermal Camera Segment to Apprehend Largest Market Share

Based on the product, the market is divided into thermal cameras, thermal scopes, and thermal modules.

The thermal camera held the highest market share during the forecast period. The growth is attributed to the increasing adoption of thermal cameras in both commercial and residential sectors. Thermal cameras constitute the largest product segment within the thermal imaging market. These systems provide standalone imaging for surveillance, inspection, and diagnostics.

Industrial users deploy thermal cameras for electrical inspection, mechanical monitoring, and energy audits. Defense and law enforcement agencies use them for reconnaissance and situational awareness. Advances in connectivity allow cameras to integrate with analytics platforms and cloud-based monitoring systems. As software capabilities improve, thermal cameras evolve into data-generating assets rather than simple visualization tools.

The thermal scopes segment is estimated to show the highest CAGR during the forecast period. The growth is owing to the increasing demand for thermal scopes from the military and defense sectors. The thermal modules segment holds a significant market share due to their low weight, small size, and low power consumption features. The thermal camera segment is expected to hold a 57.6% share in 2019.

Thermal scopes are primarily used in defense, law enforcement, and wildlife monitoring. Mounted on weapons or observation platforms, scopes enable target detection in complete darkness or adverse weather. Military modernization programs sustain demand for ruggedized, high-resolution thermal scopes. Civilian adoption remains regulated but persists in hunting and wildlife management where permitted. Thermal scopes emphasize optical precision, durability, and fast response, reinforcing their specialized role within the broader market.

Thermal modules support system integration across various applications, including automotive, drones, robotics, and industrial equipment. These compact components allow original equipment manufacturers to embed thermal sensing into larger platforms. Automotive night-vision systems, unmanned systems, and smart infrastructure increasingly rely on modular thermal components. This segment benefits from miniaturization and standardization, supporting scalable production and broader adoption. Thermal modules enable innovation by reducing integration complexity for system designers.

By Wavelength Analysis

Mid-wave Infrared (MWIR) Segment to Exhibit the Highest CAGR

Based on wavelength, the market is segmented into shortwave infrared (SWIR), mid-wave infrared (MWIR), and long-wave infrared (LWIR).

Shortwave Infrared imaging operates in the near-infrared spectrum and captures reflected rather than emitted radiation. SWIR excels in applications requiring material identification, moisture detection, and imaging through glass. Industrial inspection, semiconductor manufacturing, and scientific research rely on SWIR capabilities. Although not a traditional thermal band, SWIR complements thermal imaging in multi-spectral systems. Its role grows as users demand richer data from combined sensing architectures.

The mid-wave infrared (MWIR) is projected to be the fastest-growing segment in the years to come. The growth is attributable to its ability to operate efficiently in harsh environments, such as those with aerosols, smoke, or fog. Mid-wave Infrared imaging offers high sensitivity and long-range performance, making it essential for defense and aerospace applications. MWIR sensors support missile tracking, airborne surveillance, and precision targeting. These systems often require cooling, contributing to higher costs.

Despite this, MWIR remains indispensable for missions where detection accuracy and range cannot be compromised. Continued defense investment sustains this segment’s relevance within the thermal imaging industry.

The Longwave infrared (LWIR) segment holds the highest market share. The growth is attributed to technological advancements and the growing adoption of LWIR cameras in security and surveillance applications. Shortwave Infrared (SWIR) devices pose limited benefits compared to MWIR and LWIR.

By Application Analysis

Adoption of Thermal Cameras for C-UAS Purposes to Surge

Based on application, the market is categorized into border surveillance, vehicle targeting, C-UAS, maritime & coastal surveillance, critical infrastructure, and others.

The border surveillance segment holds the largest market share. The growth is owing to the increasing demand for these devices and rising government spending in the military and defense sectors. Border surveillance represents a core application for thermal imaging systems. Governments deploy thermal cameras to monitor land and maritime borders under all visibility conditions. Thermal imaging detects human movement, vehicles, and vessels beyond visible-light limitations. Integration with radar and analytics platforms enhances threat assessment. Ongoing geopolitical tensions and migration pressures sustain long-term demand.

- According to the Stockholm International Peace Research Institute (SIPRI) Military Expenditure Database, in 2019, the global military expenditure is estimated at around USD 1,917 billion, 3.6% higher than in 2018.

Vehicle targeting systems rely on thermal imaging for the detection, identification, and tracking of targets in military operations. Thermal sensors provide resilience against camouflage, smoke, and darkness. Modern combat vehicles integrate thermal imaging with fire-control systems, improving engagement accuracy. This application remains concentrated within defense budgets but delivers high-value contracts for vendors.

The counter-unmanned aircraft system (C-UAS) is expected to be the fastest-growing segment in the coming years. The rising demand for thermal scopes, modules, cameras, and others for vehicle targeting, critical infrastructure will aid the growth of the market. Counter-unmanned aerial systems increasingly incorporate thermal imaging to detect and track drones. Small unmanned systems often evade radar but emit distinct thermal signatures. Thermal imaging enables early detection and classification, supporting airspace security around critical infrastructure and military installations. As drone threats proliferate, this application expands rapidly.

By Vertical Analysis

Aerospace and Defense Segment to Account for Maximum Share

By vertical, the global market has been categorized into aerospace and defense, law enforcement, healthcare, automotive, oil and gas, residential, manufacturing, and others.

The aerospace and defense segment holds the maximum share in the market, as this type of imaging technique is a cost-effective alternative to lighting systems that are installed to safeguard borders. The thermal devices are used in armored vehicles, weapon stations to provide situational awareness to the military personnel.

Aerospace and defense dominate the thermal imaging market share due to sustained procurement of surveillance, targeting, and reconnaissance systems. Defense platforms demand high reliability, long lifecycle support, and regulatory compliance. Thermal imaging remains integral to modern military doctrine, ensuring consistent investment.

The law enforcement segment is expected to exhibit the highest CAGR in the coming years. Thermal imaging devices help law enforcement officers to effectively manage operations, investigate crime scenes, and trace and apprehend suspects. Thermal imaging cameras are also used by maritime law enforcement officers for coastal security, harbor navigation, and search and rescue operations. In addition, the increasing adoption of these devices in healthcare, automotive, oil and gas, residential, manufacturing, and other verticals is expected to fuel the growth of the market.

Law enforcement agencies use thermal imaging for search and rescue, suspect tracking, and surveillance. Non-lethal situational awareness drives adoption, particularly in urban environments. Budget constraints influence purchasing cycles, but operational benefits support steady growth.

Healthcare applications include temperature screening, vascular analysis, and inflammation detection. Thermal imaging offers non-contact diagnostics, aligning with infection control protocols. Adoption depends on regulatory approval and clinical validation but shows gradual expansion.

Automotive integration of thermal imaging supports night vision and advanced safety systems. Premium vehicles lead adoption, but broader integration is expected as sensor costs decline. Automotive applications represent a strategic growth frontier for the thermal imaging industry.

REGIONAL Analysis

North America Thermal Imaging Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Geographically, the market is segmented across five major regions, namely North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America Thermal Imaging Market Analysis

North America is expected to dominate the market in terms of share during the forecast period. This growth is attributable to the presence of a considerable number of device manufacturers and providers. The growing investment by the government in the military and defense sector has also contributed to the growth of the market.

- For instance, in 2019, military investment in the US accounted for around USD 732 billion, which grew by 5.3% from the previous year. The US accounted for around 38% of global military spending in 2019.

North America holds a leading share of the thermal imaging market due to sustained defense spending, advanced border surveillance programs, and early adoption of industrial inspection technologies. Aerospace and defense remain primary demand drivers, supported by homeland security and infrastructure protection initiatives. Strong research ecosystems accelerate sensor innovation. Regulatory clarity and procurement consistency enable vendors to deploy advanced thermal imaging solutions across military, law enforcement, and industrial sectors.

United States Thermal Imaging Market

The United States anchors regional demand through defense modernization, public safety investments, and industrial automation adoption. Military programs emphasize cooled and mid-wave infrared systems for targeting and surveillance. Civil applications expand across utilities, automotive safety, and healthcare screening. Federal funding stability and structured procurement frameworks support long-term deployments. Domestic manufacturers benefit from strong integration capabilities and established supplier relationships.

Asia-Pacific Thermal Imaging Market Analysis

Asia Pacific is expected to hold a strong position in the coming years. The growth is ascribable to the rising military expenditures to upgrade their military weapons will drive the market. Currently, China is the second-largest country with high spending on its military across the world.

- According to the Stockholm International Peace Research Institute, in 2019, Southeast Asia invested around USD 34.5 billion in the military and defense sector, which increased by around 4.2% from 2018.

Asia-Pacific demonstrates the fastest growth trajectory in the thermal imaging market. Rising defense budgets, infrastructure expansion, and industrial automation fuel adoption. Governments invest in border surveillance and maritime security. Manufacturing scale in the region accelerates sensor cost reductions. Commercial applications expand across automotive safety, smart cities, and utility inspection, broadening the regional demand base.

Japan Thermal Imaging Market

Japan’s thermal imaging market reflects a strong emphasis on precision, reliability, and compact system design. Defense applications focus on surveillance and maritime monitoring. Industrial sectors deploy thermal imaging for predictive maintenance and quality control. Automotive manufacturers integrate thermal sensors into advanced safety systems. Japan’s technological depth supports innovation in uncooled sensors and miniaturized thermal modules.

China Thermal Imaging Market

China’s thermal imaging market expands through defense modernization, public safety deployment, and industrial digitization. Domestic manufacturers scale production of uncooled sensors, improving affordability. Government investments support border security, smart surveillance, and infrastructure monitoring. Export-oriented production strengthens China’s role in global thermal imaging supply chains, particularly in cost-sensitive commercial applications.

Europe Thermal Imaging Market Analysis

Europe is expected to hold a significant share in the global thermal imaging market during the forecast period. The rising use of the product in security and surveillance applications is expected to boost the demand in Europe. The Middle East & Africa (MEA) and Latin America regions are expected to experience a gradual CAGR during the prediction period. This growth is owing to the increasing defense budget and rising investments by the government to adopt advanced solutions.

Europe’s thermal imaging market reflects balanced growth across defense, automotive, and industrial inspection applications. Regulatory focus on safety and energy efficiency drives adoption in infrastructure monitoring and transportation. Defense spending varies by country but remains aligned with NATO modernization priorities. European manufacturers emphasize uncooled technology innovation and system integration, supporting steady expansion across commercial and security-focused applications.

Germany Thermal Imaging Market

Germany’s thermal imaging market benefits from strong industrial manufacturing, automotive engineering leadership, and defense procurement discipline. Industrial inspection and automotive night-vision systems drive commercial demand. Defense investments prioritize border security and vehicle-mounted surveillance platforms. German buyers emphasize reliability, calibration accuracy, and compliance with stringent technical standards. This focus sustains demand for high-quality thermal imaging systems and modular components.

United Kingdom Thermal Imaging Market

The United Kingdom maintains steady thermal imaging demand through defense modernization, border monitoring, and critical infrastructure protection. Military applications dominate spending, particularly in surveillance and counter-unmanned aerial systems. Civil adoption expands in transportation safety and law enforcement. The UK’s emphasis on integrated sensing platforms supports demand for analytics-enabled thermal imaging solutions across public-sector deployments.

Latin America Thermal Imaging Market Analysis

Latin America shows gradual thermal imaging adoption driven by border security, infrastructure monitoring, and utility inspection. Budget constraints influence purchasing decisions, favoring uncooled systems with lower lifecycle costs. Public safety agencies increasingly deploy thermal imaging for search and rescue operations. Economic volatility limits large-scale defense procurement but supports selective, application-driven growth.

Middle East & Africa Thermal Imaging Market Analysis

The Middle East & Africa thermal imaging market is shaped by security requirements, energy infrastructure protection, and border surveillance needs. Defense and oil, and gas sectors dominate demand. Harsh environmental conditions favor ruggedized thermal systems. Government-led procurement drives adoption, while commercial usage remains selective but expanding across utilities and critical infrastructure monitoring.

Competitive Landscape

Emphasis of Key Players towards Developing Innovative Thermal Imaging Solutions to Strengthen Competition

Major players such as BAE Systems, PLC, Thales Group, Leonardo, S.p.A., and FLIR Systems, Inc. are strengthening their market position by launching new product lines to cater to military applications. FLIR Systems, Inc. offers safety and security solutions such as advanced intelligence, surveillance, reconnaissance, thermal imaging, and other sensing technologies. The company’s industrial business unit manufactures and develops thermal imaging devices and components.

The thermal imaging market features a competitive mix of global defense contractors, specialized sensor manufacturers, and system integrators. Leading vendors maintain broad portfolios spanning cooled and uncooled technologies, supported by long-term defense contracts and industrial supply agreements. Their strengths include vertically integrated manufacturing, proprietary detector designs, and strong lifecycle support capabilities. These players capture significant thermal imaging market share through scale, reliability, and compliance with military and industrial standards.

Niche players focus on uncooled microbolometer innovation, compact thermal modules, and application-specific imaging solutions. Many target automotive safety, industrial inspection, and drone payload markets. Their agility enables faster product iteration and customization. These firms often compete on cost efficiency, size reduction, and integration flexibility rather than raw performance metrics. As commercial demand expands, niche providers play a growing role in market diversification.

Partnerships are central to competitive positioning. Sensor manufacturers collaborate with optics specialists, analytics software providers, and system integrators to deliver end-to-end solutions. Defense primes partner with subsystem suppliers to meet program-specific requirements. Automotive original equipment manufacturers engage thermal imaging vendors for advanced driver-assistance system integration. These alliances shorten development cycles and improve deployment scalability.

Competitive differentiation increasingly depends on:

- Detector sensitivity and image resolution

- Cost-performance balance for uncooled systems

- Integration with analytics and artificial intelligence platforms

- Compliance with export controls and regulatory frameworks

- Reliability under extreme environmental conditions

As buyers prioritize total system performance rather than standalone hardware, vendors that align sensors, software, and services within cohesive architectures strengthen long-term competitiveness. The thermal imaging industry favors suppliers with proven operational track records and adaptable technology roadmaps.

List of Top Thermal Imaging Companies:

- BAE Systems Plc (Farnborough, United Kingdom)

- Leonardo S.p.A. (Rome, Italy)

- Thales Group (La Défense, France)

- FLIR Systems, Inc. (Oregon, United States)

- American Technologies Network Corporation (California, United States)

- Fluke Corporation (Washington, United States)

- Thermoteknix Systems Ltd. (Cambridge, United Kingdom)

- Seek Thermal, Inc. (California, United States)

- Cantronic Systems, Inc. (British Columbia, Canada)

- Excelitas Technologies Corp. (Waltham, Massachusetts, United States)

- Opgal Optronic Industries Ltd. (Israel)

- Dali Technology Co., Ltd. (Zhejiang, China)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Teledyne FLIR expanded its uncooled thermal camera portfolio to address industrial automation needs, integrating enhanced microbolometer sensitivity and onboard analytics to improve fault detection and predictive maintenance accuracy.

- January 2025: Leonardo S.p.A. introduced an upgraded mid-wave infrared sensor for airborne surveillance platforms, designed to improve long-range target detection through advanced cryogenic cooling and image stabilization technologies.

- September 2024: L3Harris Technologies secured a defense contract to deliver vehicle-mounted thermal imaging systems, aimed at enhancing situational awareness using high-resolution sensors integrated with fire-control and command systems.

- July 2024: Hikmicro launched a compact thermal module for automotive safety applications, focusing on cost-efficient uncooled technology and standardized interfaces to support large-scale vehicle integration.

- April 2024: Rheinmetall AG partnered with a European optics firm to develop next-generation thermal imaging sights, combining improved detector sensitivity with ruggedized optics for modern infantry systems.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The thermal imaging market research report provides a detailed industry analysis and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the key market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the key growth of the advanced market over the recent years.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021 – 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 – 2034 |

|

Historical Period |

2021 – 2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type Handheld Thermal weapon sights Handheld surveillance sights Others Fixed/Mounted |

|

By Technology Cooled Uncooled |

|

|

By Product Thermal Camera Thermal Scopes Thermal Module |

|

|

By Wavelength Shortwave Infrared (SWIR) Mid-wave Infrared (MWIR) Longwave Infrared (LWIR) |

|

|

By Application Border Surveillance Vehicle Targeting C-UAS Maritime & Coastal Surveillance Critical Infrastructure Others (Thermal Imaging in Machinery, Medical, and Firefighting, etc.) |

|

|

By Vertical Aerospace and Defense Law Enforcement Healthcare Automotive Oil and Gas Residential Manufacturing Others (Utility, Chemical, etc.) |

|

|

By Region North America (U.S. and Canada) Europe (UK, Germany, France, Russia, Rest of Europe) Asia Pacific (China, Japan, India, Southeast Asia, and the Rest of Asia Pacific) Middle East & Africa (South Africa, GCC, and the Rest of the Middle East & Africa) Latin America (Brazil, Mexico, and the Rest of Latin America) |

Frequently Asked Questions

According to Fortune Business Insights, the global thermal imaging market was valued at USD 6.76 billion in 2026, projected to reach USD 12.66 billion by 2034 at a CAGR of 8.16% during 2026–2034.

Thermal imaging is widely used for military surveillance, border security, healthcare diagnostics, industrial inspection, fever detection, and automotive safety systems such as ADAS. It enables temperature measurement and night vision by detecting infrared radiation.

The market is expected to grow at a CAGR of 8.16% in the forecast period (2026-2034).

Key growth drivers include rising demand in military and defense, increasing adoption in healthcare for fever screening, proliferation of ADAS in vehicles, and growing use of wireless thermal sensors in smart infrastructure and manufacturing plants.

Major industries include aerospace and defense, law enforcement, automotive, healthcare, oil & gas, residential, and manufacturing. Among them, aerospace & defense dominates due to its extensive use in combat operations, vehicle targeting, and night surveillance.

Major trends include AI-powered thermal detection, integration of thermal cameras with IoT and digital twins, rising adoption of mid-wave infrared (MWIR) sensors, and increased use of handheld thermal devices for both consumer and defense applications.

North America holds the largest market share, accounting for 31.8% in 2019, due to high military spending, strong presence of key manufacturers, and early adoption of advanced surveillance technologies in sectors such as defense and industrial automation.

Key restraints include export regulations under ITAR and ECCN, high initial cost of advanced systems, and limited benefits of shortwave infrared (SWIR) devices. Compliance with U.S. trade laws significantly impacts global market accessibility.

The uncooled thermal imaging segment is experiencing rapid growth due to its cost-effectiveness, lightweight design, and high production yields, making it ideal for applications requiring shorter detection ranges and scalable deployment.

Prominent companies include FLIR Systems, BAE Systems, Thales Group, Leonardo S.p.A., Seek Thermal, and Fluke Corporation. These firms focus on developing innovative thermal solutions for both commercial and military applications, often leveraging AI and sensor fusion technologies.

- 2021-2034

- 2025

- 2021-2024

- 168

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us