Advanced Packaging Market Size, Share & Industry Analysis, By Packaging Type (2.5D/3D ICs, Fan-Out-Wafer-Level Packaging (FO-WLP), Fan-In-Wafer-Level Packaging (FI-WLP), Flip-Chip Packaging, Wafer-Level-Chip-Scale Packaging (WLCSP), and Others), By End-use Industry (Consumer Electronics, Automotive, Healthcare, Industrial, Telecommunications, and Others), and Regional Forecast, 2026-2034

Advanced Packaging Market Overview

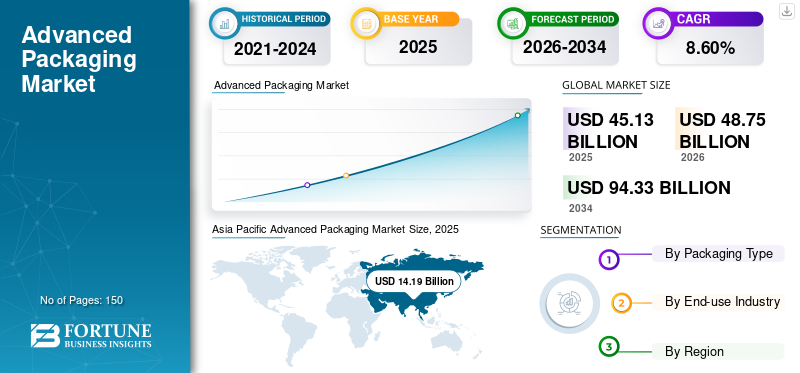

The global advanced packaging market size was valued at USD 45.13 billion in 2025. The market is projected to grow from USD 48.75 billion in 2026 to USD 94.33 billion by 2034, exhibiting a CAGR of 8.60% during the forecast period. Asia Pacific dominated the advanced packaging market with a market share of 31.44% in 2025.

The global market encompasses semiconductor packaging technologies that improve chip performance, density, and functionality by combining multiple dies or components into a single package through techniques such as 2.5D/3D packaging, system-in-package (SiP), and wafer-level packaging. The growing demand for high-performance computing, artificial intelligence, and miniaturized electronics is propelling the adoption of advanced packaging, as conventional scaling methods encounter challenges in enhancing chip performance, power efficiency, and integration density.

Furthermore, many key players, such as Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, and SK Hynix, operating in the market, are focusing on developing innovative products and conducting R&D.

Download Free sample to learn more about this report.

Advanced Packaging Market KeyTakeaways

- 2025 Market Size: USD 45.13 Billion

- 2026 Market Size: USD 48.75 Billion

- 2034 Forecast Market Size: USD 94.33 Billion

- CAGR: 8.60% from 2026–2034

- Asia Pacific dominated the advanced packaging market with a 31.44% share in 2025.

- The 2.5D/3D ICs segment accounted for the largest market share in 2025.

- The fan-out wafer-level packaging (FO-WLP) segment is projected to grow at the highest CAGR of 8.71% during the forecast period.

Asia Pacific

Asia Pacific generated USD 14.19 billion in 2025.

North America

North America reached USD 13.34 billion in 2025.

Europe

Europe reached USD 7.82 billion in 2025 and is projected to grow at a CAGR of 8.28%.

U.S.

The advanced packaging market was valued at approximately USD 11.57 billion in 2025.

Japan

The advanced packaging market reached approximately USD 2.73 billion in 2025.

Read More

ADVANCED PACKAGING MARKET TRENDS

Shift toward Heterogeneous Integration is a Prominent Trend Observed in the Market

A significant trend in the global market is the rising adoption of heterogeneous integration, which involves the combination of multiple chips with varying functionalities into a single package. This method facilitates enhanced performance, lower power consumption, and increased design flexibility when compared to conventional monolithic chips. As applications become more complex, particularly in areas such as artificial intelligence, high-performance computing, and 5G infrastructure, manufacturers are utilizing technologies such as chiplets, 2.5D interposers, and 3D stacking. Additionally, this trend is fueled by the deceleration of Moore’s Law, prompting semiconductor firms to consider packaging as a crucial layer for innovation. Consequently, advanced packaging is emerging as a fundamental strategy for achieving greater functionality and optimizing system-level performance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for High-Performance Computing Applications to Drive Market Growth

The swift growth of high-performance computing (HPC) applications serves as a significant catalyst for the advanced packaging market growth. Sectors including data centers, cloud computing, and artificial intelligence necessitate enhanced processing speeds, greater bandwidth, and superior energy efficiency, all of which advanced packaging technologies can provide. Conventional semiconductor scaling has become inadequate to fulfill these demands, leading to a transition toward packaging innovations such as system-in-package and 3D integration. As businesses increasingly depend on advanced computing capabilities, the demand for these packaging solutions is experiencing substantial growth.

MARKET RESTRAINTS

High Manufacturing and Development Costs to Hamper Market Growth

One of the primary constraints in the market is the substantial cost linked to manufacturing and development. Advanced packaging methods necessitate specialized equipment, intricate design processes, and high-precision materials, which contribute to elevated capital expenditures for semiconductor firms. Moreover, the requirement for advanced testing and inspection systems further escalates the overall cost structure. The intricacy of integrating multiple dies into a single package also heightens the risk of defects, leading to possible yield losses. These cost-related obstacles can impede widespread adoption, especially in markets that are sensitive to price.

MARKET OPPORTUNITIES

Growth in Automotive and IoT Applications Offers Potential Growth Opportunities

The growth of sophisticated electronics in the automotive and Internet of Things (IoT) sectors offers a considerable opportunity for the industry. Contemporary vehicles are increasingly dependent on electronic systems for various functions, including autonomous driving, infotainment, and advanced driver-assistance systems, all of which necessitate compact and high-performance semiconductor solutions. Likewise, IoT devices require miniaturized components that provide enhanced functionality while maintaining low power consumption. As the global adoption of smart devices and interconnected infrastructure accelerates, the demand for innovative packaging solutions is anticipated to increase significantly, driving the growth of the market.

MARKET CHALLENGES

Thermal Management and Reliability Issues Pose a Critical Challenge to Market Growth

Thermal management and reliability issues pose a significant challenge in the sector. As the integration of components into smaller packages increases, the generation of heat rises considerably, potentially impacting device performance and longevity. Moreover, intricate packaging designs such as 3D stacking may lead to mechanical stress and reliability concerns over time. To achieve long-term durability while preserving performance, the use of advanced materials and innovative design strategies is necessary, which can be technically challenging. Tackling these issues is crucial for manufacturers to guarantee consistent product quality and comply with rigorous industry standards.

Segmentation Analysis

By Packaging Type

Enhanced Performance and Integration Density to Drive the Dominance of 2.5D/3D ICs Segment

Based on packaging type, the market is segmented into 2.5D/3D ICs, fan-out-wafer-level packaging (FO-WLP), fan-in-wafer-level packaging (FI-WLP), flip-chip packaging, wafer-level-chip-scale packaging (WLCSP), and others.

In 2025, the 2.5D/3D ICs segment dominated the global advanced packaging market share. The 2.5D and 3D IC packaging sector leads owing to its capacity to provide enhanced performance, increased integration density, and a smaller form factor in comparison to conventional packaging techniques. By vertically stacking multiple dies or arranging them side-by-side on interposers, these technologies considerably minimize interconnect lengths, thereby improving signal speed and lowering power consumption. The synergy of performance improvements, spatial efficiency, and functional adaptability establishes this sector as the frontrunner in the market.

The fan-out-wafer-level packaging (FO-WLP) segment is projected to grow at a CAGR of 8.71% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Surging Demand for High-Performance Devices to Drive the Dominance of Consumer Electronics

Based on end-use industry, the market is segmented into consumer electronics, automotive, healthcare, industrial, telecommunications, and others.

The consumer electronics segment is expected to hold a dominant market share over the forecast period. The dominance is driven by the increasing demand for compact, high-performance devices such as smartphones, tablets, wearables, and gaming consoles. The rapid innovation cycles within consumer electronics compel manufacturers to implement advanced packaging to achieve quicker time-to-market and improved device functionality. Furthermore, the rising trend of feature-rich smart devices has heightened the necessity for integrated solutions, solidifying consumer electronics as the primary end-use industry propelling market growth.

The automotive industry segment is projected to grow at a CAGR of 8.98% over the forecast period.

Advanced Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Advanced Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached a value of USD 14.19 billion in 2025 and secured the position of the largest region in the market. Nations such as China, South Korea, and Taiwan concentrate on the mass production of smartphones, wearables, and Internet of Things (IoT) devices, which in turn stimulates the demand for 2.5D/3D integrated circuits (ICs) and system-in-package (SiP) solutions. The swift pace of industrialization, along with government incentives, fosters additional growth in the market.

Japan Advanced Packaging Market

The Japanese market reached around USD 2.73 billion in 2025, accounting for roughly 6.04% of global revenues. The growth of Japan's market is primarily driven by sectors such as automotive electronics, robotics, and industrial automation.

China Advanced Packaging Market

The China market is projected to be one of the largest worldwide. The 2025 revenues of the country reached around USD 4.55 billion, representing roughly 10.09% of global sales.

India Advanced Packaging Market

The India market reached around USD 3.74 billion in 2025, accounting for roughly 8.30% of the global market.

North America

North America held the second-dominant share in 2024, with a valuation of USD 12.33 billion, and maintained its second-leading position in 2025 with a value of USD 13.34 billion. In North America, the market is propelled by the significant demand from data centers, high-performance computing, and artificial intelligence applications. Additionally, government initiatives that promote the semiconductor manufacturing are further enhancing the pace of adoption.

U.S. Advanced Packaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 11.57 billion in 2025, accounting for roughly 25.63% of global sales. In the U.S., the product adoption is driven by artificial intelligence, high-performance computing, and investments in semiconductor research and development.

Europe

The Europe market is projected to grow at a CAGR of 8.28% over the forecast period, the third-highest among regions, and reached a valuation of USD 7.82 billion in 2025. The demand for Advanced Driver-Assistance Systems (ADAS), electric vehicles, and smart manufacturing necessitates compact, high-performance semiconductors, which in turn encourages product adoption. Additionally, strict energy efficiency and environmental regulations stimulate innovation in miniaturized and dependable packaging technologies.

U.K. Advanced Packaging Market

The U.K. market reached a value of at USD 1.41 billion in 2025, representing approximately 3.13% of global revenues.

Germany Advanced Packaging Market

The Germany market reached approximately USD 1.66 billion in 2025, equivalent to around 3.67% of global sales.

Latin America

The Latin America region is expected to witness moderate growth in this market during the forecast period. The Latin America market reached a valuation of USD 5.56 billion in 2025. The increasing penetration of smartphones, the rollout of 5G technology, and heightened investment in IT infrastructure create a demand for efficient, high-performance semiconductor solutions, thereby presenting opportunities for advanced packaging technologies in the region.

Middle East & Africa

In the Middle East & Africa, South Africa reached a value of USD 1.21 billion in 2025. Investment in technology hubs and initiatives for digital transformation foster innovation in semiconductors, rendering the product essential for high-performance applications in compact electronics and industrial solutions.

Saudi Arabia Advanced Packaging Market

The Saudi Arabian market reached approximately USD 1.36 billion in 2025, accounting for roughly 3.02% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expansion of Product Launches and Collaborations among Key Players to Boost Market Progress

The global market is semi-consolidated, with pivotal players including Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, and SK Hynix. The significant market shares of these packaging industry players are due to various strategic initiatives, including partnerships among operating entities for the advancement of research.

- For instance, in October 2025, Amkor Technology commenced the construction of a new advanced packaging and testing campus for semiconductors in Peoria, Arizona, with the objective of decreasing the U.S.’s dependence on foreign packaging capabilities. This campus, which is supported by funding from the CHIPS Act, will cover an area of up to 750,000 square feet dedicated to cleanroom operations and is anticipated to start production in 2028, with the initial facility expected to be operational by mid-2027.

Other notable industry players include ASE Technology, Inc., Amkor Technology, Inc., and Advanced Packaging Solutions & Products Inc. These companies are anticipated to prioritize the launch of new products and strategic partnerships to enhance their global market shares during the analysis period.

LIST OF KEY ADVANCED PACKAGING COMPANIES PROFILED

- Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan)

- Samsung Electronics (South Korea)

- SK Hynix (South Korea)

- ASE Technology, Inc. (Taiwan)

- Amkor Technology, Inc. (U.S.)

- Advanced Packaging Solutions & Products Inc. (U.S.)

- ams-OSRAM AG (Austria)

- Hitachi High-Tech Corporation (Japan)

- Advanced Packaging Inc. (U.S.)

- ASMPT (Singapore)

- Broadcom Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- Micron Technology, Inc. (U.S.)

- NXP Semiconductor (Netherlands)

- Texas Instruments (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: TSMC recorded an unprecedented demand for its CoWoS (Chip-on-Wafer-on-Substrate) advanced packaging capabilities, fueled by robust orders from cloud service providers and AI accelerators. This situation has led TSMC to expedite its production timelines and enhance infrastructure development to address the capacity shortfall, highlighting the fact that advanced packaging capacity has emerged as a critical bottleneck within the larger semiconductor supply chain.

- November 2025: Amkor Technology's shares surged by more than 8% following the announcement from NVIDIA's CFO regarding a partnership with Amkor and Siliconware Precision Industries to collaborate on chip packaging over the next four years. This initiative is designed to enhance advanced packaging capabilities for AI accelerators and GPUs, underscoring the essential function of OSAT companies in meeting the high-performance computing requirements in a competitive market.

- September 2025: Synopsys declared a comprehensive partnership with TSMC aimed at delivering cutting-edge EDA tools and IP solutions that enhance design and sign-off processes for TSMC’s advanced packaging and multi-die technologies. This initiative bolsters AI and multi-die innovation, allowing customers to attain tape-outs more effectively on 3DIC, CoWoS, and next-generation packaging workflows.

- October 2024: Amkor Technology and Taiwan Semiconductor Manufacturing Company entered a memorandum of understanding to collaboratively enhance advanced packaging and testing capabilities near TSMC’s wafer fabrication facilities in Arizona. This partnership aims to utilize Amkor’s comprehensive services alongside TSMC’s InFO and CoWoS technologies, thereby expediting advanced packaging processes for clients focused on high-performance and communications sectors, while also reinforcing the semiconductor ecosystem in the U.S.

- April 2024: Samsung's Advanced Package (AVP) division allegedly secured a contract to deliver 2.5D packaging (I‑Cube) solutions for NVIDIA's AI GPU products. This agreement entails the packaging of several high-bandwidth memory (HBM) chips alongside GPU dies on a horizontal interposer, highlighting the increasing competition with TSMC's CoWoS solutions and affirming Samsung's commitment to advancing its packaging services.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.60% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Packaging Type, End-use Industry, and Region |

| By Packaging Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 45.13 billion in 2025 and is projected to reach USD 94.33 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 14.19 billion.

The market is anticipated to grow at a CAGR of 8.60% over the forecast period of 2026-2034.

By packaging type, the 2.5D/3D ICs segment led the market in 2025.

The rising demand for high-performance computing applications is a key factor driving market growth.

Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, and SK Hynix are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us