Ammonia Fuel Market Size, Share & Industry Analysis, By Fuel Type (Blue Ammonia, Grey Ammonia, and Green Ammonia), By Application (Maritime Transport, Power Generation, Industrial Application, and Others), By End User (Shipping & Maritime, Power & Utilities, Oil & Gas, Heavy Industries, and Others), Regional Forecast, 2026-2034

Ammonia Fuel Market Size and Future Outlook

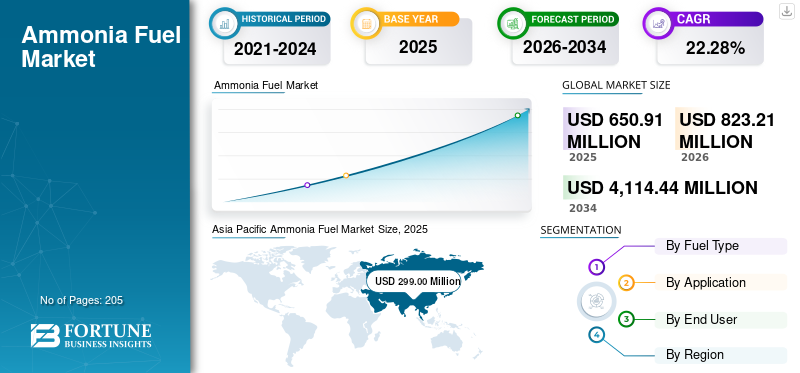

The global ammonia fuel market size was valued at USD 650.91 million in 2025. The market is projected to grow from USD 823.21 million in 2026 to USD 4,114.44 million by 2034, exhibiting a CAGR of 22.28% during the forecast period. Asia Pacific dominated the ammonia fuel market with a market share of 45.93% in 2025.

Ammonia fuel is emerging as a viable low-carbon energy carrier, particularly for hard-to-abate sectors such as shipping and power generation. Unlike conventional fuels, ammonia contains no carbon, enabling zero CO₂ emissions at the point of combustion, and offers advantages such as easier storage and transport compared to hydrogen. In 2023, the International Energy Agency (IEA) stated that ammonia could account for around 44-45% of global shipping fuel demand by 2050, positioning it as a leading alternative marine fuel.

The primary driver for product adoption is the tightening of global decarbonization regulations, particularly in maritime transport, set by the International Maritime Organization (IMO) targets for net-zero emissions by 2050. Ammonia’s ability to leverage existing global production capacity and distribution infrastructure further accelerates its adoption, reducing transition costs compared to hydrogen. Moreover, studies indicate that ammonia-based solutions could contribute significantly to low-carbon power generation, with hydrogen and ammonia co-firing expected to generate over 1,100 TWh of electricity globally by 2050, as per the IEA.

- For instance, in March 2025, JERA Co., Inc. advanced Japan’s ammonia fuel strategy by announcing expanded large-scale ammonia co-firing trials at the Hekinan thermal power plant. The project aims to increase ammonia blending ratios to reduce coal dependency and cut CO₂ emissions significantly. This initiative aligns with Japan’s national target of 3 million tons of fuel ammonia usage by 2030, reinforcing ammonia’s role in decarbonizing the power sector and accelerating commercial-scale adoption.

Some of the leading companies operating in the industry include Yara International ASA, OCI N.V., Air Liquide S.A., and others. Yara International ASA is one of the leading ammonia producers in the ammonia fuel ecosystem, actively advancing both blue and green ammonia production for energy applications. The company is involved in developing low-carbon ammonia projects and maritime fuel solutions, including partnerships for ammonia-powered shipping.

Download Free sample to learn more about this report.

Ammonia Fuel Market Key Takeaways

- 2025 Market Size: USD 650.91 million

- 2026 Market Size: USD 823.21 million

- 2034 Forecast Market Size: USD 4,114.44 million

- CAGR: 22.28% from 2026–2034

- Asia Pacific dominated the market with a 45.93% share in 2025.

- Blue ammonia segment accounted for a 51.27% share in 2025.

- Maritime transport segment accounted for a 56.08% share in 2025.

North America

The market reached USD 97.43 million in 2025 and is projected to reach USD 121.60 million by 2026.

Asia Pacific

The market reached USD 299.00 million in 2025, driven by strong demand from Japan and South Korea and expanding production capacity.

Europe

The market reached USD 155.64 million in 2025 and is expected to grow at a 21.95% CAGR during the forecast period.

U.S.

The market reached USD 74.98 million in 2025, supported by expanding blue ammonia projects and carbon capture initiatives.

Japan

The market reached USD 94.66 million in 2025, driven by increasing adoption of ammonia in power generation and shipping.

Read More

AMMONIA FUEL MARKET TRENDS

Development of Dedicated Bunkering Infrastructure at Major Ports is the Key Market Trend

A key trend shaping the market is the rapid development of dedicated bunkering infrastructure at major global ports. Ports such as Rotterdam, Singapore, and Fujairah are actively planning ammonia storage and refueling facilities to support future marine fuel demand. According to the Global Maritime Forum (2024), over 20 ports globally are in various stages of ammonia bunkering readiness assessment, indicating a shift from pilot projects to ecosystem development. This infrastructure-first approach is critical, as fuel availability at ports will directly determine the pace of adoption in shipping. Additionally, port-led consortia involving energy companies, shipping firms, and governments are accelerating standardization and safety protocols, thereby reducing commercialization barriers.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Strategic Investments in Export-Oriented Ammonia Supply Chains to Drive Market Growth

A major driver accelerating the ammonia fuel market is the rise of large-scale, export-oriented ammonia supply chains linking production hubs with demand centers. Countries such as Saudi Arabia, Australia, and Chile are investing heavily in integrated projects combining renewable energy, hydrogen production, and ammonia synthesis specifically for export to regions such as Japan, South Korea, and Europe.

According to IEA, in 2024, more than 25 Million Tons Per Annum (MTPA) of low-carbon ammonia export capacity were announced globally, with a significant portion targeting energy applications. This shift is transforming ammonia from a localized industrial chemical into a globally traded clean fuel. Long-term offtake agreements between producers and utilities or shipping companies are also reducing investment risks and accelerating project execution.

MARKET RESTRAINTS

High Cost and Energy Efficiency Losses Across the Value Chain to Hamper Market Demand

A key restraint in the ammonia fuel market is the high overall cost structure combined with energy efficiency losses across the value chain, from production to end-use. Green ammonia production involves multiple conversion steps: electricity to hydrogen (electrolysis), hydrogen to ammonia synthesis, and, in some cases, reconversion or direct combustion, each introducing efficiency losses.

According to the IEA, the overall energy efficiency of ammonia as a fuel pathway can drop below 30–40%, significantly lower than direct electrification alternatives. Additionally, green ammonia production costs remain high, often exceeding USD 700-1,000 per ton depending on renewable energy costs and electrolyzer efficiency. These cost challenges are further amplified by the need for specialized storage, handling, and engine modifications, increasing capital expenditure for end users.

MARKET OPPORTUNITIES

Integration of Ammonia with Hybrid Fuel Systems and Cracking Technologies to Create Market Opportunities

Ammonia fuel presents significant opportunities through the development of hybrid fuel systems and ammonia cracking technologies, enabling flexible energy use across multiple applications. Ammonia can be converted back into hydrogen through cracking, allowing it to serve as a transportable hydrogen carrier for fuel cells and distributed energy systems.

According to the International Renewable Energy Agency (IRENA), advancements in cracking technologies are targeting efficiencies above 70–75%, making ammonia a more viable medium for hydrogen delivery in remote and import-dependent regions. Additionally, hybrid systems combining ammonia with conventional fuels or hydrogen are being tested to improve combustion stability and reduce NOx emissions. This flexibility expands ammonia’s applicability beyond direct combustion, particularly in sectors where pure ammonia use faces technical limitations.

MARKET CHALLENGES

Safety, Toxicity, and Regulatory Compliance Constraints to Deter Product Demand

A critical challenge in the ammonia fuel market is managing safety risks, toxicity concerns, and evolving regulatory frameworks associated with its use. Ammonia is a hazardous substance with strict handling requirements due to its toxicity and corrosive nature, necessitating specialized storage systems, leak detection mechanisms, and crew training, particularly in maritime applications.

According to the IMO, comprehensive safety guidelines for ammonia as a marine fuel are still under development, creating uncertainty for shipowners and operators. Additionally, regulatory fragmentation across regions regarding transport, storage, and emissions (especially NOx) adds complexity to project deployment.

Segmentation Analysis

By Fuel Type

Blue Ammonia Segment Dominated Due to Lower Transition Costs

Based on fuel type, the market is classified into blue ammonia, grey ammonia, and green ammonia.

In 2025, the blue ammonia segment dominated the industry, accounting for 51.27% share of the global market. The segment dominates due to its ability to leverage existing natural gas-based production infrastructure combined with carbon capture technologies, enabling relatively faster and cost-effective scaling compared to green ammonia. It offers a practical transition pathway by reducing emissions while maintaining supply reliability. Additionally, major projects in regions such as the U.S. and the Middle East support its near-term dominance.

The green ammonia segment is experiencing the highest growth and is expected to grow at a CAGR of 23.97% during the study period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Maritime Transport Segment Dominated Due to Increasing Regulatory Pressure from Global Bodies to Reduce Emissions

By application, the market is classified into maritime transport, power generation, industrial applications, and others.

In 2025, the maritime transport segment dominated, accounting for 56.08% share. This growth is attributed to increasing regulatory pressure from global bodies to reduce emissions in international shipping. Ammonia is gaining traction as a viable fuel for long-haul vessels where electrification is not feasible. Additionally, rising investments in ammonia-ready ships and fuel infrastructure are supporting its early adoption in this sector.

The power generation segment is expected to grow at a CAGR of 23.35% during the forecast period.

By End User

Shipping & Maritime Segment Led due to the High Demand for Low-Carbon Emission Fuels for Long-Distance Operations

On the basis of end user, the market is classified into shipping & maritime, power & utilities, oil & gas, heavy industries, and others.

In 2025, the shipping & maritime segment dominated the global market. This growth is due to the sector’s urgent need for scalable, low-carbon emission fuels for long-distance operations. Ammonia offers high energy density and suitability for large vessels, making it a strong alternative to conventional marine fuels as industry transitions accelerate.

The power & utilities segment is expected to grow at a CAGR of 23.57% during the forecast period.

Ammonia Fuel Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Ammonia Fuel Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North American market was valued at USD 97.43 million, and continues to maintain its significant share in 2026, reaching USD 121.60 million. The market is driven by increasing investments in blue ammonia production and carbon capture integration. The U.S. leads the region with multiple announced projects leveraging its abundant natural gas resources and expanding CCS infrastructure. Additionally, government-backed initiatives such as hydrogen hubs are supporting ammonia’s role as an energy carrier and fuel. Canada is also gaining traction, particularly in green ammonia production, with projects focused on export to Europe.

U.S. Ammonia Fuel Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 74.98 million in 2025, accounting for roughly 11.52% of the global market size.

Europe

Europe is projected to record a growth rate of 21.95% in the coming years, which is the second-highest among all regions. The market was valued at USD 155.64 million in 2025. The growth is supported by strong policy-driven demand and rapid development of green ammonia production and import infrastructure. Countries such as the Netherlands and Germany are focusing on establishing ammonia import terminals and integrating it into existing energy systems, particularly for industrial and power applications. Additionally, Southern Europe, including Spain and Portugal, is emerging as a low-cost production hub supported by abundant renewable electricity.

Germany Ammonia Fuel Market

The German market reached around USD 26.10 million in 2025 and is estimated to reach approximately USD 32.52 million by 2026, representing roughly 4.01% of the global revenues. Germany plays a crucial role in the market as a major demand center rather than a large-scale producer. The country is focusing on importing green ammonia to support industrial decarbonization and energy transition goals. It is also investing in port infrastructure and supply chains to integrate ammonia into power generation and industrial applications.

Asia Pacific

The market in Asia Pacific was valued at USD 299.00 million in 2025, securing the largest share of the market. In the region, India was valued at USD 21.93 million in 2025. The dominance is supported by strong demand from countries such as Japan and South Korea, which are actively adopting ammonia in power generation and shipping. The region is also supported by major export-oriented production hubs such as Australia, enabling a well-established supply-demand ecosystem.

India Ammonia Fuel Market

The Indian market in 2025 stood at around USD 21.93 million, accounting for roughly 3.37% of global revenues. India is an emerging market, driven by its National Green Hydrogen Mission and increasing focus on developing green ammonia for domestic use and export.

China Ammonia Fuel Market

China’s market is projected to be significant worldwide during the study period, with 2025 revenues standing at around USD 50.68 million, representing roughly 7.79% of the global market.

Japan Ammonia Fuel Market

The Japanese market in 2025 stood at around USD 94.66 million, accounting for roughly 14.54% of global revenues.

Latin America

Latin America reached a valuation of USD 25.49 million in 2025 and is expected to witness moderate growth in this market during the forecast period. Latin America is an emerging region, led by Chile and Brazil, leveraging abundant renewable resources to develop green ammonia for export-oriented markets.

Brazil Ammonia Fuel Market

Brazil's market stood at around USD 11.25 million in 2025, representing roughly 1.73% of the global market.

Middle East & Africa

The Middle East & Africa reached a valuation of USD 73.35 million in 2025 and is expected to witness significant growth in this market during the forecast period. The region is emerging as a key production hub for the product, driven by large-scale blue and green ammonia projects in the GCC. The region is also gaining momentum as an export powerhouse, supplying low-cost ammonia to Europe and Asia.

GCC Ammonia Fuel Market

The GCC market was valued at around USD 48.04 million in 2025, representing roughly 7.38% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Major players are Emphasizing on Expanding Manufacturing Presence to Gain Competitive Edge

The global ammonia fuel market holds a consolidated market structure, constituting prominent players such as Yara International ASA, OCI N.V., and Air Liquide S.A. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technological advancement, expanding manufacturing presence, and other areas.

- For instance, in June 2023, Yara International announced progress on its green ammonia project in Herøya, Norway, aimed at producing low-carbon ammonia using renewable hydrogen. The facility is designed to decarbonize existing ammonia production and support maritime fuel applications. Yara is also collaborating with shipping partners to enable ammonia as a marine fuel, leveraging its global distribution network to accelerate adoption across Europe and international markets.

Other key players in the global market include CF Industries Holdings, Inc., BASF SE, and QatarEnergy. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY AMMONIA FUEL COMPANIES PROFILED

- Yara International ASA (Norway)

- OCI N.V. (Netherlands)

- Air Liquide S.A. (France)

- CF Industries Holdings, Inc. (U.S.)

- BASF SE (Germany)

- QatarEnergy (Qatar)

- ExxonMobil Corporation (U.S.)

- Royal Dutch Shell plc (U.K.)

- SABIC (Saudi Arabia)

- Eni S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- March 2024: CF Industries announced plans to expand its green ammonia production capabilities in North America, leveraging renewable energy and carbon-reduction technologies. The company is targeting ammonia supply for clean fuel markets, including maritime and power sectors. CF Industries is also collaborating with partners to develop infrastructure and supply chains, positioning itself as a key supplier of carbon-free ammonia in the evolving energy landscape.

- October 2023: OCI N.V. advanced its green ammonia strategy by announcing plans to develop low-carbon ammonia production facilities in the U.S. and Europe, focusing on integrating renewable hydrogen. The company aims to supply ammonia for fuel and industrial decarbonization applications. OCI is also exploring partnerships for export-oriented supply chains, positioning itself as a key player in delivering green ammonia to energy-importing regions.

- September 2023: Air Liquide announced its involvement in large-scale renewable hydrogen projects in Europe, supporting the production of green ammonia for energy applications. The company is focusing on integrating electrolyzer technology with ammonia synthesis to enable a low-carbon fuel supply. These initiatives are aligned with Europe’s decarbonization goals and are expected to support both industrial and maritime fuel demand in the coming years.

- August 2023: QatarEnergy announced initiatives to develop low-carbon ammonia production facilities, including green ammonia projects leveraging renewable energy integration. The company is positioning itself as a major exporter of clean ammonia to global markets, particularly Europe and Asia. These efforts align with Qatar’s broader strategy to diversify its energy portfolio and support global decarbonization efforts.

- July 2023: BASF announced its participation in green hydrogen and ammonia projects in Europe, focusing on integrating renewable energy into ammonia production processes. The company aims to reduce emissions from its chemical operations while supporting ammonia’s use as a clean fuel. BASF is also exploring partnerships to scale green ammonia supply for industrial and energy applications across the region.

REPORT COVERAGE

The global ammonia fuel market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.28% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Fuel Type, Application, End User, and Region |

| By Fuel Type |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 650.91 million in 2025 and is projected to reach USD 4,114.44 million by 2034.

In 2025, the Asia Pacific regional market value stood at USD 299.00 million.

The market is expected to exhibit a CAGR of 22.28% during the forecast period.

In 2025, the blue ammonia segment led the market by fuel type.

Growing strategic investments in export-oriented ammonia supply chains are the key factors driving the market.

BASF SE, QatarEnergy, and ExxonMobil Corporation are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us