Etching Chemicals Market Size, Share & Industry Analysis, By Application (Semiconductor, Metal Finishing, Printed Circuit Boards, Glass & Ceramics, and Others), and Regional Forecast, 2026-2034

ETCHING CHEMICALS MARKET SIZE AND FUTURE OUTLOOK

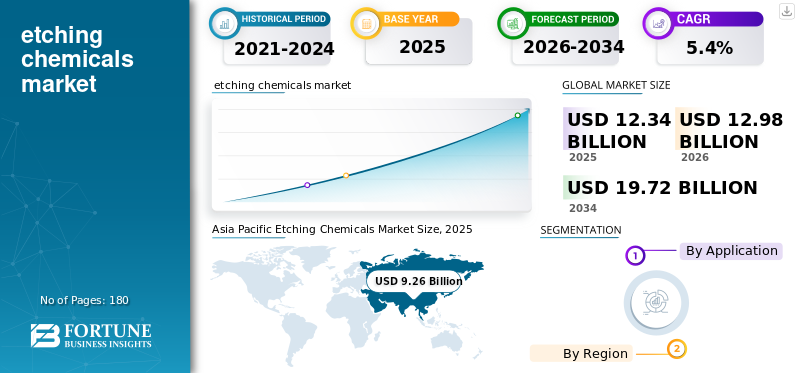

The global etching chemicals market size was USD 12.34 billion in 2025. The market is projected to grow from USD 12.98 billion in 2026 to USD 19.72 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the etching chemicals market with a market share of 75.04% in 2025.

Etching chemicals are specialty formulations used to selectively remove material from substrates such as silicon wafers, copper, metals, glass, or ceramics to create patterns, micro-textures, or activate surfaces before deposition and bonding. They are critical in semiconductor fabrication, printed circuit board copper patterning, metal finishing pickling, and ceramic surface treatment. A major demand driver is the rapid expansion of semiconductor manufacturing processes complexity, which increases consumption of high-purity etchants and associated process chemistries. FUJIFILM Holdings Corporation, Merck KGaA, Kanto Chemical, and Stella Chemifa are a few of the major players in the market.

Download Free sample to learn more about this report.

ETCHING CHEMICALS MARKET TRENDS

AI Chip Boom Accelerates Fab Expansion Driving High-Purity Etchant Demand

A major global trend is the shift toward higher purity, tighter spec etching chemistries as semiconductor and advanced packaging processes become more complex. Leading-edge nodes, 3D transistor architectures, and higher-layer interconnect stacks require greater selectivity, lower defectivity, and lower contamination, pushing fabs to qualify more sophisticated wet etchants and complementary process chemistries. In parallel, PCB makers are upgrading to finer lines and higher-density interconnect, increasing usage of micro-etch and controlled copper etchants. Sustainability is also shaping formulations for more bath life optimization, regeneration, and lower waste loads are being engineered into chemistry programs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Electronics Complexity Increases Process Steps Intensifying Etchant Consumption

The primary demand driver is the structural growth in electronic manufacturing intensity, especially semiconductors. More devices per person, accelerating data center buildouts, electrification of vehicles, and industrial automation raise silicon content and packaging complexity. This expands both front-end wafer processing and back-end packaging, each needing etch chemicals. In PCB and plating lines, demand is reinforced by the need for higher reliability boards for automotive and mission-critical electronics, sustaining consumption of etchants and activation chemistries that ensure adhesion and performance.

MARKET RESTRAINTS

Tighter EHS Rules Raise Compliance Costs Might Reduce Adoption of Hazardous Chemistries

A key restraint is regulatory and Environmental, Health, and Safety (EHS) pressure on hazardous and corrosive etchants, which increases total cost of ownership through handling controls, abatement, worker safety, and waste treatment. Customers may delay chemistry changes due to qualification burden, especially in semiconductors, where re-qualifying etch chemistry can risk yield and uptime. In metal finishing, compliance costs can push smaller shops to reduce wet processing or consolidate operations. Additionally, end-users increased demand, lower emissions, lower toxicity, and reduced wastewater loading, which can constrain legacy chemistries and slow etching chemicals market growth in applications with limited substitution options.

MARKET OPPORTUNITIES

Supply-Chain Localization Expands Regional Fabs Creating Opportunities for New Entrants

A major opportunity is the geographic diversification of manufacturing, new fabs, packaging plants, and electronics supply chains create openings for suppliers to establish local production, blending, and ultra-pure distribution near customer clusters. Winning opportunity areas include high-purity electronic-grade etchants, tailored chemistries for advanced substrates, and closed-loop regeneration and waste minimization services that reduce customer operating cost and regulatory burden. In PCB and plating, suppliers can differentiate with etchants that improve line definition, undercut control, and bath stability while enabling higher throughput.

MARKET CHALLENGES

Purity and Performance Demands Tighten While Inputs Stay Volatile, Therefore Reliability Becomes the Winning Challenge

The defining challenge is delivering consistent performance at near-zero defect tolerance amid raw-material volatility and increasingly strict impurity limits. Semiconductor customers require ultra-low metals and particles, stable etch rates, and tight lot-to-lot uniformity; any deviation can trigger yield loss and requalification. Scaling capacity adds difficulty, building and operating ultra-pure manufacturing, contamination-free packaging, and robust logistics is capital intensive. For bulk segments (metal finishing), suppliers face margin pressure from commodity input swings while customers demand reduced waste and better bath life. Across all segments, the challenge is balancing cost, sustainability, and qualification risk, while proving reliability under high-volume production conditions.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Semiconductor Regulatory Compliance and Powder Format Dominance Fuel Demand

Based on the application, the market is segmented into semiconductor, metal finishing, printed circuit boards, glass & ceramics and others.

The semiconductor segment is anticipated to hold the dominant etching chemicals market share during the forecast period. The key driver in semiconductors is the rapid increase in process complexity per wafer, not just wafer volume growth. Advanced nodes, 3D transistor architectures, and multi-layer interconnect stacks require more etch steps, tighter selectivity, and ultra-low contamination thresholds, increasing consumption of high-purity etching chemistries per wafer. In parallel, advanced packaging and heterogeneous integration add additional etch and surface-conditioning steps beyond the front end, structurally lifting etchant demand and driving market growth in tandem.

In printed circuit boards, demand is driven by the shift toward higher-density interconnect and finer copper line geometries, especially for automotive, data center, and industrial electronics. Achieving tight line definition, controlled undercut, and strong copper adhesion requires a more frequent and precisely controlled etching process. At the same time, stricter reliability and performance standards increase process control and chemistry consumption per board, making PCB etchants one of the fastest-growing uses of etching chemicals globally.

The printed circuit boards segment is anticipated to rise with a CAGR of 4.5% over the forecast period.

ETCHING CHEMICALS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Etching Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region is expected to dominate the market during the forecast period. Asia Pacific is driven primarily by semiconductor manufacturing, which dominates regional etching chemical demand due to the concentration of wafer fabs, advanced logic, memory, and packaging capacity. Rising process complexity, higher layer counts, and advanced nodes increase etch steps and purity requirements per wafer. Printed circuit boards provide a strong secondary driver, supported by fine line HDI boards for consumer electronics, data centers, and automotive. Metal finishing and glass & ceramics contribute mainly through manufacturing scale, but semiconductor-led value density makes the region the structural demand center globally.

Japan Etching Chemicals Market

Japan’s market value reached approximately USD 1.62 billion in 2025, equivalent to around 13.1% of global sales.

China Etching Chemicals Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 3.07 billion, representing roughly 24.9% of global sales.

Taiwan Etching Chemicals Market

Taiwan’s market size reached approximately USD 3.01 billion in 2025, equivalent to around 24.4% of the global market.

North America

In North America, demand is led by semiconductor fabrication and advanced packaging, driven by new fab construction, technology upgrades, and reshoring of electronics manufacturing. High-purity etching chemicals witness rising consumption as fabs ramp production and qualify advanced processes. Metal finishing supports demand through aerospace, defense, and industrial manufacturing, while printed circuit boards contribute modestly via specialized and high-reliability boards. The region’s demand growth is value-driven rather than volume-driven, reflecting a strong tilt toward advanced, tightly specified etch chemistries.

U.S. Etching Chemicals Market

The U.S. market analytically approximated at around USD 0.96 billion in 2025, accounting for roughly 7.8% of global sales.

Europe

Europe’s etching chemicals demand is anchored in metal finishing, supported by automotive, machinery, and industrial manufacturing that relies heavily on pickling and surface activation. However, semiconductor manufacturing is an increasingly important growth driver as Europe invests in power electronics, automotive chips, and strategic fabs, lifting demand for higher-value etch chemistries. Glass & ceramics also play a meaningful role due to Europe’s flat-glass and specialty materials footprint. PCB demand is steady but secondary, reflecting a smaller regional manufacturing base.

U.K. Etching Chemicals Market

U.K.’s market size reached approximately USD 0.06 billion in 2025, equivalent to around 0.5% of global market share.

Germany Etching Chemicals Market

Germany’s market size is projected to reach approximately USD 0.29 billion in 2025, equivalent to around 2.4% of global sales.

Rest of World

In the rest of the world region, demand is primarily driven by metal finishing, reflecting infrastructure development, fabrication, and general industrial activity that consume large volumes of bulk etchants. Glass & ceramics support demand through construction-related processing and materials finishing. A smaller but important value driver is semiconductor manufacturing in select countries, which disproportionately raises etching-chemical value despite limited volume. PCB and other niche applications contribute incrementally, but industrial surface treatment remains the backbone of regional demand.

Israel Etching Chemicals Market

Israel’s market value reached approximately USD 0.16 billion in 2025, equivalent to around 1.3% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Fab Complexity and Localization Shift Market Toward High-Purity Specialists

Globally, the etching chemicals market is segmented into a high-margin, qualification-heavy semiconductor segment and a more price-competitive industrial segment (PCB/metal/glass etchants) where bath life, regeneration, and EHS compliance matter. Competition is shaped by long customer qualification cycles, contamination-free manufacturing and logistics, and growing localization near new fabs and packaging clusters. Suppliers also differentiate through technical service, on-site bath management, and impurity analytics. Mild consolidation is emerging as players broaden portfolios across wet etch, post-etch cleaning, and surface preparation. Top key players include FUJIFILM Holdings Corporation, Merck KGaA, Kanto Chemical, and Stella Chemifa.

LIST OF KEY ETCHING CHEMICALS COMPANIES PROFILED

- BASF (Germany)

- Daken Chemical Limited (China)

- FUJIFILM Holdings Corporation (Japan)

- KANTO KAGAKU (Japan)

- MG Chemicals (Canada)

- Merck KGaA (Germany)

- Resonac Holdings Corporation (Japan)

- Solvay (Belgium)

- Stella Chemifa Corporation (Japan)

- Transene Company, Inc. (U.S.)

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 5.4% during 2026-2034 |

| Segmentation | By Application, and Region |

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 12.34 billion in 2025 and is projected to record a valuation of USD 19.72 billion by 2034.

In 2025, Asia Pacific stood at USD 9.26 billion.

Registering a CAGR of 5.4%, the market will exhibit steady growth during the forecast period.

The semiconductor application is expected to lead this market during the forecast period.

The rising electronics complexity increases process steps intensifying etchant consumption is driving the market growth.

FUJIFILM Holdings Corporation, Merck KGaA, Kanto Chemical, and Stella Chemifa are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us