Luxury Goods Market Size, Share & Industry Analysis, By Product Type (Watches & Jewelry, Perfumes & Cosmetics, Clothing, Bags/Purses, and Others), By End-user (Women and Men), By Distribution Channel (Offline and Online), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

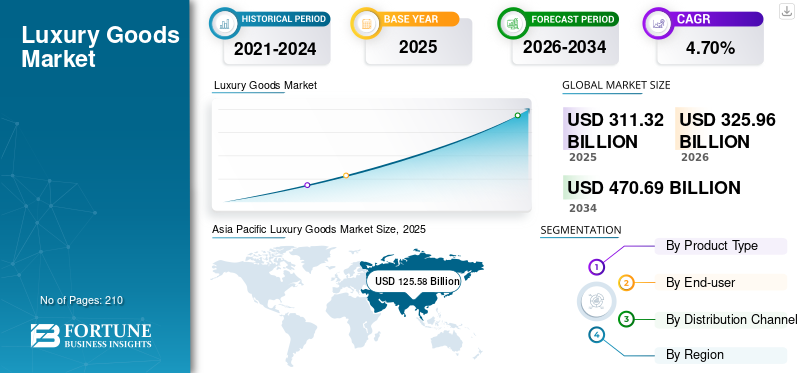

The global luxury goods market size was valued at USD 311.32 billion in 2025 and is estimated to increase from USD 325.96 billion in 2026 to USD 470.69 billion by 2034, demonstrating a CAGR of 4.70% between 2026-2034. Moreover, the luxury goods market in the U.S. is expected to grow significantly, reaching USD 86.84 billion by 2032. The demand for high-end fashion, premium accessories, and exclusive brand experiences is fueling market expansion. Asia Pacific dominated the luxury goods market with a market share of 40.34% in 2025.

Premium products are key entities showcasing the status symbol of its owner. Such products' excellent quality and high durability come at the highest price, affordable to only a small global population. Therefore, companies are targeting a wealthy population with creative designs, as the product cost is usually not the criteria for such groups, wherein the uniqueness and eminence of the product are the key deciding factors before their purchase.

For instance, in April 2023, Bernhard H. Mayer, a QNET LTD.-owned Swiss personal fashion brand, launched the Mecanique Collection, a timepiece collection of luxury watches of a unique mecanique design style in the Hong Kong market.

Therefore, introducing novel luxury goods designs would help the market grow rapidly in the forecast period of 2023-2030.

Download Free sample to learn more about this report.

Global Luxury Goods Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 311.32 billion

- 2026 Market Size: USD 325.96 billion

- 2034 Forecast Market Size: USD 470.69 billion

- CAGR: 4.70% from 2026–2034

Market Share:

- Asia Pacific dominated the luxury goods market with a 40.34% share in 2025 driven by rising disposable incomes, access to global luxury brands, and increasing consumption by middle-class and working women across China, India, and Southeast Asia.

- By product type, clothing is expected to retain the largest market share in 2025, supported by rapid fashion trend shifts and strong demand from both male and female consumers. However, handbags and smart luxury watches are experiencing rapid growth due to multifunctional use and tech innovation.

Key Country Highlights:

- United States: Expected to reach USD 86.84 billion by 2032, fueled by a high concentration of billionaires, premium lifestyle choices, and strong demand for luxury fashion and accessories, particularly among millennials and Gen Z.

- China: A leading luxury market driven by tech-enabled retail formats, personalized shopping experiences, and a surge in online sales. Strategic investments like Burberry’s social retail store in Shenzhen underscore the country's luxury dominance.

- France: Home to global luxury leaders like LVMH, Kering, and L’Oréal, France drives innovation, fashion influence, and brand prestige across global markets.

- U.A.E.: A luxury hotspot in the Middle East, with strong demand from affluent consumers and robust sales in premium fashion, beauty, and timepieces across Dubai and Abu Dhabi.

- Brazil: Steady luxury market expansion is expected, supported by urbanization and growing interest in premium fashion and accessories among high-income consumers.

LUXURY GOODS MARKET TRENDS

- Asia Pacific witnessed luxury goods market growth from USD 104.37 Billion in 2021 to USD 109.42 Billion in 2022.

Download Free sample to learn more about this report.

Emergence of Technology Embedded Products is a Prominent Trend

Innovatively created and fashion-forward goods that combine technology elements in jewelry items, handbags, or goggles will likely augment product demand. For instance, in March 2023, an innovation lab, Cathy Hackl, launched VerseLux, a luxury, high-end jewels equipped with Near-Field Communication (NFC) chips in China. Similarly, in April 2023, luxury apparel and accessories brand Coach launched Coachtopia, a line of luxury-fashioned products such as bags, wallets, footwear, and garments equipped with NFC chips. These products are available in the U.S., Canada, the U.K., and Asian markets.

LUXURY GOODS MARKET GROWTH FACTORS

Rising Number of Wealthy Population to Boost Market Expansion

Luxury items, as the name suggests, are products majorly explored by high net worth individuals. A rising number of high-income population groups is set to propel the market growth. For instance, as per Oxfam International’s data published in January 2020, about 2,153 billionaires worldwide have more wealth than about 4.6 billion people, who comprise 60% of the global population.

Companies are targeting the millennial and GenZ population with customized product offerings to gain their attention. For instance, Louis Vuitton lets customers personalize their handbags using hot stamping or hand-painting. Therefore, increasing demand for high-end fashion products from the rich population would support the personal luxury goods market growth.

Inclination toward Sustainable Products to Offer Market Growth Opportunities

The sustainability trend has also entered the luxury business, where environmentally friendly raw materials and responsible use of utilities are promoted. Plant-based leather, such as the one derived from pineapple and other natural materials, can be used to produce jackets, footwear, and handbags instead of leather goods derived from animals. For instance, in June 2020, Vikki Jones, a luxury products retailer, launched its new eco-friendly tote bags made of 100% vegan leather, ensuring no animals were harmed in the manufacturing process.

Besides, lower electricity usage, less water, and safer raw materials are being stressed to ensure sustainability throughout the supply chain. For instance, Junghans, a renowned fashion brand, offers high-end solar watches made of sustainable and recycled materials in the global market. Therefore, rising initiatives toward sustainable high-end goods production will likely surge the demand for eco-friendly products.

RESTRAINING FACTORS

Growing Adoption of Second-hand Branded Items to Hamper Demand

An increasing trend of purchasing second-hand branded products or renting luxury products is likely to hamper the market of original luxury products as second-hand products are offered at a lower cost than the original price. Similarly, the growing counterfeiting trend, wherein products resembling luxury brands are offered at lower prices, is further likely to restrain the market growth.

LUXURY GOODS MARKET SEGMENTATION ANALYSIS

By Product Type Analysis

-

The Watches & Jewelry segment led the market accounting for 27.03% market share in 2026.

To know how our report can help streamline your business, Speak to Analyst

Clothing Segment to Dominate Owing to Rapidly Changing Fashion Trends

The market is divided into watches & jewelry, perfumes & cosmetics, clothing, bags/purses, and others based on product type.

The clothing segment is expected to hold a major share owing to its increasing demand from both men and women end-users, along with rapidly changing fashion trends. However, the bags segment is expected to grow rapidly due to increasing demand for leather-based products. The demand for fashionable and matching handbags is increasing from end-users that, in turn, can be used for varied applications such as office, party, or casual bags. For instance, in February 2020, the Loewe luxury brand launched its Balloon bag, made available in all three sizes, namely, small, medium, and large, per customer requirements.

The watches & jewelry segment is expected to hold a significant share due to the increasing demand for smart luxury watches and varied jewelry items. For instance, CHRISTIE’S, a British auction house, reported 153% increase in its jewels, watches, handbags, and wine products’ luxury auction and private sales, reaching USD 980.0 million in 2021. It has 5,478 auction houses in the U.K. The others segment includes products, such as footwear and eyewear, which is expected to gain traction due to the introduction of new product designs in the market.

By End-user Analysis

Women Segment to Hold Highest Share, Backed by Greater Inclination toward Beautification

Based on end-user, the market is segmented into men and women. Most luxury products, including cosmetics, fragrances, handbags, necklaces, earrings, and bracelets are primarily used by women end-users, making women a major segment.

However, emerging male grooming trends would support the growth of the men segment, wherein branded shirts, goggles, and high-end watches would experience greater demand from them. Therefore, numerous players are focusing on introducing products that can cater to the varied demands of both end-users. For instance, in January 2020, OMEGA launched a new luxury eyewear collection featuring sunglasses suitable for both men and women.

By Distribution Channel Analysis

Online to Hold Largest Share due to its Greater Convenience in Purchasing

Based on distribution channel, the market is segmented into offline and online. The offline segment is expected to hold a major luxury goods market share, as it allows customers to physically see and touch the product and compare their features in person at the store. Companies are trying to increase their presence through retail or department stores to have a strong foothold in the market. For instance, in February 2020, Burberry announced the acquisition of Printemps in Paris, France. Printemps is a department store chain offering a wide range of luxury products, apparel, and beauty products.

However, the purchase conveniences of online channels would make it the fastest-growing segment. The COVID-19 pandemic has further provided opportunities to strengthen online channels in the luxury business. For instance, in March 2020, Reliance announced its plans to introduce a new e-commerce platform for shopping for luxury goods in India. Therefore, the online shopping trend of luxury goods is likely to continue in the near future.

REGIONAL Analysis

Asia Pacific Luxury Goods Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 125.58 billion in 2025 and USD 131.49 billion in 2026. The Asia Pacific market is projected to grow rapidly due to increasing disposable incomes of the region's middle-class population. Similarly, the rising access to global luxury brands would lead to increased product consumption. For instance, in July 2020, Burberry, a U.K.-based luxury products company, announced its first social retail store in Shenzhen, for Chinese consumers, along with Tencent’s partnership. The store spans about 539 sqm/5,800 sqft, with about 10 rooms offering various interactive, personalized retailing experiences. Moreover, a surging number of working women in the region has accelerated the consumption of women-centric luxury products, such as handbags, high-end footwear, and jewelry products, with their growing disposable income.

Europe

The considerable share of Europe in the global market is attributed to the presence of prominent players, including L’Oréal, LVMH, Burberry, and others supporting product consumption in the region. The North American market is characterized by the increasing presence of many rich people, majorly in the U.S., that has supported the product demand. For instance, as per the report titled ‘Billionaire-Bonanza-2020,’ published in April 2020 by the Institute for Policy Studies, the number of billionaires increased from 298 in 2000 to about 614 in 2020 in the U.S. Besides, the presence of a population that is highly inclined toward fashionable apparel and accessories has added impetus to the growth of the market in this region.

- In China, the Clothing segment is estimated to hold a 27.11% market share in 2022.

To know how our report can help streamline your business, Speak to Analyst

The South America market is likely to grow steadily as the urban population increases in Brazil and Chile. Changes in the standard of living are therefore expected to augment the spending on luxury products in the region. Besides, the Middle East and Africa will likely show a growing trend with the increasing demand for luxury products from Gulf countries such as the U.A.E. and Saudi Arabia. Therefore, key players have opportunities to expand their businesses in this region.

KEY INDUSTRY PLAYERS

Key Players Focus on Strategies such as Partnerships and New Product Development to Gain Market Share

Top luxury goods companies hold a major market share due to their strong product portfolios and wider reach in most regional markets. Luxury goods players are focusing on strategies, such as partnerships, new product launches, and acquisitions, to strengthen their foothold in the market. For instance, on 11th December 2020, L'Oréal signed an agreement with Prada S.p.A. that will allow the company to create, develop, and distribute luxury beauty products of the latter.

List of Top Luxury Goods Companies:

- LVHM (France)

- Compagnie Financière Richemont SA (Switzerland)

- Kering SA (France)

- Chow Tai Fook Jewellery Group Limited (Hong Kong)

- The Estée Lauder Companies Inc. (U.S.)

- Luxottica Group SpA (Italy)

- The Swatch Group Ltd. (Switzerland)

- L’Oréal Group (France)

- Ralph Lauren Corporation (U.S.)

- Shiseido Company, Limited (Japan)

KEY INDUSTRY DEVELOPMENTS:

- April 2023: Hey Harper, a Portugal-based luxury jewelry maker, launched Titled ICONS, a new capsule collection of jewelry products in the U.K. The collection includes the GILDED THORNS Ear Cuff, PETALS SPIRAL Bracelet, CRYSTAL BLOOM Ring, GARDEN OF LIGHT Brooch, and others.

- January 2021: OC Oerlikon, a Switzerland-based technology group, acquired Coeurdor, a full-service provider of components for luxury bags, belts, watches, and others to expand its presence in the high-end coatings industry for luxury goods.

- November 2020 – Farfetch, Alibaba Group, and Richemont partnered to help promote digitization in the luxury industry.

- October 2020: Ralph Lauren introduced the on-demand manufacturing of custom packable jackets in the U.S. and EMEA.

- October 2020 – LVMH announced the acquisition of Tiffany & Co. for USD 131.50 per share in cash. This acquisition in the goods market is expected to strengthen the portfolio of the luxury jewelry section of LVMH.

REPORT COVERAGE

The research report provides detailed market analysis and focuses on key aspects such as competitive landscape, distribution channel, and leading product types. Besides this, the report offers insights into the luxury goods market trends and highlights key industry developments. In addition to the aforementioned factors, the free sample of the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.70% during 2026-2034 |

|

Unit |

Value (USD Billion) |

|

|

By Product Type

|

|

|

By End-user

|

|

|

By Distribution Channel

|

|

Segmentation |

North America (By Product Type, End-user, Distribution Channel, and Country)

Europe (By Product Type, End-user, Distribution Channel, and Country)

Asia Pacific (By Product Type, End-user, Distribution Channel, and Country)

South America (By Product Type, End-user, Distribution Channel, and Country)

Middle East and Africa (By Product Type, End-user, Distribution Channel, and Country)

|

Frequently Asked Questions

According to Fortune Business Insights, the global luxury goods market was valued at USD 311.32 billion in 2025 and is projected to grow from USD 325.96 billion in 2026 to USD 470.69 billion by 2034.

The global market is expected to grow at a CAGR of 4.70% during 2023-2030.

The luxury goods market is being driven by the rising number of high-net-worth individuals, increasing disposable incomes, and growing demand for exclusive, status-driven products. Innovation in design and sustainability trends are also contributing to market expansion.

As of 2025, Asia Pacific holds the largest market share at 40.12%, driven by rising affluence, urbanization, and growing access to international luxury brands across countries such as China, Japan, and South Korea.

Key trends include the integration of technology (e.g., NFC chips in jewelry and bags), rising demand for eco-friendly luxury items, increased customization and personalization, and a shift toward online luxury retail experiences.

Sustainability is becoming a key differentiator. Brands are introducing vegan leather, solar-powered watches, and low-impact production methods to appeal to eco-conscious consumers and meet stricter environmental standards.

The luxury goods category includes watches & jewelry, perfumes & cosmetics, apparel, handbags, footwear, and eyewear. Clothing remains the largest segment, followed closely by jewelry and bags, due to evolving fashion trends and consumer preferences.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us