Polyethylene Market Size, Share & Industry Analysis, By Type (HDPE/MDPE, LDPE, and LLDPE), By End-use Industry (Packaging, Automotive, Infrastructure & Construction, Consumer Goods/Lifestyle, Healthcare & Pharmaceuticals, Electrical & Electronics, Agriculture, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

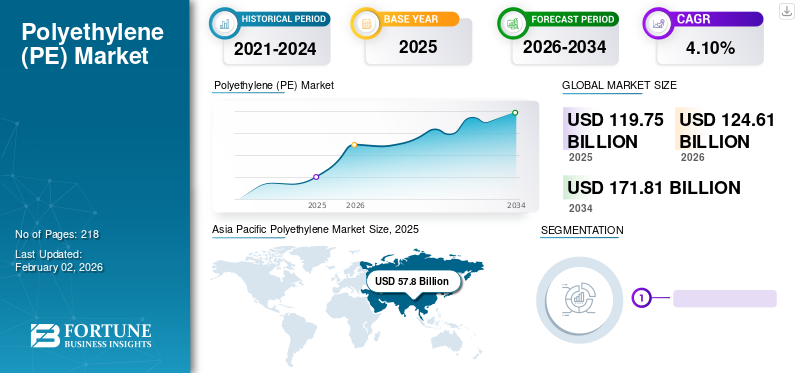

- The polyethylene (PE) market to grow from $124.61 billion in 2026 to $171.81 billion by 2034, reflecting a compound annual growth rate (CAGR) of 4.1% during the forecast period.

- Adoption of polyethylene is likely to accelerate with increasing demand from the packaging, automotive, healthcare & pharmaceuticals, electrical & electronics, and consumer goods industries, supported by its versatility and low manufacturing cost.

- Although sustainability pressures and the availability of substitutes such as PET and polypropylene present challenges, polyethylene continues to remain one of the most widely used polymers across a broad range of applications.

- Asia Pacific currently leads the polyethylene market, accounting for 48.3% of global market share in 2025, supported by strong industrial activity and growing demand across key end-use sectors.

The global polyethylene market size was valued at USD 119.75 billion in 2025 and is projected to grow from USD 124.61 billion in 2026 to USD 171.81 billion by 2034, exhibiting a CAGR of 4.1% during the forecast period. Asia Pacific dominated the polyethylene market with a market share of 48.30% in 2025. Moreover, the polyethylene market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 22.31 billion by 2032, driven by the packaging industry demand, technological innovations, sustainability pressures, and other economic factors.

The global polyethylene market remains one of the largest and most strategically important segments within the petrochemical industry, supported by its extensive use across packaging, infrastructure, automotive, healthcare, agriculture, and consumer products. Market dynamics increasingly reflect feedstock economics, sustainability requirements, and shifts in downstream manufacturing patterns rather than simple volume expansion. Polyethylene market growth remains closely tied to industrial activity, consumer spending, urbanization, and investments in logistics and construction infrastructure. Resin producers increasingly focus on portfolio optimization and circularity initiatives to maintain long-term competitiveness.

Packaging applications continue to represent the dominant source of polyethylene market size due to rising demand for flexible films, rigid containers, and e-commerce-related protective materials. High-density polyethylene (HDPE), low-density polyethylene (LDPE), and linear low-density polyethylene (LLDPE) demonstrate distinct consumption patterns because performance requirements vary considerably across end-use sectors. Demand visibility remains strongest in packaging and infrastructure applications, where material durability, processability, and cost efficiency continue influencing procurement decisions.

Supply-side dynamics increasingly reflect regional feedstock advantages and capacity expansion strategies. Producers with access to low-cost ethane feedstocks maintain structural cost advantages, while naphtha-based manufacturers continue emphasizing product differentiation and specialty grades. Capacity additions across North America, China, and the Middle East continue to reshape trade flows and competitive positioning within the polyethylene industry. Utilization rates and operating margins remain sensitive to crude oil prices, ethylene spreads, and downstream demand cycles.

The properties of polyethylene (PE) make it popular in industries such as packaging and construction. This polymer offers reduced weight, high ductility, good electrical treeing resistance, excellent chemical resistance, and increased impact strength for the products at a lower cost. It is mainly used in the form of products such as food wraps, shopping bags, detergent bottles, and automobile fuel tanks, across the globe. For instance, A-Pac Manufacturing Co., Inc. produces bags, and Merck KGaA produces BRAND wide-mouth bottles made from this polymer. Moreover, the growing industrialization and rapid growth of the packaging industry are expected to surge market growth during the forecast period.

During the period of the COVID-19 pandemic, the polyethylene supply was affected as the demand from industries, such as automotive, electrical & electronics, and consumer goods, declined. Crude oil prices were reduced due to a collapse in demand and excess supply. This resulted in declining product prices and affected the market growth. However, PE experienced high demand from the healthcare and packaging industries. The increasing demand for single-use plastic products, sampling containers, saline bottles, Personal Protective Equipment (PPE), and curtains propelled the polyethylene market growth.

Download Free sample to learn more about this report.

Polyethylene MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 119.75 billion

- 2026 Market Size: USD 124.61 billion

- 2034 Forecast Market Size: USD 171.81 billion

- CAGR: 4.1% from 2026–2034

- Asia Pacific dominated the polyethylene market with a 48.30% share in 2025.

- HDPE/MDPE is expected to lead the market with a 47.58% share in 2026.

- Packaging is projected to account for 55.32% of the market in 2026.

North American

Reached USD 19.5 billion in 2025 and is projected to grow to USD 20.2 billion in 2026, driven by packaging, healthcare, and petrochemical infrastructure.

Europe

Accounted for USD 25.5 billion in 2025 and is expected to reach USD 26.4 billion in 2026, supported by automotive demand and sustainability initiatives.

Asia Pacific

Held USD 57.8 billion in 2025 and is projected to reach USD 60.4 billion in 2026, driven by strong demand from China and India.

U.S.

The market is projected to reach USD 17.84 billion by 2026, supported by strong demand from packaging, healthcare, automotive, and electronics industries.

Japan

The market is projected to reach USD 5.69 billion by 2026, driven by advanced manufacturing and specialty polyethylene applications.

Read More

Market Trends:

High Demand for Packaging from Food & Beverages and Consumer Goods Industries to Propel Market Progress

Manufacturers prefer PE for the packaging of food, beverages, and consumer goods due to its properties such as resistance to moisture, easy customization, and durability. Polythene is an economical material that acts as an advantage for the purpose of packaging. Easy recyclability, resistance to chemicals, and the ability to protect the contained product from any external disturbances have made this polymer an ideal material. It is showcasing a propelling demand from the consumer goods, food, and beverage industries owing to the above-mentioned factors.

Circular economy considerations increasingly influence polyethylene market trends and investment priorities throughout the value chain. Consumer brands, converters, and resin producers continue expanding commitments related to recycled content and packaging sustainability. Mechanical recycling remains commercially dominant, while chemical recycling technologies attract growing capital allocation because they offer pathways for processing mixed or difficult-to-recycle waste streams.

Portfolio differentiation has become increasingly important as commodity margins fluctuate. Producers are allocating greater resources toward specialty grades and application-specific formulations capable of delivering improved performance and pricing resilience. Product development strategies increasingly emphasize downgauging, enhanced processability, and compatibility with recycled materials.

Trade flows are also evolving. Regional self-sufficiency initiatives and capacity expansion programs in China continue to reshape import patterns and alter competitive dynamics. Middle Eastern producers increasingly leverage feedstock advantages and logistics capabilities to strengthen export positions across Asia and Europe.

Digitalization and operational optimization continue to affect manufacturing economics. Advanced analytics, predictive maintenance, and process automation increasingly support higher plant

Download Free sample to learn more about this report.

Key Market Dynamics

Market Drivers:

Rising Demand from Various End-use Industries to Drive Market Growth

The demand for products is gaining momentum in various industries such as automotive, electrical & electronics, food & beverage, and consumer goods. Properties such as high rigidity make it suitable for industrial use, mainly for packaging automotive and electrical spare parts. In the automotive industry, manufacturers focus on increasing vehicles' efficiency by reducing their weight. PE is preferred as it is light in weight and offers easy processability, sealing, and stiffness properties.

In the food & beverage industry, the consumption of the product is growing at a rapid pace due to the rising demand for the production of packaging materials. Manufacturers prefer effective packaging to reduce the possibility of food contamination and loss of quality. Polyethylene has a moisture barrier property that protects food & beverages from external as well as internal environments. This property is expected to fuel the demand for materials from this industry.

The use of the product in fashion apparel, toys, and sports goods is increasing due to the ability of the product to resist physical stresses, provide flexibility & durability in packaging, and allow easy molding. In agriculture industry, the application of the product is growing owing to the increasing demand for drippers, microtubes, nozzles, and emitting pipes in irrigation fields.

Rising Product Demand from Infrastructure & Construction, Healthcare, and Pharmaceuticals Industries to Fuel Market Growth

The rising demand for polyethylene in infrastructure & construction and healthcare & pharmaceuticals industries is primarily fueled by its versatility, cost-effectiveness, and durability. In infrastructure and construction, polyethylene is used in various applications, such as pipes, fittings, insulation, and geomembranes, due to its resistance to corrosion, chemicals, and moisture, contributing to the longevity and sustainability of projects. In healthcare and pharmaceuticals, polyethylene is essential for packaging materials, medical devices, and drug delivery systems due to its inertness, flexibility, and compatibility with the sterilization process.

As global investment in infrastructure development and healthcare infrastructure continues to increase, the demand for polyethylene is expected to grow steadily. Furthermore, ongoing innovations in polyethylene technology, such as enhanced performance grades and recycling capabilities, will further drive the product’s use across these sectors.

Consumption growth across packaging, infrastructure, and consumer manufacturing continues providing structural support for the polyethylene market. Flexible packaging demand remains particularly resilient because food preservation requirements, e-commerce expansion, and logistics optimization increasingly favor lightweight polymer solutions. Brand owners and converters continue prioritizing polyethylene grades that balance mechanical performance with cost efficiency, supporting sustained resin consumption across developed and emerging economies.

Urbanization and infrastructure investment represent additional sources of polyethylene market growth. Water distribution systems, gas pipelines, insulation materials, and construction membranes increasingly rely on high-density polyethylene because durability and chemical resistance remain important operational requirements. Population growth and industrialization across the Asia-Pacific, the Middle East, and selected African economies continue to support long-term infrastructure-related demand.

Market Restraints:

Availability of Substitutes, Including PU and PET Products, to Limit Product Adoption Globally

The availability of substitute products, such as polypropylene and polyethylene terephthalate (PET), poses a threat to the market growth. These types of plastics portray properties similar to polyethylene, such as flexibility, impact resistance, chemical resistance, moldability, and low cost, which may hinder the market growth. In addition, the fluctuating prices of raw materials may negatively affect the market growth by affecting the final product's cost structure, thereby restraining the market.

Environmental scrutiny remains one of the most significant constraints affecting the polyethylene market. Regulatory initiatives targeting single-use plastics, extended producer responsibility frameworks, and waste reduction policies increasingly influence resin consumption patterns across packaging applications. Brand owners and downstream converters face growing pressure to improve recyclability and reduce virgin polymer dependence, creating uncertainty around long-term product mix evolution.

Margin volatility represents another structural challenge. Polyethylene producers remain highly exposed to fluctuations in crude oil prices, natural gas liquids, and ethylene feedstock spreads. Changes in energy costs frequently influence profitability and operating rates, particularly for naphtha-based producers competing against regions benefiting from lower-cost ethane feedstocks.

Oversupply risk also affects industry economics. Large-scale capacity additions in China, North America, and the Middle East periodically create temporary imbalances between production and downstream consumption. Such conditions may compress margins and intensify price competition, particularly in commodity-grade polyethylene segments.

Market Opportunities:

Packaging transformation presents one of the largest opportunities within the polyethylene market. Demand for lightweight, flexible, and recyclable packaging formats continues to expand as food producers, logistics operators, and consumer brands prioritize material efficiency and supply chain optimization. Advanced polyethylene grades designed for mono-material packaging structures increasingly support recycling compatibility and sustainability objectives.

Infrastructure modernization provides another favorable growth avenue. Expanding investments in water management, gas distribution, telecommunications, and energy networks continue to support demand for high-performance polyethylene pipes and construction materials. Emerging economies undergoing rapid urbanization offer particularly attractive opportunities for long-term consumption growth.

Healthcare and pharmaceutical manufacturing create higher-value opportunities for specialized polyethylene grades. Stringent quality requirements, rising healthcare expenditure, and increasing demand for sterile packaging solutions continue to strengthen market visibility for medical applications. Producers capable of meeting regulatory and purity standards may benefit from premium pricing environments.

Circularity initiatives also represent an important strategic opportunity. Investment in recycling technologies, waste collection systems, and recycled polyethylene integration allows companies to strengthen customer relationships and improve regulatory positioning. Collaboration across the value chain increasingly enhances commercial viability.

Polyethylene Market Segmentation Analysis

By Type Analysis

By type, the market is segmented into High-density Polyethylene (HDPE)/Medium-density Polyethylene (MDPE), Low-density Polyethylene (LDPE), and Linear Low-density Polyethylene (LLDPE).

HDPE Segment to Hold Highest Revenue Share Stoked by Low Manufacturing Cost

HDPE/MDPE

The HDPE segment is expected to hold the largest share of the polyethylene market, capturing 47.58% in 2026, owing to its characteristics such as low manufacturing cost, high strength-to-density ratio, and high-temperature resistance. The physical properties of HDPE vary depending on the molding process that is used to manufacture it. HDPE is highly resistant to various types of solvents and has a wide variety of applications, such as bottle caps, ballistic plates, food storage containers, boats, chemical-resistant piping, and others.

Structural performance requirements continue to support strong demand for high-density polyethylene (HDPE) and medium-density polyethylene (MDPE) grades across industrial and infrastructure applications. Their combination of strength, impact resistance, and chemical stability makes these materials particularly suitable for pressure pipes, rigid packaging, industrial containers, and fuel tanks. Procurement decisions frequently prioritize lifecycle durability and operational reliability rather than material cost alone.

Infrastructure spending represents a major demand catalyst for HDPE and MDPE consumption. Water transmission networks, gas distribution systems, and telecommunications ducting increasingly rely on polyethylene pipe solutions because corrosion resistance and service life remain important considerations. Urbanization and utility expansion projects across developing economies continue to support long-term consumption visibility.

LDPE

LDPE is mainly used for packaging due to its chemical resistance, flexibility, and softness. It is mainly used in the food industry for packaging. The rising demand for lightweight packaging in electronics, healthcare, and food & beverages is further surging the demand for LDPE in the market.

Processing flexibility and optical properties remain central factors supporting low-density polyethylene (LDPE) demand. Film producers and packaging converters frequently utilize LDPE because softness, transparency, and sealability enable efficient manufacturing across a wide range of consumer and industrial products. Market demand increasingly reflects the need for lightweight packaging solutions that improve logistics economics and reduce material consumption.

Food packaging applications account for a substantial share of LDPE consumption. Protective films, bread bags, squeeze bottles, and shrink wraps rely on the material's ability to provide moisture resistance and processing consistency. Packaging companies continue emphasizing downgauging strategies, encouraging the adoption of grades capable of maintaining performance with lower material intensity.

LLDPE

LLDPE is produced by copolymerizing ethylene with butene and small amounts of hexene and octene, using Ziegler-Natta catalyst, and has a structure similar to that of LDPE. The former is used to produce a wide range of products. It is usually processed unaccompanied or blended with LDPE and HDPE. Its properties can be altered by varying the type and amount of chemicals. The properties of LLDPE, such as high tensile strength, high impact resistance, and flexibility, make it suitable for packaging, agriculture, healthcare, and construction industries.

Demand for linear low-density polyethylene (LLDPE) increasingly reflects changing packaging requirements and efficiency-focused manufacturing practices. Film applications benefit from superior tensile strength and puncture resistance, allowing converters to reduce thickness while preserving functionality. Such characteristics improve cost efficiency and support broader sustainability objectives.

Flexible packaging remains the primary outlet for LLDPE consumption. Stretch films, industrial liners, agricultural covers, and heavy-duty sacks frequently depend on the material because load stability and durability remain critical operational requirements. Rapid expansion of e-commerce logistics and food distribution systems continues to strengthen consumption across these applications.

Producers increasingly prioritize advanced LLDPE formulations capable of supporting mono-material packaging structures. These developments enhance recycling compatibility and align with circular economy objectives pursued by consumer brands and regulators. Product differentiation has therefore become increasingly important within this segment.

By End-use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Based on end-use industry, the market is categorized into packaging, automotive, infrastructure & construction, consumer goods/lifestyle, healthcare & pharmaceuticals, electrical & electronics, agriculture, and others.

Packaging Segment to Lead Backed by Rising Demand from the Food & Beverages Industry

Packaging

The packaging segment is expected to dominate the product market, capturing a share of 55.32% in 2026. and is the fastest growing segment throughout the forecast period, owing to its increasing demand in the manufacturing of several packaging solutions for the food & beverage industry. According to the Flexible Packaging Association, the food & beverage industry accounts for over 60% of the flexible packaging market.

No other downstream sector exerts a greater influence on the polyethylene market than packaging, which accounts for the largest share of global resin consumption. Demand patterns are shaped by food preservation requirements, transportation efficiency, shelf-life extension, and the rapid expansion of e-commerce channels. Polyethylene remains deeply embedded within flexible and rigid packaging systems because converters value its processability, sealing characteristics, and cost competitiveness.

Flexible packaging formats represent a particularly important growth area. Stand-up pouches, protective films, stretch wraps, and multilayer structures increasingly depend on polyethylene grades capable of delivering durability while reducing material intensity. Brand owners are simultaneously pursuing sustainability targets, prompting greater emphasis on mono-material structures and recyclable packaging solutions.

Changing consumer preferences are also influencing procurement behavior. Convenience-oriented packaging formats, smaller product sizes, and increasing online retail activity continue supporting demand for protective and lightweight materials. Emerging markets exhibit particularly strong consumption potential because packaged food penetration and organized retail infrastructure continue expanding.

Infrastructure & Construction

The infrastructure & construction segment is considered the second most prominent segment in the end-use industry. The increasing use of the product in manufacturing various construction materials, such as films and sheets, for windows, flooring, countertops, roofing, covering building materials, and sealing off rooms is expected to surge its demand in this industry.

Infrastructure investment continues to provide structural support for polyethylene consumption across both mature and developing economies. Utility modernization programs, urban expansion, and industrial development projects increasingly require materials capable of delivering long service life under demanding environmental conditions. Polyethylene solutions are widely adopted because corrosion resistance and installation efficiency remain important considerations.

Pipe systems represent the largest area of demand within this segment. Water distribution networks, sewage systems, natural gas pipelines, and telecommunications infrastructure frequently rely on HDPE and MDPE grades because lifecycle costs compare favorably with traditional materials. Municipal authorities increasingly prioritize reliability and maintenance efficiency when evaluating procurement strategies.

Construction applications extend beyond piping systems. Geomembranes, insulation materials, vapor barriers, and protective films continue to support consumption across residential and commercial projects. Industrial facilities also depend on polyethylene components to improve durability and reduce maintenance requirements.

Consumer Goods/Lifestyle

The consumer goods/lifestyle industry is expected to enhance PE sales during the forecast period due to increased demand for fashion apparel, housewares, ice boxes, sports goods, and toys from various regions. Properties, such as high durability, easy moldability, and flexibility, will support manufacturing the above-mentioned products.

Lifestyle changes and evolving consumption behavior continue supporting polyethylene usage across numerous consumer product categories. Household containers, toys, storage solutions, sporting goods, furniture components, and personal care packaging increasingly rely on polyethylene because processing versatility and affordability support mass-market manufacturing strategies.

Product manufacturers frequently prioritize materials capable of balancing appearance, durability, and production efficiency. Polyethylene grades provide flexibility in design and allow producers to maintain competitive pricing while meeting quality expectations. Demand patterns within this segment are closely linked to disposable income levels and retail activity.

Premiumization trends are gradually influencing material requirements. Consumers increasingly favor products demonstrating improved functionality and sustainability attributes. As a result, manufacturers are exploring recycled polyethylene integration and lightweight product architectures to strengthen environmental positioning.

Healthcare & Pharmaceuticals

Stringent quality requirements and expanding healthcare expenditure continue to reinforce polyethylene consumption across medical and pharmaceutical applications. Material purity, chemical resistance, and sterilization compatibility make polyethylene indispensable for products where regulatory compliance and patient safety represent non-negotiable priorities. Demand visibility within this segment benefits from relatively defensive healthcare spending patterns and rising pharmaceutical production capacity.

Medical packaging constitutes one of the largest application areas. Bottles, blister pack components, closures, intravenous containers, and sterile barrier systems increasingly utilize specialized polyethylene grades capable of preserving product integrity throughout storage and transportation. Regulatory agencies and pharmaceutical manufacturers place considerable emphasis on contamination prevention and traceability, favoring suppliers with strong quality assurance capabilities.

Electrical & Electronics

Rapid digitalization and rising electrification requirements continue to support polyethylene consumption across the electrical and electronics industries. Reliability, insulation performance, and moisture resistance remain essential considerations, making polyethylene an important material for cable systems, protective coatings, and electronic components. Procurement strategies increasingly prioritize long-term performance and manufacturing efficiency rather than solely focusing on material costs.

Wire and cable applications account for a substantial share of demand. Telecommunications infrastructure, renewable energy installations, and electric vehicle charging networks increasingly require insulation materials capable of maintaining operational stability under varying environmental conditions. Polyethylene grades possessing excellent dielectric properties continue to benefit from these structural shifts.

Agriculture

Agricultural productivity requirements increasingly influence polyethylene demand, particularly in regions confronting water scarcity and changing climatic conditions. Farmers and agribusiness operators continue adopting polymer-based solutions to improve crop yields, enhance resource efficiency, and reduce operational losses. Material selection frequently reflects durability, weather resistance, and economic viability under demanding outdoor conditions.

Film applications dominate agricultural consumption. Greenhouse covers, silage wraps, mulch films, and protective sheets rely heavily on polyethylene because flexibility and environmental resistance support year-round agricultural operations. Controlled-environment farming and precision agriculture practices are further expanding material requirements across commercial farming systems.

REGIONAL INSIGHTS

Asia Pacific Polyethylene Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific Polyethylene Market Analysis:

Asia Pacific dominated the market with a valuation of USD 57.8 billion in 2025 and is projected to reach USD 60.4 billion in 2026. and is expected to grow at the highest growth rate throughout the forecast period due to the region's leading consuming countries, such as China and India.

According to Plastivision, the demand for the product would grow at a rate of 9.0% by 2023 in India. Its increasing demand from industries, such as packaging and infrastructure & construction, coupled with rapid industrialization, is driving the market growth in this country. The Japan market is projected to reach USD 5.69 billion by 2026, the China market is projected to reach USD 28.86 billion by 2026, and the India market is projected to reach USD 6.16 billion by 2026.

Industrial expansion and urbanization continue to position Asia-Pacific as the largest regional contributor to the polyethylene market. Packaging, infrastructure, automotive manufacturing, and consumer goods sectors collectively support substantial resin demand. China, India, Japan, and Southeast Asia remain key consumption centers. Rising middle-class populations and manufacturing investments continue to accelerate polyethylene market growth across the region.

Japan Polyethylene Market:

Technology-driven manufacturing and stringent quality standards characterize Japan's polyethylene market. Electrical components, healthcare products, and packaging applications account for significant consumption. Producers increasingly prioritize specialty materials and circular economy initiatives to address environmental requirements. Stable industrial demand and advanced processing capabilities continue to support polyethylene market share despite relatively mature end-use industries.

China Polyethylene Market:

China occupies a dominant position within the polyethylene market because of its vast manufacturing ecosystem and expanding downstream industries. Packaging, infrastructure, electronics, and consumer products drive substantial consumption volumes. Capacity additions and self-sufficiency initiatives continue to reshape regional trade flows. Urbanization, industrial upgrading, and domestic demand expansion continue to strengthen polyethylene market growth prospects.

Europe Polyethylene Market Analysis:

Europe contributed approximately USD 25.5 billion to the global market in 2025, accounting for 21.30% share, and is expected to reach USD 26.4 billion in 2026. Europe accounted for the second-largest share in the global market. The increasing demand for plastic products from the automotive industry is expected to contribute to the high market revenue in the region.

Polyethylene is the most preferred polymer among others used in Europe due to its properties such as electric insulation, corrosion inhibition, good heat resistance, and low density. The UK market is projected to reach USD 1.84 billion by 2026, while the German market is projected to reach USD 7.07 billion by 2026.

Regulatory priorities and sustainability objectives increasingly shape the European polyethylene market. Packaging recyclability targets, extended producer responsibility frameworks, and carbon reduction initiatives continue influencing procurement strategies. Producers emphasize specialty grades and recycled material integration to preserve competitiveness. Demand from healthcare, consumer products, and industrial applications supports market stability despite relatively mature consumption patterns.

Germany Polyethylene Market:

Manufacturing intensity and engineering expertise continue to support Germany's role within the polyethylene market. Automotive production, industrial packaging, and infrastructure investments represent important demand sources. Producers increasingly focus on resource efficiency and recycled material utilization to address regulatory expectations. Advanced conversion technologies and strong downstream industries continue contributing to polyethylene market growth across the country.

United Kingdom Polyethylene Market:

Packaging demand and consumer goods manufacturing remain central to the United Kingdom's polyethylene market. Sustainability regulations and corporate circularity commitments increasingly influence resin selection and recycling investments. Imports continue playing an important role in balancing domestic requirements. Healthcare applications, food packaging demand, and infrastructure upgrades collectively support long-term polyethylene market development.

North America Polyethylene Market Analysis:

The market in North America reached USD 19.5 billion in 2025, representing 16.30% of total market revenue, and is projected to reach USD 20.2 billion in 2026. On the other hand, North America is projected to showcase significant growth in the global market.

The U.S. accounted for the largest share due to high demand for this polymer from healthcare & pharmaceuticals, electrical & electronics, packaging, and automotive industries. Also, the rising demand for consumer goods and the increasing development of this region's electrical & electronics, automotive, and medical industries would augment market growth. The U.S. market is projected to reach USD 17.84 billion by 2026.

Feedstock availability and integrated petrochemical infrastructure continue to underpin North America's position within the polyethylene market. Ethane-based production economics provide cost advantages that support export competitiveness and capacity utilization. Packaging, healthcare, and construction applications remain major demand centers. Investments in recycling capabilities, logistics infrastructure, and specialty resin development continue to strengthen polyethylene market growth across the region.

United States Polyethylene Market:

The United States represents a leading contributor to the polyethylene market because abundant shale-derived feedstocks support globally competitive production costs. Packaging applications account for a substantial share of domestic consumption, while export activity remains strategically important. Capacity expansions, advanced manufacturing capabilities, and increasing investment in circular economy initiatives continue to reinforce the polyethylene market size and international market positioning.

The rest of the world

In the Middle East & Africa, increasing demand from the packaging and consumer goods industries is one of the major factors influencing growth. The rising demand for safe and viable packaging, increasing urbanization, and the surging number of packaging companies are some of the factors expected to boost the market growth in this region.

Latin America is expected to observe substantial growth in the market. Brazil is the largest country in this region. Owing to its characteristics, such as high strength and durability, the material is used in numerous applications, consisting of plastic bags, bottles, and construction materials in the region. The Latin America market accounted for USD 7.3 billion in 2025, representing 6.10% of the global industry, and is expected to reach USD 7.6 billion in 2026.

Economic development and expanding consumer industries continue supporting polyethylene demand across Latin America. Packaging applications represent the largest consumption category, followed by agriculture and construction. Infrastructure improvements and growing urban populations contribute to long-term demand visibility. Investments in petrochemical capacity and logistics networks continue to enhance polyethylene market growth throughout the region.

Middle East & Africa maintained a strong presence in the global market, reaching USD 9.62 billion in 2025, accounting for 8.00% share, and is expected to reach USD 10.04 billion in 2026. Feedstock advantages and ongoing petrochemical investments continue strengthening the Middle East & Africa polyethylene market. Export-oriented production remains strategically important, while infrastructure development supports domestic consumption. Packaging, agriculture, and construction applications represent major demand sources. Capacity expansions and improving industrial capabilities continue to support long-term polyethylene market growth.

Polyethylene Industry Competitive Landscape

Companies Implemented Business Expansion and Acquisition Strategies to Retain their Market Share

The major companies are present throughout the globe. Among these companies, LyondellBasell deals with the plastics, chemicals, and refining sectors. It offers a wide range of products. The company has adopted acquisition and expansion strategies to increase its presence in the market. ExxonMobil, on the other hand, is expanding throughout the globe by using strategies such as joint ventures and acquisitions and by providing a diversified range of polymer products. Besides, SABIC has a strong influence in the Middle East & Africa, and it provides numerous grades of polymer products. The company adopted the strategy of a joint venture to increase its competence in the market.

Competitive dynamics within the polyethylene market are primarily shaped by feedstock integration, scale advantages, product portfolio breadth, and access to downstream conversion ecosystems. Large producers compete not only on production capacity but also on cost position, logistics capabilities, sustainability initiatives, and the ability to supply differentiated resin grades. As margin volatility intensifies, operational efficiency and portfolio optimization increasingly determine long-term competitive positioning.

Integrated energy and petrochemical companies continue to control a substantial share of the global polyethylene market size. Major producers, including ExxonMobil, Dow, LyondellBasell, SABIC, Chevron Phillips Chemical, Borealis, INEOS, Braskem, Reliance Industries, and Sinopec, maintain competitive advantages through upstream feedstock access, extensive manufacturing footprints, and broad customer relationships. Vertical integration enables these companies to manage raw material fluctuations more effectively and sustain profitability during cyclical downturns.

Strategic priorities increasingly extend beyond commodity production. Producers are allocating capital toward specialty polyethylene grades, advanced catalyst technologies, and circular economy solutions to improve pricing power and strengthen customer retention. Recycled polyethylene integration and chemical recycling investments have become important competitive differentiators as sustainability expectations intensify across packaging and consumer industries.

LIST OF KEY COMPANIES PROFILED:

- LyondellBasell Industries N.V. (Netherlands)

- ExxonMobil Chemical (U.S.)

- SABIC (Saudi Arabia)

- Reliance Industries Limited (India)

- INEOS (U.K.)

- China National Petroleum Corporation (China)

- China Petroleum & Chemical Corporation (China)

- Ducor Petrochemicals (Netherlands)

- Formosa Plastic Group (Taiwan)

- Braskem (Brazil)

- Repsol (Spain)

- Borouge (UAE)

- Borealis AG (Austria)

- MOL Group (Hungary)

Latest Polyethylene Industry Developments

- March 2025: LyondellBasell Industries announced the expansion of circular and low-carbon polyethylene production capabilities to strengthen sustainable resin offerings for packaging and consumer applications. The strategic objective focused on increasing recycled-content availability and supporting customer decarbonization targets. The initiative involved mechanically recycled feedstocks, advanced recycling integration, and mass balance certification capabilities to improve circular polymer supply.

- January 2025: SABIC expanded collaboration with downstream packaging companies to accelerate the commercialization of circular polyethylene solutions. The move aimed to enhance packaging recyclability and strengthen participation in closed-loop material ecosystems. Technologies involved included certified circular polymers, feedstock recycling processes, and material traceability systems supporting sustainability compliance.

- October 2024: ExxonMobil advanced polyethylene production efficiency through investments supporting high-performance resin capacity and process optimization. The initiative sought to improve product differentiation and reinforce supply reliability across packaging and industrial markets. Capabilities involved included proprietary catalyst technologies, advanced polymerization processes, and specialty polyethylene grade development.

- August 2024: Dow Inc. expanded partnerships across the recycling value chain to increase the availability of recycled polyethylene materials for flexible packaging applications. The strategic purpose centered on improving circular economy performance and addressing customer demand for sustainable packaging solutions. The initiative incorporated mechanical recycling technologies, packaging design optimization expertise, and material compatibility capabilities.

- May 2024: Borealis AG strengthened investment activities aimed at expanding circular polyethylene production and improving resource efficiency. The action was intended to support regulatory compliance and strengthen long-term competitive positioning within the European market. Technologies and capabilities involved included advanced recycling platforms, renewable feedstock integration, and circular polymer manufacturing processes.

- November 2023: NOVA Chemicals Corporation and Amcor announced the signing of a Memorandum of Understanding (MoU) for mechanically recycled polyethylene. As per the agreement, NOVA Chemicals Corporation, the leading producer of polyethylene, would supply mechanically recycled polyethylene to Amcor, a prominent global packaging solutions manufacturer.

- February 2023: LyondellBasell and KIRKBI A/S signed an agreement for investing in APK, specialized in a solvent-based recycling technology for LDPE. By signing the agreement, LyondellBasell and KIRKBI A/S became the minority shareholders of APK.

REPORT COVERAGE

The research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, types, end-use industry, and products. Also, it provides quantitative data regarding volume and value, market analysis, research methodology for market data, and insights into industry trends. It highlights vital industry developments and the competitive landscape. In addition, the report encompasses various factors that have contributed to the growth of the market in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.1% from 2026 to 2034 |

|

Unit |

Value (USD Billion); Volume (Million Ton) |

|

Segmentation |

By Type

|

|

By End-use Industry

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 119.75 billion in 2025 and is projected to reach USD 171.81 billion by 2034.

In 2025, the market value stood at USD 119.75 billion.

Registering a significant CAGR of 4.1%, the market will exhibit considerable growth in the forecast period (2026-2034).

The packaging segment is expected to lead the market during the forecast period.

Rising product demand from various end-use industries, including automotive and electrical & electronics, is expected to fuel the market growth.

China held the highest share in the market in 2025.

LyondellBasell Industries N.V., ExxonMobil Chemical, and China National Petroleum Corporation are the leading players in the market.

The rapid growth in the food & beverages industry and growing technological advancements are anticipated to boost the consumption of the product.

- 2021-2034

- 2025

- 2021-2024

- 218

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us