Ammonium Fluoride Market Size, Share & Industry Analysis, By Type (Industrial/Technical Grade, Electronic Grade, Reagent/Analytical Grade, and Others), By Application (Glass Etching/Frosting, Semiconductor & Electronics, Metal Surface Treatment, Analytical/Lab & Chemical Synthesis, and Others), and Regional Forecast, 2026-2034

Ammonium Fluoride Market Size and Future Outlook

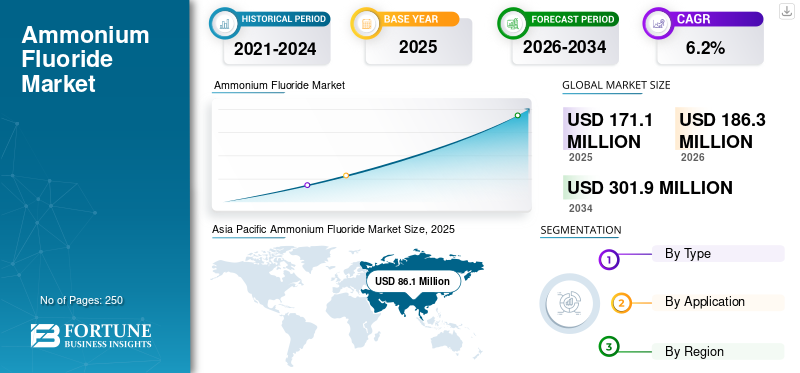

The global ammonium fluoride market size was valued at USD 171.1 million in 2025. The market is projected to grow from USD 186.3 million in 2026 to USD 301.9 million by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the ammonium fluoride market, accounting for 50.32% of the market in 2025.

Ammonium fluoride (NH₄F) is an inorganic fluoride salt widely used for glass etching, semiconductor processing, metal surface treatment, and laboratory synthesis. It is valued for its ability to react with silica and metal oxides, enabling controlled surface modification and cleaning applications. Industrial and technical-grade ammonium fluoride is used in bulk glass frosting and metal treatment processes. At the same time, high-purity electronic and reagent grades are utilized in semiconductor manufacturing and analytical laboratories. Growing demand from specialty glass processing and electronics fabrication significantly supports market expansion. Increasing miniaturization in semiconductor devices further strengthens demand for high-purity grades. Expanding industrial surface treatment and chemical synthesis applications also contribute to steady consumption. As electronics manufacturing and precision surface technologies continue to evolve globally, ammonium fluoride maintains strategic importance in both industrial and advanced technology sectors, thus reinforcing its relevance in specialty chemical markets.

The major key players operating in the market are Solvay S.A., Arkema S.A., Navin Fluorine International Limited, Tanfac Industries Limited, and Fluorsid S.p.A.

Download Free sample to learn more about this report.

Ammonium Fluoride Market KEY TAKEAWAYS

- 2025 Market Size: USD 171.1 million

- 2026 Market Size: USD 186.3 million

- 2034 Forecast Market Size: USD 301.9 million

- CAGR: 6.2% from 2026–2034

- Asia Pacific dominated the ammonium fluoride market with a 50.32% share in 2025.

- The electronic grade segment is projected to grow at a CAGR of 5.3% during the forecast period.

- The glass etching/frosting segment is expected to grow at the fastest CAGR of 7.2% during the forecast period.

Asia Pacific

Asia Pacific USD 86.1 million in 2025, driven by strong semiconductor fabrication and specialty glass production.

North America

North America Expected to witness steady growth, supported by semiconductor reshoring and industrial glass manufacturing.

Europe

Europe Expected to register significant growth due to advanced specialty manufacturing and semiconductor investments.

U.S.

U.S. USD 26.5 million in 2025, supported by growing electronics manufacturing and architectural glass demand.

Japan

Japan Supported by strong demand from semiconductor manufacturing, specialty glass production, and high-purity chemical applications.

Read More

Ammonium Fluoride Market Trends

Semiconductor Miniaturization and Decorative Glass Applications are Reshaping Consumption Patterns

The market is influenced by rapid advancements by semiconductor manufacturers and growing decorative glass applications. Increasing demand for precision etching chemicals in integrated circuit fabrication is driving high-purity electronic-grade consumption. Simultaneously, architectural and automotive decorative glass usage supports steady industrial-grade demand. Rising production of solar panels and specialty optical components further strengthens etching chemical consumption. Regulatory emphasis on controlled chemical handling influences production standards and supply chain practices. Technological advancements in ultra-high purity fluoride formulations are enhancing compatibility with sensitive electronic processes. Additionally, industrial automation and surface treatment expansion in emerging economies contribute incremental growth. These electronics-driven and architectural trends are reshaping demand patterns, thus supporting stable expansion in the market.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Strong Product Demand from Glass Etching and Semiconductor Fabrication Activity Boosts Market Growth

The primary driver of the market is strong demand from glass etching and frosting applications. It reacts effectively with silica, enabling controlled surface treatment for decorative and industrial glass. Expanding architectural and automotive glass usage significantly supports demand. Additionally, semiconductor fabrication processes rely on fluoride-based chemicals for wafer cleaning and etching, driving electronic-grade consumption. Rising investments in chip manufacturing facilities further reinforce demand growth. Increasing industrial metal treatment applications also contribute to consumption. These diversified industrial and electronic drivers sustain steady demand expansion, thus maintaining ammonium fluoride market growth momentum.

Market Restraints

Toxicity Concerns and Regulatory Oversight Limit Market Flexibility

Ammonium fluoride is a hazardous chemical requiring strict handling, storage, and transportation protocols. Regulatory scrutiny regarding worker safety and environmental discharge increases compliance costs. Exposure risks necessitate advanced protective equipment and monitoring systems in manufacturing facilities. Additionally, the availability of substitute etching chemicals in certain applications may limit demand in cost-sensitive segments. Environmental regulations governing fluoride waste disposal further impact production economics. These safety and regulatory pressures create operational constraints, hence moderating overall market growth potential.

MARKET OPPORTUNITIES

Expanding Electronics Manufacturing and Specialty Glass Demand Generate New Market Growth Prospects

Significant opportunities exist in expanding the semiconductor industry along with fabrication facilities, particularly in Asia Pacific and North America. Government incentives supporting domestic chip production increase demand for electronic-grade ammonium fluoride. Growth in specialty glass used in consumer electronics, automotive displays, and solar panels presents additional expansion avenues. Industrial modernization in metal finishing and surface preparation also supports broader technical-grade adoption. Increasing research activity in chemical synthesis and analytical testing further enhances reagent-grade demand. Emerging economies investing in electronics assembly and precision manufacturing create incremental market opportunities. As technology-driven manufacturing continues to expand globally, ammonium fluoride consumption is expected to rise steadily, therefore strengthening long-term market prospects.

MARKET CHALLENGES

Quality, Supply, and Regulatory Challenges Influence Competitive Dynamics

A key challenge in the market is maintaining demand for high purity levels required for semiconductor and electronic applications. Even minor impurities can impact chip fabrication yields, requiring advanced refining and quality control systems. The sourcing of Raw materials and fluorine supply stability also influence pricing and availability. Additionally, balancing industrial-grade volume production with specialty-grade precision manufacturing adds operational complexity. Increasing environmental and occupational safety compliance costs further impact margins. These quality, supply, and regulatory challenges shape competitive positioning, therefore influencing long-term market stability.

RESEARCH AND DEVELOPMENT TRENDS

R&D efforts focus on improving ultra-high purity ammonium fluoride formulations for semiconductor applications. Advances in contamination control and packaging technologies are enhancing product reliability for sensitive electronic processes.

Segmentation Analysis

By Type

High-Volume Glass and Metal Processing Applications Boost Industrial/Technical Grade Segment Growth

Based on type, the market is segmented into industrial/technical grade, electronic grade, reagent/analytical grade, and others.

The industrial/technical grade segment holds the largest ammonium fluoride market share due to its widespread use in glass etching, frosting, and metal surface treatment. Bulk architectural glass production and decorative glass processing significantly support consumption. Industrial cleaning and oxide removal applications further contribute to steady demand. Its relatively lower purity requirement compared to electronic grade ammonium fluoride allows cost-efficient large-scale production. Growing construction activity and automotive glass usage sustain stable volume demand. These high-volume industrial applications ensure dominant market positioning, thus maintaining industrial-grade leadership in the market.

The electronic grade segment is expected to grow at a CAGR of 5.3% during the forecast period, as it is used in semiconductor wafer cleaning and etching processes where ultra-high purity is critical. Increasing chip manufacturing investments and device miniaturization significantly support demand. Though lower in volume than industrial grade, higher pricing and value addition characterize this segment. Expanding global semiconductor fabrication capacity sustains long-term growth, hence reinforcing its strategic importance.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rapid Expansion of Chip Fabrication Facilities Boosted Semiconductor & Electronics Segment Growth

In terms of application, the market is segmented into glass etching/frosting, semiconductor & electronics, metal surface treatment, analytical/lab & chemical synthesis, and others.

The semiconductor & electronics segment held the largest market share in 2025. Ammonium fluoride is essential in semiconductor wafer processing for oxide removal and etching. The rapid expansion of chip fabrication facilities globally strengthens demand. Though lower in volume than glass applications, high-value electronic-grade usage supports incremental growth, hence enhancing segment importance.

The glass etching/frosting segment is growing at a highest CAGR of 7.2% during the forecast period. This is due to ammonium fluoride’s ability to react with silica and create controlled surface textures. Growing architectural design trends and automotive decorative glass applications significantly support demand. Expanding specialty glass manufacturing further reinforces consumption, thus maintaining segment growth.

AMMONIUM FLUORIDE MARKET REGIONAL OUTLOOK

Based on region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Ammonium Fluoride Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The market size in Asia Pacific stood at USD 86.1 million in 2025. Asia Pacific holds the dominant share in the market due to strong semiconductor fabrication capacity and expanding specialty glass production. China, Japan, South Korea, and Taiwan are major hubs for electronics manufacturing, driving demand for high-purity electronic-grade ammonium fluoride used in wafer cleaning and etching processes. Additionally, rapid infrastructure development and decorative architectural trends increase demand for glass etching and frosting applications.

Expanding solar panel production and display glass manufacturing further reinforces industrial-grade consumption. Competitive chemical manufacturing costs and integrated supply chains strengthen regional production capabilities. Growing government incentives for domestic semiconductor expansion in China and India also support long-term demand. These electronics-driven and construction-related factors collectively sustain strong consumption, thus reinforcing Asia Pacific’s leadership in the global market.

China Ammonium Fluoride Market

Based on Asia Pacific’s strong contribution and China’s position as the leading country in the regional market, the China market was valued at USD 28.6 million in 2025, accounting for approximately 16.7% of regional revenues. Growth is driven by large-scale semiconductor fabrication capacity and expanding specialty glass manufacturing.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a stable and technology-driven market, supported by expanding semiconductor reshoring initiatives and established industrial glass production. The U.S. is the primary contributor, with increasing investments in domestic chip fabrication facilities driving demand for electronic-grade ammonium fluoride. Strong aerospace and defense manufacturing sectors further support specialty electronic applications.

U.S. Ammonium Fluoride Market

The U.S. market in 2025 reached a valuation of USD 26.5 million, accounting for approximately 15.5% of regional revenues. Expansion is supported by increasing electronics manufacturing initiatives and rising architectural glass demand.

Europe

Europe’s market is shaped by stringent environmental regulations and advanced specialty manufacturing industries. Countries such as Germany, France, and the U.K. exhibit steady demand from specialty glass production, automotive surface treatment, and semiconductor-related industries. Although semiconductor fabrication capacity is smaller than in the Asia Pacific, ongoing EU-backed investments in chip manufacturing support incremental growth. Strict REACH regulations influence production processes and encourage high-purity, compliant formulations.

Germany Ammonium Fluoride Market

Germany’s market reached a valuation of USD 8.4 million in 2025, accounting for approximately 4.9% of regional revenues. Demand is driven by specialty automotive glass production and advanced industrial surface engineering.

Latin America & Middle East & Africa

Latin America demonstrates gradual growth in the market, primarily driven by expanding infrastructure and glass processing industries. Brazil and Mexico lead regional demand due to increasing architectural glass usage and automotive manufacturing. Industrial surface treatment and metal processing activities support steady technical-grade consumption.

The Middle East & Africa region is witnessing gradual growth in ammonium fluoride demand, supported by infrastructure diversification and expanding industrial activities. GCC countries are investing in construction, architectural glass production, and specialty surface treatment industries. Growing petrochemical and metal processing sectors further reinforce industrial-grade consumption.

GCC Ammonium Fluoride Market

The GCC market in 2025 was valued at USD 5.2 million, accounting for approximately 3.1% of revenues. Expansion is driven by infrastructure development and increasing architectural glass frosting applications.

Competitive Landscape

Key Industry Players

Purity Requirements and Integrated Fluorochemical Production Shaping Market Structure

The global market is moderately fragmented, with competition largely driven by fluorochemical integration and product purity capabilities. Leading manufacturers benefit from access to fluorspar resources and vertically integrated hydrofluoric acid production, enabling cost control and supply stability. Electronic-grade suppliers compete on ultra-high purity standards and contamination control technologies, while industrial-grade producers focus on scale and export reach. Asian manufacturers leverage cost efficiencies, whereas European and Japanese players emphasize specialty and semiconductor-grade formulations. Strict environmental impact and safety regulations create entry barriers and encourage continuous technological upgrades. These integration advantages and purity-driven requirements collectively shape competitive positioning, therefore reinforcing the dominance of established fluorochemical producers.

LIST OF KEY AMMONIUM FLUORIDE COMPANIES PROFILED

- Solvay S.A. (Belgium)

- Arkema S.A. (France)

- Navin Fluorine International Limited (India)

- Tanfac Industries Limited (India)

- Fluorsid S.p.A. (Italy)

- Derivados del Flúor S.A.U. (DDF) (Spain)

- Morita Chemical Industries Co., Ltd. (Japan)

- Harshil Industries (India)

- Jayfluoride Private Limited (India)

- Mars Chemical Corporation (India)

REPORT COVERAGE

The global ammonium fluoride market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, type, and application. Also, it offers insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors contributing to the market's growth in recent years. It further includes historical data & forecasts revenue growth at global, regional, and country levels and analyzes the industry's latest market dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Million) and Volume (Kiloton) |

| Growth Rate | CAGR of 6.2% from 2026 to 2034 |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 171.1 million in 2025 and is projected to reach USD 301.9 million by 2034.

In 2025, the Asia Pacific market size stood at USD 86.1 million.

Registering a CAGR of 6.2%, the market will exhibit steady growth during the forecast period (2026-2034).

By application, the semiconductor & electronics segment led the market in 2025.

Strong product demand from glass etching and semiconductor fabrication activity is boosting market growth.

Solvay S.A., Arkema S.A., Navin Fluorine International Limited, Tanfac Industries Limited, and Fluorsid S.p.A. are the major players in the market.

Asia Pacific dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us