Semiconductor IP Market Size, Share & Industry Analysis, By Design IP (Interface IP, Processor IP, Memory IP, and Others), By Revenue Source (License and Royalty), By Core Type (Soft Core and Hard Core), By Industry (Consumer Electronics, IT & Telecommunications, Automotive, Industrial, Aerospace & Defense, and Others), and Regional Forecasts, 2026-2034

Semiconductor IP Market Size

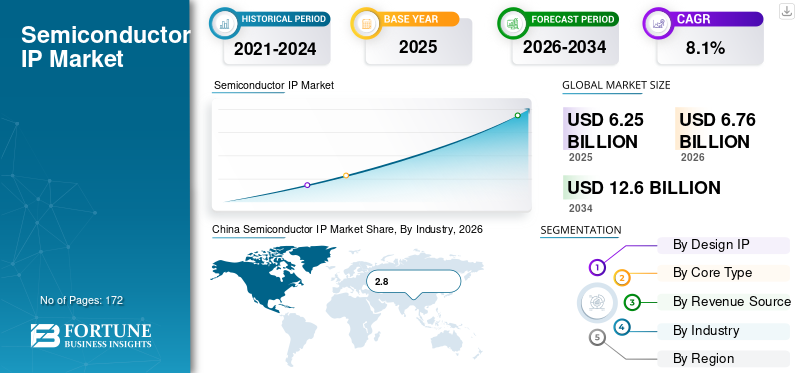

The global semiconductor IP market size was valued at USD 6.25 billion in 2025 and is estimated to increase from USD 6.76 billion in 2026 to USD 12.60 billion by 2034, demonstrating a CAGR of 8.10% between 2026-2034. Asia Pacific dominated the semiconductor IP market with a market share of 52.63% in 2025. Rising requirements for automation and increasing adoption of the IP Core products in the consumer electronic industry at a rapid pace aids the market growth. Also, the industry is growing at a fast pace owing to rising internet penetration and increasing adoption of the smart connected devices aids the market growth.

Also, numerous prime players in the market are adopting patented IP solutions across consumer electronics manufacturing. For instance,

- In March 2022, Kudelski television access and management systems IoT Hardware Security manufacturers launched a secure IP product portfolio. This secure IP hardware product offers semiconductor manufacturers robust cryptographic capabilities integrated into their system-on-chip product categories.

The report's scope comprises various design IP solutions and products from key players such as Arm Limited, Synopsys Inc., Lattice Semiconductor Corporation, Cadence Design Systems, Inc., Imagination Technologies Ltd., and others. These players offer Interface IP, Denali Memory Interface, and Storage IP that support a wide range of industry standards for controllers and smart device manufacturing. Also, Renesas IP solutions firm offers a wide range of IP solutions for various microcontroller units (MCUs) and system-on-chip (SoC) products. These IP solutions include central processing units IP, processor IP solution, digital IP, memory IPs, interface IP, timer IP, memory IP, and analog IP. Renesas offers its customers access to IP solutions that provide a high-quality, high-performance, silicon-based IP portfolio.

Download Free sample to learn more about this report.

Semiconductor IP Market TRENDS

Download Free sample to learn more about this report.

Rising Adoption of Wireless Technologies Devices Drives the Market Growth

The increasing adoption of wireless technology-based devices and rising investments by the leading players to develop advanced wireless products assist the market growth. According to the International Telecommunication Union (ITU), the capital investment in wireless technologies reached around USD 600 billion in 2020 across the U.S., owing to the rising adoption of 5G and wireless devices. Also, leading players in the market are investing in developing wireless technology devices around the globe to meet consumers' demands. For instance,

- In March 2021, Apple, Inc. invested around USD 1.2 billion in developing wireless technology in Munich, Germany. The company aimed to create future 5G wireless technologies through seamless hardware and software products.

Such an increase in wireless technology development and investment surges the demand for IP solutions. These solutions, such as silicon-based design (ASIC) IP, interface IP, and processor IP, are the building blocks of portable and wireless technology-based devices. They are used to manufacture wireless technology devices such as smartwatches, headphones, and smartphones.

SEMICONDUCTOR IP MARKET GROWTH FACTORS

Increasing Demand for Advanced Consumer Electronics Devices Drives Market Growth

Rising adoption and development of advanced technology-based consumer electronics around the globe have propelled the global semiconductor IP market growth. According to the Center for National Interest Organization, in 2020, the global consumer electronics market will be valued at around USD 683 billion and is expected to reach USD 881.7 billion by 2025. In 2021, there were approximately 4.4 billion units of consumer electronics that have been shipped globally, an increase of 2.7% compared to 2020.

These IP solutions are widely used in manufacturing several categories of electronics devices such as smartphones, headphones, wearables, and several innovative home products. Wearable devices are built with the memory and interface IP that brings technology into everyday lives to enhance the functionality of things that deliver real-time feedback. These devices play a significant role in the growing connected world as IP solutions help design System on Chips (SoCs) that fit into these devices. The rising sale of wearables and other smart connected devices around the globe with the surge in consumer's demand for these smart devices worldwide is expected to drive the global market growth.

RESTRAINING FACTORS

Continuous Technology Changes and Rising Concerns about IP Theft in Industry Impede Market Growth

Technology is an ever-converting concept, especially in the electronics industry. The semiconductor industry is facing the physical limit for manufacturing the existing materials and also rising potential threats pertaining to Moore's law. Moore's law is used for the projection and observation of historical trends. It helps to link the experience and production of the market needs.

The electronics industry faces issues related to IP thefts from various vendors. For instance, in July 2022, Tower Semiconductor (TS), an electronics component manufacturer, was accused of semiconductors IP thefts. IQE Ltd., a wafer manufacturer, has filed IP theft at the U.S. Central District Central Court of California. The Cardiff-based IQE further says it has "significant evidence" supporting its accusations.

Such an increase in IP thefts and continuous technological changes in the consumer electronics industry hinder the market growth.

SEGMENTATION Analysis

By Design IP Analysis

Rising IoT Devices Penetration with Surge in Consumer Electronics Goods Drives Market Growth

Based on design IP, the market is segmented into interface IP, processor IP, memory IP, and others (verification IP, graphics IP). The processor IP segment is predicted to hold the largest market share as it is widely used in manufacturing consumer electronics goods such as smartphones, CPUs, laptops, and others. The rising sale of these smart and IoT devices globally aids the processor IP market growth. According to the World Economic Forum Organization, the consumer's Internet of Things devices sale is expected to increase from USD 45 billion in 2021 to USD 154 billion by 2028.

In addition, the memory IP segment is anticipated to grow with the greatest CAGR during the forecast period, as customers are speedily embracing storage devices such as flash drives, memory devices, high computing devices, and data centers.

By Core Type Analysis

Rising 5G technology Adoption and Increasing Advancement of Consumer Electronics Aid Hard Core Segment

Based on core type, the market is segmented into hard core and soft core. The hard core segment is expected to hold the maximum market share owing to rising demand for the processors in consumer electronics goods such as laptops, personal computers, and others.

Additionally, the soft sore segment is estimated to show notable growth during the forecast period, with the highest CAGR over the forecast period. Rising investment and development of advanced technologies, such as 5G, AI, and cloud-based solutions, among enterprises are driving the IP core segmental growth. According to the GSMA Intelligence Report, in 2021, investments in 5G network technology are expected to reach around USD 1 trillion by 2025 globally.

By Revenue Source Analysis

Royalty to Perceive High Growth owing to Rising Bulk Purchase of IP Products by Electronics Device Manufacturers

The market is segmented into royalty and licensing based on revenue source. The royalty segment is expected to hold the largest market share owing to bulk procurements of semiconductors IPs from the leading electronics device manufacturers.

However, the licensing segment is estimated to show reliable growth with the highest CAGR over the forecast period. This is primarily attributed to the rising adoption of licensed semiconductor IP products and wireless device manufacturers' solutions. Several wireless device manufacturers are developing connected communication devices using the license IP solutions. For instance,

- In June 2020, ASUS launched a new AI noise-canceling wireless microphone (AI Mic) technology. The new technology provides clear voice communication eliminating unwanted background noise. This wireless microphone technology filters out and removes other human voices, traffic, or wind noise using chipset-based machine learning. In addition, the in-built chipset manages all sound processing so that the adapter does not hamper the performance of the laptop, mobile device, or connected PC.

By Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Rising Development of the Wireless Consumer Electronics Devices by Leading Players Aids the Market Growth

The market is segmented into consumer electronics, IT and telecommunications, automotive, industrial, aerospace & defense, and others (government) based on industry.

The Consumer Electronics segment is projected to dominate the market with a share of 31.1% in 2026. The consumer electronics segment is projected to hold the largest market share owing to the rising developments of wireless technology devices and growing development of wireless devices by the key players. For instance,

- June 2022: Vissonic Electronics Ltd. updated its teleconferencing system by launching the meeting room's Vissonic 5G Wi-Fi Wireless conference system. It consists of a wireless microphone, conference system, and presentation system integrated with a 5G Wi-Fi wireless access point providing convenient local video and audio access solutions.

The automotive segment is assessed to grow at the highest CAGR during the forecast period. This growth is owing to the increasing adoption of electric vehicles with a surge in implementation of wireless technology for EVs. For instance, according to the International Energy Agency Report 2021, the global electric vehicles sale reached 6.6 million in 2021, doubled as compared to 2020. Semiconductor IP products, such as interface IP, processor IP, and memory IP, are widely used in electric automotive.

REGIONAL Analysis

Asia Pacific Semiconductor IP Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Geographically, the market share is fragmented into Asia Pacific, North America, the Middle East & Africa, Europe, and South America. They are further classified into countries.

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 3.29 billion in 2025 and is projected to reach USD 3.56 billion in 2026. Asia Pacific is anticipated to account for the largest market share in the global market during the forecast period, owing to rising investment by key players in the manufacturing of electronics devices in this region. For instance,

- In May 2022, Samsung Group planned to invest around USD 489 billion in developing semiconductors and biologics for the next five years in the Asia Pacific region.

Further, the presence of electronics device manufacturers and the rising export of electronics components from the Asia Pacific region drive the market growth. According to the Invest Asean Organization, the consumer electronics sector accounted for around 50% of the total exports from most Asia Pacific countries, including China, India, and Japan.

North America

North America is expected to grow at a moderate CAGR during the forecast period owing to the rising proliferation of wireless technology and 5G technology developments. According to Semiconductor Equipment and Materials International (SEMI), North America represented around 38.9% of the global electronics industry spending in 2020.

Europe

Europe is expected to grow with a moderate CAGR due to rising consumer demand for connected devices. According to the Broadband Forum, in 2020, the market value of connected devices for homes in Europe is expected to reach around USD 157 billion by 2023. This growth is primarily attributed to the COVID-19 pandemic owing to the rapid adoption of digital technology-based devices.

South American countries, such as Argentina, Brazil, and others, are increasing at a lower rate owing to slow investment in the research & development in the semiconductor industry. South America's IP market is expected to be driven by the rising adoption of smart devices such as laptops, smartphones, and personal computers.

China Semiconductor IP Market Share, By Industry, 2026

To get more information on the regional analysis of this market, Download Free sample

The Middle East and Africa is growing with moderate CAGR owing to rising IoT spending and a surge in digital transformation strategies by several countries in this region. According to the International Data Corporation (IDC), the Internet of Things (IoT) technologies spending across the Middle East and African countries reached USD 8.47 billion in 2019 and is expected to reach USD 17.63 billion by 2023. Such an increase in IoT spending is expected to witness potential opportunity for the growth of semiconductor IP products and solutions in the region.

KEY INDUSTRY PLAYERS

Key Players in the Market are Escalating their Processes by Presenting Advanced Semiconductor IP

The global market is consolidated with leading players such as Arm Holdings Ltd., Synopsys Inc., Cadence Design Systems, Inc., Ceva Inc., Lattice Semiconductor Corporation, and others. These crucial players are increasing their operations by implementing corporate tactics such as acquisitions, mergers, partnerships, product launches, and collaborations. For instance,

- June 2022: Imagination, the U.K.-based semiconductor intellectual property IP firm, launched semiconductor IP service that does not charge license fees. These IP services provide technical support and maintenance.

- May 2022: Quadric and MegaChips partnered to deliver the system on chips and application-specific integrated circuit (ASIC) solutions for building Quadric’s AI-based processors. MegaChips received around USD 21.0 million in funding that aimed at helping Quadric to release next-generation processor architecture.

List of Key Companies Profiled in Semiconductor IP Market:

- Arm Holdings Ltd (U.K.)

- Synopsys Inc. (U.S.)

- Cadence Design Systems, Inc. (U.S.)

- Imagination Technologies Ltd (U.K.)

- Ceva Inc. (U.S.)

- Lattice Semiconductor Corporation (U.S.)

- Rambus Inc. (U.S.)

- eMemory Technology, Inc (Taiwan)

- Silicon Storage Technology, Inc (U.S.)

- VeriSilicon Microelectronics Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- In May 2022, Faraday Technology Corporation launched Soteria's advanced security IP subsystems. This solution provides a custom SoC design that enables hardware security for a wide range of IoT applications. Faraday Technology Corporation offers several security solutions, including IP security system software solutions for secure SoC development.

- In June 2021, Sondrel launched a quad-channel, an IP platform with ISO-26262 applications. This IP reference platform is designed for simplifying and architecting the semiconductor components.

- In November 2021, Elmos Semiconductor SE partnered with Arm Holdings Ltd to manufacture and design energy-efficient IP processors. Arm Holdings Ltd provided over 200 billion chips for advanced computing. Elmos Semiconductor SE licensed a wide range of IP products from Arm Holding Ltd for its automotive microcontroller unit products.

- In October 2021, Synopsys Inc. launched an IP solution named HBM3 for various semiconductor components such as controllers, physical layer devices, and verification IPs. HBM3 IP technology helps the designers to meet low-power memory and high-bandwidth requirements for SoCs.

- In August 2021, Rambus Incorporated developed and licensed chips manufacturer acquired PLDA SAS licensor of semiconductor intellectual property firm. This acquisition has expanded the company's digital controller offerings and gained building blocks for its CXL Memory Interconnect Initiative.

REPORT COVERAGE

The report offers qualitative and quantitative insights into the market and a detailed analysis of the size & growth rate for all possible segments in the market. It also elaborates on market research, dynamics, emerging trends, and the competitive landscape. Key insights offered in the report are the adoption of automation by individual segments, recent industry developments such as partnerships, mergers & acquisitions, consolidated SWOT analysis of key players, business strategies of leading market players, macro and micro-economic indicators, and key industry trends.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Design IP, Core Type, Revenue Source, Industry, and Region |

|

By Design IP |

|

|

By Core Type |

|

|

By Revenue Source |

|

|

By Industry |

|

|

By Region |

|

Frequently Asked Questions

The global market is predicted to reach USD 12.6 billion by 2034.

In 2025, the market value stood at USD 6.25 billion.

The market is projected to grow at a CAGR of 8.1% during the forecast period (2026-2034).

The memory IP segment is expected to show the highest CAGR during the forecast period.

North America dominated the market due to rising research and development activities related to the semiconductor industry in the U.S.

Increased adoption of wireless technologies based devices with the surge in digitalization aids the market growth.

Some of the top players in the market are Arm Holdings Ltd., Synopsys Inc., Cadence Design Systems Inc., Imagination Technologies Ltd., CEVA Inc., Lattice Semiconductor Corporation, and others.

- 2021-2034

- 2025

- 2021-2024

- 172

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us