Commercial Vehicle Market Size, Share & Industry Analysis, By Vehicle Type (Light Commercial Vehicle, Heavy Vehicle, and Buses), By Fuel Type (I.C. Engine, EV), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

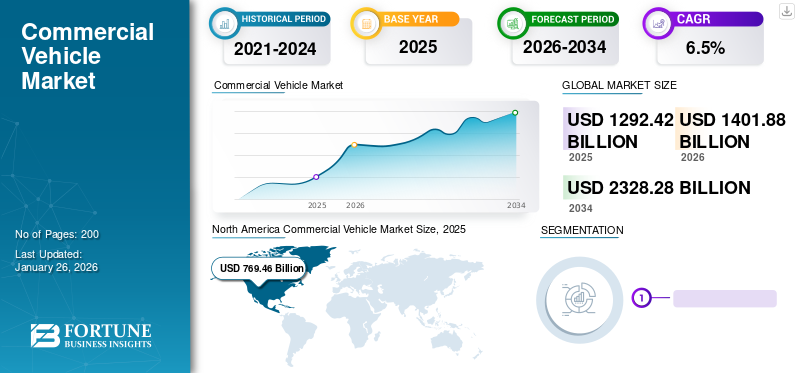

The global commercial vehicle market size was valued at USD 1292.42 billion in 2025 and is projected to grow from USD 1401.88 billion in 2026 to USD 2328.28 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. North America dominated the global market with a share of 59.54% in 2025. Additionally, the commercial vehicle market in the U.S. is projected to grow significantly, reaching an estimated value of USD 1,026.01 Billion By 2032.

The global commercial vehicle market encompasses a wide range of vehicles designed for commercial use, including trucks, buses, vans, and trailers. The vehicles play a crucial role in various industries such as logistics, construction, agriculture, and public transportation. Commercial vehicles are essential for transporting goods and passengers, facilitating economic activity and infrastructure development worldwide.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Global Commercial Vehicle Market Overview

Market Size:

- 2025 Value:USD 1292.42 billion

- 2026 Value:USD 1401.88 billion

- 2034 Forecast:USD 2328.28 billion, with a CAGR of 6.5% from 2026–2034

Market Share

- Regional Leader:North America led in 2026 with approximately 59.54% of the global market share, supported by mature logistics infrastructure and strong commercial vehicle demand

- Fastest‑Growing Region:Asia Pacific is projected for rapid growth, driven by infrastructure expansion, industrialization, and increasing adoption of EV/commercial vehicle fleets in China, India, and Southeast Asia

- End‑User Leader:Light Commercial Vehicles (LCVs) dominate the market, favored for urban logistics, delivery services, and flexible utility applications

Industry Trends

- Electric Vehicle Adoption:The EV segment is emerging fast, especially within heavy-duty and light commercial vehicles, aided by fuel-efficiency regulations and declining battery costs

- Segment Growth Dynamics:Heavy-duty vehicles are expected to register the highest CAGR (11.8%) over the forecast period, as freight and infrastructure project demand rises

- Buses and Coaches Segment:Stabilizing demand driven by public transport modernization and last-mile mobility requirements in urbanizing regions

Driving Factors

- Infrastructure & Industrial Expansion:Global urbanization and large-scale infrastructure investments are increasing commercial transport needs

- E-commerce & Logistics Growth:Demand from delivery networks and fleet operators fuels LCV demand worldwide

- Environmental Regulations:Stringent emission norms and efficiency mandates are accelerating the shift toward electric and hybrid commercial vehicles

- Technological & Fleet Innovation:Automation, telematics, and connected vehicle platforms are improving fleet management efficiency and safety

- Economic Growth in Emerging Markets:Rapid development in APAC, Latin America, and MEA regions is expanding fleet ownership and commercial vehicle penetration

The market growth is influenced by factors such as economic growth, industrialization, urbanization, government regulations, and technological advancements. Emerging economies in the Asia Pacific, Latin America, and Africa are experiencing rapid urbanization and infrastructure development, driving the demand for commercial vehicles. Additionally, advancements in technology, such as electric and autonomous vehicles, are reshaping the commercial vehicle landscape, offering opportunities for efficiency improvements and environmental sustainability.

However, the market also faces challenges such as fluctuating fuel prices, regulatory changes, supply chain disruptions, and shifting consumer preferences. Despite these challenges, the global market is expected to continue its growth trajectory, driven by the increasing demand for transportation services and infrastructure development initiatives worldwide.

The COVID-19 pandemic had a significant impact on the global commercial vehicle market as lockdown measures, supply chain disruptions, and economic uncertainties led to a decline in demand for commercial vehicles. With restrictions on movement and business activities, industries such as logistics, construction, and transportation experienced a reduced demand for commercial vehicles. However, the market was recorded to recover as economic activities gradually resumed and infrastructure projects were relaunched.

Commercial Vehicle Market Trends

Growing Usage of Advanced Technologies and Systems in Cargo Vehicles to Drive Market Growth

The use of cloud computing in the vehicle industry is growing rapidly. Cloud computing plays a vital role in freight vehicle production, and its services range from operation to design to management of various systems. The functions of cloud computing can reduce costs, thereby minimizing and reducing waste. Cloud computing makes it possible to communicate with vehicles from remote locations and retrieve and store data. Telematics is also a valuable technology for recording and evaluating operational data from vehicles. Many companies are rapidly adopting telematics in their commercial fleets. For instance, in 2020, Europcar strengthened its partnership with Geotab and Telefónica as part of its “Connect” roadmap to connect its entire fleet by 2023.

Commercial Vehicle Market Growth Factors

Electrification and Adoption of Advanced Technologies to Boost the Market Growth

Globally, the rising air pollution caused by the fuel emitted by conventional vehicles leads to environmental crises. This has encouraged manufacturing companies to shift toward sustainable sources of energy. The public transportation systems of various regions are adopting electrification in freight vehicles to promote zero-emission public transport while keeping the environment clean and breathable for residents.

Governments have imposed stringent regulations to curb the rising emission level and taken various initiatives to promote the electrification of vehicles. The logistics sector is also focusing on electric vehicles by developing the infrastructures for the same. The OEMs are also working toward reducing the cost of batteries to encourage the use of electric vehicles across the globe. Various prominent players, such as Toyota, Daimler, and Volvo, are shifting toward electric vehicles to meet the rising demand. Moreover, electric vehicles are also gaining popularity in the global market, owing to their various properties such as high battery life, increased range, energy efficiency, and advancement in electronic systems. Moreover, freight vehicles are observing a trend of automation, which is driving the market.

Adopting Advanced Driving Assistance System (ADAS), such as lane departure warning systems, driver drowsiness detection systems, driver monitoring systems, and blind spot detection systems, boosts the market. Furthermore, connectivity and telematics are transforming operations to a large extent, encouraging the manufacturers to equip vehicles with several connected services as they provide enhanced safety and prevent unauthorized access to vehicles, thereby avoiding mishandling and wear & tear of freight vehicles. This is anticipated to help boost market growth over the next few years. For instance, Valeo and Wabco signed a Memorandum of Understanding (MoU) to jointly work toward developing ADAS technologies in freight vehicles. The association is working on a radar solution to deliver blind-spot warning assistance to drivers, thus complying with the German regulations.

Advancements in Infrastructure and Industrialization to Propel Market Expansion

The global commercial vehicle market is expanding propelled by developments in infrastructure and industrialization across various regions. As countries continue to invest in infrastructure projects such as road construction, highway expansion, and urban development, the demand for commercial vehicles rises. These vehicles are essential for transporting construction materials, equipment, and workers to project sites, facilitating the progress of infrastructure initiatives.

According to the International Monetary Fund (IMF), global infrastructure investment is projected to reach USD 3.7 trillion annually by 2035. The Government of India, in the 2020-21 Union Budget, allocated USD 24.27 billion to the infrastructure sector, mainly highways, renewable energy, and transportation. Japan and India have announced their association to develop infrastructure for India’s north-eastern states and set up an India-Japan Coordination Forum for the development of north-eastern infrastructure projects. This significant investment is driving the demand for commercial vehicles, particularly heavy-duty trucks and construction equipment, which play a vital role in infrastructure development projects.

Furthermore, industrialization in emerging economies is contributing to the growth of the market. As these economies experience rapid urbanization and industrial expansion, there is a growing need for efficient transportation solutions to support manufacturing, distribution, and logistics activities. Commercial vehicles such as trucks, vans, and buses are essential for transporting raw materials, finished goods, and workers within and between industrial zones.

Moreover, the adoption of e-commerce and the rise of last-mile delivery services are driving the demand for commercial vehicles, particularly light commercial vehicles (LCVs) and delivery vans. With the growth of online shopping, there is a need for efficient and reliable transportation solutions to fulfill orders and meet customer demands.

In conclusion, developments in infrastructure and industrialization are key drivers of the global commercial vehicle market. As countries continue to invest in infrastructure projects and industrial expansion, the demand for commercial vehicles is expected to remain strong, presenting opportunities for manufacturers and suppliers in the commercial vehicle industry.

RESTRAINING FACTORS

Complexity in Operating Advanced Systems and High Cost of Investment May Restrain the Market Growth

As the automobile industry is shifting toward electrification and adopting advanced technology in vehicles, the high cost incurred during production and the complex mechanism in advanced systems will likely hamper the market growth. The manufacturing companies invest a high percentage of research in developing new technologies in freight trucks. The high cost of lithium-ion batteries used in vehicles, installation of software, and high capital investment ultimately increase the vehicles' manufacturing cost.

Advanced driver assistance systems, such as the adaptive cruise control, driver monitoring, park assist, driver drowsiness detection, blind spot detection, and automated emergency braking, consist of sensors, cameras, radars, mapping, and other software systems. These highly technological systems bring many technical challenges and complications with them. As these systems operate on batteries, the constant consumption of battery power may lead to battery disturbances as well as relying on these systems may add a calculated risk of malfunctioning and failures. Also, the electronic components in these systems may malfunction and project incorrect information. Moreover, the high risk of cyber security threats and the complexity faced by the driver in operating the system may cause hazards to the vehicles and the passengers and driver. Any malfunctions or forced and unforced errors in these advanced systems may be dangerous and life-threatening for the users.

Thus, the complex mechanism, high replacement and maintenance costs of these systems, and lack of skilled laborers are likely to restrain the global commercial vehicle market growth.

Commercial Vehicle Market Segmentation Analysis

By Vehicle Type Analysis

Light Commercial Vehicle Segment to Hold the Largest Market Share

Based on vehicle type, the market is segmented into light commercial vehicle, heavy vehicle, and buses. In 2026, the light commercial vehicle segment accounts for a significant share of 67.1% in the global market, owing to its highest usage in logistics operation in a smaller range. It is expected to continue to account for most of the global market. The heavy vehicle segment is also expected to develop exponentially over the forecast period. It is expected to exhibit the highest CAGR (11.8%) during the forecast period. The bus market is also expected to grow exponentially during the forecast period. It is anticipated to exhibit the second-highest CAGR. The rising urban population & their needs and the increasing infrastructure web in developing Asian countries, such as India and China, contribute to the global market growth.

By Fuel Type Analysis

To know how our report can help streamline your business, Speak to Analyst

EV Segment is Anticipated to be the Fastest-Growing Segment Owing to Rising Sale of Electric Mobility in all Vehicle Types

In terms of fuel type, the market is divided into I.C. engine and Electric Vehicle (EV). In 2026, the I.C. engine segment has the highest commercial vehicle market share of 95.43% in the global market. However, the EV segment is predicted to experience promising growth due to the rise in demand, owing to stringent regulations regarding fuel economy standards. Additionally, to increase EV sales, manufacturers are continuously focusing on reducing the price of the battery, propelling the global market growth. Compared to conventional I.C. engines, Commercial EVs produce no noise and air pollution and have a greater driving range. They are also more compatible with autonomous driving. Hence, the EV segment is expected to exhibit the highest CAGR during the forecast period.

REGIONAL INSIGHTS

North America Commercial Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed 59.54% to the global market in 2025, with a valuation of USD 769.46 billion, and is projected to reach USD 834.87 billion in 2026. North America holds the largest position in the market, owing to the growing demand for freight vehicles in North America. This is evident attributed to the fact that according to OICA, North America witnessed a decline of 20.3% in freight vehicle production due to the COVID-19 pandemic. However, there was a surge in new orders as soon as lockdowns were lifted. Also, there was increasing demand for long-distance operations from fleet management in this region. It is estimated that the region will exhibit good growth in the global market. As the demand for personnel and cargo transportation continues to increase, it is expected that this demand will significantly increase in the future.The U.S. market is projected to reach USD 708.62 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 319.29 billion in 2025, capturing 24.70% of global revenue, and is estimated to reach USD 347.23 billion in 2026. The region is likely to dominate the global market as the second-largest automotive hub, owing to increasing vehicle production per year in the region's countries. The growing adoption of vital governmental initiatives, the use of electric vehicles, and autonomous vehicles are likely to promote the development of the market in the region during the forecast period. Countries, such as India and China, heavily invest in infrastructure and the startup ecosystem. This is a boosting factor for the growth of the market in this region. Furthermore, the growth of businesses, such as mining and logistics, in developing countries in this region will propel the development of the market.The Japan market is projected to reach USD 49.96 billion by 2026, the China market is projected to reach USD 178.87 billion by 2026, and the India market is projected to reach USD 28.16 billion by 2026.

Europe

Europe accounted for USD 161.83 billion in 2025, representing 12.52% of the global market share, and is projected to reach USD 174.34 billion in 2026. Europe holds the third position in the global market. The region is expected to grow with a constant CAGR. The switching of fleet operators from fossil fuel-powered trucks to EV-powered vehicles can help propel the growth of the market. According to a survey, in 2018, about 40% of the fleet operators said they would want to include electric or hybrid trucks in their new purchases. In 2021, that number jumped to around 60%, with the fleet operators expecting their fleets to have almost 50% of electric trucks by 2025. By 2030, buyers expect electric freight vehicles to edge out fossil fuel trucks with a 60% market share. Hence, these factors will help propel the growth of the global market.The UK market is projected to reach USD 21.53 billion by 2026, while the Germany market is projected to reach USD 28.03 billion by 2026.

Rest of the World

The Rest of the World region captured 3.24% of the global market in 2025, generating USD 41.84 billion in revenue, and is projected to reach USD 45.44 billion in 2026. In the market, the rest of the world contributes very little compared to other regions, and this is due to fewer automotive OEMs, low adoption of technology, and less presence of all types of vehicles. However, it is expected to grow in the future at a CAGR of 8.6%.

List of Key Companies in Commercial Vehicle Market

Daimler AG is a Top Player in the Market Owing to Strong Geographical Presence and Wide Product Portfolio

Daimler Truck is one of the biggest producers of freight vehicles and the world's biggest manufacturer of premium cars with a footprint across the globe. With more than 40 production facilities worldwide and more than 100,000 staff, the company is one of the major cargo vehicle manufacturers with a global reach. Daimler Truck encompasses seven brands, BharatBenz, Freightliner, Western Star, Mercedes-Benz, Fuso, Setra, and Thomas Built Buses. North America Daimler Trucks's brands include Freightliner and Western Star. Moreover, Daimler Truck has Mercedes-Benz Vans & Cars, Daimler Buses & Trucks, and mobility divisions. The company has headquarters in Germany, Europe, with more than 300,000 employees across the globe.

LIST OF KEY COMPANIES PROFILED:

- Daimler AG (Germany)

- PACCAR Inc. (U.S.)

- Hino (Japan)

- Scania (Sweden)

- Tata Motors (India)

- Navistar International Corp (U.S.)

- BYD Auto Co., Ltd. (China)

- AB Volvo (Sweden)

- Toyota Motor Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

- February 2024 - VE Commercial Vehicles Ltd, a joint venture between Sweden’s Volvo Group and Eicher Motors, entered the small commercial vehicle (SCV) market by launching an electric product in the fast-growing 2-3.5 GVW (gross vehicle weight) pick-up segment market.

- February 2024 - NITI Aayog proposed financial and non-financial incentives along with VAT reduction and accelerated depreciation to encourage the use of LNG-fueled commercial vehicles. They have also suggested setting up a demand aggregator for buying LNG trucks. The aim is to lower carbon dioxide emissions and increase the share of natural gas in the energy mix.

- February 2024 - Tata Motors, along with its authorized distributor, Tata Africa Holdings Limited, launched its successful range of multipurpose smart heavy-duty trucks – Ultra T.9 and Ultra T.14, in South Africa.

- January 2024 - Tata Motors, announced connecting 5 lakh commercial vehicles with Fleet Edge. It is dedicated connected vehicle platform designed specially for efficient commercial vehicle fleet management. Fleet Edge uses smart technologies to increase vehicle uptime and improve road safety, shares action-able insights in real time on vehicle status, health, location, and driver behavior of every vehicle connected to it. This helps enhance operational efficiency, lowering logistics costs and improving profits.

- December 2023 - Scania Commercial Vehicles partnered with the Hyderabad-based PPS Motors, designating them with pan-India coverage sales and service operations for Scania’s mining tippers in India. PPS Motors has established six regional warehouses across India, which has close proximity to the mining sites and strategically connected to Scania’s central warehouse in Nagpur, creating a hub-and-spoke model.

REPORT COVERAGE

The global commercial vehicle market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, vehicle types, and leading product applications. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition, the report encompasses several factors that have contributed to the market's growth.

An Infographic Representation of Commercial Vehicle Market

View Full Infographic

View Full InfographicTo get information on various segments, share your queries with us

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.5% over 2026 to 2034 |

|

Unit |

Value (USD Billion) & Volume (Thousand Units) |

| Segmentation |

By Vehicle Type

|

|

By Fuel Type

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1292.42 billion in 2025 and is projected to reach USD 2328.28 billion by 2034.

In 2025, the North America market size stood at USD 769.46 billion.

The market is projected to grow at a CAGR of 6.5% and will exhibit steady growth during the forecast period (2026-2034).

The light commercial vehicle segment is expected to be the leading segment in this market during the forecast period.

Advancements in infrastructure and industrialization are poised to propel the market expansion.

Daimler AG is the leading player in the global market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us