Aircraft Ignition System Market Size, Share & Industry Analysis, By Aircraft Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, and Unmanned Aerial Vehicle (UAV)), By Engine Type (Turboprop Engine, Turbofan Engine, Turbojet Engine, and Piston Engine), By System Type (Electric Ignition and Magneto Ignition), By Component (Ignition Leads, Igniters, Spark Plugs, Exciters, and Others), and Regional Forecast, 2026-2034

Aircraft Ignition System Market Size and Industry Overview

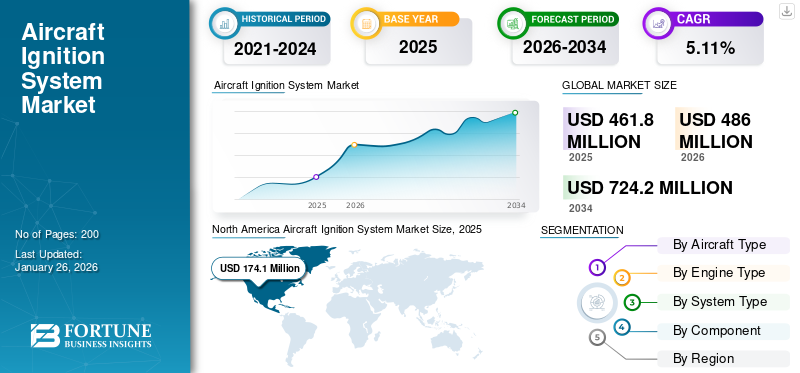

The global aircraft ignition system market size was valued at USD 461.80 million in 2025 and is projected to grow from USD 486.00 million in 2026 to USD 724.20 million by 2034, exhibiting a CAGR of 5.11% during the forecast period. North America dominated the global market with a share of 37.70% in 2025.

The demand for aircraft ignition systems is fueled by expanding commercial and general aviation fleets, increased air travel, and a growing focus on engine efficiency and reliability. Turbofan-powered aircraft and electric ignition systems lead the market due to their high performance and durability. The aftermarket remains dominant, as MRO activities and routine engine overhauls sustain continuous replacement demand for igniters, spark plugs, and exciters. Technological advancements, including lightweight designs, solid-state ignition controls, and digital diagnostic systems, further enhance adoption, ensuring the market’s long-term stability across civil, military, and unmanned aviation platforms.

Leading companies such as Champion Aerospace, Tempest Aero Group, and Hartzell Engine Technologies anchor the market with wide product portfolios and certified reliability. TransDigm Group plays a pivotal role through component integration and global aftermarket reach. Electroair, SureFly, and G3i advance electronic ignition conversion systems, enhancing performance and fuel efficiency. Aero Accessories, Air Power Inc., and Sky Dynamics cater to specialized MRO and retrofit needs, supporting both OEM and aftermarket channels. Collectively, these players drive competition, reliability, and technological progress in ignition system design worldwide.

Download Free sample to learn more about this report.

AIRCRAFT IGNITION SYSTEM MARKET TRENDS

Trend of Integrating Digital and Solid-State Ignition Technologies is Gaining Traction

The market is witnessing a substantial shift toward digital, solid-state, and electronically controlled ignition systems that enhance engine reliability, reduce maintenance, and improve fuel efficiency. Traditional magneto-based systems are being replaced with electronic ignition solutions that deliver consistent spark performance across variable altitudes and temperatures. Manufacturers are integrating FADEC (Full Authority Digital Engine Control) interfaces and diagnostic sensors, enabling real-time performance monitoring and predictive maintenance. The push for lightweight components and additive manufacturing methods is also reshaping production, reducing cost, and improving durability. Furthermore, hybrid-electric and sustainable aviation programs are influencing design priorities, emphasizing ignition systems optimized for fuel flexibility and combustion stability. Increasing aircraft deliveries, fleet modernization, and extended engine service life are all accelerating the shift toward smarter, high-efficiency ignition solutions. This trend reflects the industry’s broader move toward digitalization, sustainability, and lifecycle optimization across both commercial and general aviation sectors.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Aircraft Production and Engine Overhaul Rates to Boost Market Growth

The aircraft ignition system market growth is primarily driven by rising aircraft deliveries and engine overhaul cycles across commercial, business, and general aviation sectors. OEM production ramp-ups by Airbus and Boeing, combined with expanding fleets from Embraer and regional aircraft manufacturers, directly boost ignition system installations. Simultaneously, a surge in engine shop visits, notably for CFM LEAP and Pratt & Whitney GTF engines, has intensified aftermarket demand for igniters, exciters, and leads. Strong passenger demand, sustained flight hours, and robust general aviation activity in the U.S. also reinforce continuous component replacement. On the supply side, manufacturers are developing durable, high-energy ignition systems that reduce misfire risks and improve combustion efficiency, aligning with the aviation industry’s fuel-burn reduction goals. Furthermore, defense aviation programs and the rise of UAVs utilizing small turbine engines add to the growth momentum. Together, these factors create a stable demand environment, making ignition systems a vital enabler of aircraft operational reliability.

MARKET RESTRAINTS

Regulatory Complexity and High Certification Costs May Hamper Market Growth

Despite positive momentum, the market faces restraints tied to stringent certification processes, high R&D costs, and long qualification cycles for aerospace components. FAA and EASA regulations demand rigorous testing for ignition system reliability, EMI compatibility, and environmental compliance, extending product development timelines. Smaller firms face barriers in obtaining approvals for new designs or retrofits, limiting innovation speed. Additionally, volatile raw material costs, especially for high-temperature alloys and titanium used in igniters, increase production expenses. Supply chain disruptions particularly during global crises impact timely component delivery and aftermarket availability. Aircraft OEM delays, such as reduced output from Boeing in 2023–2024, also ripple into ignition system demand fluctuations. Moreover, the slow pace of electric and hybrid aircraft certification reduces near-term adoption of advanced ignition solutions. Together, these factors restrict market agility and profitability, especially for smaller suppliers competing against large Tier-1 aerospace groups with established compliance infrastructure.

MARKET OPPORTUNITIES

Expanding Fleet Modernization and Aftermarket Potential Accentuates Market Opportunity

A key opportunity in the aircraft ignition system market lies in fleet modernization and the growing aftermarket sector. With commercial air traffic exceeding pre-pandemic levels, operators are upgrading older engines with digital ignition systems to improve efficiency and reduce emissions. Moreover, emerging markets in Asia Pacific, the Middle East, and Latin America are expanding their fleets, driving new OEM installations. The rise of MRO hubs in India, Singapore, and the UAE further amplifies service demand. In general aviation, the retrofit trend toward electronic ignition upgrades, led by FAA-certified systems from Electroair and SureFly, offers sustained revenue growth. As sustainability targets tighten and next-generation engines enter service, ignition systems designed for alternative fuels, hybrid powertrains, and optimized combustion will unlock new technological and commercial opportunities worldwide.

MARKET CHALLENGES

Transition to Hybrid-Electric and Alternative Propulsion Systems are Major Obstacles in the Market

A major challenge for the aircraft ignition system market growth is adapting to emerging propulsion technologies, including hybrid-electric, hydrogen, and fully electric aircraft, which require minimal or no traditional ignition components. As sustainable aviation gains traction, engine OEMs are redesigning combustion architectures, thereby reducing long term demand for conventional ignition hardware. The growing use of solid-state ignition substitutes and plasma-assisted combustion introduces technical uncertainty for existing suppliers. At the same time, maintaining compatibility with biofuels, synthetic fuels, and higher-pressure combustors requires redesigning ignition parameters and materials. Additionally, global competition from low-cost suppliers, intellectual property constraints, and integration of digital health monitoring systems pose significant technological and strategic hurdles. The challenge lies in balancing innovation investment with market readiness, developing systems that remain relevant across both conventional and alternative propulsion platforms. Successfully addressing these shifts will determine which players sustain leadership in the evolving aerospace power ecosystem.

SEGMENTATION ANALYSIS

By Aircraft Type

Rising Flight Activity Sustains Demand for Fixed-Wing Aircraft Ignition Systems

By aircraft type, the market is segmented into fixed-wing aircraft, rotary-wing aircraft, and Unmanned Aerial Vehicle (UAV).

In 2025, the fixed-wing aircraft segment is projected to captured the largest market with a share of 75.36% in 2026, as it dominates global fleet counts and engine deliveries, sustaining high ignition system demand. Growing airline traffic, active general aviation use, and ongoing replacement of ignition components in commercial and business jets drive consistent sales. Fleet modernization programs and higher engine utilization rates further reinforce aftermarket demand for reliable ignition solutions.

The unmanned aerial vehicle (UAV) segment is expected to grow at a CAGR of 7.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Engine Type

Expanding Commercial Fleets Boost Turbofan Engine Ignition Requirements

The engine type segment is classified into turboprop engine, turbofan engine, turbojet engine, and piston engine.

In 2025, the turbofan engine segment is anticipated to dominate with a share of 46.04% in 2026, by capturing the largest market share. Turbofan engines power the majority of narrow-body and wide-body aircraft, making them the largest consumers of ignition components. Strong passenger growth, airline fleet expansion, and increased long-haul operations elevate igniter and exciter usage. Rising shop-visit volumes and durability upgrades in LEAP and GTF engines amplify aftermarket ignition demand globally.

The turboprop engine segment is expected to grow at a CAGR of 4.7% over the forecast period.

By System Type

Shift Toward Efficient, Reliable Systems Drives Electric Ignition Adoption

By system type, the market is bifurcated into electric ignition and magneto ignition.

The electric ignition segment held the leading position in 2025 and will sustain its position in 2026 with a share of 66.36% in 2026. Electric ignition systems are replacing legacy magneto types due to superior reliability, reduced maintenance, and compatibility with digital engine controls. As turbine engines dominate new aircraft production, electric ignition demand rises. OEMs favor these systems for performance optimization, while MRO operators benefit from improved lifespan and simplified service procedures.

The magneto ignition segment is expected to grow at a CAGR of 4.8% during the forecast period.

By Component

Frequent Maintenance Cycles Sustain High Demand for Spark Plugs

By component, the market is classified into ignition leads, igniters, spark plugs, exciters, and others.

In 2025, the spark plugs segment is projected to attained the largest market with a share of 33.78% in 2026. Spark plugs remain essential consumables in piston-engine aircraft, creating steady aftermarket demand. General aviation and flight training sectors drive frequent replacement needs, typically every 400–500 flight hours. Despite low unit costs, high replacement frequencies, and vast active piston fleets, spark plug sales remain robust across North America and Europe.

The igniters segment is expected to grow at a CAGR of 5.9% over the forecast period.

AIRCRAFT IGNITION SYSTEM REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Aircraft Ignition System Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 174.1 million, contributing 37.70% to global market revenue, and is projected to grow to USD 183.2 million in 2026. The region’s strong growth is driven by a vast general aviation and business jet fleet, high MRO intensity, and consistent replacement of spark plugs, magnetos, and turbine igniters. The U.S. market dominates with large installed fleets and strong flight activity recovery, sustaining steady ignition component sales across piston and turbine segments.

In 2026, the U.S. market is estimated to reach USD 150.7 million as it is the largest single market for aircraft ignition systems, supported by extensive general aviation and defense fleets, robust commercial operations, and mature MRO infrastructure. The country’s demand is underpinned by frequent component replacement cycles, strong aftermarket activity, and ongoing modernization of ignition technologies across both turbine and piston engine platforms.

Europe

Europe’s projected growth rate for the forecast period is 5.0%, while sustaining a market size of USD 128 million in 2025, representing 27.71% of the global industry, and is expected to reach USD 134.4 million in 2026. The region’s robust demand reflects sustained airline utilization, robust turbofan engine operations, and a renewed focus on general aviation activity in Germany, France, and the U.K. Regional MRO hubs, such as Lufthansa Technik and Safran, maintain stable repair volumes. Europe’s moderate growth is steady as green aviation projects gradually modernize ignition technologies and fleet efficiency. The UK aircraft ignition system market is valued at USD 24.1 million by 2026, while the Germany aircraft ignition system market is valued at USD 25.5 million by 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 138.2 million in 2025, capturing 29.92% of the global market share, and is projected to reach USD 146.2 million in 2026, as product demand is accelerated by the expansion of commercial fleets in China and India, strong domestic flight recovery, and new turbine-powered aircraft deliveries. Local MRO capacity in Singapore, Malaysia, and India is scaling rapidly, supporting ignition component replacement and overhaul cycles as the region leads global passenger and fleet growth. The Japan aircraft ignition system market is anticipated to valued at USD 15.7 million by 2026, the China aircraft ignition system market is anticipated to valued at USD 52.3 million by 2026, and the India aircraft ignition system market is valued at USD 18.6 million by 2026.

Rest of the world

The Rest of the World market was valued at USD 21.6 million in 2025, capturing 4.67% of global revenue, and is estimated to reach USD 22.2 million in 2026. The rest of the world market benefits from expanding fleets in the Middle East, as well as emerging growth in Latin America and Africa. Increasing aircraft deliveries, rising air travel, and investment in regional MRO centers boost ignition system demand, especially for turbofan engines operating in high-temperature, high-cycle environments typical of these regions.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Innovation, Certification, and Aftermarket Reach Drive Leadership among Key Players

Key players dominate the aircraft ignition system market share by combining certified reliability, innovation, and global service coverage. Champion Aerospace, Tempest Aero Group, and Hartzell Engine Technologies lead with FAA-approved ignition components and strong OEM partnerships. TransDigm Group excels with integrated product portfolios and global distribution networks. Emerging firms such as Electroair, SureFly, and G3i gain traction through digital ignition conversion kits that improve fuel efficiency and reduce maintenance intervals. Meanwhile, Aero Accessories, Air Power Inc., and Sky Dynamics strengthen aftermarket support with repair, overhaul, and replacement solutions, collectively ensuring product availability, compliance, and technological advancements across aviation sector.

LIST OF KEY AIRCRAFT IGNITION SYSTEM COMPANIES PROFILED

- Aero Accessories (U.S.)

- Air Power Inc. (U.S.)

- Champion Aerospace (U.S.)

- Electroair (U.S.)

- G3i (General Aviation Ignition Systems) (U.S.)

- Hartzell Engine Technologies (U.S.)

- Sky Dynamics (U.S.)

- SureFly (U.S.)

- Tempest Aero Group (U.S.)

- TransDigm Group (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025 – Textron Aviation announced that its flagship training aircraft, the Cessna Skyhawk, is now equipped with a Dual Electronic Ignition System (dual EIS). This upgrade enhances the aircraft’s maintenance efficiency, performance, and overall operational reliability. The advanced dual Lycoming electronic ignition system is now a standard feature on all newly manufactured Cessna Skyhawk models.

- July 2025 – Piper Aircraft, Inc. introduced the new Piper Seminole DX, a diesel-powered variant of the PA-44 Seminole. The aircraft is equipped with DeltaHawk’s FAA-certified DHK4A180 engine, a 180-horsepower heavy-fuel, compression ignition powerplant. The Seminole DX is the result of a successful partnership between Piper Aircraft and DeltaHawk, first announced in early 2024, marking a significant step toward more efficient and sustainable training aircraft solutions.

- February 2025 – At the Aero India trade show in Bengaluru, Safran Aircraft Engines, France’s leading aircraft engine manufacturer, signed a contract with Hindustan Aeronautics Limited (HAL), India’s premier aerospace company. Under the agreement, HAL will produce turbine forged components for Safran’s LEAP engines, strengthening the industrial partnership between the two companies and supporting the growing demand for next-generation aircraft propulsion systems.

- January 2024 – Swiss startup Sirius Aviation AG unveiled the Sirius Jet, the world’s first hydrogen-powered vertical take-off and landing (VTOL) aircraft. Developed in collaboration with BMW’s Designworks and the Sauber Group, the Sirius Jet represents a major breakthrough in sustainable aviation. The aircraft combines cutting-edge design, safety, and eco-friendly technology, underscoring Sirius Aviation’s commitment to innovation and the advancement of zero-emission flight.

- May 2023 – PBS has launched a pyrotechnic ignition variant of its PBS TJ150 turbine engine, which is an advancement over the TJ100 model. This updated version incorporates a pyrotechnic ignition start-up mechanism that enables in-flight starts at speeds reaching up to 0.8 Mach. In contrast to conventional spark plug ignition systems in gas turbine combustors, which face difficulties with fuel-lean mixtures, turbulent environments, and high-altitude relights, the innovative pyrotechnic system addresses these issues by utilizing specialized pyro materials to ensure dependable ignition under challenging conditions.

REPORT COVERAGE

The aircraft ignition system market research report delivers a comprehensive analysis, outlining the leading companies, product segments, and primary applications within the sector. It also emphasizes key market trends and significant advancements shaping the industry. Furthermore, the report examines various factors that have driven the market’s expansion in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.11% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Aircraft Type · Fixed-Wing Aircraft · Rotary-Wing Aircraft · Unmanned Aerial Vehicle (UAV) |

|

By Engine Type · Turboprop Engine · Turbofan Engine · Turbojet Engine · Piston Engine |

|

|

By System Type · Electric Ignition · Magneto Ignition |

|

|

By Component · Ignition Leads · Igniters · Spark Plugs · Exciters · Others |

|

|

By Geography · North America (By Aircraft Type, Engine Type, System Type and Component) o U.S. (By Aircraft Type) o Canada (By Aircraft Type) · Europe (By Aircraft Type, Engine Type, System Type and Component) o U.K. (By Aircraft Type) o Germany (By Aircraft Type) o France (By Aircraft Type) o Russia (By Aircraft Type) o Rest of Europe (By Aircraft Type) · Asia Pacific (By Aircraft Type, Engine Type, System Type and Component) o China (By Aircraft Type) o Japan (By Aircraft Type) o India (By Aircraft Type) o Rest of Asia Pacific (By Aircraft Type) · Rest of the World (By Aircraft Type, Engine Type, System Type and Component) o Middle East & Africa (By Aircraft Type) o Latin America (By Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 486.00 million in 2026 and is estimated to reach USD 724.20 million by 2034.

The market is growing at a CAGR of 5.11% during the projection period.

Spark plugs is the leading component of the global market.

The fixed-wing aircraft segment leads in the global market.

Aero Accessories (U.S.), Air Power Inc. (U.S.), Champion Aerospace (U.S.), Electroair (U.S.), G3i (General Aviation Ignition Systems) (U.S.) are some of the leading copanies.

North America is projected to attain the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us