Airport Runway Safety Systems Market Size, Share & Industry Analysis, By System Type (Surveillance & Conflict Detection Systems, Incursion Prevention & Alerting, Surface Condition Monitoring, FOD Detection & Automated Runway Inspection, Aircraft Arresting & Mitigation), By Application (Incursion Prevention, Excursion Prevention, Collision Avoidance), By Technology (Radar & Multilateration, ADS-B & Vehicle Tracking, AI), By Installation Type (Retrofit, New Installation, Lifecycle Upgrade), By End User (Airport Operators, Aviation Agencies, Defense Airfield), & Regional Forecast, 2026-2034

Airport Runway Safety Systems Market Size and Future Outlook

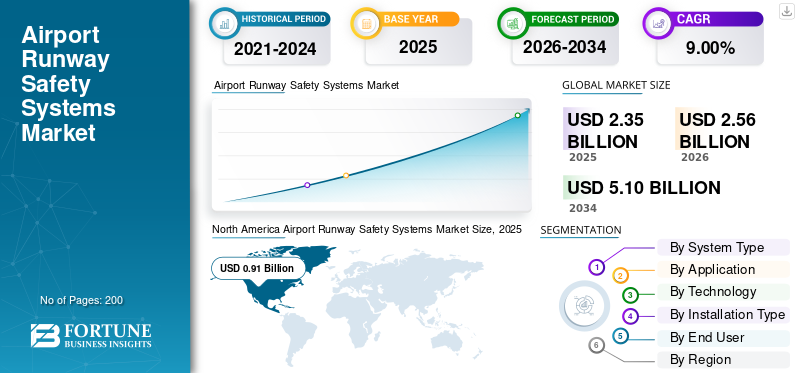

The global airport runway safety systems market size was valued at USD 2.35 billion in 2025. The market is projected to grow from USD 2.56 billion in 2026 to USD 5.10 billion by 2034, exhibiting a CAGR of 9.00% during the forecast period.

The airport runway safety systems are integrated technologies designed to prevent runway incursions, excursions, and collisions at airports. Key components include Runway Status Lights (RWSL) for visual alerts to hold short or takeoff and Airport Surface Detection Equipment Model X (ASDE-X) for radar-based surveillance fusing data from multilateration and ADS-B. Other components include Engineered Material Arresting Systems (EMAS) using crushable beds to stop overruns and Runway Safety Areas (RSAs) as graded zones beyond runways. Growth stems from surging air traffic, strict ICAO/FAA regulations, and innovations in surveillance and AI monitoring.

Major players in the market include Honeywell International Inc., Thales Group, Saab AB, Indra Sistemas, ADB SAFEGATE, Varec, and Navtech Radar. These players provide integrated surveillance radars, runway incursion prevention systems, or surface movement guidance technologies for commercial and military airports.

Download Free sample to learn more about this report.

AIRPORT RUNWAY SAFETY SYSTEMS MARKET TRENDS

Integration of AI Driven Predictive Maintenance and Analytics is a Market Trend

The integration of artificial intelligence driven predictive maintenance and analytics marks a pivotal trend in airport runway safety systems, enabling proactive risk mitigation. FAA's Aviation Risk Identification and Assessment (ARIA) tool fuses surveillance data to predict collision risks on runways via vertical, lateral, and speed analysis, supporting data-driven decisions at equipped airports. In March 2025, in order to identify runway incursions, the Federal Aviation Administration announced on Wednesday that it will install improved safety systems at 74 airports by the end of 2026. The Runway Incursion Device, a memory assist for air traffic controllers that shows when a runway is occupied, is being installed by the FAA. ICAO-endorsed systems leverage video analytics for FOD detection and surface defect prediction, cutting incidents by up to 30%. These advancements shift from reactive to predictive safety amid rising traffic.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Air Traffic is Anticipated to Drive Market Growth

Rising air traffic drives airport runway safety systems market growth by intensifying congestion on runways and taxiways, where an increasing number of aircraft sharing limited space multiplies collision risks exponentially rather than linear volume. Overstretched infrastructure amplifies surface condition issues such as contamination, turning survivable overruns into serious events amid rapid operational build-up. Furthermore, IATA emphasizes that expanding demand strains human oversight, miscommunications, and situational awareness, fueling runway excursions and loss-of-separation incidents on shared surfaces.

MARKET RESTRAINTS

High Upfront Costs for Advanced Systems is a Market Restraint

High upfront costs for advanced runway safety systems such as radar surveillance and arresting beds restrain market growth, particularly burdening smaller regional airports with tight budgets. Installation demands extensive infrastructure retrofits, power upgrades, and integration with legacy equipment, stretching multi-year funding cycles. Ongoing expenses for maintenance, cybersecurity, and staff training further deter adoption, as even falling hardware prices leave substantial program costs.

MARKET OPPORTUNITIES

Airport Modernization to Create New Market Opportunities

Airport modernization creates new market opportunities for runway safety systems amid global infrastructure booms. Emerging hubs such as India's UDAN-linked expansions and China's mega-airports demand embedded safety tech during greenfield builds. In June 2025, Saab was given a major contract by the Federal Aviation Administration (FAA) to install its Aerobahn Runway and Surface Safety service at 26 more U.S. airports. This award advances efforts to improve runway safety through cutting-edge, technologically advanced technologies, and is part of the FAA's Surface Awareness Initiative (SAI) Block 3 deployment.

MARKET CHALLENGES

Environmental Compliance and Construction Disruptions Present a Major Market Challenge

Environmental compliance and construction disruptions challenge market growth by imposing lengthy permitting delays for wetland mitigation, erosion control, and stormwater management during RSA expansions or EMAS installations. Construction phases force runway closures often nighttime or seasonal disrupting flight schedules, rerouting traffic, and reducing airport throughput. These halt revenues while escalating costs for phased work, equipment relocation, and passenger accommodations. Further, heightened noise complaints trigger community opposition and legal halts, while supply chain issues for eco-materials prolong timelines.

Segmentation Analysis

By System Type

Real-Time Movement Fusion to Drive Runway Surveillance & Conflict Detection Systems Segment Growth

Based on the system type, the market is segmented into runway surveillance & conflict detection systems, runway incursion prevention & alerting systems, runway surface condition monitoring systems, FOD detection & automated runway inspection systems, aircraft arresting & overrun mitigation systems, and others.

The runway surveillance & conflict detection systems segment is anticipated to account for the largest market share. Segmental growth in the market is driven by real-time movement fusion, as multilateration-radar integration provides controllers with unified 3D surface views that enable predictive conflict resolution before runway violations occur during peak layered operations.

The runway incursion prevention & alerting systems segment is anticipated to rise with a high CAGR of 9.65% over the forecast period.

By Application

Escalating Surface Congestion Alerts to Propel Runway Incursion Prevention Segment Growth

Based on application, the market is segmented into runway incursion prevention, runway excursion prevention, surface collision avoidance, FOD detection & runway inspection, and others.

In 2025, the runway incursion prevention segment dominated the global airport runway safety systems market share. The segmental growth is driven by escalating surface congestion alerts in runway incursion prevention applications, as layered RWSL lights and SAI fusion automate real-time occupancy warnings to pilots and controllers. Further, minimizing human error amid rising taxiway conflicts and regulatory mandates for high-traffic environments.

The FOD detection & runway inspection segment is projected to grow at a high CAGR of 9.54% over the forecast period.

By Technology

GNSS-Independent Precision Tracking to Boost Radar & Multilateration-Based Systems Segment Growth

Based on the technology, the market is segmented into radar & multilateration-based systems, ADS-B & vehicle tracking systems, AI / computer vision-based systems, smart airfield lighting systems, and others.

The radar & multilateration-based systems segment is anticipated to witness a dominating market share over the forecast period. The segmental growth is driven by GNSS-independent precision tracking in radar & multilateration-based systems, as they fuse transponder signals from multiple ground receivers to deliver sub-meter accuracy in radar-shadowed areas. Further, ensuring reliable surface surveillance without expensive infrastructure while providing ADS-B redundancy essential for incursion alerts in dense operations.

The AI / computer vision-based systems segment is projected to grow at a high CAGR of 9.65% over the forecast period.

By Installation Type

Non-Disruptive Upgrades to Accelerate Retrofit/Modernization Segment Growth

Based on installation type, the market is segmented into retrofit / modernization, new installation, replacement / lifecycle upgrade, and others.

The retrofit / modernization segment dominated the market share. The segmental growth in the market is owing to non-disruptive upgrades in retrofit/modernization installations, as modular sensor overlays and software alerts enhance legacy infrastructure without full closures. Further, allowing busy airports to achieve FAA/ICAO compliance through phased integration that preserves revenue flows.

In addition, the new installation segment is projected to grow at a high CAGR of 9.49% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Regulatory Accountability to Fuel Airport Operators/Authorities Segment Growth

Based on end user, the market is segmented into airport operators / airport authorities, air navigation service providers / ATC authorities, government aviation agencies, defense airfield operators, and others.

The airport operators / airport authorities segment dominated the market share. The segmental growth in the market is driven by regulatory accountability for airport operators/authorities, as end-to-end platforms enable centralized RST audits, GRF reporting, and incident tracking. These capabilities help demonstrate due diligence, secure grants, and mitigate liability amid intensifying scrutiny over surface safety performance.

In addition, the air navigation service providers / ATC authorities segment is projected to grow at a CAGR of 9.17% during the forecast period.

Airport Runway Safety Systems Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America held the dominant share in 2024, valuing at USD 0.84 billion, and also maintained the leading share in 2025, with USD 0.91 billion. The region’s dominance is due to FAA's stringent mandates requiring surface surveillance at high-traffic hubs, where dense operations amplify incursion risks.

North America Airport Runway Safety Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

U.S. Airport Runway Safety Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.62 billion in 2026. Further, accounting for roughly 9.24% of CAGR over the forecast period. The U.S. leads adoption driven by FAA's focus on SAI platforms and runway incursion devices at major airports, tackling near-miss surges from complex taxiing. Growth stems from radar-multilateration upgrades providing controllers fused surface maps, enabling proactive conflict resolution during peak hours.

Europe

Europe is projected to record a steady growth rate of 9.04% during the forecast period, the second-highest among all regions, and is estimated to reach a valuation of USD 0.62 billion by 2026. Europe's growth arises from EASA's harmonized aerodrome standards mandating RESA expansions and incursion prevention across diverse facilities. Regional hubs prioritize low-visibility surface guidance and standardized phraseology training, addressing variable weather impacts on excursions.

U.K. Airport Runway Safety Systems Market

The U.K. market in 2026 is estimated at around USD 0.20 billion, representing roughly 9.50% CAGR during the forecast period. The market expansion is propelled by CAA's runway safety team audits targeting regional aerodromes, where smaller fields face heightened incursion risks from mixed operations. Growth factors include enhanced stop bar enforcement and LED runway lighting upgrades, improving low-vis procedures and pilot situational awareness.

Germany Airport Runway Safety Systems Market

Germany’s market is projected to reach approximately USD 0.17 billion in 2026. Germany drives growth through EASA-aligned RESA compliance during major hub expansions, focusing on advanced friction testing to mitigate wet runway excursions.

Asia Pacific

Asia Pacific is estimated to reach USD 0.57 billion in 2026, making it the third-largest market region, and the fastest-growing during the forecast period. Asia Pacific is witnessing explosive growth from surging mega-hub traffic overwhelming existing surveillance, spurring international technology collaborations for incursion prevention. Regional authorities prioritize radar fusion and RWSL deployment to manage intersection operations and rapid LCC expansion.

Japan Airport Runway Safety Systems Market

The Japan market in 2026 is estimated at around USD 0.10 billion, accounting for roughly 9.51% of CAGR during the forecast period. Japan's growth follows enhanced runway protection protocols post-major incidents, emphasizing ANSP training and international best practice adoption. Focus shifts to precision multilateration for low-vis Haneda-type scenarios, integrating predictive alerts with dense urban airspace constraints.

China Airport Runway Safety Systems Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.18 billion. China's market surges via integrated surveillance during massive greenfield airport constructions, addressing capacity-safety tensions at world's busiest hubs. Growth factors include centralized multilateration platforms tracking dense ground movements, supporting AI-driven conflict prediction amid explosive domestic travel.

India Airport Runway Safety Systems Market

The India market in 2026 is estimated at around USD 0.16 billion. India accelerates growth through regional connectivity initiatives deploying detection technologies at secondary airports handling LCC booms. Runway incursion prevention gains priority amid mixed military-civil ops and monsoon challenges.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America regions. Latin America builds resilient master planning with multilateration upgrades, Middle East & Africa modernizes CNS infrastructure via AI surveillance. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.23 billion and USD 0.15 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Integrated Runway Safety Solutions Fuel Market Expansion

The airport runway safety systems market remains moderately consolidated, with established aerospace specialists such as Honeywell, Thales Group, Saab AB, Indra Sistemas, and ADB SAFEGATE commanding major shares. These companies maintain their positions through certified surveillance radars, multilateration networks, and integrated surface guidance solutions tailored for high-traffic commercial and military aerodromes.

As air traffic densities rise, these firms focus on improving radar fusion, predictive conflict detection, and AI-enhanced warning to fulfill increasing FAA/EASA/ICAO safety standards. Rapid market penetration is fueled by strategic partnerships. For example, Saab integrates its Aerobahn software into the FAA's 74-airport RID rollout, Honeywell teams with major U.S. airport authorities on SAI platform deployments, and Thales partners with European ANSPs for seamless multilateration upgrades. Further, Indra provides alerting systems to Asia Pacific hubs during capacity expansions and ADB SAFEGATE works with international operators on RWSL/EMAS retrofits that combine arrestor bed technologies.

LIST OF KEY AIRPORT RUNWAY SAFETY SYSTEMS COMPANIES PROFILED

- Honeywell International Inc. (U.S.)

- Thales Group (France)

- Saab AB (Sweden)

- Indra Sistemas (Spain)

- ADB SAFEGATE (Belgium)

- RTX Corporation (U.S.)

- Navtech Radar (U.K.)

- Terma A/S (Denmark)

- Frequentis AG (Austria)

- L3Harris Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: The Federal Aviation Administration (FAA) has awarded Rohde & Schwarz a contract worth up to USD 4.9 billion. It is to replace the analog communication infrastructure in airports and air traffic control facilities with the field-proven CERTIUM Voice Communication System.

- January 2026: As part of H.R. 7148, the Consolidated Appropriations Act of 2026, Congressman Troy E. Nehls announced the approval of USD 2 million in government funds for the runway upgrade project at Sugar Land Regional Airport. The money is intended to solve Runway 17–35 safety issues.

- January 2026: Delhi International Airport Ltd. (DIAL) proposed a complete rehabilitation program for Runway 11R/29L, also known as the third runway of Indira Gandhi International Airport. Subject to the Directorate General of Civil Aviation's (DGCA) permission, the rehabilitation project is slated to start on February 16, 2026, and the runway is anticipated to be recommissioned in early July.

- December 2025: To lessen the effect of fog on flight operations this winter, Delhi Airport has included AI technology, sophisticated predictive analytics, and improved runway capabilities. These technological advancements should contribute to safer, more effective aircraft operations and less disturbance under low-visibility conditions (LVPs).

- July 2024: Indra announced that AeroBOSS, its SAI (Surface Awareness Initiative) product, has been authorized by the Federal Aviation Administration (FAA). In order to successfully prevent mishaps and provide security for aircraft, passengers, and airport personnel, this technology enables air traffic controllers to have a comprehensive picture of the situation on the apron and runways. This enhanced visibility helps controllers monitor aircraft movements more effectively and improve overall airport safety.

REPORT COVERAGE

The global airport runway safety systems industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, porter’s five forces analysis, company profiles, and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key aviation industry developments and prevalence by key regions. The global market report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.00% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By System Type, Application, Technology, Installation Type, End User and Region |

| By System Type |

|

| By Application |

|

| By Technology |

|

| By Installation Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.35 billion in 2025 and is projected to reach USD 5.10 billion by 2034.

In 2025, the market value stood at USD 0.91 billion.

The market is expected to exhibit a CAGR of 9.00% during the forecast period.

By system type, the runway surveillance & conflict detection systems segment is expected to dominate the market.

The rising air traffic is anticipated to drive market growth.

Honeywell International Inc. (U.S.), Thales Group (France), Saab AB (Sweden), Indra Sistemas (Spain), ADB SAFEGATE (Belgium), and RTX Corporation (U.S.) are a few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us