Polyethylene Market Size, Share & Industry Analysis, By Type (HDPE/MDPE, LDPE, and LLDPE), By End-use Industry (Packaging, Automotive, Infrastructure & Construction, Consumer Goods/Lifestyle, Healthcare & Pharmaceuticals, Electrical & Electronics, Agriculture, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

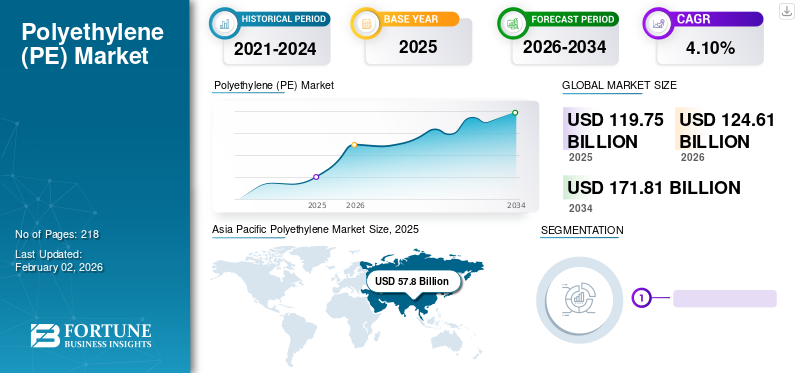

The global polyethylene market size was valued at USD 119.75 billion in 2025 and is projected to grow from USD 124.61 billion in 2026 to USD 171.81 billion by 2034, exhibiting a CAGR of 4.1% during the forecast period. Asia Pacific dominated the polyethylene market with a market share of 48.30% in 2025. Moreover, the polyethylene market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 22.31 billion by 2032, driven by the packaging industry demand, technological innovations, sustainability pressures, and other economic factors.

The properties of polyethylene (PE) make it popular in industries such as packaging and construction. This polymer offers reduced weight, high ductility, good electrical treeing resistance, excellent chemical resistance, and increased impact strength for the products at lower cost. It is majorly used in the form of products such as food wraps, shopping bags, detergent bottles, and automobile fuel tanks, across the globe. For instance, A-Pac Manufacturing Co., Inc. produces bags and Merck KGaA produces BRAND wide-mouth bottles made from this polymer. Moreover, the growing industrialization and rapid growth of the packaging industry are expected to surge market growth during the forecast period.

During the period of COVID-19 pandemic, the polyethylene supply was affected as the demand from industries, such as automotive, electrical & electronics, and consumer goods, declined. Crude oil prices were reduced due to a collapse in demand and excess supply. This resulted in declined product prices and affected the market growth. However, PE experienced high demand from the healthcare and packaging industries. The increasing demand for single-use plastic products, sampling containers, saline bottles, Personal Protective Equipment (PPE), and curtains propelled the polyethylene market growth.

Download Free sample to learn more about this report.

Global Polyethylene Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 119.75 billion

- 2026 Market Size: USD 124.61 billion

- 2034 Forecast Market Size: USD 171.81 billion

- CAGR: 4.1% (2026–2034)

Market Share:

- Asia Pacific dominated with 48.30% market share in 2025

- U.S. polyethylene market projected to reach USD 22.31 billion by 2032

Regional Market Insights:

- Asia Pacific: Largest share in 2023; fastest growth driven by China, India, and industrialization. India’s demand growing at 9% annually.

- Europe: Second largest share; strong demand from automotive and packaging industries.

- North America: Significant growth; U.S. leads due to healthcare, packaging, automotive, and electronics demand.

- Middle East & Africa: Growth driven by packaging and consumer goods sectors amid rising urbanization.

- Latin America: Substantial growth with Brazil as largest market; uses include plastic bags, bottles, and construction materials.

Polyethylene Market Trends

High Demand for Packaging from Food & Beverages and Consumer Goods Industries to Propel Market Progress

Manufacturers prefer PE for the packaging of food, beverages, and consumer goods due to its properties such as resistance to moisture, easy customization, and durability. Polythene is an economical material that acts as an advantage for the purpose of packaging. Easy recyclability, resistance to chemicals, and ability to protect the contained product from any external disturbances have made this polymer an ideal material. It is showcasing a propelling demand from the consumer goods, food, and beverage industries owing to the above-mentioned factors.

Download Free sample to learn more about this report.

Polyethylene Market Growth Factors

Rising Demand from Various End-use Industries to Drive Market Growth

The demand for products is gaining momentum in various industries such as automotive, electrical & electronics, food & beverage, and consumer goods. Properties, such as high rigidity, make it suitable for industrial uses, mainly for packaging automotive and electrical spare parts. In the automotive industry, manufacturers focus on increasing vehicles' efficiency by reducing their weight. PE is preferred as it is light in weight and offers easy processability, sealing, and stiffness properties.

In the food & beverage industry, the consumption of the product is growing at a rapid pace due to the rising demand for the production of packaging materials. Manufacturers prefer effective packaging to reduce the possibility of food contamination and loss of quality. Polyethylene has a moisture barrier property that protects food & beverages from external as well as internal environments. This property is expected to fuel the demand for materials from this industry.

The use of product in fashion apparel, toys, and sports goods is increasing due to ability of the product to resist physical stresses, provide flexibility & durability in packaging, and allow easy molding. In agriculture industry, the application of the product is growing owing to the increasing demand for drippers, microtubes, nozzles, and emitting pipes in irrigation fields.

Rising Product Demand from Infrastructure & Construction, Healthcare, and Pharmaceuticals Industries to Fuel Market Growth

The rising demand for polyethylene in infrastructure & construction and healthcare & pharmaceuticals industries is primarily fueled by its versatility, cost-effectiveness, and durability. In infrastructure and construction, polyethylene is used in various applications, such as pipes, fittings, insulation, and geomembranes due to its resistance to corrosion, chemicals, and moisture, contributing to the longevity and sustainability of projects. In healthcare and pharmaceuticals, polyethylene is essential for packaging materials, medical devices, and drug delivery systems due to its inertness, flexibility, and compatibility with the sterilization process. As global investment in infrastructure development and healthcare infrastructure continues to increase, the demand for polyethylene is expected to grow steadily. Furthermore, ongoing innovations in polyethylene technology, such as enhanced performance grades and recycling capabilities will further drive the product’s use across these sectors.

RESTRAINING FACTORS

Availability of Substitutes Including PU and PET Products to Limit Product Adoption Globally

The availability of substitute products, such as polypropylene and polyethylene terephthalate (PET) poses a threat to the market growth. These types of plastics portray properties similar to polyethylene such as flexibility, impact resistance, chemical resistance, moldability, and low cost, which may hinder the market growth. In addition, the fluctuating prices of raw materials may negatively affect the market growth by affecting the final product's cost structure, thereby restraining the market.

Polyethylene Market Segmentation Analysis

By Type Analysis

HDPE Segment to Hold Highest Revenue Share Stoked by Low Manufacturing Cost

By type, the market is segmented into High-density Polyethylene (HDPE)/Medium-density Polyethylene (MDPE), Low-density Polyethylene (LDPE), and Linear Low-density Polyethylene (LLDPE). Amongst these, The HDPE segment is expected to hold the largest share of the polyethylene market, capturing 47.58% in 2026. owing to its characteristics such as low manufacturing cost, high strength-to-density ratio, and high-temperature resistance. The physical properties of HDPE vary depending on the molding process that is used to manufacture it. HDPE is highly resistant to various types of solvents and has a wide variety of applications such as bottle caps, ballistic plates, food storage containers, boats, chemical-resistant piping, and others.

LDPE is mainly used for packaging due to its chemical resistance, flexibility, and softness. It is majorly used in the food industry for the packaging industry. The rising demand for lightweight packaging in electronics, healthcare, and food & beverages is further surging the demand for LDPE in the market.

LLDPE is produced by copolymerizing ethylene with butene and small amounts of hexene and octene, using Ziegler-Natta catalyst, and has a structure similar to that of LDPE. The former is used to produce a wide range of products. It is usually processed unaccompanied or blended with LDPE and HDPE. Its properties can be altered by varying the type and amount of chemicals. The properties of LLDPE, such as high tensile strength, high impact resistance, and flexibility, make it suitable for packaging, agriculture, healthcare, and construction industries.

By End-use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Packaging Segment to Lead Backed by Rising Demand from Food & Beverages Industry

Based on end-use industry, the market is categorized into packaging, automotive, infrastructure & construction, consumer goods/lifestyle, healthcare & pharmaceuticals, electrical & electronics, agriculture, and others. Amongst these, The packaging segment is expected to dominate the product market, capturing a share of 55.32% in 2026. and is the fastest growing segment throughout the forecast period owing to its increasing in the manufacturing of several packaging solutions for food & beverage industry. According to the Flexible Packaging Association, the food & beverage industry accounts for over 60% of the flexible packaging market.

The infrastructure & construction segment is considered the second most prominent segment in the end-use industry. The increasing use of the product in manufacturing various construction materials, such as films and sheets, for windows, flooring, countertop, roofing, cover building materials, and seal-off rooms is expected to surge its demand in this industry.

Similarly, the consumer goods/lifestyle industry is expected to enhance PE sales during the forecast period due to increased demand for fashion apparel, housewares, ice boxes, sports goods, and toys from various regions. Properties, such as high durability, easy moldability, and flexibility, will support manufacturing the above-mentioned products.

REGIONAL INSIGHTS

Asia Pacific Polyethylene Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 57.8 billion in 2025 and is projected to reach USD 60.4 billion in 2026. and is expected to grow at the highest growth rate throughout the forecast period due to the region's leading consuming countries such as China and India. According to Plastivision, the demand for product would grow at a rate of 9.0% by 2023 in India. Its increasing demand from industries, such as packaging and infrastructure & construction, coupled with rapid industrialization, is driving the market growth in this country. The Japan market is projected to reach USD 5.69 billion by 2026, the China market is projected to reach USD 28.86 billion by 2026, and the India market is projected to reach USD 6.16 billion by 2026.

Europe

Europe contributed approximately USD 25.5 billion to the global market in 2025, accounting for 21.30% share, and is expected to reach USD 26.4 billion in 2026. Europe accounted for the second-largest share in the global market. The increasing demand for plastic products from the automotive industry is expected to contribute to the high market revenue in the region. Polyethylene is the most preferred polymer among others used in Europe due to its properties such as electric insulation, corrosion inhibition, good heat resistance, and low density. The UK market is projected to reach USD 1.84 billion by 2026, while the Germany market is projected to reach USD 7.07 billion by 2026.

North America

The market in North America reached USD 19.5 billion in 2025, representing 16.30% of total market revenue, and is projected to reach USD 20.2 billion in 2026. On the other hand, North America is projected to showcase significant growth in the global market. The U.S. accounted for the largest share due to high demand for this polymer from healthcare & pharmaceuticals, electrical & electronics, packaging, and automotive industries. Also, the rising demand for consumer goods and the increasing development of this region's electrical & electronics, automotive, and medical industries would augment market growth. The U.S. market is projected to reach USD 17.84 billion by 2026.

Rest of the world

In the Middle East & Africa, increasing demand from the packaging and consumer goods industries is one of the major factors influencing growth. The rising demand for safe and viable packaging, increasing urbanization, and the surging number of packaging companies are some of the factors expected to boost the market growth in this region. Latin America is expected to observe substantial growth in the market. Brazil is the largest country in this region. Owing to its characteristics, such as high strength and durability, the material is used in numerous applications consisting of plastic bags, bottles, and construction materials in the region.

Middle East & Africa maintained a strong presence in the global market, reaching USD 9.62 billion in 2025, accounting for 8.00% share, and is expected to reach USD 10.04 billion in 2026.

The Latin America market accounted for USD 7.3 billion in 2025, representing 6.10% of the global industry, and is expected to reach USD 7.6 billion in 2026.

List of Key Companies in Polyethylene Market

Companies Implemented Business Expansion and Acquisition Strategies to Retain their Market Share

The major companies are present throughout the globe. Among these companies, LyondellBasell deals with the plastics, chemicals, and refining sectors. It offers a wide range of products. The company has adopted acquisition and expansion strategies to increase its presence in the market. ExxonMobil, on the other hand, is expanding throughout the globe by using strategies, such as joint ventures and acquisitions, by providing a diversified range of polymer products. Besides, SABIC has a strong influence in the Middle East & Africa and it provides numerous grades of polymer products. The company adopted the strategy of a joint venture to increase gain competence in the market.

LIST OF KEY COMPANIES PROFILED:

- LyondellBasell Industries N.V. (Netherlands)

- ExxonMobil Chemical (U.S.)

- SABIC (Saudi Arabia)

- Reliance Industries Limited (India)

- INEOS (U.K.)

- China National Petroleum Corporation (China)

- China Petroleum & Chemical Corporation (China)

- Ducor Petrochemicals (Netherlands)

- Formosa Plastic Group (Taiwan)

- Braskem (Brazil)

- Repsol (Spain)

- Borouge (UAE)

- Borealis AG (Austria)

- MOL Group (Hungary)

KEY INDUSTRY DEVELOPMENTS:

- November 2023: NOVA Chemicals Corporation and Amcor announced the signing of a Memorandum of Understanding (MoU) for mechanically recycled polyethylene. As per the agreement, NOVA Chemicals Corporation, the leading producer of polyethylene, would supply mechanically recycled polyethylene to Amcor, a prominent global packaging solutions manufacturer.

- February 2023: LyondellBasell and KIRKBI A/S signed an agreement for investing in APK, specialized in a solvent-based recycling technology for LDPE. By signing the agreement, LyondellBasell and KIRKBI A/S became the minority shareholders of APK.

- April 2022: ExxonMobil launched Exceed S performance PE resins that offer stiffness and toughness properties while being easy to process. The new PE platform will help the company to offer lucrative opportunities to decrease the complexity of film designs and formulations while improving conversion efficiency, film performance, and packaging durability versus current market references.

- August 2021: Braskem launched HD1954M, a high-density PE, which provides a combination of excellent impact strength, high rigidity, and Environmental Stress Cracking (ESCR), rendering packaging optimization and productivity gains. The launch will help the company to meet the demands from the agrochemical and chemical markets.

- December 2020: INEOS acquired the remaining 50% interest in the Gemini HDPE joint venture from Sasol Chemicals. The acquisition increased the group’s interest in Gemini to 100%.

- September 2020: INEOS Olefins & Polymers Europe announced the expansion of the Recycl-IN range of products. Through this partnership, INEOS Olefins & Polymers could develop high-performance polyethylene Recycl-IN resins, which meet the needs of converters, brand owners, and retailers in using more than 60% recycled plastics in demanding applications, such as stretch and lamination films, particularly used in flexible pouches for personal care product and detergents.

- June 2020: Thong Guan and Dow Chemicals collaborated to launch a bio-based polyethylene product series. The PE film will be targeted to meet the increasing demand for plastic films in the Asia Pacific.

REPORT COVERAGE

An Infographic Representation of Polyethylene (PE) Market

Market")

View Full Infographic

View Full InfographicTo get information on various segments, share your queries with us

The research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, types, end-use industry, and products. Also, it provides quantitative data regarding volume and value, market analysis, research methodology for market data, and insights into industry trends. It highlights vital industry developments and competitive landscape. In addition, the report encompasses various factors that have contributed to the growth of the market in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.1% from 2026 to 2034 |

|

Unit |

Value (USD Billion); Volume (Million Ton) |

|

Segmentation |

By Type

|

|

By End-use Industry

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 119.75 billion in 2025 and is projected to reach USD 171.81 billion by 2034.

In 2025, the market value stood at USD 119.75 billion.

Registering a significant CAGR of 4.1%, the market will exhibit considerable growth in the forecast period (2026-2034).

The packaging segment is expected to lead the market during the forecast period.

Rising product demand from various end-use industries, including automotive and electrical & electronics, is expected to fuel the market growth.

China held the highest share in the market in 2025.

LyondellBasell Industries N.V., ExxonMobil Chemical, and China National Petroleum Corporation are the leading players in the market.

The rapid growth in the food & beverages industry and growing technological advancements are anticipated to boost the consumption of the product.

- 2021-2034

- 2025

- 2021-2024

- 218

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us