Anti-Collision Sensor Market Size, Share & Industry Analysis, By Sensor Type (Radar, LiDAR, Camera / Vision, Ultrasonic, Infrared), By Function (Autonomous Emergency Braking (AEB), Adaptive Cruise Control (ACC), Blind Spot Detection (BSD), Lane Departure Warning / Lane Keeping Assist (LDW / LKA), Parking Assistance, and Rear Collision Warning), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Range (Short-range (< 5 m), Medium-range (5–60 m), Long-range (> 60 m)), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

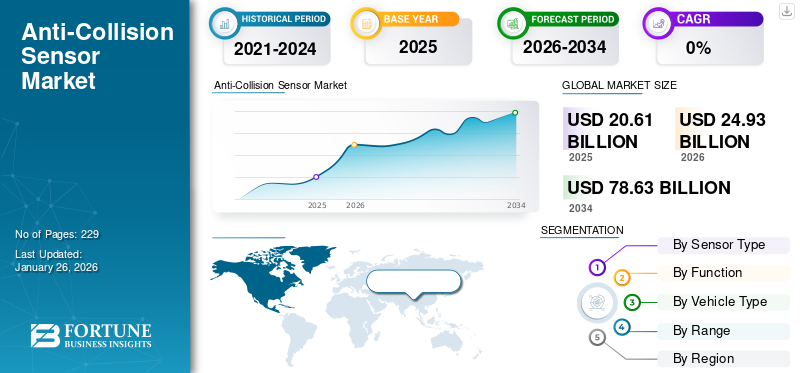

Anti-Collision Sensor Market Size and Future Outlook

The global anti-collision sensor market size was valued at USD 20.61 billion in 2025. The market is projected to grow from USD 24.93 billion in 2026 to USD 78.63 billion by 2034, exhibiting a CAGR of 15.44% during the forecast period. Asia Pacific dominated the anti-collision sensor market with a market share of 48.26% in 2025.

Automotive anti-collision sensors are electronic perception devices and subsystems that detect, classify, and track nearby objects to prevent or mitigate collisions. They include sensor technologies such as radar, cameras, LiDAR, ultrasonic, and infrared modules integrated with ECUs and software stacks to provide functions such as automatic emergency braking, adaptive cruise control, blind spot monitor. These sensors measure distance, relative speed, and object signatures, then feed algorithms that trigger warnings or automated interventions. Robust sensor fusion and calibration are critical for real-world reliability across weather, lighting, and traffic scenarios, making them core components of modern vehicle safety systems.

The anti-collision encompasses sensor hardware, used across passenger and commercial vehicles. Growth is driven by regulatory mandates, NCAP scoring, increasing ADAS adoption, and rising vehicle electrification that centralizes sensor suites. Market segmentation spans sensor type (radar, LiDAR, camera, ultrasonic, infrared), function (AEB, ACC, BSD, LDW/LKA, parking assist, rear warning), vehicle class, and range. Major players include Tier-1 suppliers Bosch, Continental, Denso, Valeo, Aptiv, and ZF; specialist perception firms such as Mobileye, Luminar, and Velodyne; and regional innovators (Hesai, LeddarTech). Competitive dynamics hinge on ASP declines, sensor fusion IP, and OEM partnerships.

Download Free sample to learn more about this report.

Anti-Collision Sensor Market Key Takeaways

- 2025 Market Size: USD 20.61 billion

- 2026 Market Size: USD 24.93 billion

- 2034 Forecast Market Size: USD 78.63 billion

- CAGR: 15.44% from 2026–2034

- Asia Pacific dominated the anti-collision sensor market with a 48.26% share in 2025.

- Camera/vision sensors are expected to lead with a 41.72% share in 2026.

- Autonomous emergency braking (AEB) is projected to hold a 32.14% share in 2026.

Asia Pacific

Asia Pacific reached USD 9.95 billion in 2025, accounting for 48.26% of global revenue.

Europe

Europe generated USD 5.77 billion in 2025, representing 28.02% of the global market.

North America

North America recorded USD 4.5 billion in 2025, supported by rising ADAS adoption.

U.S.

The U.S. market is projected to reach USD 3.97 billion by 2026, driven by AEB regulations and vehicle safety adoption.

Japan

The Japan market is projected to reach USD 2.21 billion by 2026, supported by strong automotive technology adoption.

Read More

IMPACT OF TARIFFS

U.S. tariff actions meaningfully affect anti-collision sensors by raising component costs, reshaping sourcing, and incentivizing reshoring. As per article published by White & Case LLP in March 2025, Recent U.S. measures impose duties affecting vehicle and parts imports, effectively adding roughly 25% to many auto and parts shipments, raising procurement costs and prompting re-qualification and redesign work. Suppliers report tariff-related component price uplifts of about 15–20% for LiDAR, radar, and compute modules, squeezing margins and slowing rollout schedules; concurrent supply risks for rare-earth magnets and chips exacerbate disruption and increase inventory and compliance costs.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for ADAS & Autonomous Driving to Propel Market Expansion

The increasing deployment of Advanced Driver Assistance Systems (ADAS) has emerged as a critical factor driving the anti-collision sensor market share. ADAS technologies such as forward collision warning systems, adaptive cruise control, lane-keeping assistance, and blind-spot detection depend on a combination of radar, LiDAR, cameras, and ultrasonic sensors for effective operation. As safety regulations tighten and consumer awareness grows, manufacturers are standardizing these features across vehicle segments, including mid-range and entry-level models. This widespread integration is accelerating demand for a reliable and cost-effective collision avoidance sensor.

Moreover, global safety initiatives, such as the European Union’s mandate on mandatory advanced safety features in new vehicles by 2024, have further reinforced the adoption of advanced driver assistance systems ADAS. Consequently, the automotive ecosystem is witnessing robust growth in sensor utilization, positioning collision-avoidance technologies as essential enablers of next-generation mobility. This development will drive market growth during the forecast period.

The market is also significantly influenced by the global push toward autonomous driving, which demands advanced and redundant sensing capabilities. Semi- and fully autonomous vehicles require a continuous, high-fidelity understanding of their environment to ensure safety in complex and dynamic road conditions. This necessitates multi-sensor architectures, integrating long-range radar, LiDAR, vision systems, and ultrasonic modules, supported by advanced sensor fusion algorithms.

For instance, Level 3 and Level 4 autonomous systems depend on multiple layers of redundancy to minimize collision risks in scenarios where driver intervention is limited or absent. Manufacturers are increasingly investing in such technologies to maintain competitiveness in the evolving mobility landscape. As a result, the adoption of anti-collision sensors is expanding in both passenger and commercial vehicle categories, fueling the market growth during the forecast period.

MARKET RESTRAINTS

Regulatory Ambiguity, Fragmented Standards, and Liability Issues Act as Significant Restraining Factors for Market

Regulatory uncertainty, standards fragmentation, and liability concerns form a powerful, intertwined brake on the global anti-collision sensor market growth as they convert technical risk into legal and commercial risk for OEMs and suppliers. Regulators across jurisdictions are moving at different speeds. At the same time, the U.S. has issued a formal AEB rulemaking and tightened data/recorder requirements; implementation timing and scope have shifted, creating gaps between what manufacturers can deploy today and what will be legally required in the future.

International forums such as WP.29/UNECE are approving targeted amendments (for example, on automated lane keeping) but not yet delivering a single harmonized global standard. Hence, OEMs face fragmented technical requirements across markets and higher certification costs. Fragmentation amplifies liability exposure when feature performance varies between jurisdictions or lacks common validation protocols, determining “standard of care” after a crash becomes more complex, and that fuels litigation and insurance pressures. Cases tied to missed/incorrect ADAS calibrations have risen substantially, forcing manufacturers to factor legal contingencies into product rollouts. High-visibility recalls and software withdrawals for automated systems further sharpen regulator and public scrutiny, prompting stricter post-deployment monitoring and longer certification cycles.

Practically, these dynamics make OEMs more conservative about standardizing advanced sensor stacks globally they delay or throttle feature launches to wait for clearer, harmonized regulations or enhanced evidence of cross-condition reliability, slowing economies of scale and ASP declines. In short, until regulators converge on interoperable standards, clarify liability rules, and streamline evidence/EDR requirements for automated actions, the market will face higher compliance costs, longer time-to-market, and elevated legal provisioning that jointly restrain rapid, universal adoption.

MARKET OPPORTUNITIES

Integration with Vehicle-to-Everything (V2X) Communication Propels Market Growth

The integration of anti-collision sensors with Vehicle-to-Everything (V2X) communication technologies is emerging as a transformative opportunity in the automotive safety ecosystem. While traditional sensors such as radar, LiDAR, and cameras provide real-time environmental data, their detection capabilities are limited to the line of sight. Weather, obstacles, or blind spots can disrupt them. V2X complements these sensors by enabling vehicles to communicate directly with other vehicles, infrastructure, and pedestrians, offering predictive awareness of potential collisions before they occur. This interchange between physical sensing and digital communication enhances overall system reliability and reduces accident risks, creating a strong value proposition for automakers and regulators.

A key driver of this opportunity is the growing emphasis on connected mobility and smart city initiatives. Governments in regions such as Europe, China, and North America are investing heavily in connected infrastructure, including smart traffic lights, pedestrian crosswalks, and vehicle-to-roadside communication units.

For instance, in 2024, the U.S. Department of Transportation launched pilot programs in Michigan and Florida to test V2X-enabled vehicles for real-time traffic management and collision prevention. These initiatives create fertile ground for the integration of anti-collision sensors with V2X, accelerating the commercialization of more advanced safety systems. Automakers that adopt this combined approach can differentiate themselves with enhanced safety ratings and compliance with upcoming regulatory mandates.

ANTI-COLLISION SENSOR MARKET TRENDS

Sensor Fusion & Software Intelligence to Fuel Market Growth

The anti-collision sensor market trend is rapidly shifting from a hardware-centric approach toward sensor fusion and intelligent software platforms. Traditional systems relied on a single sensor type, radar for distance measurement or cameras for object recognition. However, these technologies have inherent limitations; for instance, cameras can struggle in low light or fog, while radar may misinterpret stationary objects. Sensor fusion resolves this challenge by combining data from multiple sources, such as radar, LiDAR, ultrasonic, and cameras, to generate a holistic, accurate, and reliable perception of the driving environment. This layered redundancy significantly improves safety performance, which is essential for advanced driver assistance systems (ADAS) and higher levels of autonomous driving.

The market is witnessing a surge in the role of software intelligence. The vast volumes of raw data generated by modern vehicles require powerful processing algorithms capable of real-time decision-making. Companies are increasingly embedding artificial intelligence (AI) and machine learning (ML) into perception systems to classify objects, predict movement, and minimize false alerts. This shift means that the value proposition is no longer just in sensor units, but in the ability to process and interpret sensor data effectively. As a result, software-driven innovation is becoming a key differentiator among market leaders.

For instance, in 2024, NVIDIA unveiled its Drive Hyperion platform, a next-generation architecture designed to accelerate the adoption of advanced driver assistance systems (ADAS) and autonomous driving technologies. The platform integrates a suite of sensors, including cameras, radar, and LiDAR, while leveraging NVIDIA’s powerful AI computing chips to process fusion data in real time. This multi-sensor approach enables critical anti-collision capabilities such as pedestrian detection, lane-level localization, and predictive collision avoidance, setting a new benchmark for safety in intelligent vehicles.

Download Free sample to learn more about this report.

Segmentation Analysis

By Sensor Type

Faster and Clearer vision generated from Camera Drive Sensor Type Segmental Growth

On the basis of sensor type, the market is classified into radar, LiDAR, camera / vision, ultrasonic, and infrared.

The camera/vision segment is expected to emerge as the leading segment with a 41.72% share in 2026 & anti-collision sensors, as they deliver rich semantic information (lanes, signs, pedestrian posture, and intent) at relatively low cost and compact form factor, enabling broad ADAS roll-out across vehicle segments. Their versatility supporting LDW/LKA, AEB pedestrian detection, traffic-sign recognition, and surround-view makes them the primary sensor in mainstream fitment bundles, accelerating unit volumes and software monetization for OEMs.

Governments and NCAP programs increasingly require camera-based capabilities (including night/pedestrian test protocols), pushing manufacturers to standardize camera stacks across model lines; this regulatory pressure, plus OEM preferences for camera-centric solutions, has driven high camera penetration in new vehicles, while industry debates (camera-only vs. LiDAR fusion) and recent supplier innovations keep improving accuracy and model robustness. Recent industry coverage highlights intense innovation and market focus on camera AI stacks and production scaling, reinforcing cameras’ role in growing overall anti-collision sensor revenues and software service opportunities.

To know how our report can help streamline your business, Speak to Analyst

By Function

Increasing Mandation and Standardization of Autonomous Emergency Braking (AEB) due to its Highly Responsive Rate Drives Segmental Demand

In terms of function, the market is categorized into autonomous emergency braking (AEB), adaptive cruise control (ACC), blind spot detection (BSD), lane departure warning / lane keeping assist (LDW / LKA), and parking assistance.

AEB leads anti-collision functional adoption as it directly prevents high-frequency crash types and is increasingly mandated or incentivized by regulators, creating rapid standardization across new vehicles & growing with a share of 32.14% in 2026. Evidence from government and safety bodies shows AEB cuts front-to-rear crashes roughly by half and reduces pedestrian crash risk by about a quarter, establishing clear safety ROI for OEMs and fleet operators; those quantitative benefits have underpinned regulatory moves such as recent NHTSA rulemaking and NCAP advancements that require robust AEB and pedestrian-AEB performance (including dark-condition testing). News reports and manufacturer statements show accelerated AEB software updates and recalls to meet evolving standards, while suppliers scale sensor fusion and compute to meet new validation requirements. This convergent pressure pushes AEB from premium to mainstream, driving the largest slice of anti-collision systems shipped and catalyzing related sensor (camera/radar) demand.

By Vehicle Type

Larger share of production makes Hatchback/Sedan to Drive Segment Growth

Based on vehicle type, the market is segmented into Hatchback/Sedan, SUV, LCV, and HCV.

Hatchbacks and sedans dominate global anti-collision sensor volumes as they represent the largest share of passenger car production in many markets. They are the primary targets for rapid ADAS diffusion driven by regulation and affordability. High production volumes, global car production exceeded around 93 million vehicles recently, with major shares produced in China, the U.S., and Japan, meaning even modest per-vehicle fitment rates translate to large absolute sensor unit demand; OEMs therefore prioritize camera+radar bundles for high-volume compact models to capture scale economies. Fleet renewal, urbanization, and consumer demand for safety features in entry segments have prompted tier-1s to offer cost-optimized sensor packages for hatchbacks/sedans, increasing shipment volumes and aftermarket retrofit interest. Recent industry and trade updates confirm growing production momentum in passenger cars and targeted supplier offerings for compact platforms, sustaining this vehicle class as the principal growth engine for global anti-collision sensor shipments. The SUV segment is set to dominate the market, holding 37.42% share in 2026.

By Range

Effective Range and Reasonable Cost for Majority of Urban and Highway Vehicles Drives Medium-Range (5–60 M) Segmental Growth

Based on the range, the market is classified into short-range (< 5 m), medium-range (5–60 m), and long-range (> 60 m).

Medium-range sensing (5–60 m) is the market’s workhorse as it best balances resolution, range, and cost for the majority of urban and highway anti-collision tasks, blind-spot monitoring, lane-change assist, adaptive cruise control, and mid-speed AEB scenarios. With a share of 50.02% in 2026, Mid-range radar and camera fusion provide reliable lateral and longitudinal tracking at commuter speeds, enabling crucial, timely interventions without the expense or data burden of long-range LiDAR systems. Suppliers are actively optimizing mid-range radar SoCs and imaging stacks for higher resolution and multi-target tracking, and recent product announcements illustrate strong investment into mid-range modules designed for volume production. Industry reporting on new mid-range radar products and semiconductor advances points to accelerating adoption of medium-range solutions across vehicle classes, which in turn drives the bulk of annual sensor unit shipments and the mid-market revenue pool.

ANTI-COLLISION SENSOR MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

ASIA PACIFIC

Asia Pacific Anti-Collision Sensor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 9.95 billion in 2025, capturing 48.26% of the global market share, and is projected to reach USD 12.91 billion in 2026. Asia Pacific dominated the market with a valuation of USD 9.95 billion in 2025 and USD 12.91 billion in 2026. The market is propelled by China’s massive vehicle volumes, aggressive ADAS adoption targets, and fast OEM uptake, making it the single largest, dominating, and fastest-growing regional contributor to global anti-collision sensor demand. Academic and industry projections show steep AEB adoption trajectories in China (single-digit penetration turning to double digits within five years and reaching majority levels by 2030), while recent industry reports highlight dramatic growth in camera installations tens of millions annually as OEMs scale surround-view and front/side camera suites thus benefiting Asia Pacific collision avoidance sensors market size. Rapid EV growth, domestic suppliers cutting LiDAR prices, and expanding local Tier-1 capacity together compress ASPs and drive global unit volumes and innovation diffusion. The Japan market is projected to reach USD 2.21 billion by 2026, the China market is projected to reach USD 6.62 billion by 2026, and the India market is projected to reach USD 1.45 billion by 2026.

NORTH AMERICA

In 2025, North America generated USD 4.5 billion, contributing 21.85% to global market revenue, and is projected to grow to USD 4.96 billion in 2026. North America is characterized by rapid ADAS standardization driven by a mix of regulatory action, detailed model-year penetration data, and strong OEM adoption, which together accelerate anti-collision sensor deployment across vehicle classes. U.S. model-year data show Automatic Emergency Braking (AEB) penetration climbing to roughly the mid-90s percent in recent model years, reflecting near-universal new-vehicle fitment among many makes; U.S. rulemaking now requires AEB on nearly all new light vehicles by 2029, a change estimated to save hundreds of lives annually and prevent tens of thousands of injuries. These dynamics push suppliers to scale radar/camera production and sensor-fusion software. At the same time, OEMs standardize bundles, shortening the time from premium to mainstream and raising unit volumes that substantially bolster global sensor shipments and software monetization.

The U.S. market is driven due to robust model-year penetration datasets and NHTSA’s AEB mandate, driving near-full new-vehicle fitment. With AEB requirements phased through 2029 and strong voluntary deployment beforehand, suppliers face urgent high-volume qualification cycles, and OEMs negotiate nationwide standardization. This regulatory certainty (despite litigation tensions) accelerates domestic sensor sourcing, calibration services, and aftermarket retrofit programs, making the U.S. both a large unit market and a technical proving ground that shapes global product roadmaps. The U.S. market is projected to reach USD 3.97 billion by 2026.

EUROPE

The European market accounted for USD 5.77 billion in 2025, representing 28.02% of the global industry, and is expected to reach USD 6.58 billion in 2026. Europe’s outlook is anchored by harmonized safety mandates, notably the revised General Safety Regulation that made multiple ADAS systems mandatory for new vehicle approvals beginning July 2022, rapidly elevating fitment rates for camera/radar bundles. European Union regulatory clarity reduces certification fragmentation within member states, incentivizes OEMs to adopt standardized sensor suites across platforms, and forces suppliers to meet stringent performance test protocols; this regulatory-driven uniformity yields scale economies and faster ASP declines in the region. Concurrent NCAP advances and national fleet renewal programs further amplify uptake, making Europe's collision avoidance sensors market size a high-density market that sets technical and safety benchmarks, influencing global sensor validation and demand. The UK market is projected to reach USD 1.22 billion by 2026, while the Germany market is projected to reach USD 1.99 billion by 2026.

REST OF THE WORLD

The rest of the world constitutes Latin America, Africa, and the Middle East, adoption lags developed regions due to slower regulatory mandates, longer vehicle replacement cycles, and higher price sensitivity, which constrains immediate standardization of anti-collision sensors. However, rising urbanization, fleet-safety initiatives, and the trickle-down of lower-cost sensor modules are driving incremental uptake; global vehicle production and registration growth (with world production exceeding 90 million vehicles recently) means that even modest penetration gains generate meaningful incremental unit demand. Over time, harmonized standards and cheaper sensor hardware will convert latent demand into concrete shipments, expanding the global market beyond traditional centers.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strong Investment and Technological Leadership by Robert Bosch GmbH Drives Competitive Edge

Robert Bosch GmbH is widely regarded as the leading global supplier of automotive collision avoidance sensors attributed by its long-standing dominance in automotive electronics, deep systems-level integration capabilities, and massive scale across radar, camera, ultrasonic, and sensor-fusion software. Bosch reached leadership through decades of OEM relationships, large R&D investments in radar SoCs and perception stacks, and early commercialization of imaging radar and camera solutions that balance cost, reliability, and regulatory compliance. Its product portfolio spans short- and long-range radar modules, multi-camera systems, ultrasonic arrays, radar SoCs, sensor fusion middleware, and ADAS compute platforms that OEMs adopt as fully integrated bundles, making Bosch the default choice for many high-volume programs and cross-regional rollouts.

Continental is also leading among key players due to its exceptional radar volume, focused investments in high-performance radar imaging, and expansive sensor production footprint; the company recently announced production milestones that underscore its scale in radar sensors. Continental’s ascent rests on strong OEM partnerships, targeted innovation in mid- and long-range radar, and integrated ADAS ECUs and software stacks that enable full vehicle-level safety solutions. Its anti-collision portfolio includes medium- and long-range radar families, camera modules, ultrasonic sensors, LiDAR collaborations, and end-to-end sensor fusion and domain controllers positioning Continental as the second global leader by unit shipments and program content.

LIST OF KEY ANTI-COLLISION SENSOR COMPANIES PROFILED:

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Denso Corporation (Japan)

- Valeo SA (France)

- Aptiv PLC (Ireland)

- ZF Friedrichshafen AG (Germany)

- Magna International Inc. (Canada)

- Hyundai Mobis Co., Ltd. (South Korea)

- Hella GmbH (Germany)

- Mobileye (Israel)

- Veoneer, Inc. (U.S.)

- Hesai Technology (Shanghai, China)

- Sensata Technologies (U.S.)

- Luminar Technologies, Inc. (U.S.)

- Velodyne Lidar, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In September 2025, Valeo signed a partnership with Momenta to establish a comprehensive, long-term, and global partnership to jointly develop advanced mid to high-level Intelligent Assisted Driving and Autonomous Driving products, systems, and solutions, in China and overseas.

- In July 2025, Bosch introduced two new radar SoCs, SX600 and SX601, aimed at enabling advanced driver assistance functions under SAE Level 2+ (e.g., automatic emergency braking, adaptive cruise, and blind-spot detection).

- In April 2025, Mercedes-Benz signed a partnership agreement with Luminar Technologies to develop and integrate its latest LiDAR product. The contract with the German auto giant is the first deal for Luminar's smaller, more efficient Halo LiDAR sensors, and it comes as global automakers race to launch safer self-driving vehicles.

- In October 2023, Koito Manufacturing Co., Ltd. and Denso Corporation signed a contract to develop a system to improve the object recognition rate of vehicle image sensors by coordinating lamps and image sensors, with the aim of improving driving safety at night.

- In September 2025, ZF Friedrichshafen AG presented technologies for software-defined chassis and e-mobility at the IAA Mobility 2025. The Group is already supplying production-ready drives as well as by-wire systems and software for the chassis, and is thus shaping the software-defined electric vehicle of the future.

REPORT COVERAGE

The global anti-collision sensor market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The anti-collision sensor market forecast is a detailed competitive landscape with information on the market share, growing opportunities, and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.44% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Sensor Type

By Function

By Vehicle Type

By Range

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 20.61 Billion in 2025 and is projected to reach USD 78.63 Billion by 2034.

In 2025, the market value stood at USD 9.95 billion.

The anti-collision sensor market growth is expected to exhibit a CAGR of 15.44% during the forecast period of 2026-2034.

The Medium-range (5–60 m) segment led the market in the Range segment.

Rising demand for ADAS & autonomous driving to propel market growth.

Top players including Bosch, Denso, Continental, ZF, and Magna dominate the industry.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 229

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us